So I came across a pretty interesting debate on Facebook recently.

The debate was on whether dividend income retirement is a reliable / safe retirement model.

You know, the idea that you save up $1 million in cash, invest in a 5% dividend yielding portfolio, and retire off the $50,000 a year dividend income.

Can you really rely on the dividend income to support yourself in retirement?

Summarising the debate

It all started with this article from Investment Moats where he argued that the “Dividend Income Retirement Mindset is Not a Good Retirement Risk Management Model”:

He cited 9 reasons why:

- They Based Their Retirement on a Model That Has Little Empirical Evidence

- How do they deal with Income Volatility?

- Trusting that 5-15 Years of Dividend Record Too Much Without Considering the Base Rate – Most Companies Don’t do Well In the Long Run if You Buy and Hold

- It Makes You Focus on Picking Companies with Dividend Payouts

- Too Much Yield Targeting Leading to More Risky Stocks

- Underestimating the Effort Needed to Manage the Portfolio

- Achieving Income Stability and Inflation Adjustment Requires Either Enough Conservativeness or Reducing the Volatility of the Portfolio

- Not Running Out of Money is Not Just About Not Spending Your Capital

- I Hope Your Heirs Want to Manage Your Dividend Portfolio

Difficulty of managing portfolio + Risk that it doesn’t generate enough returns in retirement

You can read his full reasoning if you’re keen (which I suggest you do as I don’t think my summary does it justice – lots of nuance I was not able to fully capture).

But if I were to summarise it, he is citing 2 key problems with dividend investing:

- Difficulty of managing a dividend portfolio

- Potential risk that it doesn’t generate enough returns in retirement

I suppose if you want to be technical this can all be summarised into one point:

That the level of knowledge, effort, and sophistication required to manage a dividend portfolio to sustain yourself indefinitely in retirement is not easy.

And if you fail on this, you might not have enough money in retirement.

Which would then mean your options are to either (a) spend less money in retirement, or (b) find a way to make more money in retirement.

Both are not ideal for a retiree.

It’s a very interesting debate, and I wanted to share some views on this.

And hopefully it might help you guys in your investment journey.

My Personal Views on Dividend Income investing as a retirement model

2 key views from me:

- Past 40 years was very beneficial for investing – that may not hold true the next 40 years

- Every generation needs to build wealth their own way, don’t copy your parents/grandparents exactly

Past 40 years was very beneficial for investing – that may not hold true the next 40 years

Let’s take a step back.

The past 40 years since 1980, was a period of secular falling interest rates.

Look at the 40 year chart of the US Fed Funds Rate since 1980.

Interest rates basically went from 20% in 1980 to 0% in 2020.

Now if you’re investing in stocks – what is the singular best thing that can happen for you as an investor?

Declining Interest Rates.

Or to put in in another way, the past 40 years was basically just one big party for financial markets (leaving aside the occasional market crash after the Feds tried to raise interest rates).

What are you trying to say FH?

I suppose what I’m trying to say.

Is that investing has gotten very popular after a 40 year period of the best possible financial circumstances for stocks.

You have all these stories of people who invested their income for the past 40 years in a diversified stock portfolio, and they are retiring with million.

Backtest any portfolio today, and you’ll be looking at a 40 year period of declining interest rates supercharging investment returns.

Yeah well, that’s what happens when interest rates go from 20% to 0% over 40 years.

But will the same returns hold true going forward?

But what if you’re a fresh investor today.

What if you’re a 25 year old fresh graduate, who will be investing your paycheck for the next 40 years into the same markets.

What if you’re a 55 year old with a million in cash, looking to invest in a dividend portfolio for the next 30 years?

Are you going to see the same returns the previous generation did?

Zoom in closer to the chart below, and you’ll find that for the first time in 40 years, the Feds had to hike interest rates higher this cycle (2023), than they did the previous cycle (2020).

In plain English – the 40 year downtrend in interest rates is broken.

Every generation needs to build wealth their own way, don’t copy your parents/grandparents exactly

Which brings me to my next point.

Every generation builds wealth in their own way.

Every generation has a specific “flavour” of investing that worked for them.

You know how people of a certain generation will swear by real estate as the only form of “real” investment?

While people of another generation will tell you stories of how they scrimped and saved to put every single paycheck into REITs / Dividend stocks and are now living off the dividend income?

Yes, that is what worked for them.

But what worked for them, may not necessarily work for you.

So yes, we all know of people who built their wealth via real estate, REITs or stocks like DBS.

And for those who did, well done.

But for those who haven’t, and are still in the process of wealth building.

The question to you here is this.

Dividend investing is popular because it did well the past 40 years.

Does it do well the next 40 years?

Even if you think the answer is yes, is this something you are prepared to bet your retirement future on?

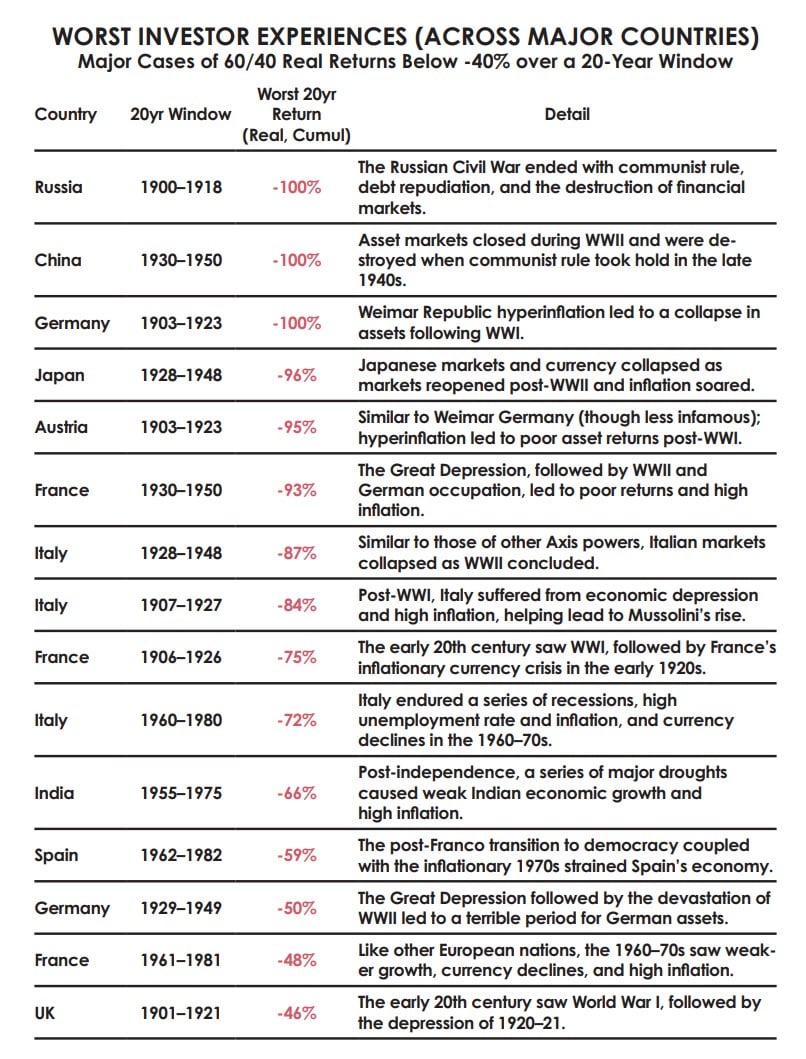

The chart below shows the worst investment returns over the past 100 years.

There are certain countries where a diversified 60/40 portfolio would have led to complete losses over a 20 year period.

Now nobody is saying this might play out going forward.

I’m saying that when you invest your retirement funds, you need to at least be aware of this possibility.

How would I do it – Invest in a dividend portfolio for retirement?

So what is the solution?

How I would approach dividend investing today – if I were investing for retirement income?

3 points:

- Approach dividend investing like you would investing – manage and diversify your portfolio

- Dividend Growth Investing

- Margin of safety in Portfolio Size (Proper Asset Allocation)

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Approach dividend investing like you would investing – manage and diversify your portfolio

I think the underlying problem is that many people think of dividend investing as buying a bunch of dividend stocks.

Leaving them alone for the next 40 years.

And getting very rich at the end.

That may work if you’re buying a diversified ETF like the S&P500 in a period of secular declining interest rates.

But if you’re buying 5 dividend stocks and 5 REITs listed on the SGX, I’m not so sure how that approach works out.

So what I would say is this.

Dividend investing in my view, is perfectly viable as a retirement strategy.

But just buying a bunch of 10 stocks and expecting to live off the dividend income for the next 40 years without making any changes to the portfolio.

May not be so workable.

I mean it’s workable if you’re a master stock picker like Warren Buffet.

But for lesser mortals like us, I think at the very least you need to be prepared to actively manage the portfolio.

If individual stocks start to perform poorly, you need to know when to sell, and what to replace them with.

And you need to diversify.

Across industries, and across countries.

And position size well – the loss of any one position should not wipe out your portfolio.

In other words, you need to actually manage your dividend portfolio.

Dividend Growth Investing

From Investopedia:

A dividend aristocrat is a company that not only consistently pays a dividend to shareholders but annually increases the size of its payout.

A company will be considered a dividend aristocrat if it raises its dividends consistently for at least the past 25 years.

If you wanted to stock pick a dividend portfolio today, as a retirement portfolio.

I would say you want to pick as much future dividend aristocrats as you can.

This means instead of buying a company that has raised its dividends for the past 25 years.

You buy a company that will raise its dividend for the next 25 years.

The problem though, is that most dividend investors get it the other way around.

They focus obsessively on getting a high dividend yield.

But the problem is that the high dividend yield usually comes at a cost.

It usually means a company with a mature business model, with a high dividend payout ratio.

And if the core business goes into decline (as it inevitably will with a mature business model), there is a real risk of dividend cut and capital loss.

Instead of buying companies that raise dividends over the next 25 years, they buy companies that cut dividends.

So yes, dividend stock investing definitely works, but you need to pick the right stocks.

Dividend yield is fundamentally backward looking in nature.

Look at the future, buy companies that can raise its dividend year after year for the next few decades.

Margin of safety in Portfolio Size (Proper Asset Allocation)

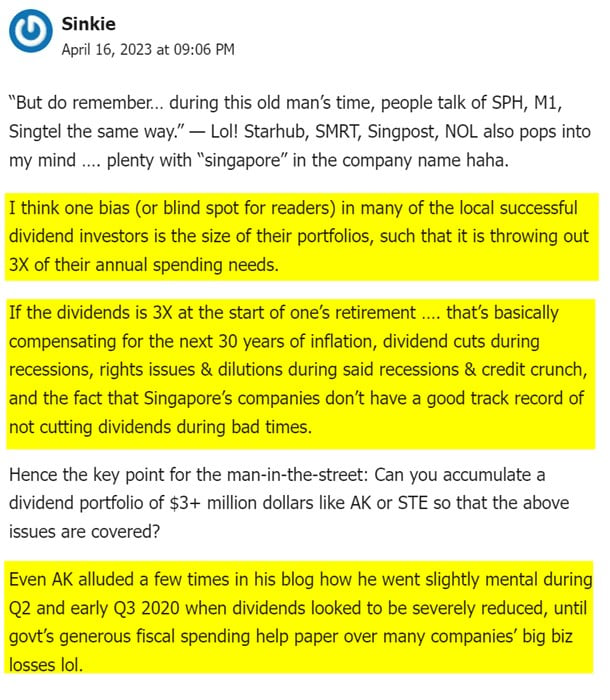

There was a comment on the Investment Moats article that I thought was absolute gold:

It is the concept of margin of safety.

If you need to spend $50,000 a year.

And you build a dividend portfolio diversified across countries and asset classes that throws up $500,000 a year.

Nobody is doubting for a second that you have a very good chance of retiring comfortably.

But if you need to spend $100,000 a year.

And your dividend portfolio of 5 stocks / REITs throws up $110,000 a year.

Then you’re cutting it pretty close.

So don’t forget about the margin of safety when building a retirement dividend portfolio.

If you’re sophisticated and comfortable in your ability to manage the portfolio to generate higher returns, maybe you can cut it finer.

If you’re not so comfortable in your ability to manage the portfolio, then maybe you want to buffer in a bigger margin of safety.

Closing Thoughts: Dividend Income Investing is a very viable strategy

So just to be clear on my views.

I think Dividend Income Investing can definitely be a viable strategy in retirement.

But for the record – I do agree with Investment Moats that many investors are underestimating how difficult it is to manage a dividend portfolio in retirement.

You do need to put real thought and effort into it.

You need to buy the right stocks, diversify across industries and countries, and position size well.

And even then you probably want to buffer in a sufficient margin of safety, such that you have room to breathe if you take investment losses or get hit by dividend cuts (eg. if March 2020 repeats).

And even then, I’m going to venture out on a limb and say that I think the next 40 years of investing.

It’s going to be a lot harder (and very different) from the past 40 years.

I think we’re going into a period of higher structural inflation, and higher nominal interest rates.

All while geopolitical conflict between the US and China continues to play out, and the world coalesces around these 2 superpowers.

But who are we kidding.

I love every second of investing, and I plan to be doing it until the day I die.

So how exactly to manage our portfolio in the next few decades, let’s figure it out together.

This article is written on 21 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

What Kyith doesn’t say, is that in a crash, ETFs will also crash, not just dividends cut. Retirees who see their diversified ETFs crash will also need to cut their spending to keep their retirement on track.

Of course, the good thing about Kyith is that he’s not a sellout, he is pure of heart. No investment courses, no tie-ups with banks. His blind spot is, he doesn’t take well to any criticism – an autocrat.

HI Overdraft, thanks for the comment. I would like to think that term autocrat might not be very appropriate. I don’t rule over your life and you are free to choose what you want.

But I do have strong views, and sometimes, my views are stronger either because the topic is important enough for me, or that I kind of know what I am talking about more than I have imposter syndrome about it.

Afterall, the post is a response to a group of reader’s question why I would say I moved away from that mindset and just flushing out my thoughts.

What is my motivation? I want a sensible and practical method that work. I moved away because I find the reasons to be less practical personally for myself.

If you find that it works for you even at 80 or 90 years old, then you can continue with it. Afterall, it is your plan.

But I do want to share what I learn with people.

The part also is about how much I know. I don’t profess I know everything, and there are a lot of things fill with uncertainties, which is why I feel a dividend model is less practical because for many, they came from a planning angle that they will go through a 20, 30-year sequence that is lucky enough.

I prefer to plan with a model where we can see the extreme unlucky angle better and factor that into my planning.

Regarding the comment that diversified ETFs crash and cut spending, I think if you read the research where the model is based on, it does factor that in. The model in a way, is a model trying say there is a spectrum of outcome, that you can be very lucky, or very unlucky and consider them in your planning.

So it does factor in that situation.

I would volunteer a piece of information, it is not the crash that kills retirement usually. That may be easier to handle even with a dividend portfolio.

The issue tends to be very high inflation where the markets didn’t crash much nominally but your spending goes up too fast.

I learn over time, through talking to people, that people don’t read or go into that methodology well enough to debate on the same level.

It is true I don’t take well to criticism.

If you say “Kyith you are stupid.” Do you think I will take well to that? Of course I will be infurarated.

But sometimes we have to separate whether i disagree with things because i am just being an idiot and whether there is a certain basis to what I am talking about.

If it helps – I thought some of the comments by Chris (on Facebook) were a bit uncalled for.

But hey, it is what it is.

Keep up the writing, don’t let him grind you down!

ok I found that FB group. spicy!

I think it is difficult to summarize my points because the reason why I shifted away is because planning for income is just more complex than just one or two points. Perhaps the very short summary is that there needs to be more consideration and if you consider more, a person may begin to see the short comings.

For those that can accept, they can go ahead with dividend investing during retirement. For those that cannot, they have to find another method.

I think you explain it well but I think the way you position may not be the right framing. I moved towards a model that consider more the spectrum of outcome rather than assume only a few good outcomes so that I can view things better. It also becomes more conservative.

The issue is I cannot see the spectrum of outcome in retirement with the dividend model with the limited data I have. So many times, I am basing on hope that the plan I drawn up in my head works.

Hi Kyith,

Thanks for sharing your thoughts.

Yes I agree that your 9 points were not easy to summarise. I tried my best to summarise for the sake of the article, but there were a lot of nuances I could not capture. I will add a note that readers should read your full post for the fuller insight.

Also to add that after I wrote this piece, it did help me to crystallise a lot of thoughts further.

I think the problem is that a lot of the problems we may be raising on income investing did not exist the past 20 – 30 years (which was a low inflation climate for example). So it may not be easy for an income investor today to imagine the full range of possibilities that can arise to derail a dividend portfolio.

Take a period of sustained inflation and currency depreciation for example. Someone from Brazil/Argentina (no offence) might appreciate that problem a lot better than I could as a Singapore based investor. So even I don’t profess to be able to truly appreciate the problems of an income portfolio over a multi decade period.

In any case, great debate, and thanks for putting the piece out there like you did. I enjoyed reading your article and the follow up piece.

Hi Kyith,

I really shouldn’t have said autocrat, real dick move ???? in light of the heated responses you have suffered through. Let me withdraw that and say once again, your strengths are 1. Quantitative 2. Purity of purpose.

If you are interested, there are data based studies on retirement funded by dividends. Jeremy Siegel of Wharton, Charles Asness and Jan Holman. In historical data, dividends comprised 52% of total returns and were more steady than the usual capital appreciation.

Hi Overdraft, thanks for pointing me towards that. I think even before this, I thought of taking some data and do certain sequence just to see how that flush out.

Dividends as a group tend to be more steady. That I agree. but it is whether as an aggregate how does it flow with inflation that may be something that I wish to appreciate more.

Hi FH,

The Covid pandemic was the latest reminder to us not to be fully dependent on the dividend and rental incomes. Thats why we have “relegated” the above two passive income sources to “bonus” taps.

For me at least, I see that the human asset (myself) is the best income generating asset. Unfortunately the reality is that the human asset will eventually become a liability one day (when we retire). Instead of generating income, it will only be spending money.

So I have been preparing for this eventuality for a long time. To borrow the term (income taps) from the late CW, we have been building up our income taps as below. We ranked our income taps according to their stability / dependability or reliability.

Gold taps for income sources that are most stable / dependable. Our two Gold Taps are the yearly interests from our OA&SA, and the payout from CPF Life.

Silver taps for the next most stable / dependable. They are our SRS savings and our Medisave Account (MA).

Bonus taps for those not so stable / dependable sources ie our dividend and rental income sources.

Below is how the income taps come into play (combined for couple) :

2023 (we are 62 currently)

Gold Tap 1 (OA & SA interest) : $68K pa

(2022 interest was $65K)

Silver Tap 1 (SRS drawdown) : $42.4K pa

(Drawdown over 10 years)

Bonus Tap 1 (Dividends) : $88K pa

(2022 dividend = $88K)

Bonus Tap 2 (rental) : $42K pa

(2022 rental = $39.2K)

2031 (70 yo)

Gold Tap 1 (OA & SA interest) : $68K pa

Gold Tap 2 (CPF Life payout) : $72.2K pa

Silver Tap 1 (SRS drawdown) : $42.4K pa

(Drawdown over 10 years)

Bonus Tap 1 (Dividends) : $88K pa

Bonus Tap 2 (rental) : $42K pa

The SRS tap will stop in 2032 after 10 years.

We planned our retirement lifestyle based only on our gold taps :

Gold tap 1 (OA & SA interest) : $68K pa

Gold tap 2 (CPF Life payout) : $72.2K pa (starts at 70)

The incomes from the Silver tap, the bonus taps (dividends & rental) are bonuses to us. We will use them to pamper ourselves, buy a car, go for long holidays, gifting, reinvesting, etc…but we can live without them. Also if our bonus taps perform well year after year, we may defer tapping on our Gold taps and let them compound further.

I am still working, so all the dividends and rentals collected are reinvested yearly to grow the dividends further. Interests earned in CPF stay in CPF to compound.

For details on how we built up our income taps, please visit : https://t.me/CPF_Tree

Amazing comment Mysecretinvestment.

For someone who has put this much though into a dividend strategy, I don’t doubt for a second that it can be absolutely workable for you.

I really like how you plan your spending around the more “stable” sources of income only. And use the less stable sources of income as a bonus, so even if it doesn’t come in your quality of life would not be impacted.

I think that’s a perfect way to approach dividend investing into retirement.

Dear Mysecretinvestment,

Very impress by your gold tap 1 ability to give you $65K interest per annum. Very well done.

Most folks use their OA to pay for their housing loan and will have difficulty accumulating sufficient principal sum in OA+SA to get $65K interest per annum when they hit 62 year old.