It’s almost the new year.

Time for a quick dust-up, round-up to get your finances in order before the new year.

This article was written by a Financial Horse Contributor.

1) “Use-it-or-lose-it” tax reliefs (deadline: 31 Dec 2025)

A. CPF Cash Top-Ups (RSTU / MA)

- Relief cap (cash top-ups): $8k (self) + $8k (family) per YA; subject to the $80k total personal relief cap and the CPF Annual Limit $37,740.

- Practical: If you and your spouse/parents are in different tax bands, run the numbers—often topping up a parent’s RA/MA yields higher household savings.

B. SRS (Supplementary Retirement Scheme)

- Contribution cap: $15,300 (SG/PR) or $35,700 (foreigners).

- Contribute by 31 Dec 2025 to reduce YA2026 taxable income (still subject to the $80k overall cap).

C. Charitable giving (IPCs)

- 250% tax deduction remains in force through 31 Dec 2026 (current policy). Donations auto-transmit to IRAS.

Check the $80k relief cap before topping up. Model your CPF Annual Limit (salary + bonus CPF + any voluntary top-ups) to avoid reversals.

2) Park idle cash smartly

Segment your cash:

- 1–3 months expenses → high-yield savings.

- 3–12 months → 6-month T-bill ladder / SSBs rolled monthly.

- >12 months → short-duration bond funds or term deposits (rate-shop).

Execution tip: Put MAS auction dates in your calendar; roll maturing T-bills into the next auction automatically.

3) Optimise CPF across the family

Suggested sequence:

- Top up MediSave (MA) to BHS first.

- MA is versatile (pays MediShield/IP/riders, hospital bills).

- When MA is at Basic Healthcare Sum (BHS), future mandatory CPF “overflow” can channel to SA (<55) or RA (≥55), compounding at higher rates.

- Then top up SA/RA (RSTU).

- Your SA (<55) acts like a “super-bond.”

- Parents’/grandparents’ RA top-ups can meaningfully boost lifelong payouts.

- Voluntary Housing Refund (OA).

- If you used OA for housing, refunding voluntarily cuts accrued interest and rebuilds OA.

- Think of it as earning the OA rate, risk-free, by paying yourself back.

Note:

- Track the CPF Annual Limit ($37,740) with your year-end bonus in mind.

- Don’t overfill MA above BHS (excess gives you no extra benefit and may cause reversals).

4) Lock in 2026 automations now

- GIROs for income tax, property tax —smoother cashflow, fewer penalties.

- Auto-invest DCA into your core ETF(s)

Rules-based alerts:- “Bank bonus criteria met?” on the 25th monthly.

- “Miles/points expire?” quarterly.

- “SRS deploy?” monthly if your SRS is sitting in cash.

5) Insurance: boring but essential

Annual coverage check: term life, CI, TPD, H&S (IP + rider).

Ensure the emergency fund covers deductibles/co-pays (so you don’t sell assets at bad prices).

Price-shop riders; remove overlaps (e.g., employer plan + your own).

6) Estate planning — the no-drama version

The goal is to make it simple and drama-free for loved ones to access money and follow your wishes.

- Will

- Name an executor, list beneficiaries plainly, include a simple asset locator (banks/brokers/policies).

- Get it done with a lawyer so there is no dispute.

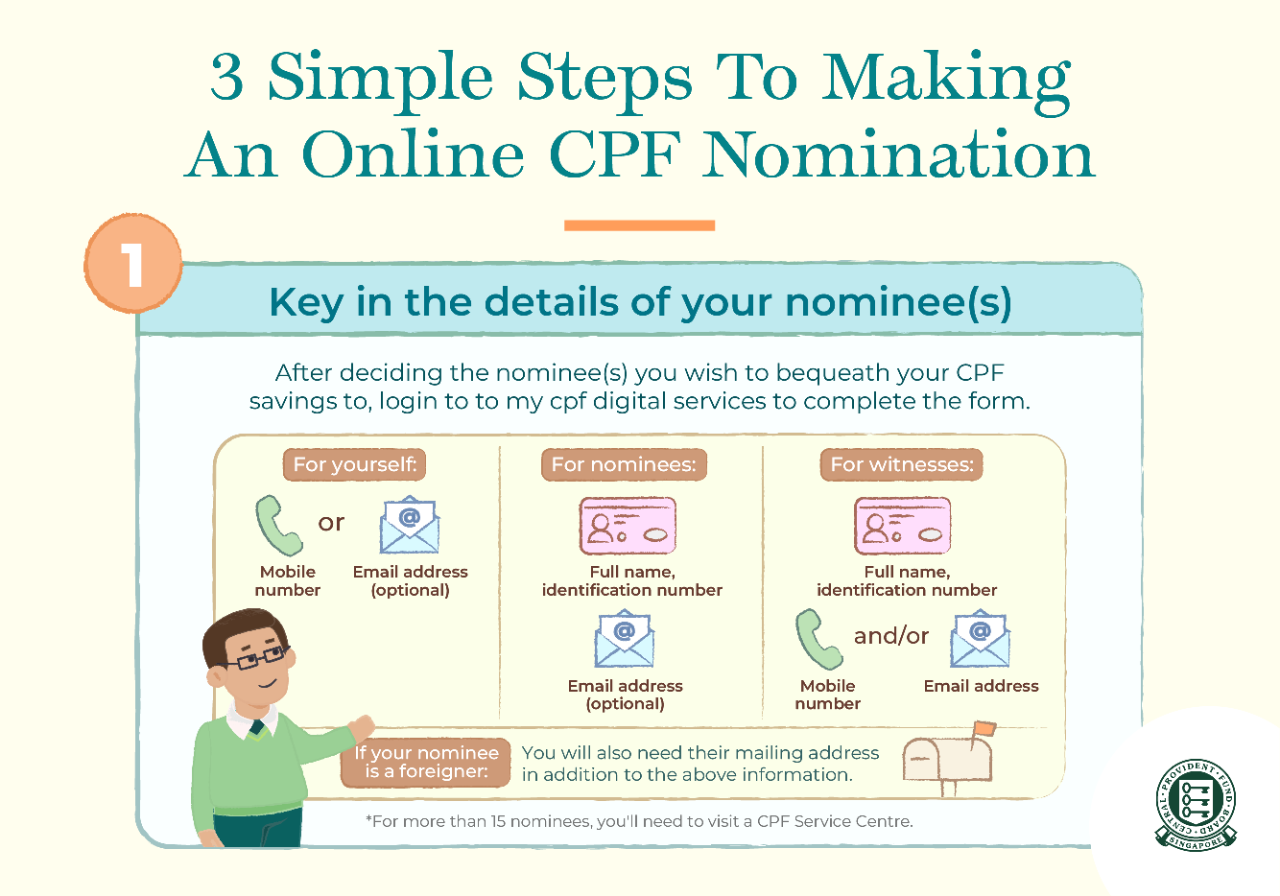

- CPF Nomination (5 minutes).

- CPF doesn’t follow your will. Set/update nomination with clear percentages.

- CPF doesn’t follow your will. Set/update nomination with clear percentages.

- Insurance nominations.

- Confirm each policy’s nominee. Decide trust vs revocable nomination deliberately.

- Confirm each policy’s nominee. Decide trust vs revocable nomination deliberately.

- Letter of Wishes

- Kids/guardianship preferences, where documents live, password manager access, funeral notes.

- Store with your will; share with the executor.

7) Small leaks can sink a big ship

An annual budget check sets you up for success in the new year.

Find the zombies (subscriptions, apps, memberships).

- Tag your Top 5 by cost → keep, downgrade, or kill.

- If unsure, use a 30-day snooze: cancel now; re-subscribe only if you truly miss it.

Utilities & telco quick switch.

- Match real usage (kWh/GB) to new-customer promos.

- If the breakeven is < 6 months, switch. Calendar the new contract end date.

Brokerage & banking clean-up.

- Consolidate to keep it simple and maintenance low.

- Close dormant accounts (fees + fraud risk).

- Keep 2–3 cards aligned to your spend; cancel the rest to avoid annual fees and mental clutter.

8) A one-page IPS for 2026

Why one page? Because you’ll use it. Long plans live in drawers.

Fill these six boxes:

- Goals (dated, sized): “$X downpayment in 2027,” “$Y passive income by 2032,” “$Z tuition fund by 2035.”

- Risk budget: “Max drawdown I can tolerate without selling: −20%.”

- Target mix: e.g., 60–70% global equities, 15–25% bonds/SSB/T-bills, 5–10% REITs, 0–5% speculative; rebalance triggers = ±5% or ±20% of position weight.

- Allowed products & fee ceiling: list tickers/brokers; “All-in product cost ≤ 0.40% p.a.”

- Playbooks (pre-commitments):

- If S&P −30%: deploy 3 tranches (−10/−20/−30%) using cash/T-bills maturing <6 months.

- If SG REITs −20%: rotate to strongest balance sheets at ≤1.0× P/B.

- If T-bill <2%: move 50% of maturing ladders to short-duration IG bond fund.

- What I’ll never do: no options unless fully collateralised; no >10% in any single stock; no leveraged tokens/CFDs.

Thank you for the useful playbook, very helpful tips condensed into point form.

What IG bonds would you recommend? As the current Tbill rates are quite low.

Btw I think there are some typos in your One Page IPS 2026 diagram.

I would probably just use a SGD hedged bond fund. Something like PIMCO GIS for example.

Provides diversification, and you don’t need to be an AI to access.