Okay, I know what many of you are thinking.

But FH, my stock XXX has already fallen 50% from highs. You talk about a market crash, but the market has already crashed…

And I agree.

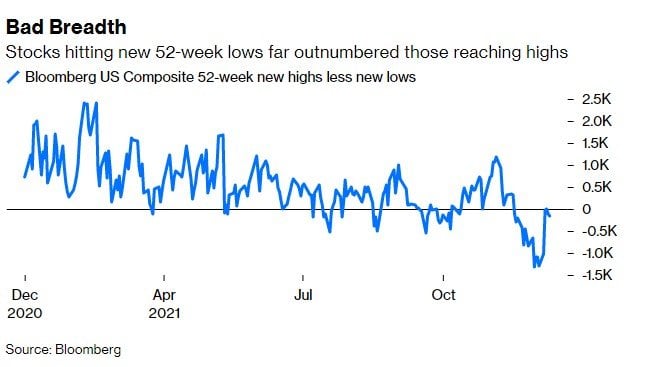

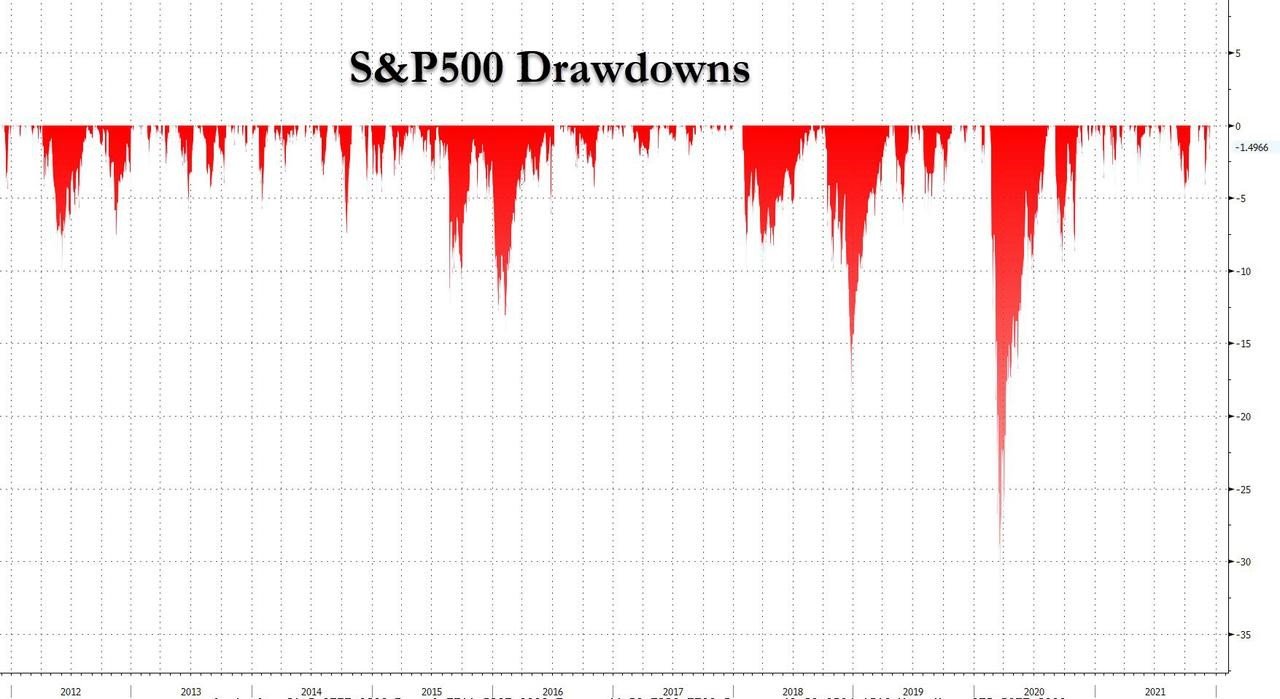

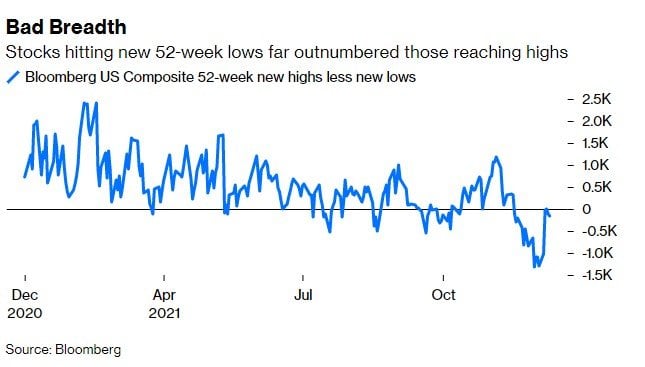

Market breadth is absolutely disgusting of late:

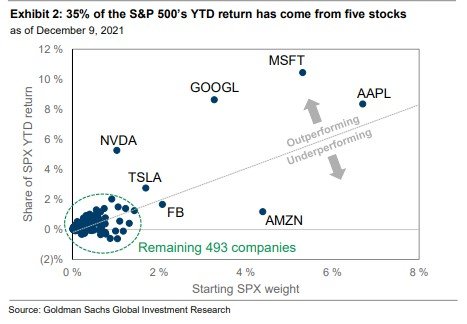

The bulk of the market return to date has come from just 5 stocks – NVIDIA, Tesla, Google, Microsoft and Apple.

Strip out these 5 stocks, and the market performance looks a lot less sexy.

At the same time, insider selling (so-called smart money), is hitting all time highs:

Market breadth and insider selling are leading indicators.

Is the market signalling to us that bigger moves may come in 2022?

To answer this question, we need to dig a bit deeper into the fundamentals.

3 Big Things that Worry me about 2022?

3 things that worry me:

- Inflation

- Omicron

- China slowdown

Let’s discuss each individually.

Note: moomoo trading app is running a Christmas Bonus now, with extra gifts on top of the free Apple Share.

From now till 1 Jan, at 8pm each day, grab an iPhone 13 256GB, AirPods 3, or more when you fund your account between 30 Nov, 10:00 SGT to 31 Dec 2021, 09:59 SGT.

This is on top of the free Apple share (worth $230), $40 stock coupon, and 180 days free stock trading which is a pretty great deal.

Sign up link here, and full details at the end of this post!

1. Inflation

Latest Developments in Monetary Policy

Last week was an absolutely monster for monetary policy.

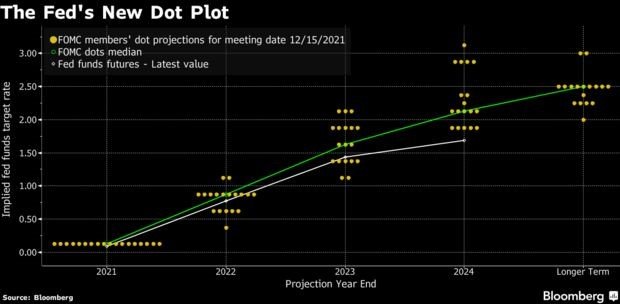

Key developments from the Federal Reserve are:

- Inflation not transitory – Jerome Powell admits that inflation is no longer “transitory” and is a problem (which he conveniently realised only after being reappointed as Fed Chair)

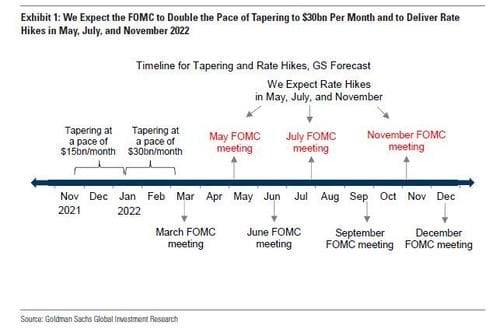

- Accelerated Taper – Feds will accelerate Tapering from $15 billion a month to $30 billion a month from January 2022. This means that the Fed buying of Treasuries will end completely by March 2022, paving the way for rate hikes as early as March 2022

- 3 Rate Hikes in 2022 – Fed’s latest Dot Plot now anticipates 3 rate hikes in 2022.

Market is pricing in rate hikes in May, July and November 2022.

A total of 75 bps (0.75%) increase in 2022.

And if we zoom out into 2023 and 2024, the Fed expects another 3 rate hikes in 2023, and 2 rate hikes in 2024, for a terminal Fed Funds rate of 2.1% by the end of 2024.

In any case, the market just flat out disagrees with this.

The market is pricing in a cycle top for rates at 1.5%, before Feds are forced to cut again (note that cycle top for the 2018 cycle was 2.0%).

Central Banks are behind the curve

I’m just going to put it out there.

I think central banks are way behind the curve on inflation.

I think in hindsight, the Feds pumping $120 billion a month into the economy and keeping interest rates at 0% while inflation is running at 40-year highs may go down in history as a colossal policy mistake.

And I think in 2022, Jerome Powell is going to need to play catch up on inflation. And I think the market is underpricing this risk.

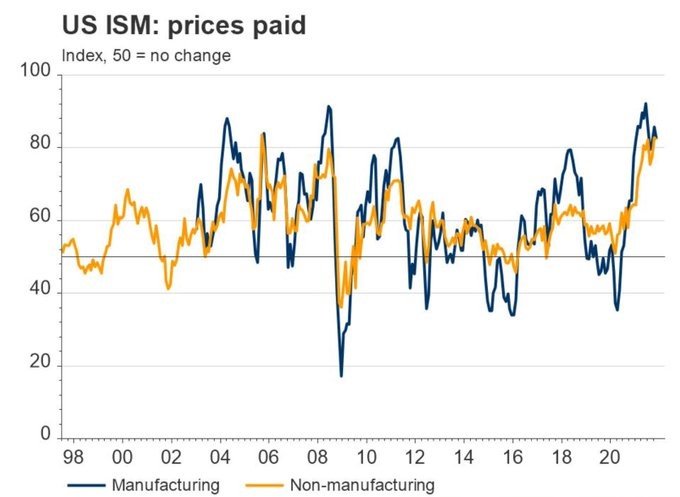

Inflation is everywhere

I’ve been talking to a lot of business owners across industries recently.

And what I’m hearing, is that inflation is everywhere.

Fertilizer, Aluminium, Beef, Petrol, Chemicals, animal feed etc. You name it, there’s probably some supply chain issue in an Emerging Market somewhere that explains why prices are soaring.

And we’re talking 5% – 10% increases in input costs across the board.

For now, producers are absorbing the price increase, but word on the street is that 2022 is when they will start passing on the cost to consumers.

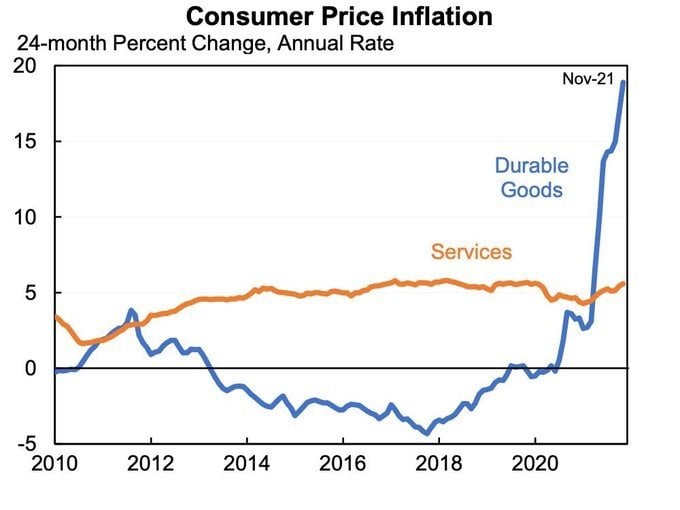

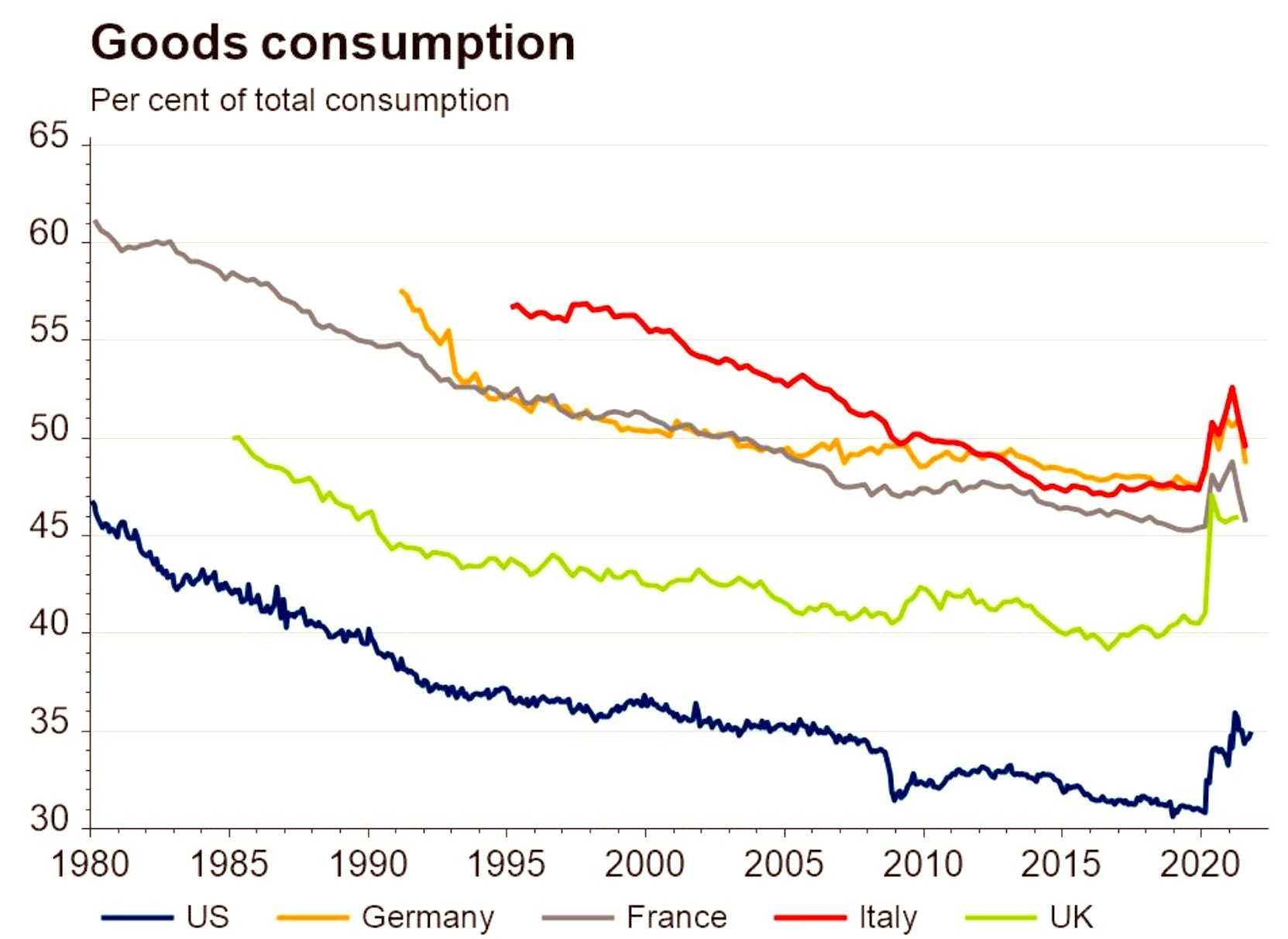

Where is the inflation coming from?

The prevailing wisdom is that inflation is driven by record demand for goods.

Because of COVID, people stay indoors. They spend their money on stuff like Xbox and furniture (goods), instead of restaurants and hotels (services).

Once COVID goes away, people go out again, and switch back to services spending.

And inflation goes down.

At least that’s the theory.

The problem though is that so far at least, the data isn’t backing it up.

Goods consumption has come down slightly, but they haven’t dropped to pre-COVID levels.

And if you look at services inflation, inflation there isn’t as dormant as you would expect.

Don’t forget that services have lower supply elasticity than goods. If demand for services spike, supply cannot increase quick enough to catch up (it takes time to hire and train new chefs etc).

And that’s even before you consider the potential impact from Omicron.

2 ways this plays out

I see 2 ways inflation can play out.

Base Case inflation – Goods spending gradually switches over to services inflation. Consumer expectations on inflation come down. Inflation comes down from Q4 levels (6%+), but stays high for a while in the 4% range. Feds hike 3 time in 2022.

Inflationary spiral – There is a wage price spiral, loss of central bank credibility, and shift in consumer expectations. If this plays out 3 rate hikes in 2022 won’t cut it.

What is a wage price spiral?

Basically – workers demand higher salaries because the price of stuff is going up. Because wages go up producers have to raise prices. Because price goes up workers demand more rate hikes. In a vicious cycle.

The last time we saw this in the developed economies was the 1970s. It was wave after wave of inflation, until Paul Volcker (Fed Chair at the time) hiked interest rates to 20% to kill inflation once and for all.

I don’t think we’re there yet.

I think base case we still see the Base Case inflation scenario.

But I don’t think it would be wise to rule out the possibility of an inflationary spiral.

Long story short – I think 2022 is going to be volatile. Market may be mispricing inflation here.

There is a small possibility that consumer demand falls in 1H2022 due to rising prices and slowing growth, and inflation goes away by itself. That’s possible especially if you consider the potential impact from Omicron. But for now I think this is a lower probability outcome.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

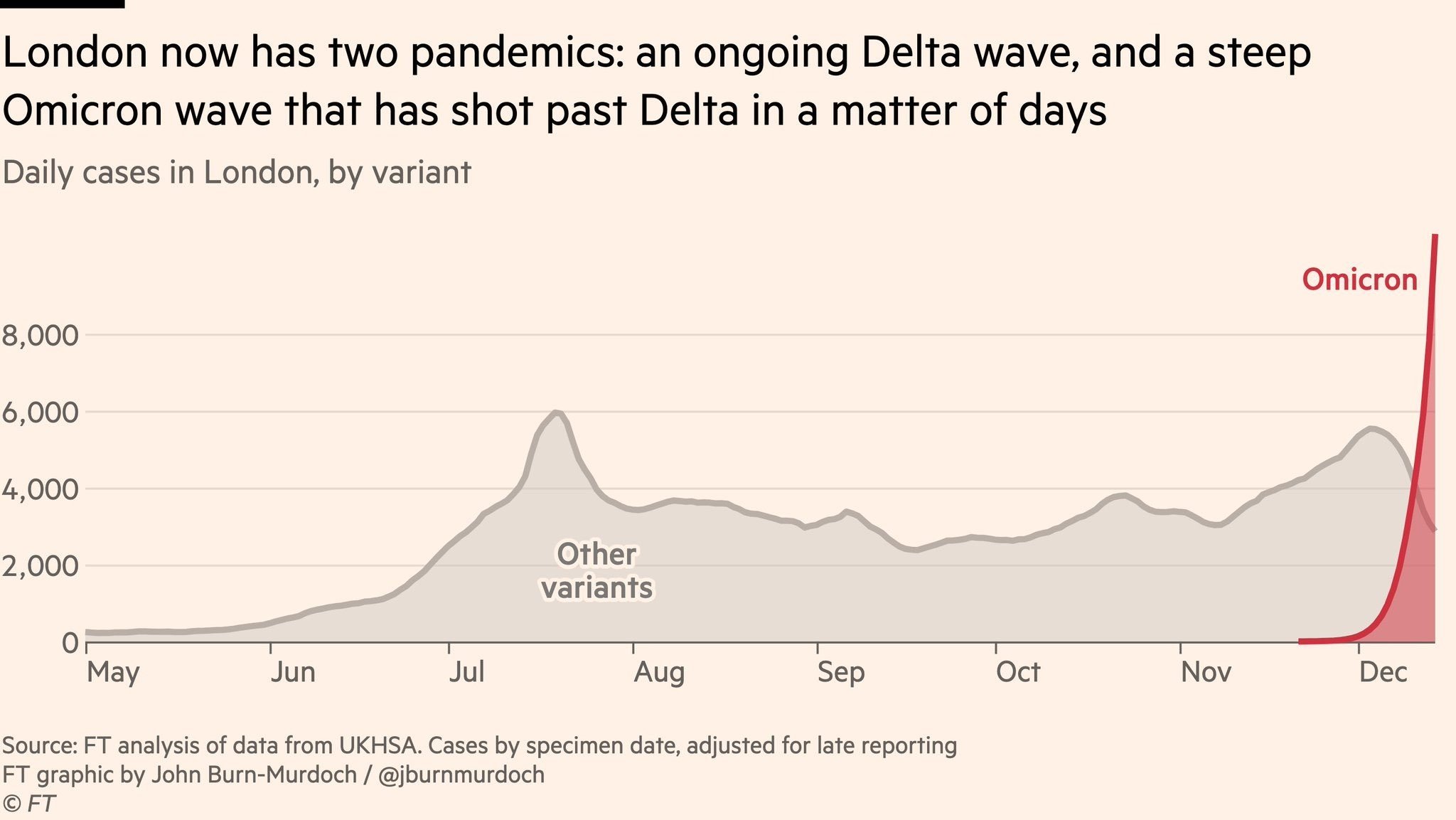

2. Omicron

I shared about my worries for Omicron a while back.

And those worries are playing out at speed now.

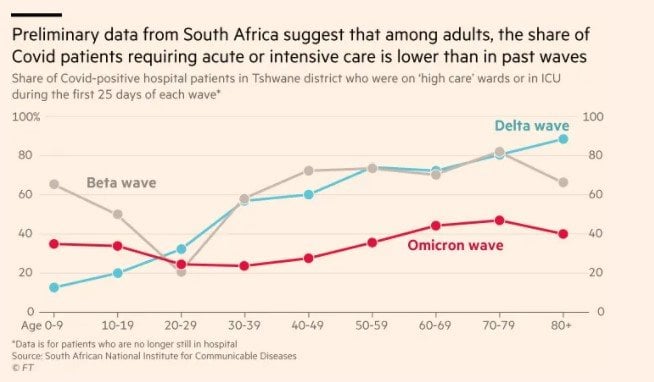

To sum up what we know about the Omicron variant so far:

- Transmissibility – Omicron is very transmissible (estimated R0 is 4.0). Reports suggest Omicron replicates 70 times faster than Delta in the Bronchus (windpipe), but 10 times less in the lungs. Which would indicate why it seems to be more transmissible, but less deadly.

- Immune Escape – 2 Dose Vaccine or prior infection isn’t sufficient to prevent Omicron infection, which may explain why Omicron is spreading so fast.

- Vaccine Efficacy – A 3 Dose Vaccine will help prevent Omicron infection, and 2 Dose Vaccine does protect against serious illness. So all is not lost.

- Fatality – Data is mixed. Early reports indicate Omicron is less deadly than Delta, but a recent Imperial study says “no evidence” Omicron is less severe than Delta. Note that Delta is reportedly 4 times more severe than Alpha (the original COVID), so even if Omicron is less deadly it may only take us back to original COVID levels.

I compiled some charts below if you’re interested.

A virus with a lower fatality rate, but significantly higher transmissibility and immune escape, could be a big problem.

More infected people could translate into more deaths even though fatality is lower.

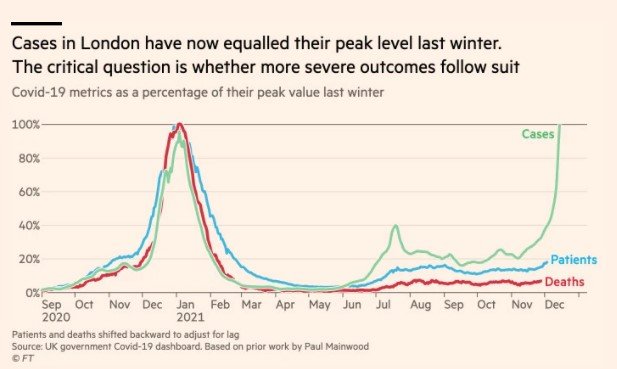

The problem with Omicron is that sometimes it’s not so much about the virus, but how governments react.

If governments deem it necessary to protect the population (sometimes for political reasons), they may impose further COVID restrictions.

We already saw hints of this the past week with Netherlands locking down, UK implementing tighter restrictions, , and France restricting UK travellers.

More may come as 2022 plays out.

Catch-22 for the Market

And this is truly a catch-22 situation for the market.

If Omicron is a problem and it leads to COVID restrictions, then supply chain bottlenecks get worse, inflation is stickier than expected, and Feds are forced to tighten to combat inflation in 2022.

If Omicron is not a problem then there are little COVID restrictions, the economic impact is reduced, so Feds have no reason not to raise rates to combat inflation.

Either way, it looks like damned if you do, damned if you don’t.

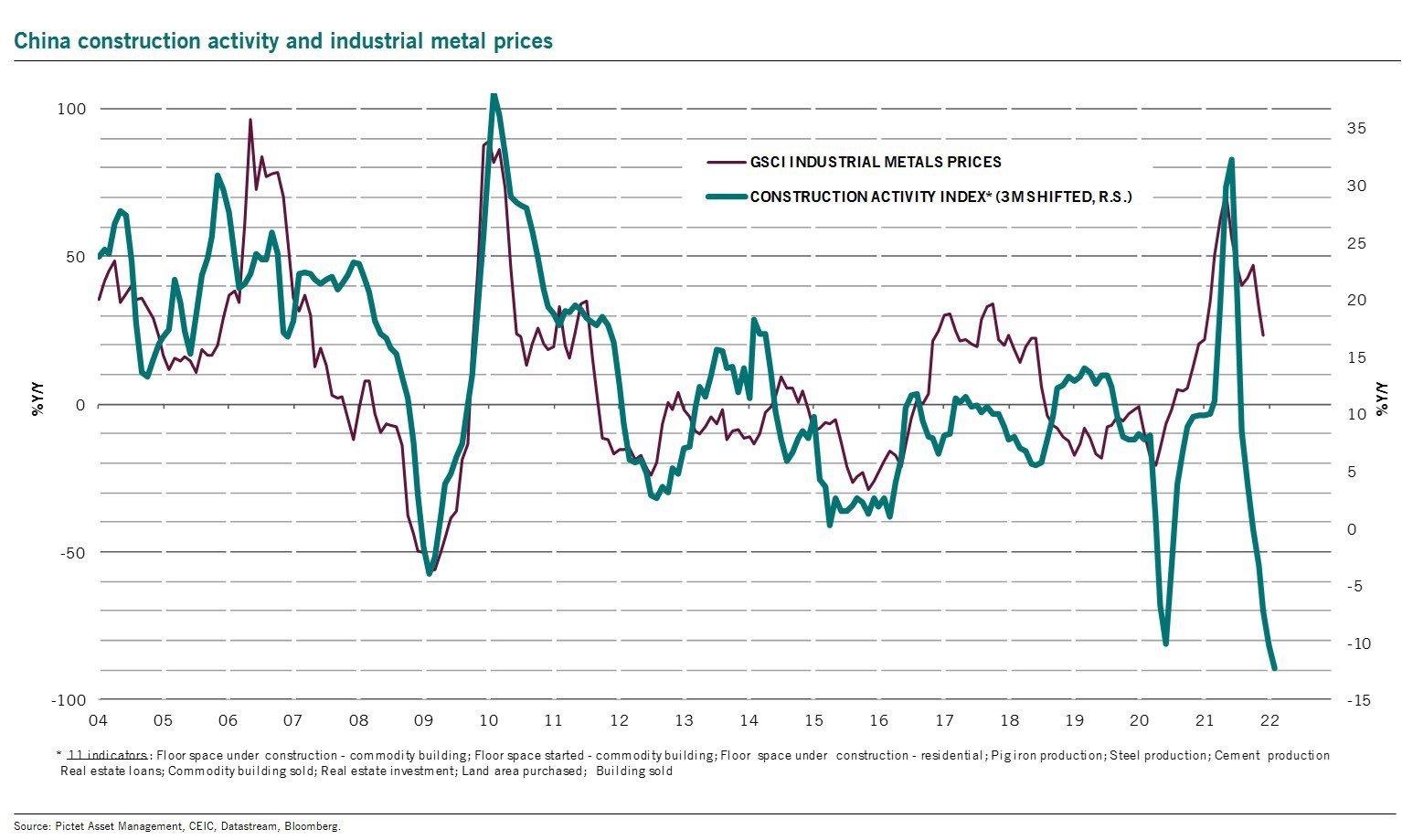

3. China Slowdown

At the same time, the China slowdown is playing out in earnest.

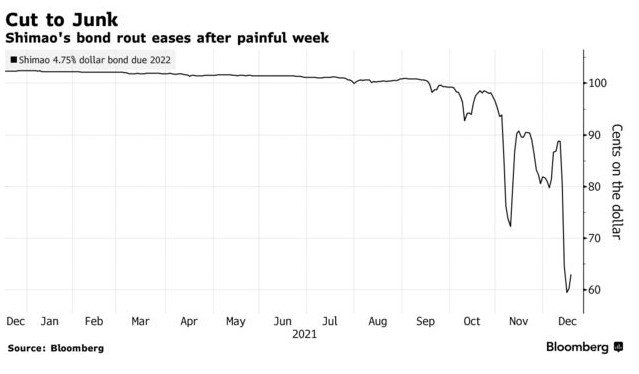

The past week saw Shimao face liquidity issues.

Before this, the property developers who defaulted – Evergrande and Kaisa, were all junk rated developers.

So the market already knew they were in trouble.

But Shimao is the first Investment Grade (IG) rated developer to run into liquidity issues.

This signals to the market that even the IG rated developers are not immune, and is a significant escalation in the real estate crisis.

This will raise borrowing costs for all IG rated China developers across the board, exacerbating liquidity issues.

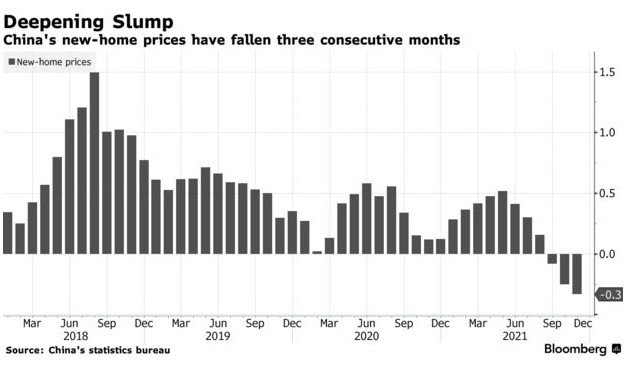

At the same time, China home sales have collapsed, together with construction activity.

This is a deflationary path… that takes years to play out

The way I see it, the path that China is on – is to restructure their economy away from reliance on real estate, and into things like manufacturing and hard tech.

This is not a path that ends in 1 – 2 years.

This is a 5 – 10 year path, kind of like Japan in the 1990s.

And if the CCP is serious about this deleveraging, they need to keep monetary policy tight.

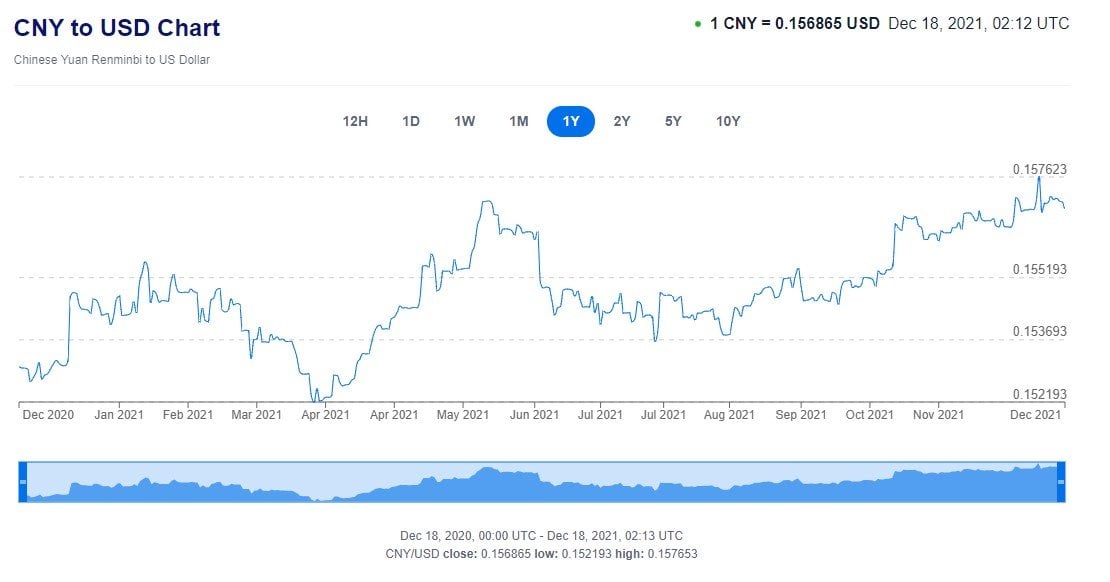

This is a deflationary path, and it explains why the RMB is so strong of late.

I think many western commentators are missing this point. If the CCP eases monetary policy in a big way then they will undo all the good work they’ve done this year on real estate.

Don’t Expect China to be the growth engine to save the world this time around

If I am right, then China’s growth may stay slow for a while, as they focus on restructuring the economy.

So unlike 2008 where it was China that powered the global economy to new highs, this time around the west is on their own.

This is bad for Emerging Markets because they can’t rely on huge growth in exports to China going forward.

This is bad for the West because they can’t count on China to stimulate growth, at the same time as the West is tightening monetary policy to combat inflation.

Impact on Stocks

Okay, so those are my 3 big macro concerns for 2022.

What is the impact on stock prices?

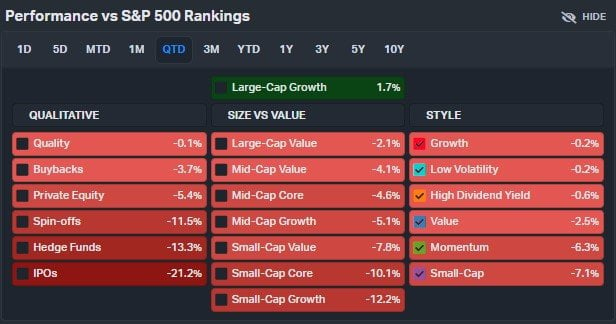

Quarter to date, the most speculative parts of the market have been getting crushed.

IPOs down 21%. Small-cap growth down 12.2%.

Will the stock market crash in 2022?

I think what is tricky about this market is that the strike price for the Fed Put is now a lot lower than what it was previously.

Or in plain English – Don’t expect Jerome Powell to save the day so soon.

In 2018, it took a 20% drop in the S&P500 before Jerome Powell reversed the path of rate hikes.

In 2020, it took a 30% drop in the S&P500 before Jerome Powell went into unlimited QE and buying of Junk Bonds.

In 2022, if inflation runs hot and Feds hike 3 times, what kind of drop will we need before Jerome Powell reverses course?

As things stand, the S&P500 sits at 4620, down just 3% from all time highs.

I don’t think a 10% drop will cut it given how serious inflation is.

More realistically, we need a 20% drop in the S&P500 before the Feds consider changing path.

So there may be a lot more pain going forward.

As to when the market actually crashes, I don’t have a strong view on that.

Morgan Stanley is calling for huge volatility in the first half of 2022 as we have the first rate hike, which is possible.

Either way I would expect significant volatility.

Nothing goes to hell in a straight line, and there will be plenty of bull and bear traps along the way. Expect vicious rallies and vicious drops.

It will be heaven for traders at least.

How am I positioning? Which parts of the market has value?

As shared previously, I’ve generally dialled back on my rate of purchases the past few months.

China stocks have already collapsed, so comparatively there is more value there compared to US. But the bottoming will take some time to play out, so it would be wise to average in.

US stocks have split into 2.

The speculative growth and small cap names are already in the process of collapse. But rate hikes are truly scary for speculative growth stocks, and I would want to give it some time for the dust to settle.

The big caps like FAAANM that make up the indexes, they’ve been largely immune from the sell-off so far.

Which makes me nervous heading into the first half of 2022, because that’s the last remaining bastion of strength in this bull market. That will probably be the last one to fall.

Cyclicals like banks and commodities are interesting.

Rate hikes are traditionally good for bank stocks, as long as they don’t trigger a recession.

If Omicron causes a sell-off in oil, I think that could be an interesting add as a mid term play. I think all the underinvestment in fossil fuels is going to come back and haunt us in 2023/2024.

I think blue chip S-REITs are the one bright spot in this market where valuations look more reasonable. As shared last week, I bought some recently, and I plan to buy more going forward.

Sure, S-REITs may sell off short term as the Feds hike but comparatively their starting valuations are not as demanding as other parts of the economy, so the decline shouldn’t be as big.

You can check out my full portfolio and stock watch on Patreon if you’re keen.

moomoo Christmas Bonus!

moomoo is running a Christmas Bonus now, which gives you extra gifts on top of the free Apple Share and S$40 stock cash coupon in their welcome bundle.

From now till 1 Jan, at 8pm each day, grab:

- iPhone 13 (256GB) Worth S$1,469 – 1st User to Snatch Daily

- Airpods 3rd Gen Worth S$269 – 2nd – 11th User to Snatch Daily

- Grab Voucher Worth S$50 – 12th – 211th User to Snatch Daily

- S$40 stock cash coupon (unlimited) – Those who didn’t managed to snatch one of the above gifts, will be given a S$40 stock cash coupon.

Terms and Conditions here, you just need to:

- Be a new user who has not made a first deposit before 10am on 30 November 2021

- Make your first successful deposit ($2700) between 30 November 10am and 31 December 2013 0959am

- And be the first to grab the gift at 8pm each day!

If you sign up before 31 Dec you also get:

- a free Apple share (worth est. S$230)

- S$40 Stock Cash coupon

- 180 days unlimited commission free trading for US, HK and SG

- Limited edition moomoo figurine

Frankly it’s a pretty good deal, so do check it out if you’re keen: moomoo Signup Link

Here are the winner screenshots below:

Sign up link here: moomoo Signup Link

Closing Thoughts

My concern is that buy and hold investing may not achieve the same results in this decade, as compared to the previous decade.

The post 2008 period was characterised by easy liquidity and QE from the Feds. This raised all asset prices across the board. And the best way to capture that return was passive indexing.

Going forward, if I am right, I would expect more rotation around asset classes. Money rotates from small cap growth into large cap value. Into cyclicals. Back into growth. And so on.

Think about Crypto and how the alt-coins take turns to pump, while the blue chips like BTC and ETH stay flat.

Which may potentially call for a more active approach towards investing in this decade – to lock in profits and rotate them out.

But who knows. This horse is prone to overthinking, and I might just be wrong on all this.

Whatever the case, I would love to hear what you think!

All views and opinions above are from Financial Horse.

The content is provided for entertainment & informational use only. The information and data used are for purposes of illustration only. No content herein shall be considered an offer, solicitation or recommendation for the purchase or sale of securities, futures, or other investment products. All information and data, if any, are for reference only and past performance should not be viewed as an indicator of future results. It is not a guarantee for future results. Investments in stocks, options, ETFs, and other instruments are subject to risks, including possible loss of the amount invested. The value of investments may fluctuate and as a result, clients may lose the value of their investment. Please consult your financial adviser as to the suitability of any investment.

Great article, FH and something I have been pondering for some time as well.

A few points to add

1. Another reason for persistent inflation is the world has benefited from value for money, quality goods from China for the last couple of decades. As the US pushes for more decoupling, it will mean at least some loss of this effect and hence higher inflation for everyone. I have been skeptical of the transient inflation thesis as it sounded more like “happy talk” and a wish rather than something backed by evidence, something that Lawrence Summers has been saying for a while.

2. My biggest grey rhino worry now is Omicron in China. They have successfully contained previous strains but given the transmissibility of Omicron, they may not be able to contain this. If so, given the lack of efficacy of a 2 dose Chinese vaccine regime against Omicron, it could spell a widespread epidemic in China with widespread lockdowns, hospitalizations and deaths. This would be a disaster for China and the world. If we think supply chains are broken now, imagine what would happen if this occurs and what the impact of inflation will be.

3. Given the inflation situation, many central banks have run or will run out of bullets. Can’t cut if inflation continues to run above 5% and even if they disregard this and cut, how much can they go below zero? This means what was done to save the markets last Apr cannot be repeated.

So, we could be in for El Gordo. If one is taking a long term perspective of 10 years or so, it should still be ok, batten down the hatches and sit tight. But make sure the asset allocation is the right one for ourselves.

BTW, I don’t agree with you that active investing will be better than passive because of the rotations that would happen. That is actually an argument for passive investment. Passive investments automatically take into account all the rotations as the index components shift in weight.

Hi CMC,

Great comment as always. Some thoughts from me:

1. I’ve been thinking the exact same thing about China and Omicron. If this is indeed significantly more transmissible, and China vaccines dont work against Omicron, then the kind of lockdowns they would need to maintain zero COVID in the face of Omicron would really hit their economy. Which is very worrying short term.

2. Agree on the inflation point. I think if they hike and things start to break, Feds will at some point reverse the hikes. But much will also depend on how sticky inflation is. I would think that because of inflation the pain threshold will be higher than previous cycles.

3. Agree that I could be wrong on the active investing point. Much has been said about the death of passive investing, but it continues to perform very well year after year. I would say use indexing as the bedrock of the portfolio, then layer in some active investing on top to satisfy one’s need to “do something”, and to try to generate alpha.

Dear FH,

Great article again.

Maybe the way to go for investor that do not have time to monitor & skill to pick out good individual stock to just go for ETF. It seems a safer bet of cos at much lesser potential return.

Yeah, that’s perfectly fine for those who prefer not to active invest. 🙂

What might be the sudden black swan of invasion Ukraine-Russia and China-Taiwan affect the world economy…?

China Taiwan I dont think is likely in 2022. Ukraine Russia is a real possibility though. Will be very destabilising for European gas prices.

If Russia Ukraine happens, likelihood of China Taiwan is probably higher with China seizing the opportunity perhaps? But Russians don’t seem to like the idea of attacking Ukraine though.. since they view them as the same blood.. just like China and Taiwan. But a NATO Ukraine does seem like the final straw that cannot be breached.

Actually the more I look at it, the more I think Putin might be serious about invading Ukraine. But with Putin it’s always a tough one to read, he could be doing all this to make us believe he wants to invade Ukraine.

Frankly I don’t see China Taiwan as a high probability outcome in 2022. If anything it will likely be later in this decade (if at all).

Hi FH,

Excellent article. Locally not many of us think about the implications of Central bank policy error which is a gigantic issue. Agreed that China could be another black swan if they cant control Omicron. Scientists have said how much faster Omicron spreads compared to Delta. How high do you think inflation can get? Not to fear monger, but if it goes more than 10% etc.. 1-2% interest rate hike aint gonna cut it. It would require as you mentioned Paul Volcker style rate hikes to fight inflation. But the issue is US debt is astronomically high, doubt they can raise too much. What do you think

Actually I was thinking that base case – inflation (in the US at least) may have peaked at 6.8% in Nov. Once the Feds took out the words transitory and woke up to inflation, that to me was the start of the end of inflation.

There is a possibility that inflation spirals out of control, but it wouldn’t be my base case assumption for now. That said – even after taming inflation in 2022, it’s very possible inflation could come back in 2023/2024, just like how it came in waves in the 1970s too.

I do agree that because of all the debt and how long duration the world is, the Feds cannot raise rates too much before breaking the global economy. Market is pricing in a 1.5% cycle top, which indicates a max of 4-6 rate hikes this cycle.

13M locked down in Xian today. Maybe it starts…

Yeah… will be interesting to see how 2022 plays out if China keeps this up

Dear FH

As always a great article exploring things in depth and equally good were CMC’s observations.

Firstly, China slowdown and further pain are guaranteed with poor efficacy of Sinovac, more aggressive lockdowns and property problems- all will culminate in slow down and hit the consumer hard. The HangSeng is already reflecting this and poised at multi year lows and might plunge further. Banks have been asked to lower rates to prevent recession. This will indirectly affect the broader markets with funds fleeing greater China. Indian equities might benefit and they did recently as Asia Pacific and EM funds have a mandate to invest here. The China Wright age has been traditionally around 30-45% and this might fall to 25-35%. The beneficiaries might be India and perhaps Brazil/Mexico etc

Secondly, liquidity will dry up and money supply fall- there will be a rotation out of tech

Although big cap tech will do well and are investable at pullbacks, ‘new stars’ that boast only of sales but not earnings will be slaughtered

The XLK XLC would be a safe way of buying into big tech but QQQ with its heavy loading of FAAMNG might also help

Thirdly, cyclicals – well run financials , energy and real assets such as SG REITS will do well. The banks will counterbalance the potential underperforming REITS if interest rates go up faster or higher. A barbell approach will help. Am invested heavily in this way and would be adding more at each pullback. The dividend yields offer a buffer and will put a floor under share prices

Lastly, a core and satellite approach of passive and sectoral ETF with individual blue chip shares with REAL EARNINGS and dividend record will be a safe way forward

Of course, wars and pandemics are out of our control

Thanks

Garudadri

Hi Garudadri,

Very interesting comment, appreciate the sharing. I actually share very similar views as well.

I read a recent report suggesting that high beta stocks will underperform in 2022, and for low beta stocks to outperform. Very much in line with what you suggested favouring cyclicals and not frothy tech names.

I too, am holding a lot of cyclicals, mostly accumulated from 2020. But as we head into this hiking cycle, I was actually thinking it may be time to take profit some time in 2022 for many of these names, especially for the banks. I don’t expect the Feds to get very far with rate hikes before the economy starts to break.

What I would add though, is that it ultimately goes back to one’s investing timeframe. If one is investing for say a 5 – 10 year period, then 2022 could be a good chance to pick up long term secular growth plays esp in tech if there is any sell-off.

Agreed! Absolutely good long term.

Probably one small correction -> The “new stars” have already been slaughtered hahah.. slaughtered hard

Correct. I must have added that. Many NASDAQ components at 40-50% off their recent peaks

But to me still not appealing

I’m gonna be contrarian. CSI 300 at a floor of 5100 points next year due to easing monetary policy in China. Let’s visit this post again in a year’s time :). Merry christmas to all!

Haha I can totally see a chain of events that results in this too. I guess if we see a flood of monetary stimulus from PBOC, that would be a huge buy signal. Let’s see. 😉

Merry Christmas to you too!

Hi FH,

Thanks for sharing. I plan to continue investing monthly into the S&P 500 in 2022. Simple reason:

3 rate hikes is just not substantive enough, its like bringing a water gun to save a burning house.

Inflation will continue to be persistently high, money sitting in the bank will continue to erode in value, instituitional investors will have no choice but continue to invest in the market (sure, they will increase their allocation to cash, but realistically, with pension liabilities due, how long can they stay on the sidelines?)

Interesting view. But if inflation is persistently high, wouldn’t the Feds be forced to take even more drastic action to respond, which will in turn hit stocks?

My 2 cents:

– Fed target of 2% inflation will shift and we have to deal with a higher inflation for the short / medium term

– Eventually when the fed decide to get serious on inflation, yes the market will correct, but I”ll already be up 20-30% on my investment, how much correction can the fed tolerate?

Interesting viewpoint, appreciate the sharing. Let’s see how it plays out in 2022. 🙂

My 2 cents:

– Fed target of 2% inflation will shift and we have to deal with a higher inflation for the short / medium term

– Eventually when the fed decide to get serious on inflation, yes the market will correct, but I”ll already be up 20-30% on my investment, how much correction can the fed tolerate?

Good point about inflation FH.

About Wage Spiral

I run a services company and just want to say that I’ve personally experienced a very-concerning wage-price spiral in Singapore over the last 2 years. This is without doubt caused by the net reduction of foreign labor due to Covid measures. I noticed early on that other employers were offering higher and higher wages, and it became difficult for me to recruit new employees and retain existing ones until I threw caution to the wind and adjusted our wages to slightly riskier levels. As you rightly mentioned, I am partially absorbing some of the additional costs, but have to pass them to the consumer eventually. I doubt this phenomenon is only happening in my industry, or our country, given that competition for talent is global these days.

You mentioned in base-case scenario that goods inflation will transition to services inflation as economies reopen. Given the wage-price spiral that I am already seeing, and with many of the major economies being services-driven, I am not confident that inflation will significantly abate in the next year. I think we are projecting 2-3 years into the future for inflation to return to near pre-pandemic levels.

Thanks for the sharing! Appreciated.

Yes I’ve been hearing this a lot too, which is why inflation truly concerns me in 2022.