Will there be a market crash in the second half of 2020? What will global demand look like?

We tried to answer this question 1 or 2 months back. My take on it then, was that we’ll see an asymmetric-V recovery in global demand. Or in plain English – demand will fall off a cliff, then it will recover at a slow pace than the fall.

So the recovery to Jan 2020 levels will take longer than the fall.

We’re now in May, so with the benefit of a lot more data, let’s take another stab at this question.

We’ll take the issue step by step, but if all you want is my conclusion, you can skip right to the end.

Reminder: We’re running a Labour Day Promotion for the FH Course and the REITs MasterClass. You get a big discount off the usual price, and a 3 month access to Patron thrown in.

A great way to make good use of your extended circuit breaker!

Find out more here!

Economic Data

Let’s survey the latest data that we have available.

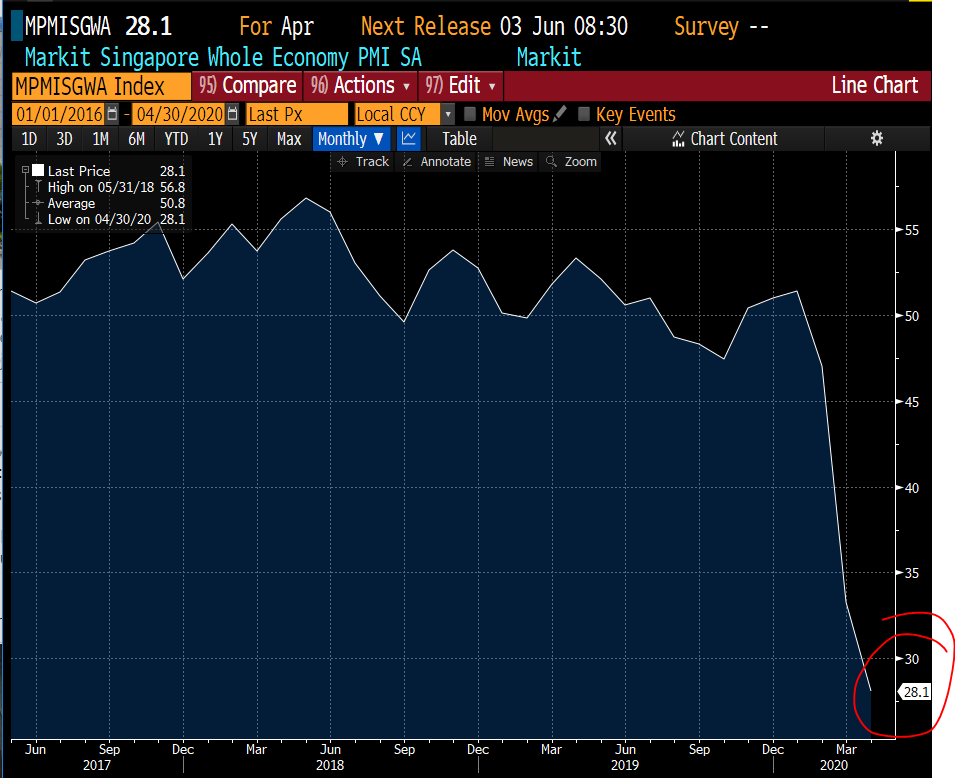

PMI

This is Singapore PMI, which has fallen off a cliff.

Industry Breakdown

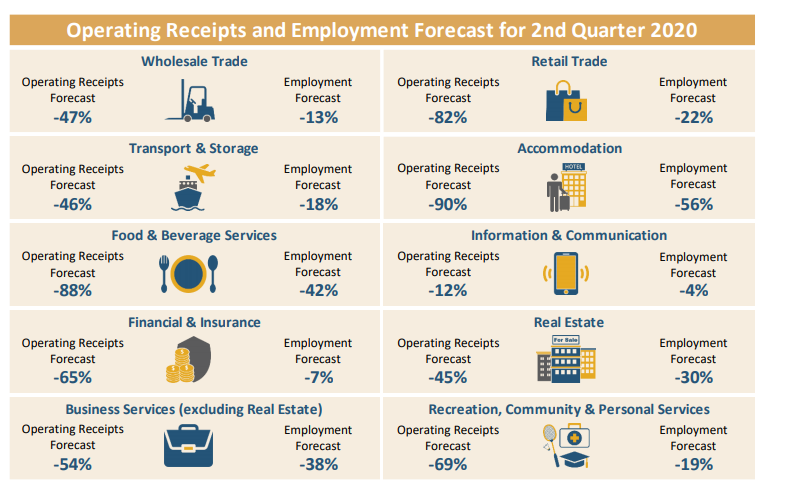

Singstat has a good breakdown on forecast for operating receipts and employment.

These forecasts are for Q2, so anything affected by the lockdown is hit hard. Retail, Hospitality, F&B and Recreational services are the really big ones. But the second tier of wholesale trade, financial & insurance, real estate, business services are also not spared.

The only one that looks somewhat decent is IT.

Retail Sales

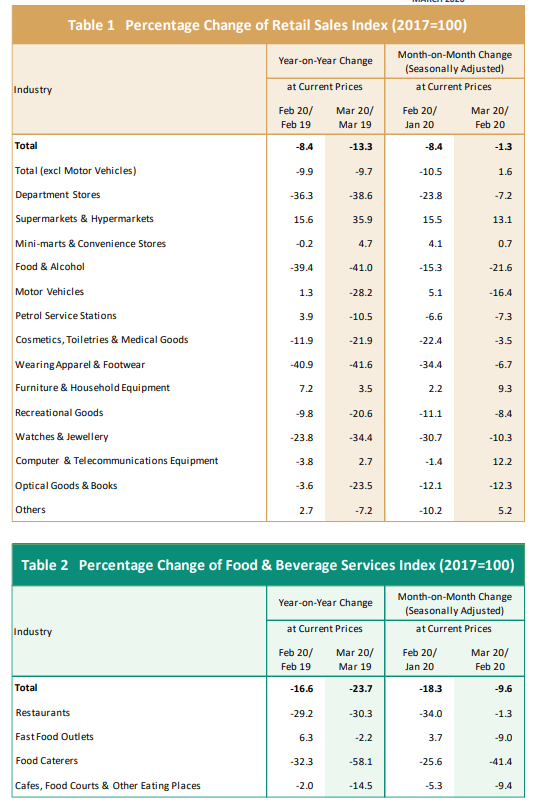

March retail sales was an interesting one:

Remember that the lockdown was in April, so the Feb and March retail sales numbers give us some indication of what Singapore will look like when we reopen.

The ones that are down big are department stores, food & alcohol, clothes, watches & jewellery, and cosmetics.

The ones that are pretty resilient are IT, minimarts, and furniture.

The only sector that did well was supermarkets.

What does the data tell us?

I think the biggest takeaway here, is that the impact on the economy is uneven. So there are industries that are completely crushed, there are some that are impacted but still do decent, and there are some that are absolutely flying right now.

COVID19 is going to create big winners, and big losers. It is going to catalyze big change in the economy, as consumer behaviour is forcibly changed.

Microsoft recently commented that they’ve seen 2 years worth of digital transformation accelerated into 2 months due to COVID19. Think about all the old folks who have never bought anything online in their life, until now. That genie is out of the bottle now.

Lessons from China – Impact to the services economy

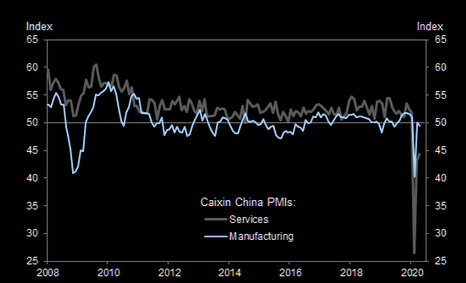

Another really interesting bit of data is that coming out of China.

Now China was the first to encounter and control this virus. They’re down to 1 or 2 cases a day now, which for a country of almost 1.4 billion, is an unbelievable feat.

So China has rush hour, people are going out etc, so we can use China as a good case study for what the world looks like when we manage to control COVID19.

Manufacturing recovers quickly – Supply Side

And what the chart above shows, is that manufacturing jumps back immediately in a V shaped recovery.

This makes sense too. When the economy restarts, factories will go back to work. Once the workers come back, the manufacturing process restarts, and everything goes back to normal levels of output.

And once you restart the factories, you can overproduce to cover last few month’s shortfall, and you can always keep extra supply in storage as inventory.

And once the goods are produced, they can be easily delivered to where they need to go.

This lockdown doesn’t stop the flow of goods, it stops the flow of people.

Services don’t recover so quick – Supply Side

But services are not like that. Services are things like restaurant dining, getting a haircut, consulting a lawyer etc.

The loss of service income is irreversible. When you don’t get a haircut for 3 months, you can’t go out and get 3 haircuts after all this is over. The barber has lost 2 months worth of haircuts. Same for restaurant dining.

And social distancing measures also impact the services economy. When restaurant capacities are capped at 30% of their prior, that’s a lot of capacity down the drain on supply side.

Demand for goods is more resilient than demand for services

And don’t forget about demand. The lesson from China is that once the reopen happens, people are a lot more cautious about their spending because they are worried about losing their job.

And going everywhere with a mask, and with social distancing, is a lot less fun, so it kills the mood too.

Starbucks is saying that they’re seeing demand about 30% below pre-COVID19 levels in China right now.

So we need to split demand between goods and services.

Another lesson from China is that if you price things with a big discount, consumers will still spend. If you give them a 30% discount, people are still keen to buy that iPad they always wanted, or those clothes they never knew they wanted.

Services though is trickier. How much discount would you need before you feel like going to Disneyland Shanghai? Or Universal Studios? Or watch a movie?

Impact on Economies

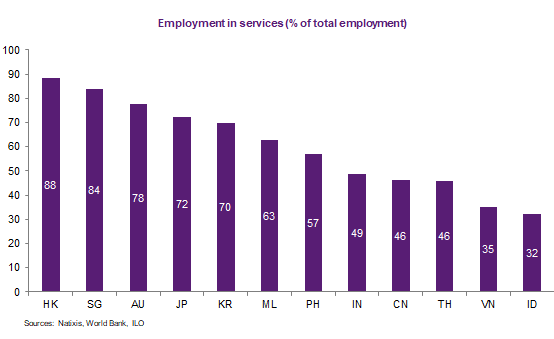

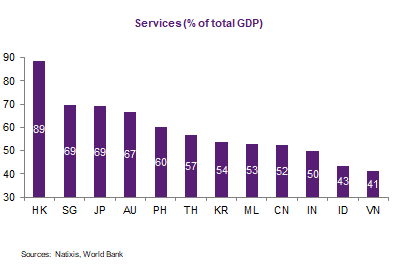

Services Economy Impacted

So economies that are very dependent on services will have a tough 2H2020. And which are those? Hong Kong, Singapore, Japan, Australia.

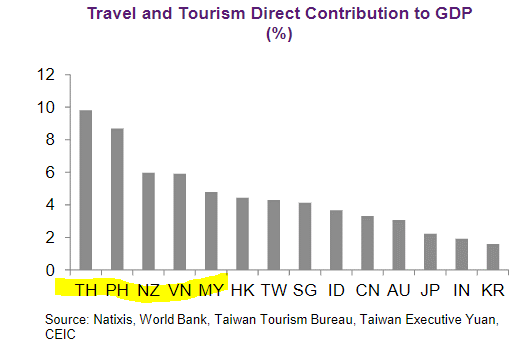

Tourism is dead

And if you thought services was bad, wait till you look at tourism.

I think international tourism in 2020 is pretty much dead. Taking an international flight again this year is probably going to be more effort than its worth, especially if you need to get quarantined and tested when you land, and once again back in Singapore.

So domestic tourism will be the new big thing in 2020. Once your country brings COVID19 under control, it’s pretty easy to travel domestically. That’s what Airbnb says too, where they’re seeing domestic AirBnb bookings pick up quite strongly this summer.

That’s great for countries with big domestic populations. Think China, and the US. Europe I’m not so sure because it depends on how the EU handles border reopens, and the EU is always a tough one to predict politically. But if you stay in a country like Denmark, your own country is big enough to take a roadtrip somewhere for a week’s vacation anyway.

But it’s really, really bad for small countries with small domestic populations. Think Singapore, and Hong Kong.

And it’s also really, really bad for countries that depend strongly on tourism. Names like Thailand and Phillipines.

What happens in 2H2020?

To sum up our discussion:

- Supply of goods will recover strongly

- Demand of goods will recover slower, but consumers can be incentivised to spend with big discounts

- Supply of services is dependent on the control of COVID19. The better the control, the less social distancing required, and the bigger the recovery in capacity

- Demand of services will not recover well:

- Lost services will never come back again

- Social distancing and fears over recession dampens the mood to consume services. No mood to go to a restaurant and order a big feast regularly, with all the uncertainty over the economy.

- Slashing prices will help, but not in a big way.

- Countries that are dependant on international travel will be hit very badly. Countries with big domestic population and ability to drive domestic consumption of services will fare better.

Now for very obvious reasons, the 5 rules above mean that every country will be impacted differently, depending on how their economy is structured.

You can’t generalise and say the whole world will do poorly, because there will still be winners and losers.

Hong Kong and Singapore

I think Hong Kong and Singapore will fare poorly.

Both are small city states very dependent on the services economy, and without a large domestic population to draw on for consumption of services (Okay I get that Hong Kong has China, but you get what I mean).

Both also lack that manufacturing output which can serve as a cushion in this crisis.

Thailand and Phillipines

Thailand and Phillipines will also suffer because of the strong dependence on tourism (10% and 9% respectively). With international travel strongly curtailed in 2020, a big part of that spending is gone.

Stimulus

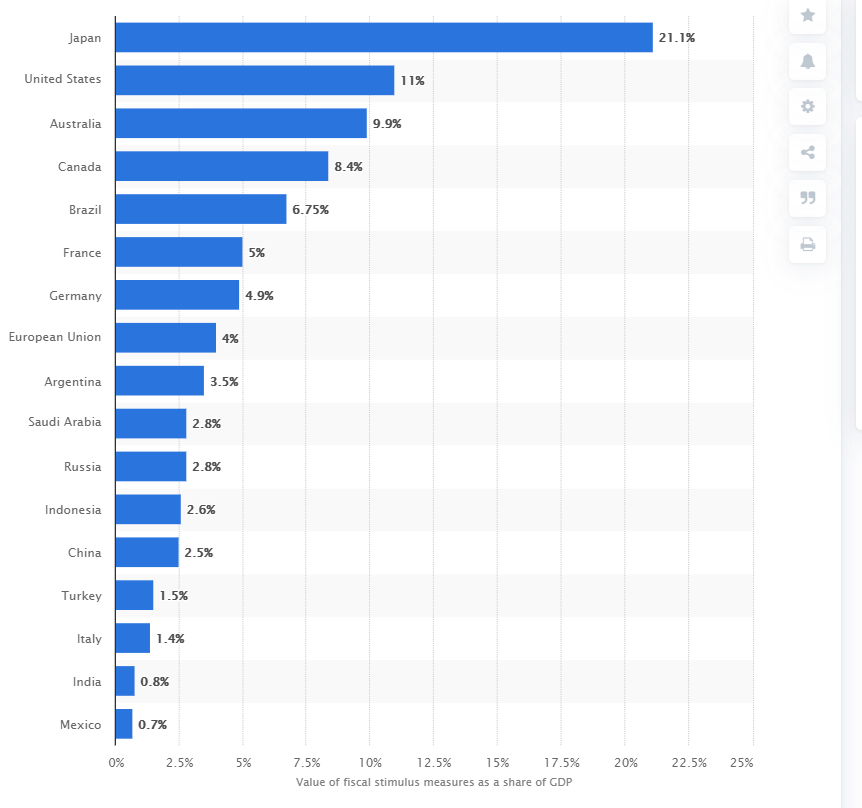

Stimulus matters though. If the economy takes a big hit, it can be offset by government stimulus – Eg. Offering to pay everyone’s salary.

Both Singapore and Hong Kong have big reserves that can be drawn on to stimulate the economy. And we’ve done exactly that – both have pumped about 10% of GDP into the economy thus far, putting us on par with the US. This will definitely help.

Other countries like Thailand and Philippines don’t have it so easy, because they can’t do such a big stimulus without weakening the currency (which will impact companies who borrowed in USD).

What happens to the Stock Market in 2H2020?

Okay and now to the million dollar question.

What happens to the stock market in 2H2020?

I think the simple answer, is that it depends.

The lesson above is that every country, and every industry is impacted differently. That’s the biggest takeaway from this virus.

You have the guy who runs supermarkets and he’s seeing the best sales he’s ever seen. Same for the guy who runs a software business.

But the guy who runs a tourism company. Or a hotel. Or who works for an airline. They’re seeing the worst downturn they’ve ever seen in their entire lives.

This virus produces big winners, and it produces big losers.

I’m in the process of compiling a massive industry by industry, country by country analysis of each asset class for Patrons. I’m already on 5000 words and Part III of the series, and nowhere close to completing because the list just keeps getting longer.

I’ll summarise some key points here, and you can refer to the Patron list for the full details (will probably need to beef it up significantly after this post).

International Airlines, Hospitality, Tourism, airline services are badly hit

Following from the 5 rules above, anything that involves international airlines, international hospitality and tourism will be badly hit. I still don’t see any signs of recovery for these industries, and I think it will take years to recover to pre COVID levels. Domestic tourism and hospitality may fare better though.

Manufacturing could be interesting

For manufacturing – a more granular analysis is required. Manufacturing on supply side seems to recover pretty strongly, so as long as the demand isn’t impacted, these guys could still perform well.

So stay away from guys who manufacture airplane parts, and buy guys who manufacture computer parts. You get the idea.

Real Estate

Follows from the rules above – avoid anything exposed to the services (ie. retail) or hospitality space, unless you get it at great prices. Between the two, retail may recover first, especially those that cater to domestic consumption. Hospitality probably takes longer to recover.

Industrial / Logistics will prove more resilient, but a lot of that may already be baked into the price.

Banks

Unfortunately banks are exposed to all sectors of the economy, so they’ll probably get hit. Low interest rates are also really bad news for them.

Software

Software is definitely a big winner of COVID19, which explains why their stocks are flying.

But even within software there are differences.

Names like Amazon and Microsoft benefit very strongly from the lockdown. Names like Facebook and Google which are ultimately ad driven also benefit from more usage, but to a lesser extent.

And then the question of how much upside is baked into the price already.

Will the Market Crash in the second half of the year?

The simple answer is – the market has already crashed.

You look at the airlines and tourism industries, most are down more than 50% from their highs. Same for oil & gas. Same for oil & gas and airline services.

Then you look at the software names, many of which are back to all time highs. That makes sense because their earnings are higher than they’ve ever been, and they’ve stolen tons of market share from the more traditional players.

You look at banks and retail REITs, they’re already down 30% from highs. Sure, there may be room to fall, but it’s hard to envisage another 50% fall from here.

So the market actually looks pretty rational. The market seems to be pricing in the impact to each industry based on earnings. A lot of people look at the S&P doing a 60% retrace and forget that about 50% of the S&P is comprised in the FAANMG stocks. The tech guys are flying, so it’s natural that the S&P is flying too right?

BUT – Don’t rule out an exogeneous shock

But in all honesty, I see real risk of another black swan event popping up.

It’s impossible to predict with certainty what this event would be – if we could, it would no longer be unexpected. Possible examples are a big name bankruptcy (WeWork?), a big currency depreciation from one of the G20, a second wave of COVID19, a mutation in COVID19 to become more deadly, an escalation in the US-China trade war etc.

The global economy was already on its last legs before this. We were already nearing the later stages of the short and longer term debt cycles, and debt levels were elevated across the US, Europe and Japan, while interest rates were at record lows. Historically, that usually signifies the later stages of debt cycle.

All COVID19 did, was to tip us over the edge. And now that we’re over the edge, all these changes will need to play out over the next few years.

So I genuinely think the next year or two at least, will be highly unstable. There’ll be lots of dislocation across all asset classes, creating lots of opportunity for the active investor.

These are really volatile times, and I would be erring on the side of caution here. I’ve always said the real secret to investing, is to lose less money than you make.

Doesn’t matter how much your neighbour is making, trying to beat them or FOMO is just a vanity metric. Focus on your own portfolio. As long as you make more money than what you’re losing, you’re already getting ahead.

Many people are trading like this crisis is already over, but the way I see it, we’ve barely even begun.

As Winston Churchill once put it: “This is not the end. This is not even the beginning of the end. But it just might be, the end of the beginning.”

Reminder: We’re running a Labour Day Promotion for the FH Course and the REITs MasterClass. You get a big discount off the usual price, and a 3 month access to Patron thrown in.

A great way to make good use of your extended circuit breaker!

Find out more here!

https://www.straitstimes.com/asia/east-asia/shanghai-disneyland-tickets-sold-out-in-minutes-for-reopening

Ooh that’s an interesting one. Thanks for the share!

Hi FH,

Great writeup as usual.

One thing you haven’t factored in which I think is crucial is the medical element. This is at the end of the day, a medical driven crisis.

For me, this has become more straightforward. It is clear that initial hopes for repurposed drugs like remdesivir and hydroxychloroquine/chloroquine + azithromycin either work only slightly (former) or not at all (latter). This means we are likely quite far away from a treatment which has a significant impact on Covid. A vaccine is still at least 12 months away by most estimates. The nearest term estimate is a group from Oxford University which gives itself an 80% chance of a vaccine by Sep but most consider that very optimistic.

Many countries are re-opening without putting in place systematic testing, contact tracing and quarantine. Especially in the US, it means that the disease will only spread further. It may take 2-3 months to reach pre-lockdown death rates again but they will get there. The only question is whether the reaction to this next wave is a repeat shutdown or whether a decision is made to just go on with life regardless of the additional deaths as Trump seems to have decided to do. The UK tried that initially but quickly reversed course while Sweden has stayed the course and while death rates in Sweden are higher than in other Nordic countries, they are not so high as to be catastrophic and Swedish society seems to have accepted this.

So the big questions are as follows

1. What decision will governments and societies make in large Western countries when the second wave arrives? Lockdown again or live with it and accept the additional deaths?

2. Will the stock market reflect what is happening in the real economy or will it diverge from this in the face of unprecedented stimulus? If it diverges, how long will this divergence last? It can last quite a while if you look at emerging economies and their equity markets – surprisingly the correlation there historically is not as high as one may expect.

Warren Buffet just held his annual meeting for Berkshire and there were 3 key slides. First, he holds an unprecedented record $137B in cash equivalents. Second, he made negligible equity trades in Q1. Third, he didn’t buy anything in Apr and instead liquidated all airline holdings. So the man who previously said “When it is raining gold, don’t put out a thimble but put out a bucket” is not buying. The question for the rest of us to ponder is Why? His answer “The cash position isn’t that huge when I look at worst-case possibilities.”

I think for anyone who wants to invest, make sure you can first support yourself and your family for the next 2-3 years in your own worst case scenario.

Hi CMC,

That’s a really good comment, thank you for sharing.

My thoughts:

1. Really good question. My personal view is that despite all the talk and bravado, they will lock down again if there is a genuine second wave. The human cost is just too high. Could be wrong though.

2. I think for the stock market the number one factor to look at is fund flow. As long as institutional money is moving into stocks, stock prices will go up. It’s simple supply demand. I think the big question now is that if institutionals don’t buy stocks, where does the money go?

USTs don’t make sense because the yields are so low, and just think about how much new UST issuance is coming. Gold, Crypto etc are good but if you’re managing $100b you can’t buy that much gold or crypto. Real estate has liquidity issues – but I think it will absorb some capital – but the time is not here yet because effect is lagged.

So for a liquid investment, there’s not much that can replace US stocks. But this analysis is pretty unique to US stocks because of USD’s reserve currency status, so the rest of the world is different. In some ways its similar to how the 1997 to 2000 period played out as a dot com boom, when money was sucked out of Asia (AFC) and fuelled the Dot Com bubble – with a tailwind from Fed cutting rates. Very similar fund flow dynamics to me.

3. I agree on the argument for cash. With where prices are now, I’ve also shifted to holding big cash positions. Market doesn’t look super attractive to go in right now in a big way, but I’m also not selling existing holdings. For now, will probably hold the cash and watch how 2020 – 2021 plays out. I think there’ll be lots of opportunities in the coming year. If not in stocks, then in the real world.

Hello,

Enjoy reading your post again.

Do you think it is fair to say if we are looking at 10 years or longer investment window, those big & well established blue chip company within those badly hit sector is still a good opportunity to go in now? OR we should wait for 1-2 more Q to let them report even more bad news (Hopefully share price drop another 20-30% more from current price before going in?)

Cheers

Personal thoughts (not investment advice):

Yes, but it really has to be a case by case analysis. Some companies may genuinely never recover from this. But for those who are badly hit, but will recover eventually, I do like current prices. Impossible to time the bottom, so I would just buy and average in.

I agree to a much extent to your views presented. I currently hold 30% stock 70% cash at the moment. Waiting at the sideline, looking to invest into the economy that might recover the first…

I came across a very interesting view.

It depends if you are bullish or bearish. For bearish people, they say WB has not dare to invest 137 Billion, waiting for the market to go lower.

But for bullish, it may means that even though he has not invested his 137 Billion, he is still vested in massive areas of the economy and not selling away the existing interests he has in all the other companies except for airlines.

Because h and Charlie Munger’s role these days are probably to to buy over distressed company. But currently FED is doing that job right now.

Which is not a sustainable way of doing things as it inject artificial stimulus into the market. Things that is meant to collapse has to collapse naturally. We cannot inject morphine to keep the economy because it will just prolong the suffering.

That’s a really interesting view. Thank you for the share.

Thanks for your article, would like to seek clarification for the following point:

“Both also lack that manufacturing output which can serve as a cushion in this crisis.”

Singapore Manufacturing industry contributes about 20% to 25% of annual GDP, I have a different view that the Singapore economic will be crusioned by this industry compare with Hong Kong which does not really have manufacturing output. MCN like illumina(bio technology), GSK (pharmaceuticals) will be greatly benefit from this crisis.

That’s a good point, thank you for raising this.

Hey FH,

I think one aspect that’s missing from the whole discussion on manufacturing would be the resurgence of anti-china rhetoric leading to an escalation of the Trade War. It looks highly likely that Trump will not win an election based on a “strong economy” so my suspicion is that he’ll pivot to blaming China for somehow causing this pandemic. Afterall, his base really does seem to hate China.

With little to no proof as of now that it did not originate in a lab (eventhough scientists are highly doubtful), I think it’s quite possible that Trump, uses China as a punching bad, increases trade sanctions as a punishment, and sacrifices the economy to win re-election.

It might appear speculative but it seems that he’s been alluding to this all week.

Yeah that’s a good point. Largely agree with you – Trump’s reelection, and the China rhetoric as we approach Nov, will come to the forefront in the coming months.