We’ve been doing a couple of pretty technical pieces recently (Comfort Delgro, SATS, Keppel etc).

So I figured for this week, let’s go back to basics.

Let’s do a piece for the newer investors among us. We were all beginner investors once, so there’s no shame at all in being one.

Some of you may have started in investing during the March COVID crisis earlier this year. Or maybe even before that.

Whoever you are, this piece is for you.

How to start investing in Singapore in 2020. My honest, open sharing here.

Basics: Why Invest?

There are 2 reasons to invest: (1) Wealth preservation, and (2) Grow wealth.

Preserve Wealth

If you want to preserve the value of your money, you need to invest. Simple as that.

The longer-term rate of inflation in Singapore is about 2.1%. It definitely feels higher than that with how quick prices have gone up the past 10 years.

If you put all the cash in the bank, the interest you get is lower than the inflation rate, so you’re just losing money (in purchasing power) every year.

This is really important to understand, especially for retirees. The $1,000,000 you have right now, may be worth only $500,000 in 10 years. Not because you lost money, but because the prices in Singapore have gone up. A bowl of noodles that cost $4, may cost $6 in 10 years.

So if you really want to preserve the value of your wealth, you need to invest in a broadly diversified portfolio.

Grow Wealth

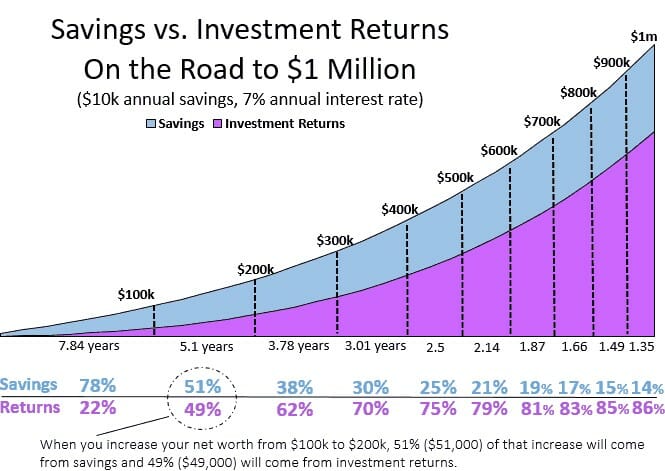

And of course, some people invest to make money. The returns start out small, but over time they really compound. If you do it right, towards the later stages of your life the bulk of your wealth comes from investing.

I pulled this chart from the FH Course to show you what it looks like.

At the start, all your money comes from savings.

At the end, all your money comes from investing.

So when you are young, focus on saving, while building up investing knowledge. It all comes in handy later on.

How to start investing?

There are 2 ways to invest.

You can either do it yourself (DIY), or you can pay someone to do it for you.

DIY

DIY investing is what the rest of this blog talks about. There’s a lot of strategy (and luck) that goes into it, but we’ll try to cover some of the basics in this article today.

If you DIY, you need a stock broker to get you access to stocks.

I have a more detailed review on stock brokers here, but basically – Recommendations are DBS Vickers Cash Upfront for Singapore stocks, and Saxo or Interactive Brokers for foreign stocks (Saxo if you’re investing small amounts, Interactive Brokers if you plan on hitting more than US$100,000).

Pay someone to do it for you

Paying someone to help you invest is what the entire fund management industry is about.

It’s a very broad spectrum of options, from cheap all the way to expensive.

On the cheaper end, you have Roboadvisors like StashAway, Endowus, Moneyowl etc.

In the middle you have things like unit trusts, where there is an active manager who invests the fund.

At the more expensive end you have endowment / investment plans that you can buy off an insurance agent.

Price doesn’t equate to performance though. Just because you pay someone more to manage your money, doesn’t necessarily mean you get better returns. Investing is funny like that.

Asset Allocation is the most important

So a lot of beginner investors obsess over individual stock picking – whether to buy DBS or UOB.

In reality though, the bulk (around 80%) of your returns come via asset allocation.

This, is how much money you put into stocks vs REITs vs private real estate vs Bonds/CPF vs cash.

For example, if you have $100,000, do you put $50,000 into stocks and the rest into REITs? Or do you split it among stocks, REITs and bonds?

The exact asset allocation has to be a personal choice. Risk and reward go hand in hand in investing. Most of the time, to get better returns, you need to take on greater risk.

If you’re someone who cannot stomach too much risk (eg. you’re a retiree), then you need to accept lower returns.

We talk about this in detail in the FH Course, but the crux is that you want to allocate some money into each of the following asset classes:

- Stocks

- REITs

- Commodities (Gold, Oil etc)

- Private Real Estate

- Bonds / CPF / Cash

Items 1 to 5 are broadly arranged in terms of risk/reward, with the most risky and highest potential returns at the top, with the bottom being the safest but lowest returns. It’s a rough guide, and there are certain situations where the order can switch, but 90% of the time, this order should hold.

For me personally, I was heavy on Bonds / Cash / Gold leading up to 2020, because I believed we were nearing the end of both the long and short term debt cycle. Once the COVID crisis hit markets in March, I gradually began rotating out of Bonds and Cash into Stocks, REITs, Gold and oil. And I will continue doing so going forward.

But really, there’s no one size fits all here. The exact mix, will depend on your personal situation, and on how you view the economy.

Lump Sum or Dollar Cost Average?

Now a lot of textbooks will tell you that over the longer term, lump sum investing gives you the highest returns.

I think that’s rubbish.

Think of it like driving a car, for beginners.

Sure, flooring the pedal and driving at 100km/h right away will get you to the destination quickest, but is that really the advice to give to a beginner driver?

It takes time to build up knowledge and confidence in markets. If you go all-in at the start, there is a good chance you blow up and lose a big chunk of that.

So my advice is to take it slow, and average in. Focus on building knowledge at the start.

With the COVID crisis playing out, there’s also big volatility in financial markets. Averaging gives you time to capitalize on the volatility.

Back to the car analogy, it’s like driving on a mountain road. Sure, you can floor the pedal and pray your driving skills hold up, but that may not end up well, because you never know what’s around the next corner.

The safer way is to go slow, even though it takes longer to reach the destination.

Local vs Foreign stocks

Whether to invest in Singapore or overseas is again a personal choice.

Some people think that Singapore is a safer market to start investing in, but I don’t necessarily agree. Both Singapore and US/China markets are equally dangerous if you don’t know what you’re doing.

Rather, focus on what you know best.

If you work in a Singapore bank and are familiar with the banking sector, that’s probably a good place to start. If you work in Micron and know the NAND Flash market like the back of your hand, you probably want to start in the US semiconductor industry. And so on.

Focus on your circle of competence when you start, then grow from there.

For me, I started out with the US market. I then moved onto Singapore markets, and then went internationally again.

But that’s my path. Find the path the works for you.

What is SGX good for?

That said, each of the markets has it’s own pros and cons, so it’s worth going through it in some detail.

The SGX (Singapore stock exchange), is good if you want to invest in mature, old world industries.

2 areas that the SGX really stands out are (1) REITs, and (2) Temasek linked companies.

REITs

Singapore is the largest REITs market in Asia excluding Japan, ranking even ahead of Hong Kong.

Singapore edges out Hong Kong because we have Temasek back in the 2000s who was able to get the Temasek Linked real estate developers (CapitaLand, Ascendas, Mapletree) to divest their crown jewels into the REIT structure. Over time, that has led to massive growth and opportunity in Singapore’s REIT market.

In Hong Kong by contrast, there was no Temasek, so the best assets are still mostly held by the property developers owned by rich families. Public shareholders lost out.

There are also tax transparency benefits thrown in (the REIT doesn’t pay any tax on rental income as long as they pay 90% to unitholders), which makes REITs a very good way to own commercial properties.

So REITs are a very good choice if you’re investing in SGX. More about REITs selection here.

Temasek Linked Companies

The other will be the Temasek Linked Companies (TLCs). The likes of DBS, ST Engineering, Singtel, Netlink, Keppel etc.

They’ve haven’t been doing so well in recent years because they’re very focused on the old-world industries, and less of the new ones like tech.

That said, we’re in a big recession now, so if you can pick the ones that will recover post-COVID, there’s still massive opportunity for gains here.

Small Caps (Penny Stocks)

Some people like to go for smaller cap / penny stocks, where you can make a lot of money very fast if you get the timing right.

Names like AEM and iFast are very popular. They are very volatile, so you can lose money as quickly as you make.

US Market

The US market is a very deep and sophisticated market. You can get growth stocks, dividend stocks, mega tech players, ETFs etc.

Whatever you want to buy, chances are you will be able to find it here.

The thing to note is the 30% withholding tax on dividends. I have a fuller guide here, but this effectively means US market makes less sense for dividend stocks.

Personally, I use the US Market mostly for capital gains style plays, because there is no capital gains tax for Singaporeans.

China Market (via Hong Kong)

The China market (via HK) is still developing, so it’s not as sophisticated as the US yet, but it will get there eventually.

For now, it’s mainly focused around banks, real estate players, and the tech giants.

China is a fast-growing economy, so just getting exposure to their companies can already be growth stocks.

Personally I like the banks and the tech players in China. Real estate is attractive too, but some of them can be played via REITs or counters listed in Singapore (eg. China REITs).

How do I do it?

For me personally, I like to use Singapore for REITs and dividend stocks. I buy the blue-chip REITs (from Mapletree or CapitaLand etc), and I buy the blue-chip dividend stocks (eg. DBS, UOB, Netlink etc).

They are very well managed, have very strong underlying businesses, and pay very decent yields outside of a recession.

But Singapore alone lacks growth, so I need to go to the US and China markets for that.

For US I mainly try to get exposure to tech software and semiconductors, and I add some stocks (like banks, oil, industrials) to get broad exposure to the US economy.

For China I like the banks and tech players. Real estate is great too, but it’s a bit bubble-ly and corporate governance can be tricky sometimes, so I prefer to play them via the Singapore listed REITs or developers.

And that would round up the equity portion (stocks / REITs) of my portfolio. Singapore forms the bulk, followed by US, and then China.

You can check out my exact portfolio breakdown on Patron if you’re interested.

How to pick Stocks / REITs?

A couple of quick notes on stock / REIT picking. In the good times you can make mistakes and not get punished too badly. But with the COVID recession in full swing, it has become really important to pick the right stocks.

My suggestion is to focus on counters with:

- Sound balance sheet to outlast COVID-19

- Resilient business model that will rebound after COVID-19.

- Ideally: Products that are loved by consumers and add value, have a competitive advantage, and good margins

- Cash flow – can’t stress this enough, cash flow is king. Look for companies with strong cash flow and not rubbish like revaluation gains (paper gains)

And, where this is not already priced into the stock. For example, Amazon fulfils all the criteria above, but you will need to decide at its current price, how much upside is left?

What about Bonds?

The problem with bonds in Singapore is that most of the corporate bonds are for accredited investors, and you need to buy them at S$250,000 each time.

This makes it hard to sneak some bonds into your portfolio.

There are retail bonds and corporate bond ETFs out there, but the retail bonds don’t come along that often, and the ETFs don’t have good liquidity or yields so it’s hard to really recommend them.

The Singapore Savings Bonds were good a year or two back when interest rates were high. They’ve dropped significantly since though, so I don’t recommend them anymore.

The way I do it is to keep my cash in high yield savings accounts like DBS Multiplier and Singlife Account (2.5% interest risk free – we just did a review on it here).

And I try to keep my CPF-OA intact as a risk free bond that pays 2.5% per annum.

That’s what I would suggest for new investors. If you get a good retail bond you can throw it in as well, but I don’t think we’ll see any for the next few years given the low yield environment we are in.

What about Gold / Commodities?

A lot of investors, even the sophisticated ones, don’t allocate to gold or commodities.

This made sense over the past 30 years which has just been a massive bull run in bonds, but going forward, such an allocation looks a bit risky.

I think that going forward, inflation may potentially make a comeback given where we are in the longer-term debt cycle.

So personally, I am maintaining exposures to precious metals (gold / silver), and commodities (oil).

I think that whatever governments may say, the only logical way out of this COVID19 recession is by printing lots of money, and injecting lots of stimulus into the economy. That’s going to reduce the value of fiat currencies. Precious Metals and Commodities will be a great hedge in such a scenario.

I shared my line of reasoning in a recent post about gold, you can read it here.

Private Real Estate

Singaporeans love investing in property.

There are 2 big benefits with property:

- Leverage – For every S$250,000 you put in, you can borrow up to S$750,000. That’s massive leverage that you would never do with stocks. So a small 2% move in real estate can be amplified to an 8% move after leverage, which really drives returns. Of course, when prices go the wrong way, you lose bigger too.

- Harder to panic sell – Stocks prices are refreshed daily. When your stocks go down, it’s really obvious. The price of your house, doesn’t necessarily change every day. If you’re underwater, you can simply ignore all property related news for a while. This makes it easier to hold onto a house even when you’re underwater, as compared to stocks. And for certain kinds of investors, this can be really important.

I shared more in depth views in a post last week. I think over the next 12 months, property prices in the private resale market will probably trend downwards. This could make it a great time to pick up a property if you’re in for the long haul.

How to Start Investing – Some tips

Some quick words of advice from me, which I wish I’d known when I first started.

A journey of a thousand miles… begins with a single step – Planning is important, but what is more important than planning, is actually doing it. There are so many beginner investors who obsess over getting the right broker, waiting for the right time, and the right stock… until they never actually buy anything. Don’t be like that. Plan what you want to do, then do it.

Be humble, know what you don’t know – The markets are a place where very smart people go to get humbled. So when you invest, always be humble. Over time, you will gradually come to realise how much there is in this world that you cannot possibly understand with certainty. A little humility goes a long way.

Always be learning – And finally, always be learning. When you invest, you will lose money. Learn from your mistakes. Understand what you did wrong, and learn from it. Stanley Druckenmiller, who ran Quantum with George Soros and has a long term track record of about 30% returns a year annualized, recently admitted to being completely wrong on the market reaction after March’s crash. If even legendary investors like that get it wrong, accept that you will get it wrong too. Don’t be too hard on yourself, but always learn from your mistakes.

The best investors I found were always asking questions. They’re always curious, always trying to find out more about the world around them. Never stop learning.

How to learn more?

Now for obvious reasons, the above was just a very brief guide on how to start investing in Singapore in 2020. There is no way to cover everything you need to know in a 2000-word post.

If you want to learn more, the FH Course or REITs MasterClass are great places to start.

FH Course

The FH Course is for beginner investors who want to learn the basics and fundamentals of investing. If you are new to investing, or have anywhere from one to five years’ experience investing, this is a great choice.

In the FH Course, you’ll learn about Asset Allocation, Understanding the Market Cycle, REITs, Property Investing, Shares, ETFs, Bonds & Fixed Income, CPF & Tax Planning, and how to put an entire portfolio together.

REITs MasterClass

The REITs MasterClass is for intermediate/advanced investors who already know the basics, and want to take their REIT and real estate investing to the next level. It’s laser focussed on REITs and real estate investing, and teaches you the ins and outs of real estate as an asset class.

In the REITs MasterClass, you learn about how to invest in REITs v Dividend Stocks v Growth Stocks, Statistics & Probabilities & Randomness, how to pick good real estate, how to read the global macro climate, how to pick REITs and know which to avoid, how to build a real estate portfolio, how to decide on the price to buy REITs, and more.

If you’re new to investing, I think both of the above are great ways to build your investing knowledge. Find out more here, or sign up via the links below.

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the Stocks Investing Masterclass or REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Just curious, in the local vs foreign stock, why did you use Micron in the example? And why NAND flash? Most of Micron’s operating profits came from DRAM: https://www.fool.com/investing/2019/02/09/how-micron-tech-makes-money-nand-dram.aspx and https://www.investopedia.com/how-micron-makes-money-4797985

No reason in particular. You’re right, the bulk of Micron’s revenue and profits are from DRAM, with NAND as a second.

A good summary, a good reminder

Glad you find it useful!

Really well thought out points, I always enjoy reading your articles!

Thanks! Glad you find them useful. 🙂