Since it’s high of 2.9 at the start of the year, Ascendas REIT has plunged 16% due to a combination of (a) the Iran war and (b) a poorly timed equity fundraise.

That said, when life gives you lemons, make lemonade.

The flip side of this, is that this is an interesting opportunity to accumulate one of Singapore’s largest industrial REITs.

A couple of you have reached out for my views on Ascendas REIT and the preferential offering, so I wanted to share latest views in this article.

Full Disclosure – I hold a position in Ascendas REIT.

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Ascendas REIT drops 16% since January 2026

How quickly fortunes change.

Ascendas REIT was trading at $2.9 in January 2026.

By March 2026, Ascendas REIT was trading as low as $2.44 – a sharp 16% drop in share price.

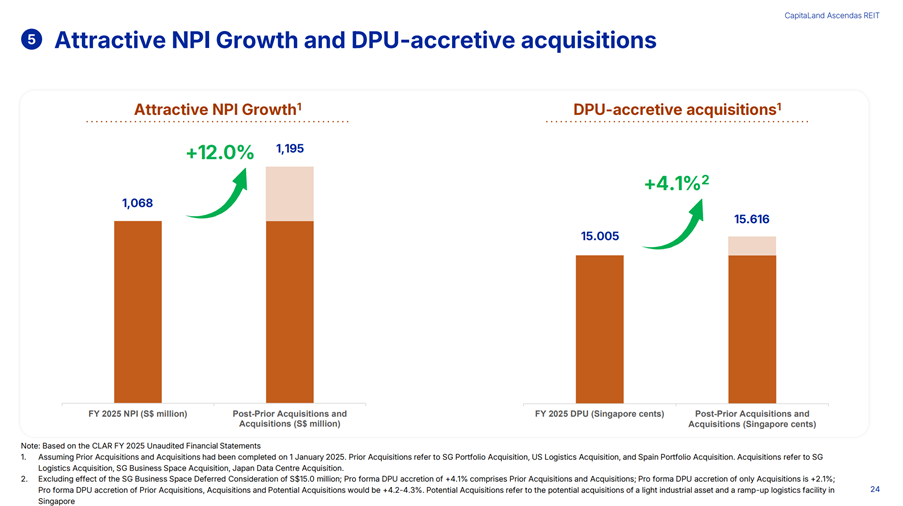

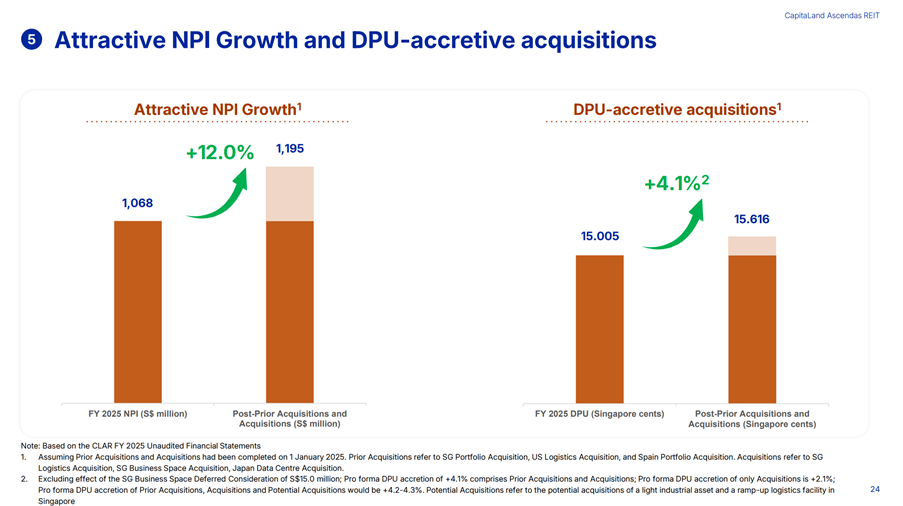

Using the pro forma DPU of 15.6 cents – Ascendas REIT at current share price trades at about a 6.2% dividend yield.

In a climate where the 6 month T-Bill trades at 1.38% – that’s actually pretty attractive being a 4.8% yield spread.

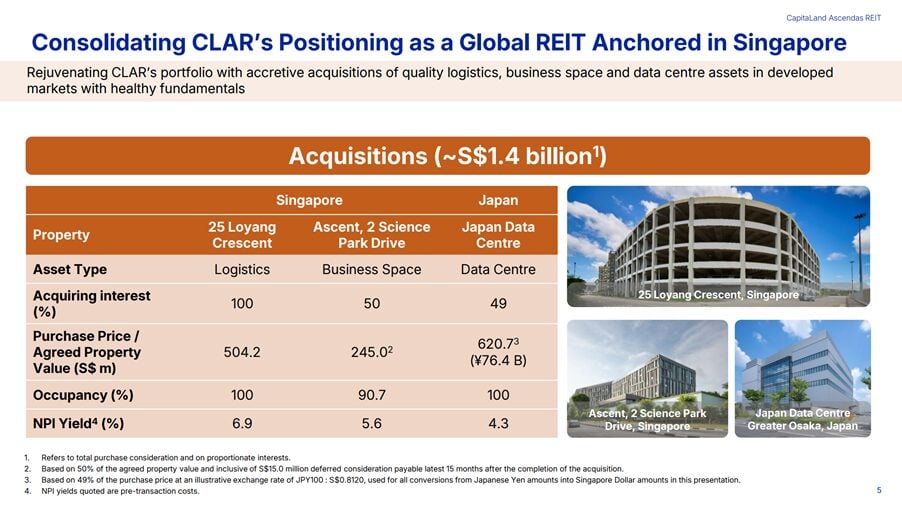

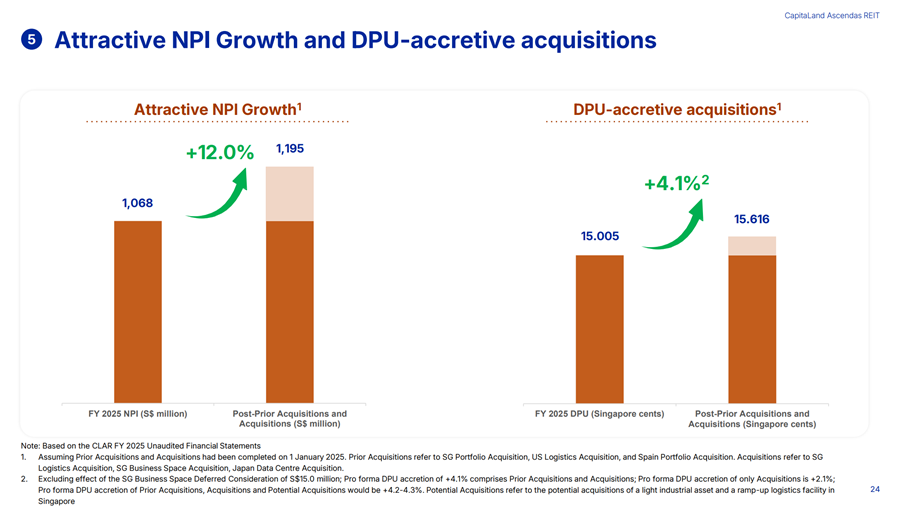

What is Ascendas REIT buying?

So why does Ascendas REIT need the funds?

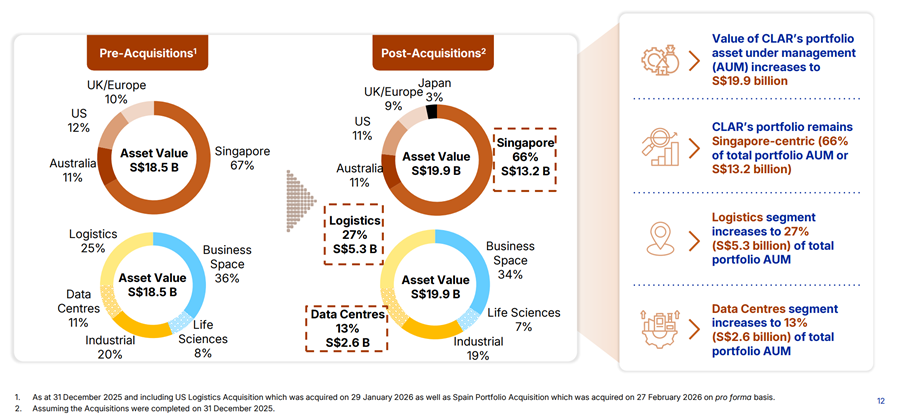

Well – they are buying 2 industrial properties in Singapore, and 1 data centre in Japan.

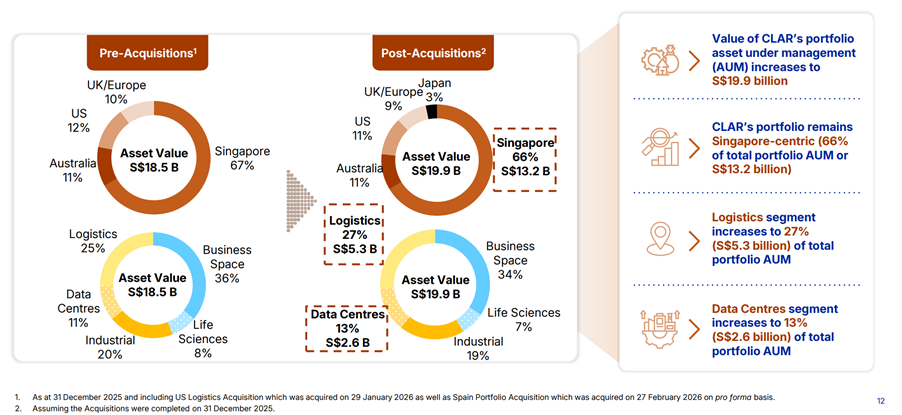

Big picture wise, because their portfolio size is so huge ($19.9 billion after acquisition), this acquisition doesn’t fundamentally change the composition of their property base.

Even after the acquisition, the bulk of Ascendas REIT’s assets is Singapore properties at 66% of the asset base.

And data centres remains a small segment of the overall portfolio at 13%.

Is it a good acquisition for Ascendas REIT?

The acquisition is DPU accretive to the tune of 4.1%.

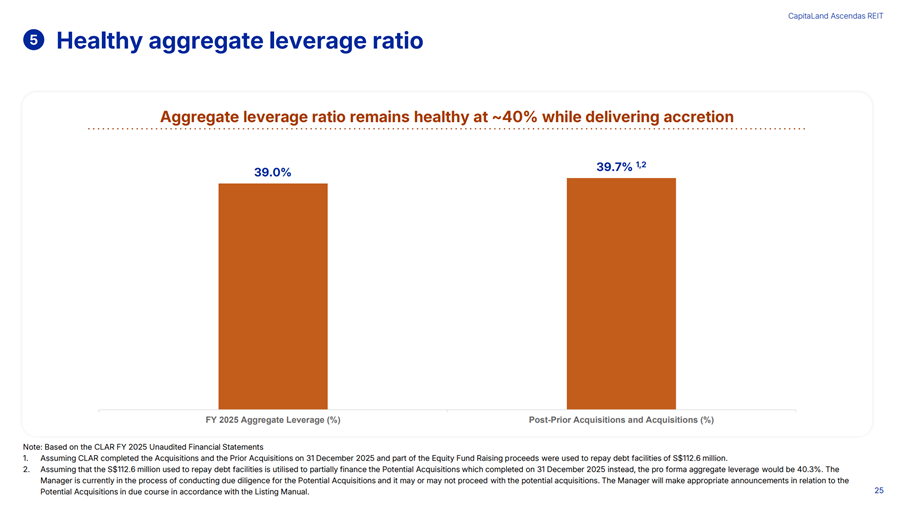

That said post-acquisition the leverage ratio goes up to 39.7%.

That does look on the high side, as after REITs were burnt by the higher interest rates most of them look to run lower leverage ratios these days.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

My Personal Views on the acquisition

Personally I see this as a pretty run of the mill transaction.

REIT managers are incentivized to do deals and grow AUM, so as a REIT investor this is part and parcel of investing in REITs.

The current deal doesn’t fundamentally change the risk profile of Ascendas REIT as it remains predominantly Singapore industrial assets.

And the acquisition is DPU accretive so it’s not like management is destroying shareholder value.

All in, a pretty run of the mill transaction and nothing in particular jumps out at me.

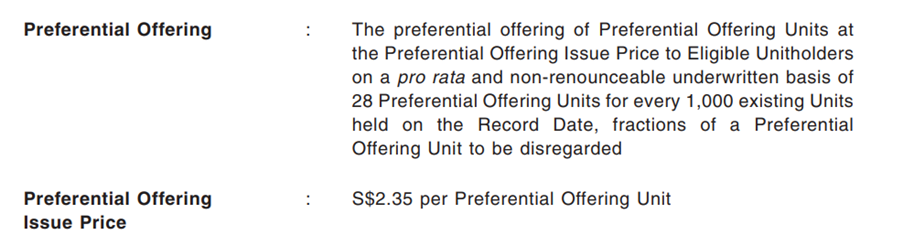

Preferential Offering Details – $2.35 per unit, 28 pref units per 1000 held

To finance the acquisition, Ascendas REIT is doing a preferential offering.

Investors get 28 preferential units per 1000 held.

And units are issued at $2.35.

That’s about a 7% discount to the latest market share price of $2.52, so it is actually pretty meaningful.

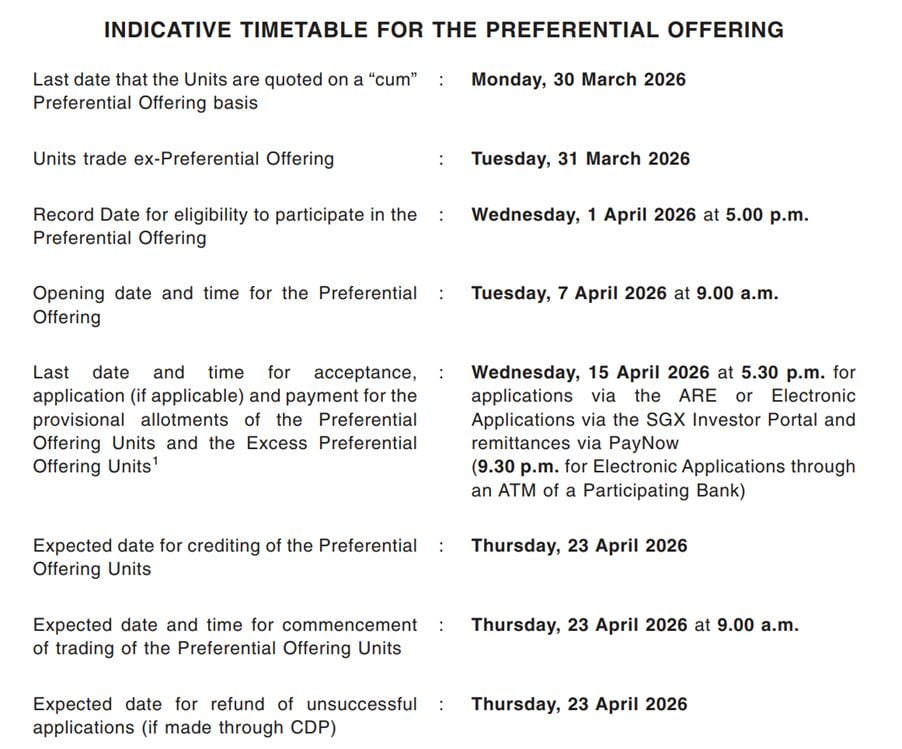

The Preferential Offering is open on 7 April, and closes on 15 April.

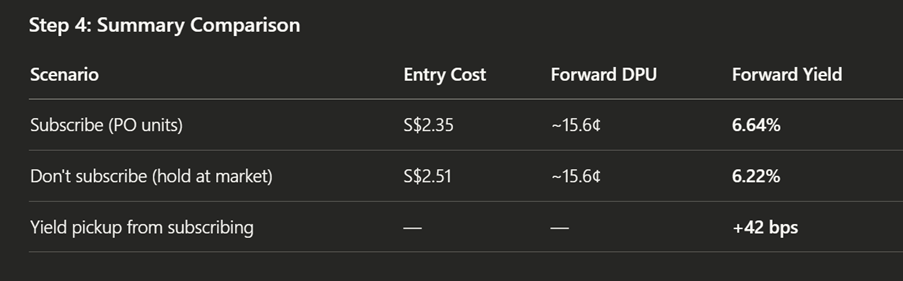

Forward dividend yield of 6.6% at preferring offering price

Running the numbers using the pro forma 15.6 cents DPU.

If you subscribe, you’re effectively buying in at an estimated 6.6% dividend yield.

While if you just buy the units on the market today, you’re only buying in at a 6.2% dividend yield.

Will I subscribe for the preferential offering at 6.6% dividend yield?

At the start of the year, I said that I saw myself as buying less REITs in 2026.

But that was because REIT prices at the start of the year were near cycle highs, and yields were not attractive.

3 months later – all that has changed.

And when prices (and facts) change, I change my mind.

At current prices, I find REITs a much more decent buy.

For Ascendas REIT’s preferential offering in particular, I find it a no brainer.

This is a core REIT position for me, and this is an opportunity to accumulate at 6.6% dividend yield, and a 7% discount to the market price (after a meaningful sell-off).

So yes, I will be subscribing for Ascendas REIT’s preferential offering, and I will likely be applying for excess rights as well.

Love to hear what you think though!

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.