For those of you who are keen to top up your Supplementary Retirement Scheme (SRS) – don’t forget to top up by 31 December 2022 if you want to enjoy the tax relief.

I wrote a full guide to SRS recently, do check it out if you are keen.

But in this article I wanted to discuss something else.

For those who don’t plan on using your Supplementary Retirement Scheme – you should still open one and top up $1 into your SRS account.

Why you should top up $1 into your SRS Account

The simple reason why – is that the Statutory Retirement Age for purposes of your SRS account is locked in on the day you make your first SRS contribution

Before 1 July 2022, it was 62.

After 1 July 2022, it went up to 63, and who knows it may go up in future.

So by opening an SRS Account and topping up $1 today, you’re protected against any future changes to the Statutory Retirement Age for your SRS Account.

I extract the section from the IRAS website below, emphasis mine:

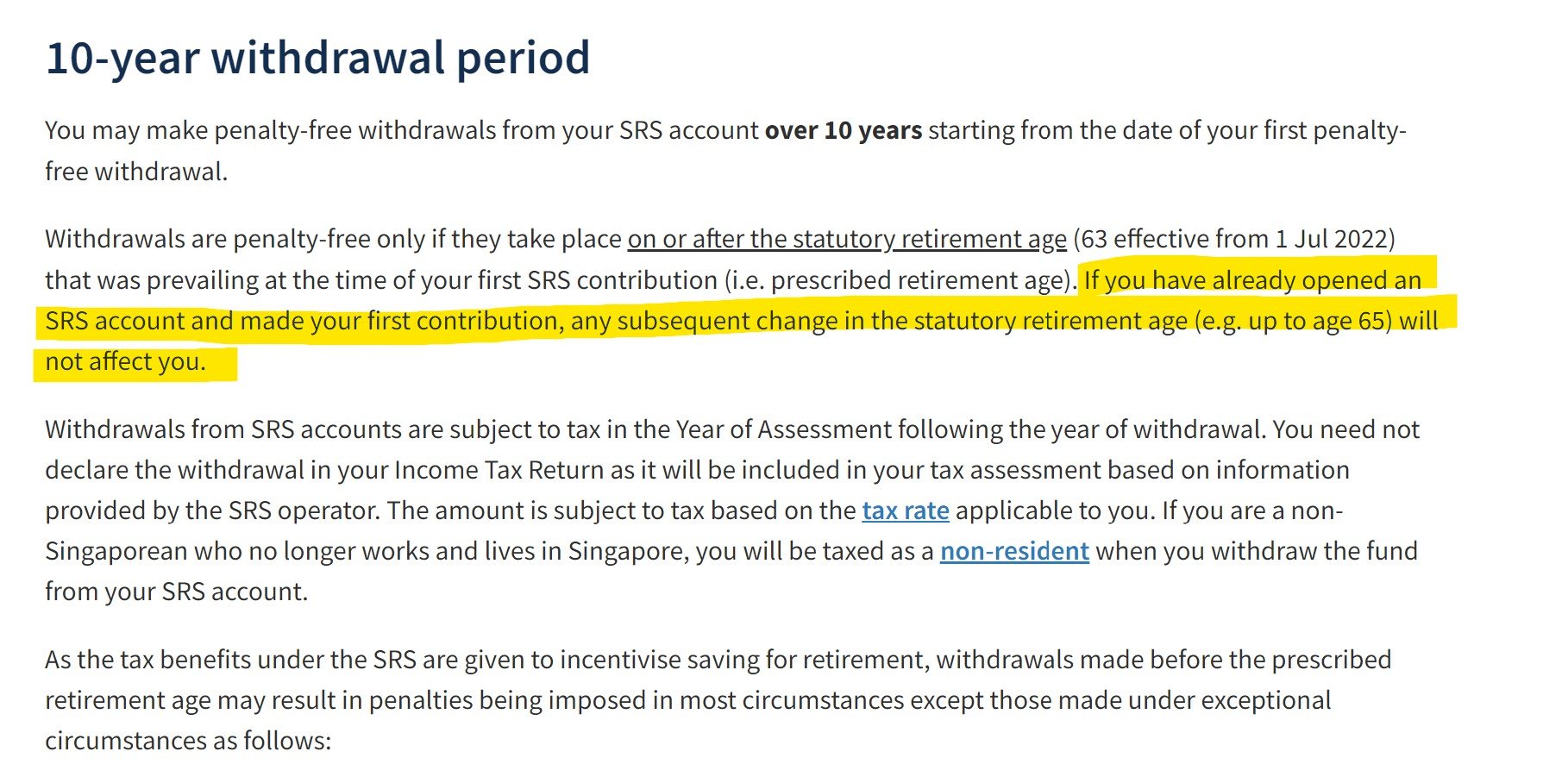

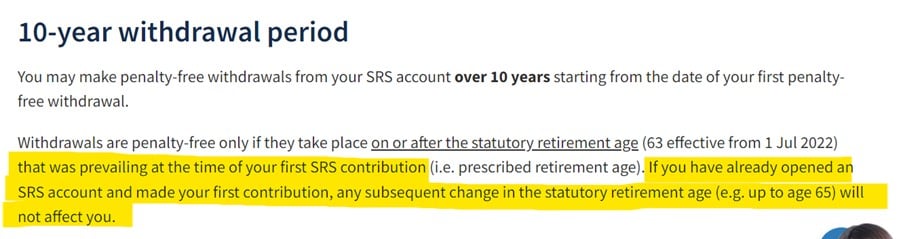

“You may make penalty-free withdrawals from your SRS account over 10 years starting from the date of your first penalty-free withdrawal.

Withdrawals are penalty-free only if they take place on or after the statutory retirement age (63 effective from 1 Jul 2022) that was prevailing at the time of your first SRS contribution (i.e. prescribed retirement age). If you have already opened an SRS account and made your first contribution, any subsequent change in the statutory retirement age (e.g. up to age 65) will not affect you.“

I mean… unless they change the law on how the SRS Account works of course.

But given that you can open the account online in 5 minutes tops, and it’s just $1, I do suggest doing this.

It’s low effort, and who knows what it may protect you from in the future!

More on the SRS Account, and exactly what are this implications of this, below!

Basics: What is Supplementary Retirement Scheme (SRS)?

From the IRAS website, emphasis mine:

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage individuals to save for retirement, over and above their CPF savings.

Contributions to SRS are eligible for tax relief.

Investment returns are tax-free before withdrawal and only 50% of the withdrawals from SRS are taxable at retirement.

What is the benefit of Supplementary Retirement Scheme (SRS)?

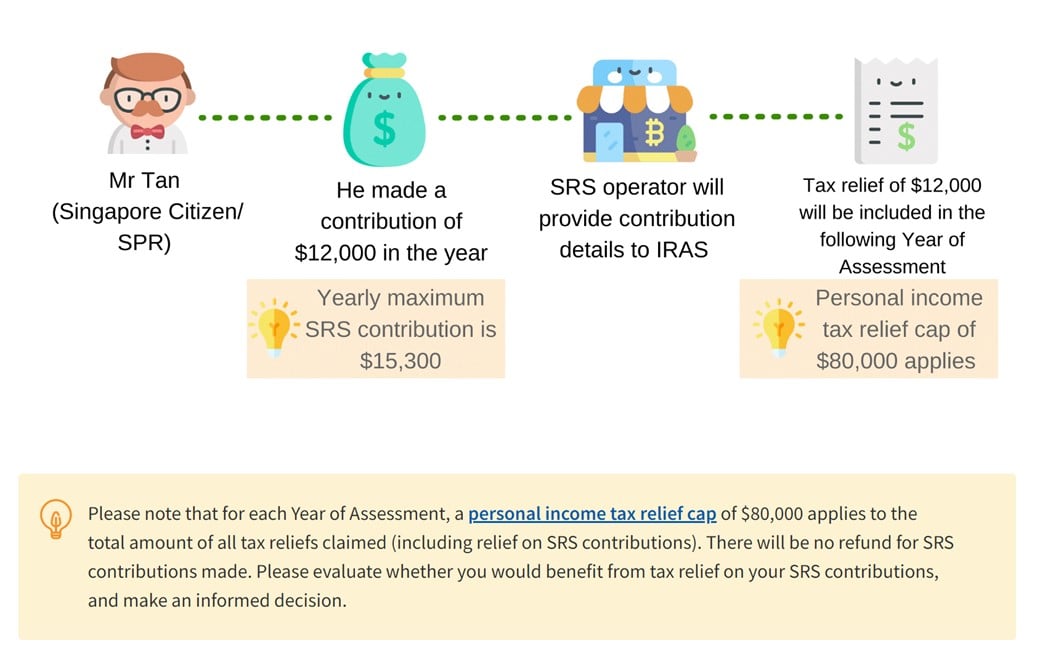

The main benefit of SRS – Income Tax Relief.

Basically, Singapore Citizens / PRs can top up $15,300 a year into SRS, and the amount topped up is fully exempt from income tax.

Yes – you pay absolutely no income tax on the amount that goes into your SRS account that year.

What is the drawback to using Supplementary Retirement Scheme (SRS) Account?

SRS is not without its drawbacks though.

The main limitation – is liquidity.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

If you withdraw before statutory retirement age (63), you need to pay tax on 100% of the amount withdrawn + 5% penalty

If you want to withdraw any amount from your SRS Account before statutory retirement age, you need to pay:

- Income Tax on 100% of the amount withdrawn (based on your income tax bracket)

- An additional 5% penalty on the amount withdrawn

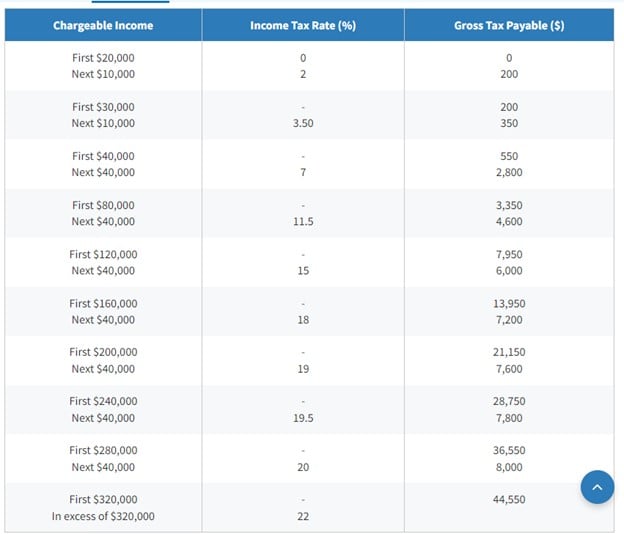

To give an example, let’s say you’re in the $120,000 tax bracket.

And you’re a bit tight on cash, so you withdraw $10,000 from your SRS account that year.

You need to pay:

- Income Tax on 100% of the amount withdrawn – 15%

- An additional 5% penalty on the amount withdrawn – 5%

So in total, you pay a 20% tax, or $2,000, on the $10,000 withdrawn.

In a way you can think of SRS as a liquidity tax.

You’re not banned from using the money, you just need to pay a penalty if you want to use it before statutory retirement age.

If you withdraw after statutory retirement age, you only pay tax on 50% of the withdrawal amount (spread over 10 years)

If you do withdraw from your SRS account after statutory retirement age though, then there is no penalty fee.

In that case, you only pay income tax on 50% of the withdrawal amount.

At this point though, you should not be earning significant income anymore, so the income tax is very low.

Or at least that’s how it should work in theory.

So to give an example.

Imagine you retire at 63, and your income drops to zero.

Then you withdraw $40,000 from SRS that year.

You only pay income tax on 50% of that – which is $20,000.

And the first $20,000 of income pays 0% tax, so you pay absolutely no tax on the withdrawal from your Supplementary Retirement Scheme (SRS) account.

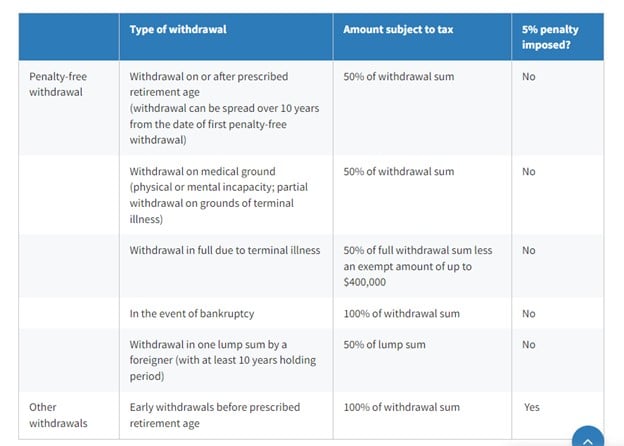

There are other situations where you can withdraw the money, for example on medical grounds, or terminal illness.

I set out the screenshot below for your reference.

Note: Statutory Retirement Age prevailing when you topped up the SRS Account

Just a sidenote that the Statutory Retirement Age for purposes of SRS withdrawal, is the Statutory Retirement Age that was prevailing at the time of your first SRS contribution.

In plain English, this means when you first top up your SRS account, you lock in the Statutory Retirement Age on that date.

Before 1 July 2022, it was 62.

After 1 July 2022, it went up to 63, and who knows it may go up in future.

So even if you don’t plan to use the SRS account, you really should just open one and top up $1 into it today.

This helps you lock in the Statutory Retirement Age for your SRS account, just in case you want to use it in future.

SRS Accounts can be opened online in just a few minutes, so there’s really no reason to be lazy about this.

Just top up $1 into your SRS Account to lock in the statutory retirement age (for your SRS account)…

Long story short, it’s worth it to open an SRS Account and top up $1, even if you don’t plan on using it.

You can do the entire account opening online (takes no more than 5 minutes – less if you’re tech savvy).

And frankly it’s just $1.

It’s possible that the rules may change in future to have retroactive effect.

But who knows, it also might not.

Whatever the case, given that it’s quite a low effort move, I do think it’s worth it just to get it done and lock in your Statutory Retirement Age for the SRS Account!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!