One big question I get on Financial Horse is whether to invest in REITs, or to buy a rental property.

So I wanted to crunch the numbers today and try to answer the question.

If you’re a Singapore investor with S$1 million in cash, should you buy a portfolio of REITs… or a rental condo?

Which buys more “freedom” over a 10 year timeframe?

What do we mean by “freedom” over 10 years?

I’ll judge the options on four levers:

- Cash-flow freedom – steady income you can live on.

- Time freedom – how many hours of hassle it creates.

- Flexibility – liquidity and flexibility if life changes.

- Sleep-well risk – concentration, policy and rate risks.

Now the analysis is a bit long.

So I figured I would start with a summary, and then dive into the full breakdown below.

Quick summary – Buy REITs or Rental property?

Full analysis below.

But high level, based on the numbers and analysis, I think a diversified REIT portfolio is *probably* the better default if your goal is freedom—steady cash you can spend, minimal admin, and the flexibility to sell and get your cash back without a lengthy sale process / transaction fees.

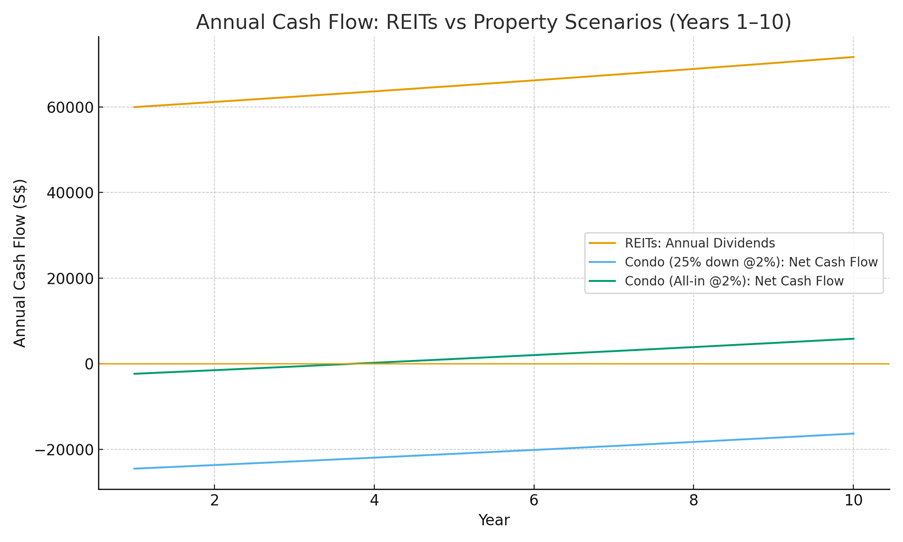

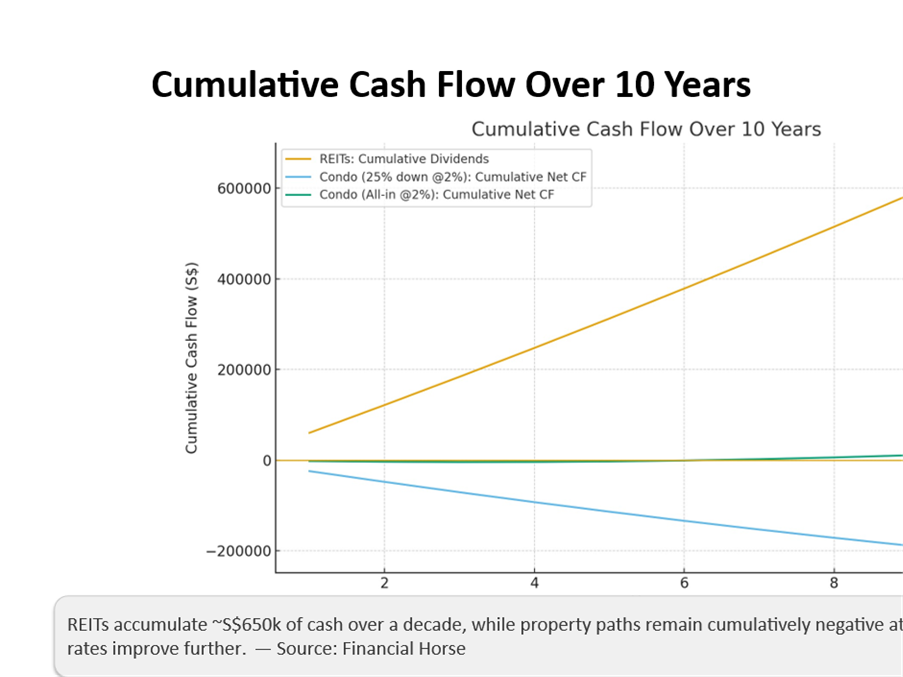

With S$1m, REITs throw off ~S$60k in Year 1 (growing towards ~S$70k by Year 10) and ~S$650k cumulative cash over the decade, while keeping your capital liquid.

The problem of course, is that you’re exposed to capital market cycles, so you need to be comfortable with the market volatility, and not panic sell if your REITs drop in price.

The rental-condo path only works on a different promise—equity later—and even then you’re likely cash-flow negative for years unless you (i) avoid ABSD, (ii) borrow near 2%, and (iii) deploy the full S$1m into the purchase so the loan is small.

In that best case you get close to cash-flow breakeven by mid-decade and end with ~S$1.6m net equity—but you’ve traded away time, flexibility, and a safety buffer.

The benefit with property though, is that if property prices perform very well you could see decent upside after 10 years.

Or if you’re the kind that is prone to panic selling in a market crash, the property is not marked to market daily and harder to sell, so this could make it easier to hold.

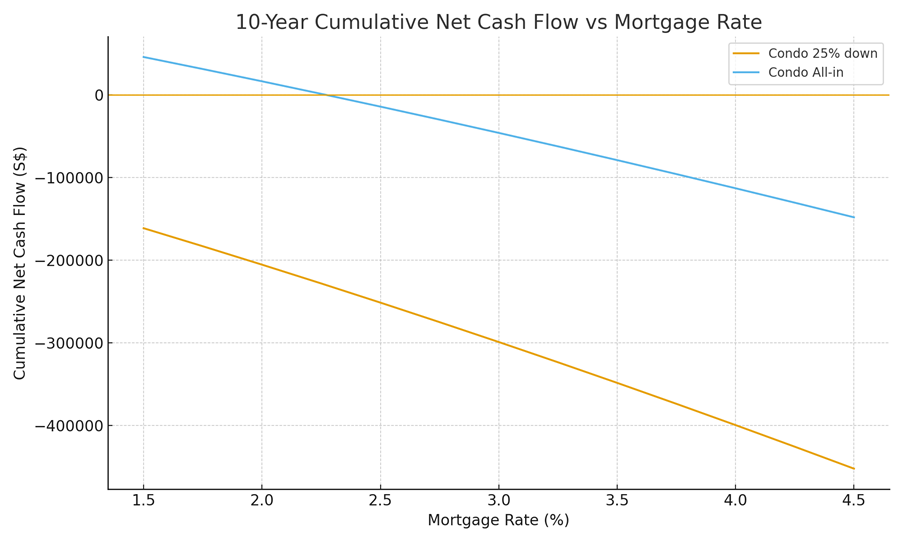

But with property, you do need to be very careful with mortgage rates.

If mortgage rates start to go up again, and rentals do not, things could get pretty hairy.

Let’s run through the numbers for each of the options below.

Path A: S$1 million into REITs

Let’s start with the straightforward one.

Invest $1 million into a basket of diversified REITs.

Assuming:

- 6% starting yield

- 2% dividend growth p.a.,

- 0–1% price growth.

- Dividends tax-exempt for individuals.

Then the numbers look roughly like the below:

- Year 1 income: S$60,000.

- Year 10 income (with 2% growth): ~S$71k.

- 10-year cumulative dividends (no reinvestment): about S$650k.

- Capital value after 10 years:

- Flat prices: ~S$1.0m.

- 1% p.a. growth: ~S$1.105m.

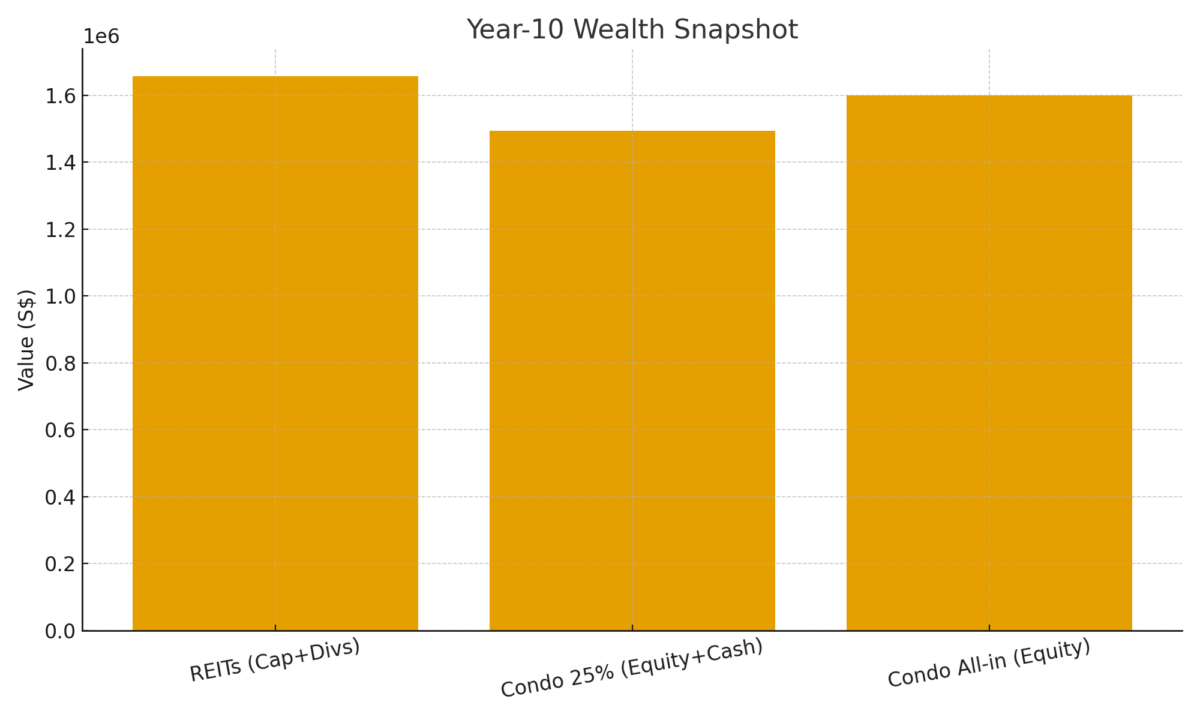

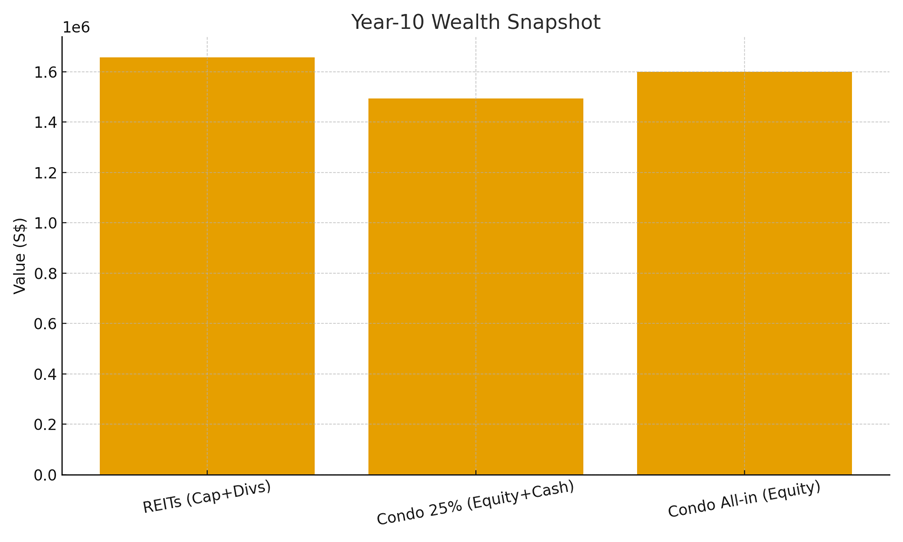

- Total Value after 10 years (capital + dividends): ~S$1.65–1.76m

What this feels like for the investor?

- Cash-flow is positive from day one.

- You can scale up/down easily, and sell a slice without moving house or calling a contractor.

- BUT – Mark-to-market volatility is real (you’ll see red and green daily), and if markets plunge you will feel the pain.

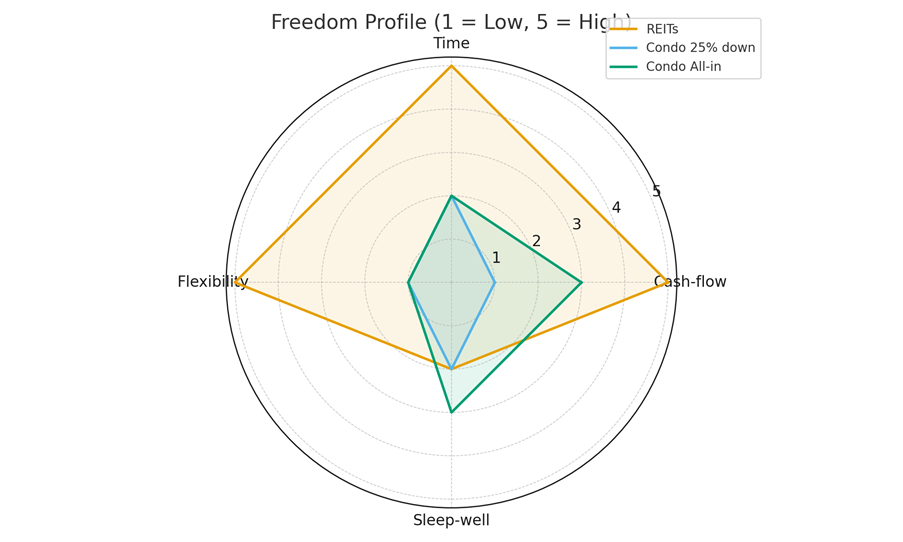

Freedom score:

- Cash-flow freedom: High (income now).

- Time freedom: Very high (click to buy/sell, no physical real estate to manage).

- Flexibility: Very high (liquidity).

- Sleep-well risk: Poor (market volatility, REIT leverage, sector cycles).

Path B: Buy a Rental Property

What about if you buy a rental property?

Assuming you buy a $2 million rental property today, there’s 2 ways you can do this.

The first is to pay the minimum 25% down payment and finance the rest via a loan.

The second is to use the full $1 million to pay the property, and only borrow the rest.

We discuss both approaches below.

(I am assuming this is the first property because once you factor in ABSD, the returns are pretty terrible).

Path B: Buy a Rental Property (Pay minimum 25% deposit)

- Condo Rental (Private, 2BR mass-market): Purchase S$2.0m.

- Financing: 25% down (S$500k), 30-year loan on S$1.5m @ 2.0% average interest.

- Upfront costs: Buyer’s stamp duty + legal/reno ≈ S$100k (round figure).

- Gross rental yield: 3.2% on property value (S$64k/yr).

- Vacancy/expenses (property tax, condo fees, maintenance, leasing): Net-off ~1/3 of gross and allow ~5% vacancy ⇒ net yield ≈ ~2.1% (≈ S$42.6k/yr initially).

- Rent growth: 2% p.a.

- Price growth: 2% p.a. (base case).

- Transaction costs on exit: Agent + legal ≈ ~2%+ of sale price.

Upfront cash used

- Downpayment S$500k + costs ~S$100k ⇒ ~S$600k.

- Cash buffer left from your S$1m: ~S$400k.

Annual cash-flow (starting)

- Mortgage payment (30yr @ 2% on S$1.5m): ~S$66.5k/yr (≈ S$5,544/mth).

- Net rent (after costs & vacancy): ~S$42.6k.

- Net carry: ~–S$23.9k/yr (still negative, but far better than –S$41k at 3.8%).

- Even by Year 10, net rent (S$66.5k). Cash-flow breakeven only around Year ~24.

Over 10 years

- Total rent collected (2% growth): ≈ S$466k.

- Total mortgage paid (principal + interest): ≈ S$665k.

- Net cash carry (top-ups): ~–S$199k over the decade

- Cash buffer left after funding top-ups: ~S$200k of the original S$400k.

- Outstanding loan after 10 years: ~S$1.096m

- Property value @ 2% p.a.: ~S$2.438m.

- Gross equity: ~S$1.342m.

- Total Return (including the $200k cash): ~S$1.493m net equity (≈ S$1.49m).

What this feels like for the investor

- Negative carry persists for many years, just smaller.

- Same concentration risk and admin (tenant turnover, maintenance, viewings).

- Leverage works faster at 2%: amortisation is quicker, equity compounds more.

Freedom score

- Cash-flow freedom: Low initially (still negative).

- Time freedom: Low-to-Moderate (repairs, agents, viewings unchanged).

- Flexibility: Low (lumpy, slow exit, frictional costs unchanged).

- Sleep-well risk: Slightly better (smaller cash burn; faster equity), but still concentrated + policy/rate reset risk.

Path B (All S$1m into the Property; Mortgage the Remainder)

Now what if you use the full $1 million and invest into the property?

This is what the rough numbers look like:

Upfront cash used

- S$1.0m (S$900k down + ~S$100k costs).

- Cash buffer left from the S$1m pot: S$0 (you’ll fund top-ups from salary/other assets).

Annual cash-flow (starting)

- Loan size: S$1.0m.

- At 2.0%: Mortgage ≈ S$48.8k/yr; Net rent ~S$42.6k ⇒ ~–S$6.2k in Year 1; ~+S$2.1k by Year 10. Breakeven ~Year 8.

Over 10 years

- Total net rent (2% growth): ≈ S$466k.

- Total mortgage paid: ~S$488k.

- Cumulative net carry (top-ups): ~–S$21k.

- Outstanding loan after 10 yrs: ~S$804k

- Property value @ +2% p.a.: ~S$2.438m.

- Gross equity (value – loan): ~S$1.634m

- Net equity after selling costs (~2%): ~S$1.60m

What this feels like for the investor

- You’ve eliminated the buffer, so negative carry must come from income/other cash.

- 2.0%: Near breakeven out of the gate; mild top-ups early, then small surplus by ~Year 8–10.

Freedom score

- Cash-flow freedom: Moderate at 2.0% (turns positive mid-decade).

- Time freedom: Low-to-Moderate (repairs, agents, viewings still apply).

- Flexibility: Low (lumpy, slow exit, frictional costs).

- Sleep-well risk: Better than the higher-loan cases (smaller mortgage, faster equity build), but no cash buffer = tighter liquidity.

10-Year Scoreboard (Context vs REITs)

Summing up the 3 positions below:

REITs

Cumulative dividends: ~S$650k

End capital: S$1.0–1.105m

Total economic value (capital + dividends): ~S$1.65–1.76m

Cash-flow now: Strong positive from Day 1

Condo @ 2% (25% upfront)

Net equity after sale (after costs): S$1.49m

Net cash carry over 10 yrs: ~–S$199k

Condo (all-cash + remainder mortgage):

At 2.0%: Net equity ~S$1.60m;

Net cash carry over 10 yrs ~–S$21k (near breakeven decade).

My personal take – Buy REITs or Rental property?

Personally, I think a diversified REIT portfolio is *probably* the better default if your goal is freedom—steady cash you can spend, minimal admin, and the flexibility to sell and get your cash back without a lengthy sale process / transaction fees.

With S$1m, REITs throw off ~S$60k in Year 1 (growing towards ~S$70k by Year 10) and ~S$650k cumulative cash over the decade, while keeping your capital liquid.

The problem of course, is that you’re exposed to capital market cycles, so you need to be comfortable with the market volatility, and not panic sell if your REITs drop in price.

The rental-condo path only works on a different promise—equity later—and even then you’re likely cash-flow negative for years unless you (i) avoid ABSD, (ii) borrow near 2%, and (iii) deploy the full S$1m into the purchase so the loan is small.

In that best case you get close to cash-flow breakeven by mid-decade and end with ~S$1.6m net equity—but you’ve traded away time, flexibility, and a safety buffer.

The benefit with property though, is that if property prices perform very well you could see decent upside after 10 years.

Or if you’re the kind that is prone to panic selling in a market crash, the property is not marked to market daily and harder to sell, so this could make it easier to hold.

But with property, you do need to be very careful with mortgage rates.

If mortgage rates start to go up again, and rentals do not, things could get pretty hairy.

If I had $1 million to invest, which buys more Freedom over 10 Years?

Ultimately, everyone’s personal situation is different.

But if this were me?

I think I would start with REITs as the income core.

Add property only when the stars line up (no ABSD, good micro-location with real rental depth, mortgage near 2%, and I’m comfortable locking in time and liquidity).

Alternatively, a hybrid approach may work too.

Put S$600k into REITs for income, keep S$400k for a smaller/more efficient unit (or a Shoebox in a higher-yielding locale) to reduce negative carry.

Love to hear what you think though!

If you had $1 million to invest – would you buy REITs or a rental property?

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Nice post. Love to see a follow up of which REITs/ etf / funds to put the $1M in.

Sure! Let me think about this.

can you comment on centurion accommoodation reit IPO?

Wrote a full article on this here, let me know if any questions!

https://financialhorse.com/centurion-accommodation-reit-ipo-review-will-i-buy-this-8-1-dividend-yielding-worker-and-student-accommodation-reit/

This analysis, in my humble opinion, misses out on a key factor Taxes. Rental income is taxed, and if you have a 1Million to spare, you will probably be in 10-15% + income tax bracket

Also, you have to add in the non-owner-occupied property tax ( 4-6%). Both combined will result in a 15-20% reduction in income for the hard property, making it an economically worse decision.

That’s fair – good point.

Thank you very much for the insights, pondering over the same thing. Enjoyed the ‘Freedom Score’ and math crunching examples.

Glad you found it useful!