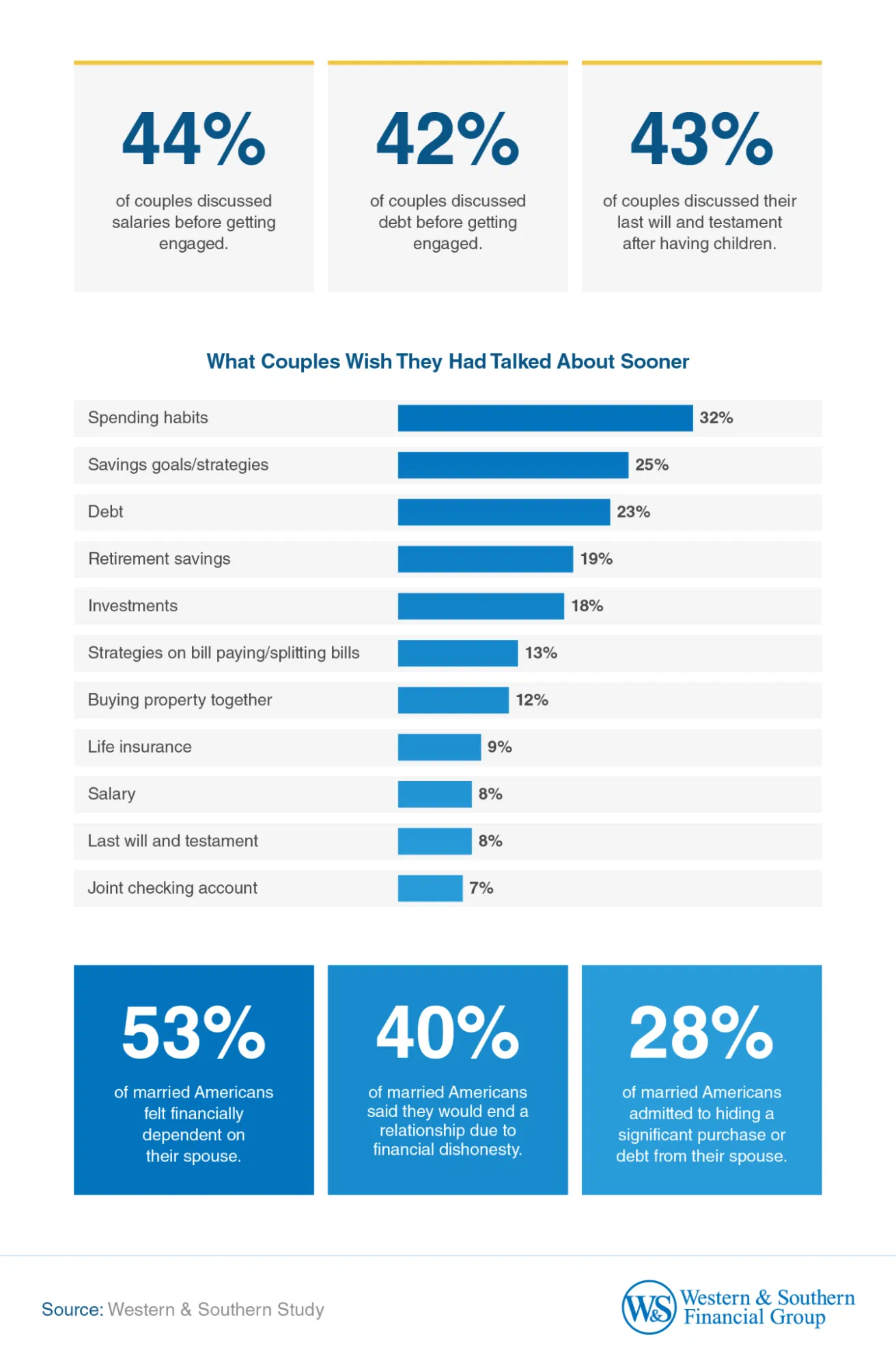

Surveys in 2025 show 45% of partners still fight over money, 28% hide debt, and financial conflict underpins ~60 % of break-ups.

What are the 5 most common budgeting pitfalls for couples, and how do we avoid these money traps?

This article was written by a Financial Horse Contributor.

1. Money-Talk Avoidance

Avoiding frank and candid money talks with your partner can only lead to disaster.

For instance, not knowing each other’s pay and bonuses, and at least a general ballpark of each other’s net worth (assets, liabilities, investments, property holdings etc.)

While not everyone wants a spreadsheet of their finances, having a clear understand of each other’s finances is vital for long-term planning.

In particular, any “surprises” such as debt.

According to HBKS Wealth Advisors, 45% of couples argue about money and 25% call it their biggest relationship hurdle.

Start small. Schedule a monthly 30-min “money date” → list income, recurring bills, joint goals.

This can become a quarterly thing once everyone is sorted on the fundamentals of the household’s finances.

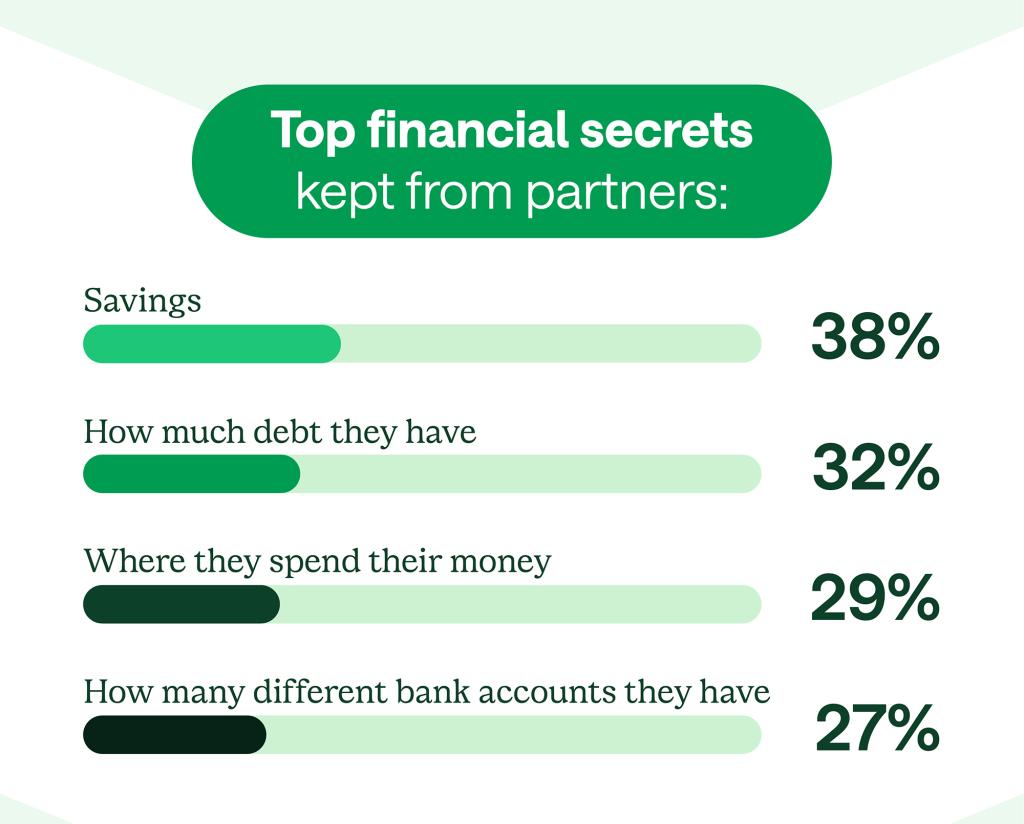

2. Financial Infidelity

Related to the above, a lack of money transparency with your spouse will quickly sink the boat.

Especially unwanted surprises like credit card debt.

According to this study, 28% of couples admit hiding major purchases or debt, and 40% would leave over money lies.

More talk = more money!

Having more transparency about each other’s finances, espeically the “bad” things, will hold each other accountable so you can meet your shared goals.

Even with a shared budget, you can also build in some flexibility.

Set a “no-questions” spending threshold (e.g., S$500) above which both must agree.\

3. Forgetting Lumpy & Irregular Costs

Having a budget is important for most households’ financial planning.

However, it is easy to overlook things.

Common misses include property tax, annual insurance premiums, CNY angbaos, kids’ additional enrichment classes.

Solution? Build a “sink fund” for annual/quarterly expenses, and automate monthly transfers into a high-yield savings account or Singapore T-bills ladder.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Financial Horse also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

4. Lifestyle Inflation & Over-Leveraging

One of the biggest risks to couples’ finances is lifestyle inflation and over-leveraging.

Before any big upgrades, do a realistic forecast of future income and stress test different situations.

Dual income → upgrade condo, car, and memberships = but does this work if the income variables change?

MAS Total Debt Servicing Ratio (TDSR) cap is 55%. Many couples edge close, leaving no safety margin.

Stress-test:

- Can this still work with a single income?

- +2% higher mortgage rates

- cap fixed outflows (loan + recurring) at 45% of take-home

5. No Emergency or Long-Term Buffers

Financial rows reportedly drive up to ~60% of marriage breakdowns.

Protect yourself with an emergency fund and long-term protection measures.

Some money buffering strategies to adopt:

- 6-month emergency fund in SSBs/MMFs.

- Annual CPF-SA top-up to lock in 4 % risk-free.

- Term insurance matching 10× joint annual spend.

Recap: Quick Checklist

- Schedule quarterly “money dates” to check-in on your net worth + expenses

- Declare all debts to each other

- Agree on spending thresholds + map annual/irregular expenses

- Hold a 6-month emergency fund

- Stress-test for income variables before considering big upgrades to lifestyle

- Keep TDSR ≤ 45 %