After last week’s article on Singapore Savings Bonds, I received a very interesting question:

“With central banks raising interest rates across the globe are we likely to see a 3% (year 1) Singapore Savings Bond?

Are there chances that we may see an average of a 5% SSB?”

Now the answer is not so straightforward because it requires an understanding of how short term interest rates will move in the months ahead.

And because of how the Singapore Savings Bond curve is derived, it also requires a prediction on long term interest rates.

The more I thought about it, the more I found this to be quite an intriguing question.

So I wanted to pen an article to share some quick thoughts.

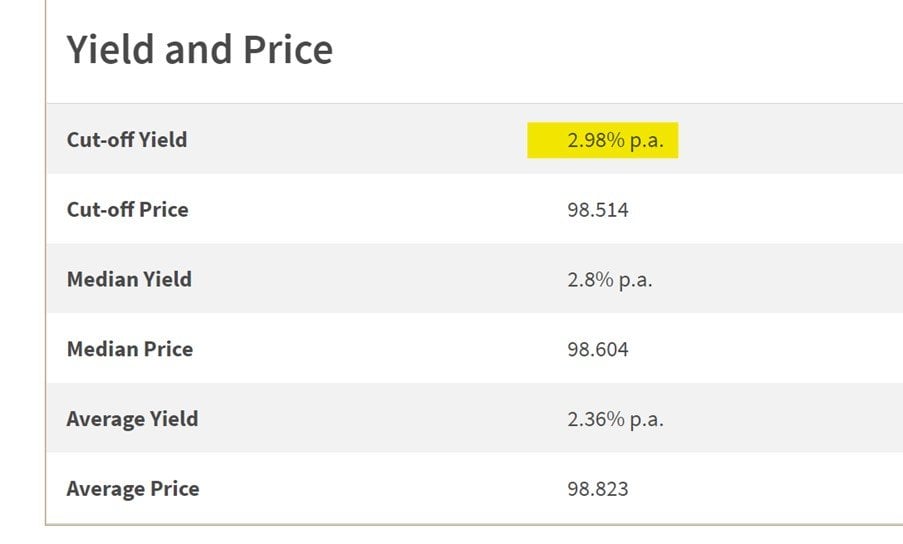

T-Bills (6 months) already yield close to 3%

First off – T-Bills, basically Singapore Government Securities of a short term tenure – already yield close to 3%.

Here’s the latest T-Bills auction for 6-month tenure, they closed at 2.98%.

In other words, you can lend money to the Singapore government, completely risk free for a period of 6 months, and the government pays you interest at 2.98% per annum.

The problem though, as shared in last week’s article, is that T-Bills cannot be easily sold or redeemed prior to maturity.

Which means Singapore Savings Bonds are still a superior product for retail investors who want the liquidity.

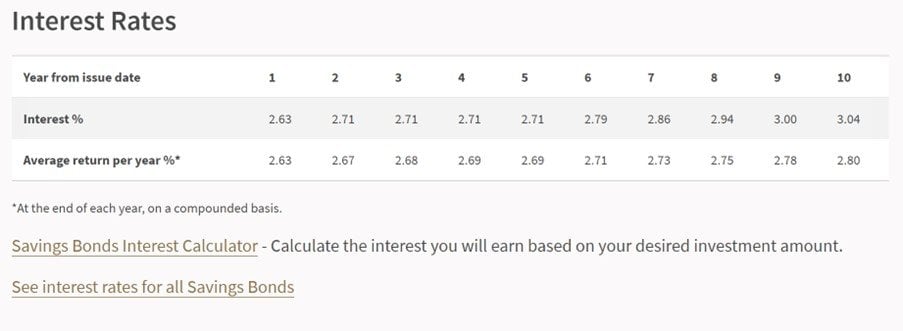

Why don’t Singapore Savings Bonds yield 3% first year?

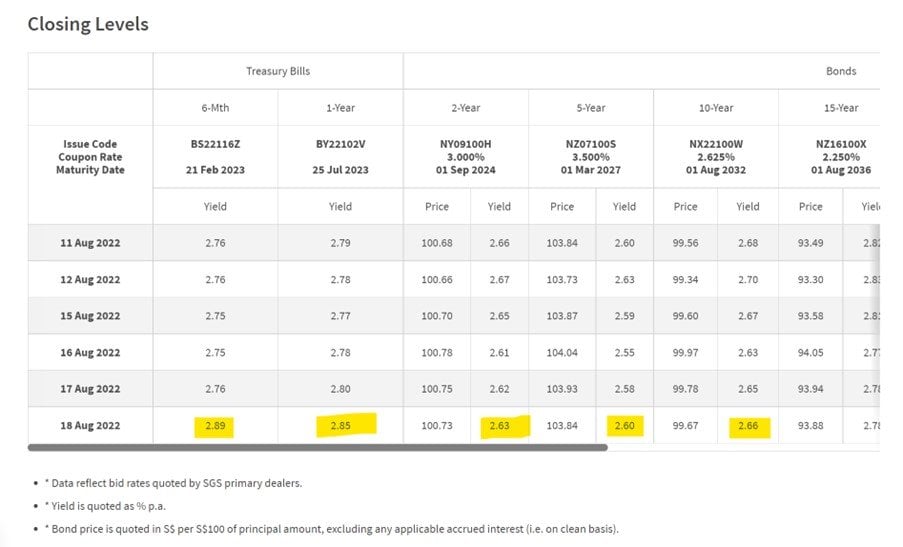

Here’s the latest yields on the Singapore Savings Bonds:

You might ask why is the 1 year yield only 2.63%, when a similar T-Bill is going for almost 3%?

The answer is because of a weird quality of the Singapore Savings Bonds, where the short term interest rate on the Singapore Savings Bonds, cannot be higher than the long term interest rates.

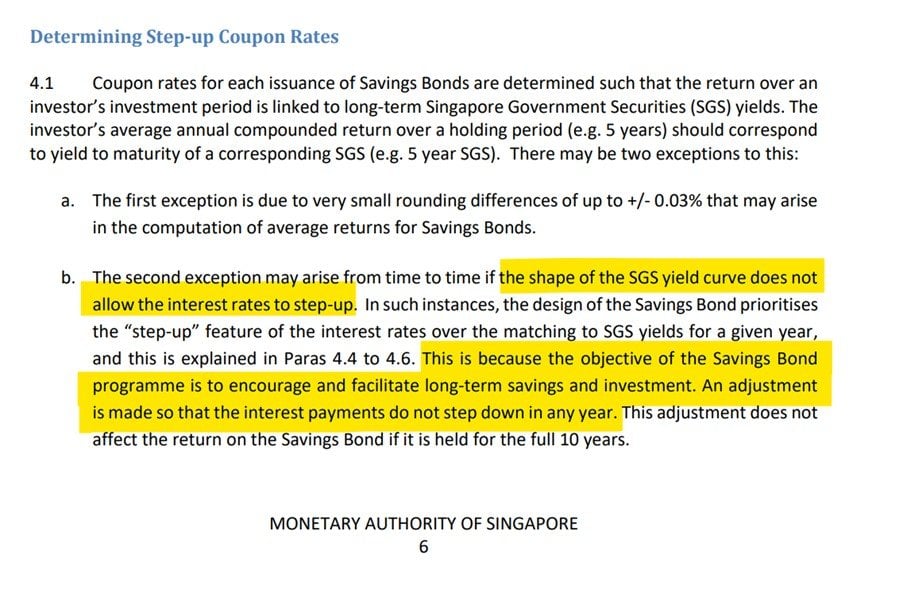

Here’s the extract from the Singapore Savings Bonds Technical Specifications:

In text form:

The second exception may arise from time to time if the shape of the SGS yield curve does not allow the interest rates to step-up. In such instances, the design of the Savings Bond prioritises the “step-up” feature of the interest rates over the matching to SGS yields for a given year, and this is explained in Paras 4.4 to 4.6. This is because the objective of the Savings Bond programme is to encourage and facilitate long-term savings and investment. An adjustment is made so that the interest payments do not step down in any year. This adjustment does not affect the return on the Savings Bond if it is held for the full 10 years.

Or in plain English – the government wants it such that the interest rates on the Singapore Savings Bonds go up every year.

The interest rate if you hold the Singapore Savings Bonds for 1 year, can never be higher than if you hold it for the full 10 years.

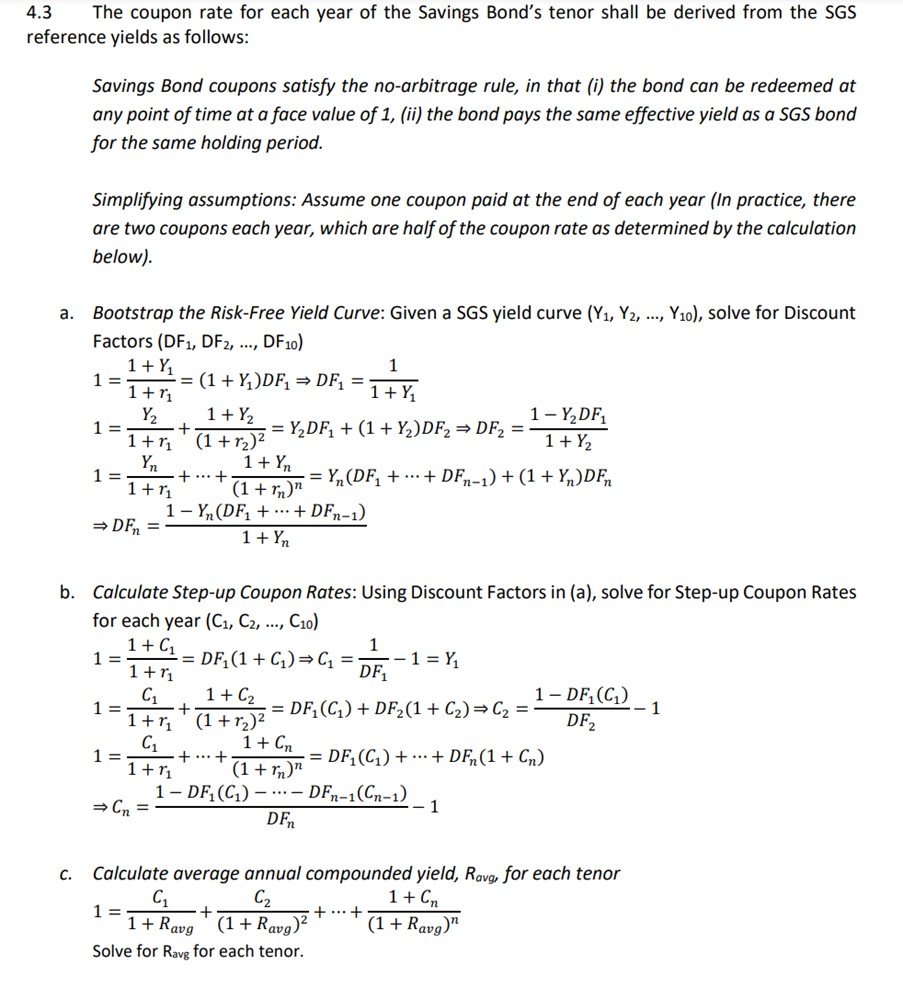

How are Singapore Savings Bonds Yields derived?

For the more mathematically inclined, here is the full formula for how MAS smooths out the Singapore Savings Bonds curve to achieve this step up:

Latest Singapore Government Security Yields

And this is exactly what is going on now.

With the latest Singapore Government Security Yields, you can see that the 6 month interest rates at 2.89% are higher than the 10 year interest rates at 2.66%.

And because of this feature above, 1 year yields cannot be allowed to be higher than 10 year yields on the Singapore Savings Bonds.

So they are artificially smoothed out, resulting in a Singapore Savings Bond yield that looks like this.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will Singapore Savings Bonds yield 3% (first year) by Dec 2022?

So to answer this question, we need to know 2 things:

- Where will Short Term Interest Rates be by Dec 2022?

- Where will Long Term Interest Rates be by Dec 2022?

Where will Short Term Interest Rates be by Dec 2022?

This one is easy.

MAS does not control SGD interest rates because we control the SGD foreign exchange rate, and we have free movement of capital (you can google the Impossible Trinity if you’re curious to learn more about this).

This means that SGD interest rates track global interest rates – which are dominated by USD interest rates (as the global reserve currency).

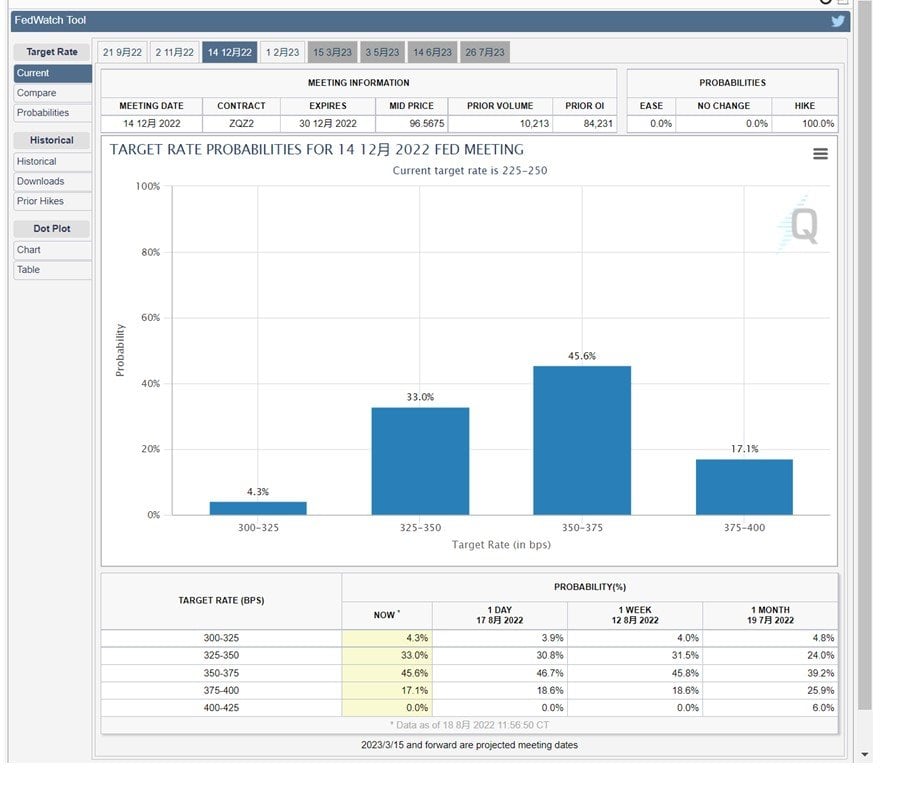

So to determine where short term interest rates for SGD will be by Dec 2022, you need to look at what the US Federal Reserve (US Central Bank will do).

And here it’s pretty obvious as well, because Jerome Powell has told us – They will be raising to 3.5% by Dec 2022.

So by Dec 2022, you’ll probably see the 6 month T-Bill at close to 3.25-3.5%.

Where will Long Term Interest Rates be by Dec 2022?

But remember, to predict the short term interest rate on the Singapore Savings Bonds, you also need to know where long term interest rates are.

Long Term Interest Rates (10 Year) are not so straightforward.

The US Federal Reserve controls short term interest rates via the Fed Funds rates.

But where long term interest rates go, are at the mercy of the market.

They reflect among other things, market expectations as to the path of future rate hikes, possibility of a recession, and the path of inflation.

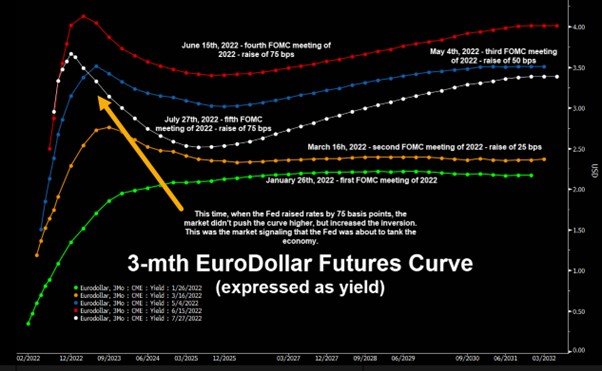

You can get some clues from the shape of the Eurodollar futures curves (which tells you market expectations as to how short-term US interest rates will evolve going forward).

And here it is very interesting – because the market is expecting a very rapid rate of interest rate increases to 3.5% over the next 6 months, but it thinks that in 2023 interest rates will get cut:

Because of this, 10 year interest rates has not gone up significantly, and is sitting below the 6 month – 1 year interest rates, like you see with the SGS yields.

So FH… Will Singapore Savings Bonds yield 3% (first year) by Dec 2022?

I’ve shared a lot of background on how Singapore Savings Bonds work and how interest rates curves work.

But I know some of you only want the answer.

So let me try to answer it simply.

Will Singapore Savings Bonds yield 3% (first year) by Dec 2022?

It will depend on the long end of the interest rate curve (10 year interest rates).

But my view – I think there is a very good chance it will.

The short end is definitely going up, and I think the long end will as well once the market realises the economy is more resilient than expected.

Will Singapore Savings Bonds yield 5% (average) by Dec 2022?

This one’s much easier.

For this to happen, the 10 year interest rate needs to yield more than 5%.

I don’t see that happening.

Worst case if inflation gets unhinged and we go higher for longer, I think we may see 4 – 4.5% on the 10 year.

But I find it hard to see it ever going beyond 5% this cycle.

I am applying for Singapore Savings Bonds

Whatever the case, I think Singapore Savings Bonds are one of the best places to be parking cash right now.

The only problem is that allocation is incredibly low, at $9,000 per person last month.

Investors with a lot of spare cash can go with T-Bills which are yielding close to 3%, but do note that you sacrifice the liquidity, because you cannot sell T-Bills before maturity easily.

For me – I’m just applying for Singapore Savings Bonds patiently every month.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try here.

As always, this article is written on 19 Aug 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.