As many of you probably know by now.

We’re getting a new REIT IPO.

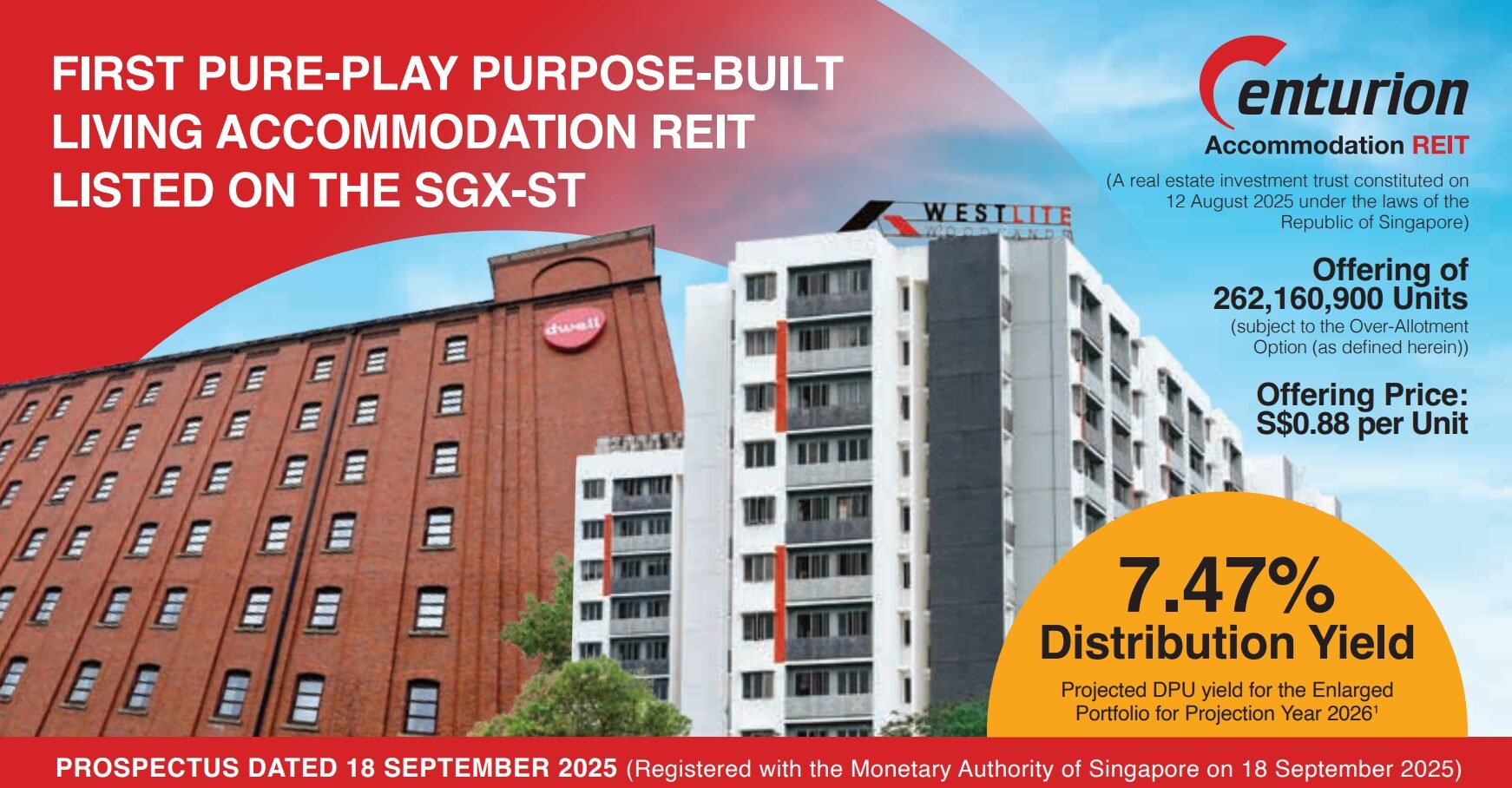

Centurion Accommodation REIT – spun off from Centurion Corp, holding primarily Workers Accommodation, but with some Student Accommodation thrown in as well (this would be the first of its kind in Singapore).

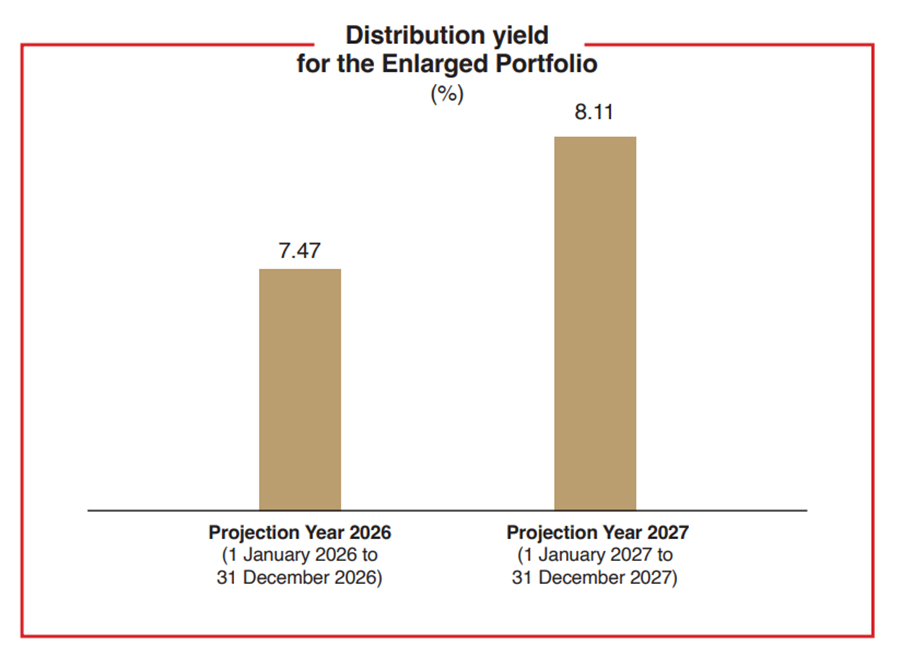

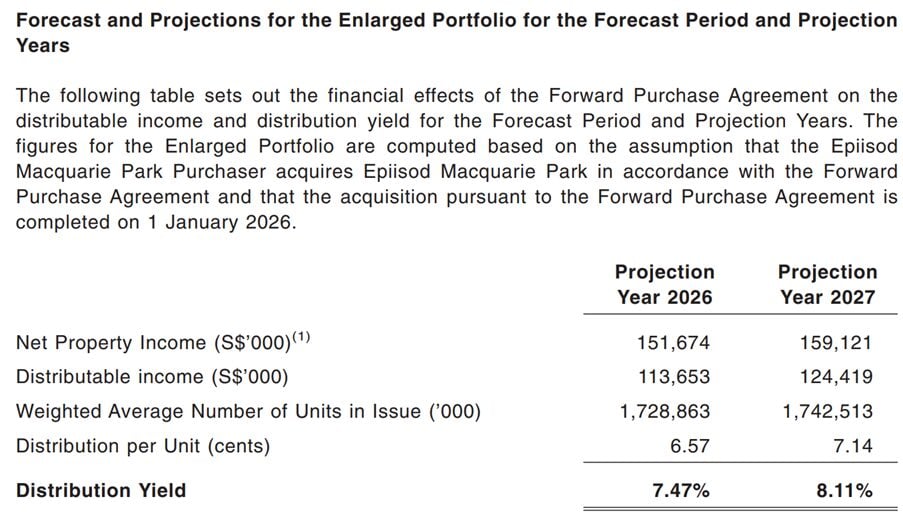

Projected 7.47% dividend yield for FY26, and 8.11% dividend yield for FY27.

I’ve been getting a lot of questions for my views on Centurion Accommodation REIT.

So let’s go.

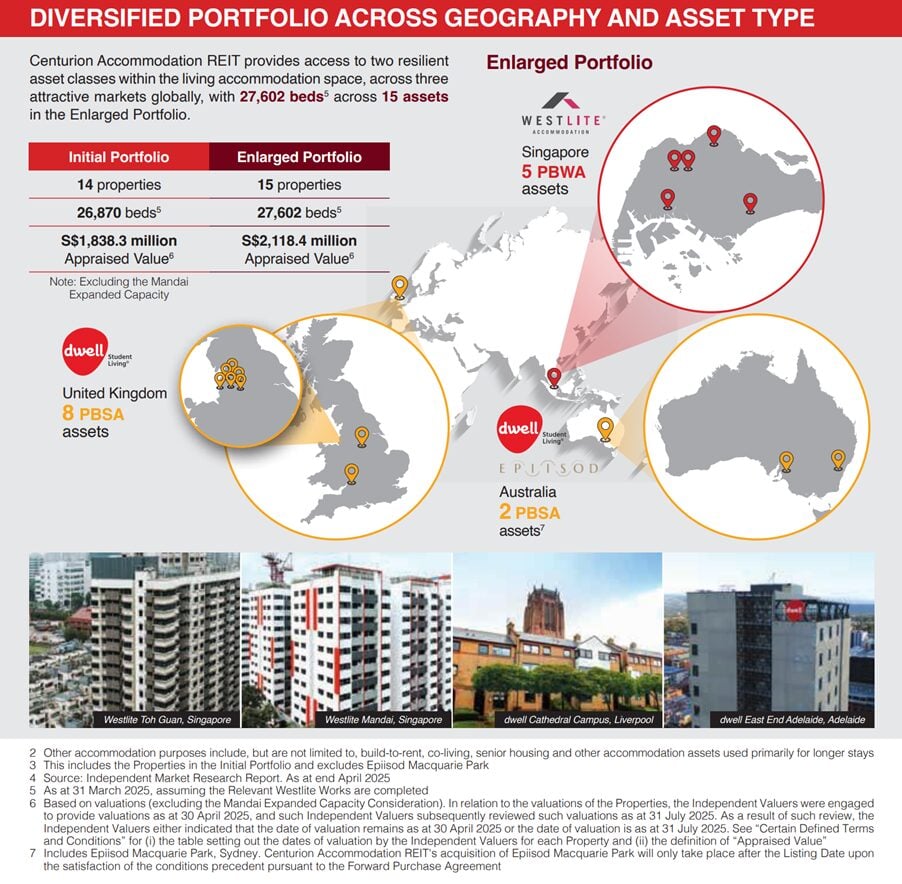

Property Portfolio of Centurion Accommodation REIT

The full prospectus is here for those who are keen.

Initial portfolio is:

- 5 workers accommodation in Singapore

- 8 students accommodation in UK (Manchester, Liverpool, Nottingham)

- 2 students accommodation in Australia (Sydney and Adelaide)

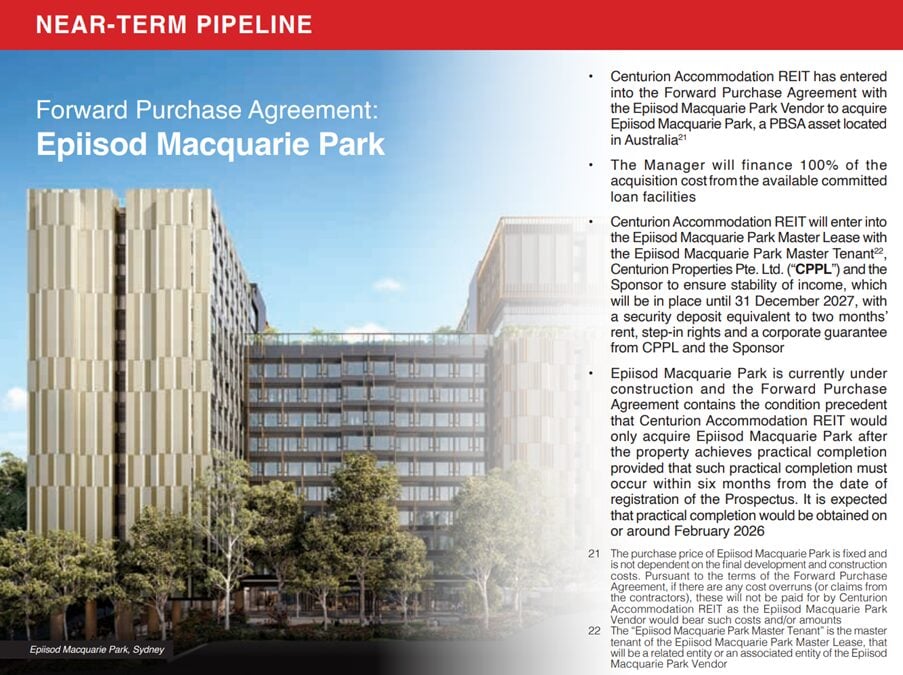

The way it works is that there is an initial portfolio of assets, and then the Australian Student Accom (Sydney – Epiiisod Macquarie Park) will be injected once it is completed – currently anticipated to take place on Feb 26.

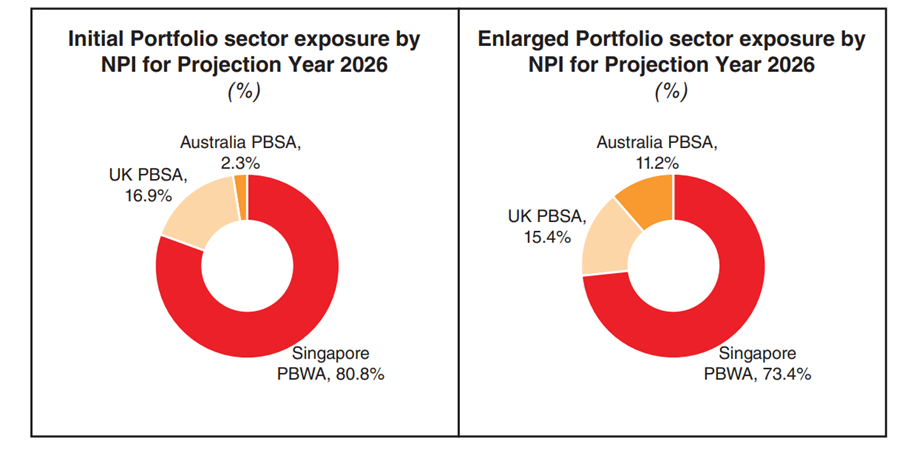

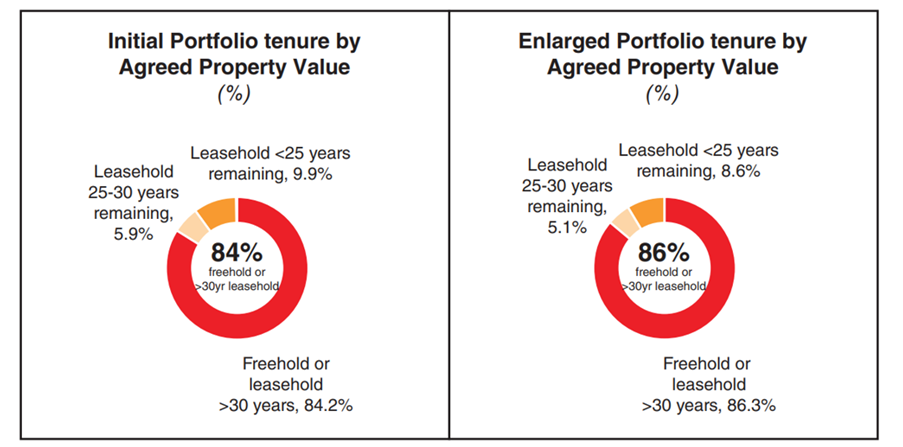

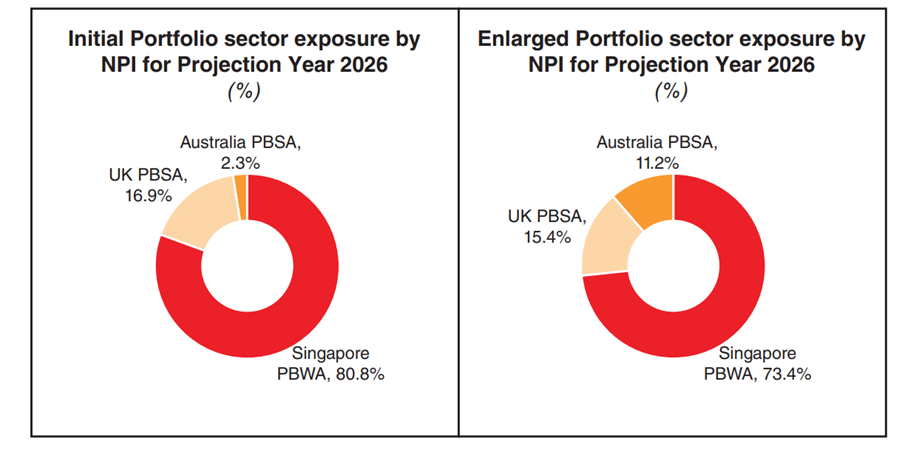

The breakdown of the initial and enlarged portfolio below.

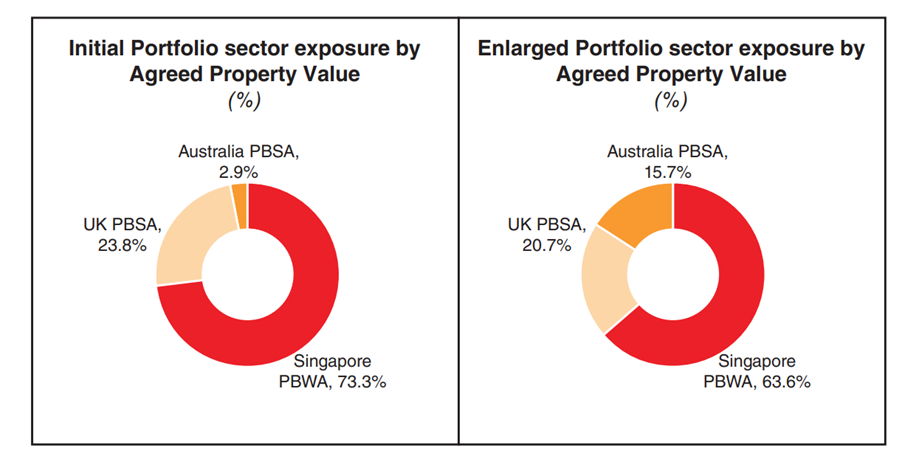

The bulk of the enlarged portfolio is Singapore workers accommodation (64%).

But frankly the student accommodation is not small as well, forming almost 36% of the enlarged REIT.

Centurion Accommodation REIT – How much duration left on the leases?

Now I know that Singapore REIT investors are obsessed over whether the properties are freehold or not.

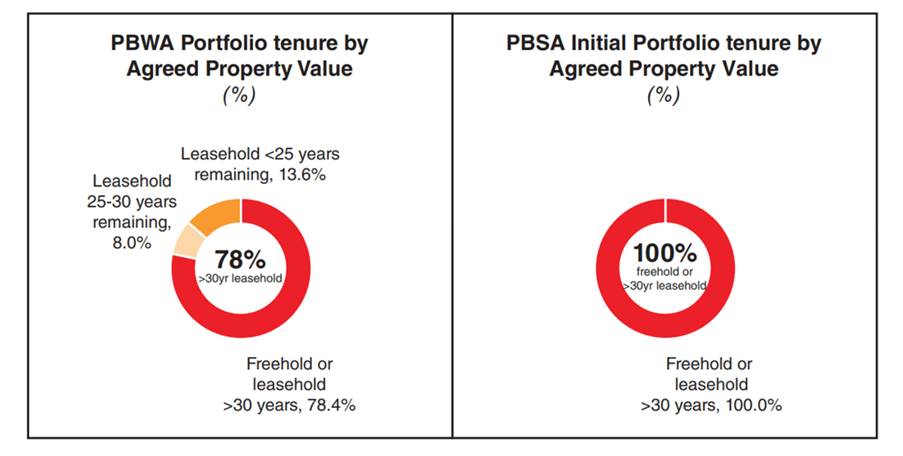

You can see the breakdown below.

The student accommodation in UK and Australia are pure freehold or >30 years left on the lease.

But the workers accommodation in Singapore, there is 21.6% of the REIT that has less than 30 years left on the lease.

To be fair this is not unusual since most of this would be government or JTC land, and you typically cannot get a long term lease extension for such use.

But it is a point to note in that this affects valuations and cash flows longer term.

What I like about Centurion Accommodation REIT

Let me cut to the chase.

What do I like about Centurion REIT?

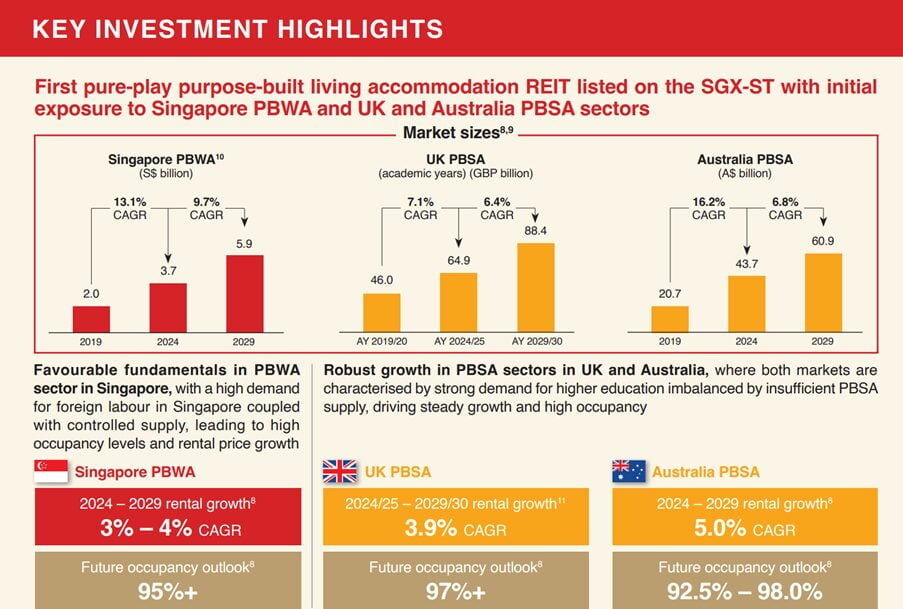

Demand supply imbalance of Singapore Workers Accommodation

The biggest one?

Is that for now at least, there is a demand supply imbalance for Singapore Workers Accommodation, which makes this a fairly unique (and dare I say, attractive) asset class.

The long and short of it.

Is that there’s a lot of demand for foreign workers in Singapore (for construction work etc).

And yet there’s not a lot of supply.

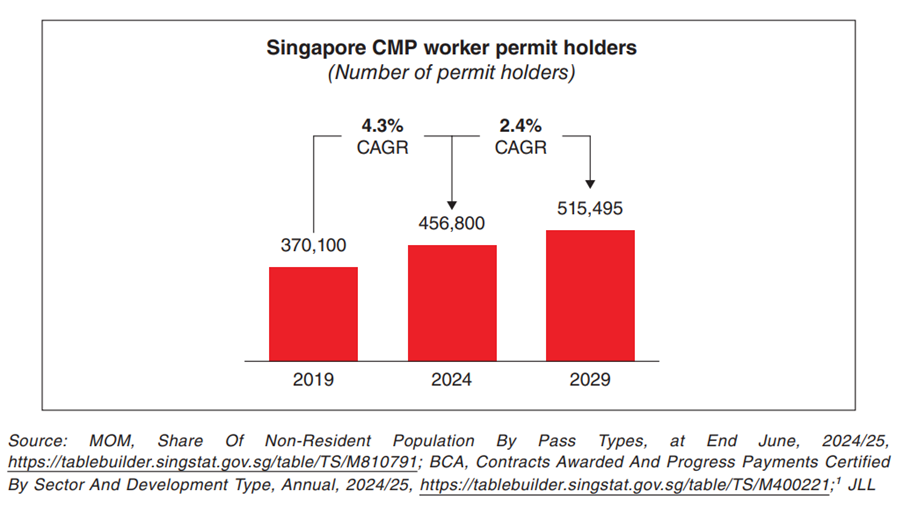

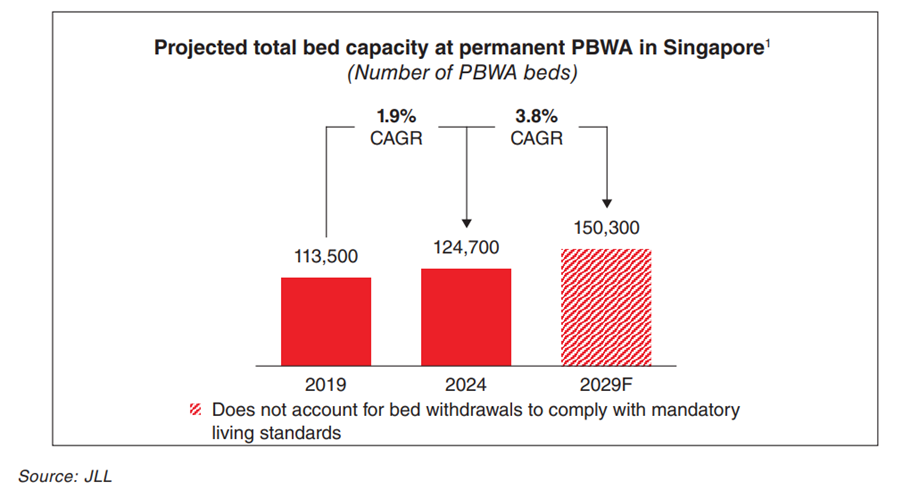

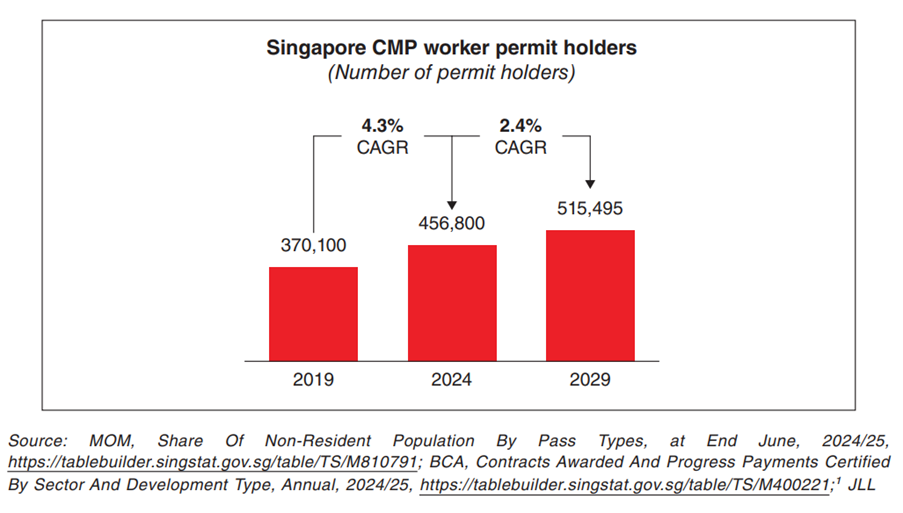

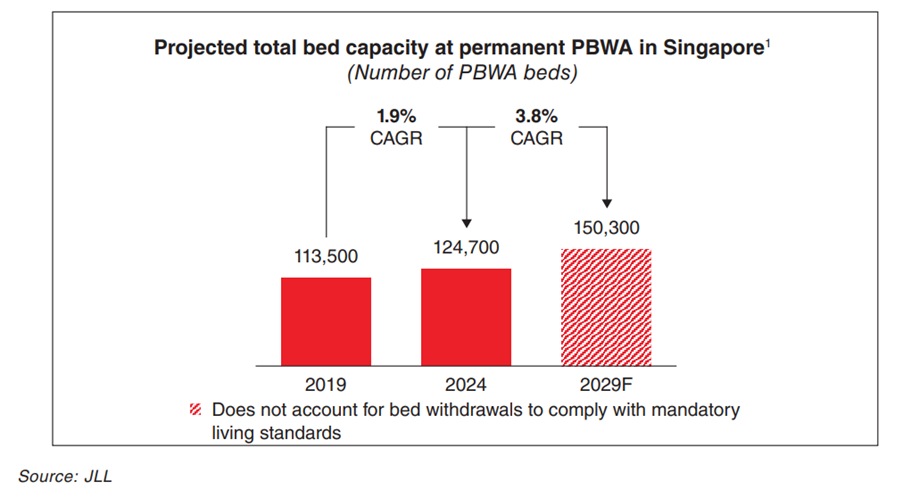

You can see how from 2019 to 2024, the number of work permit holders grew at a 4.3% Compounded Annual Growth Rate (CAGR), while the total bed capacity only grew at 1.9%.

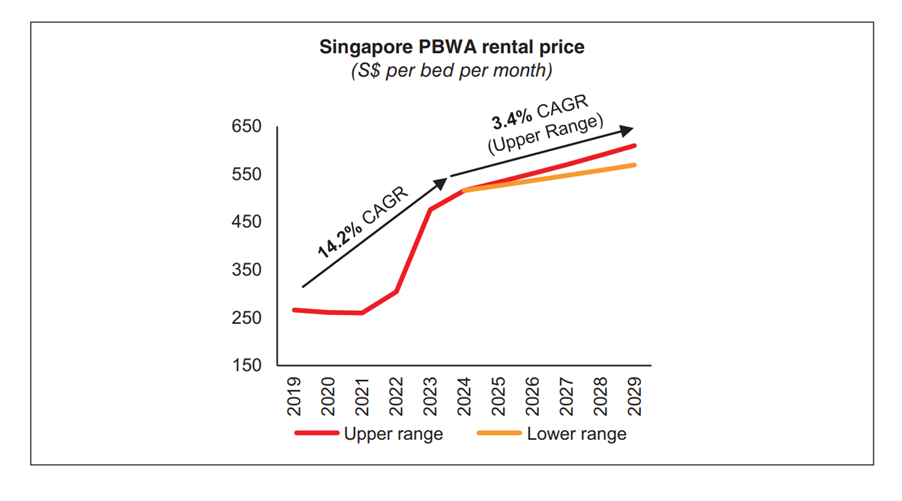

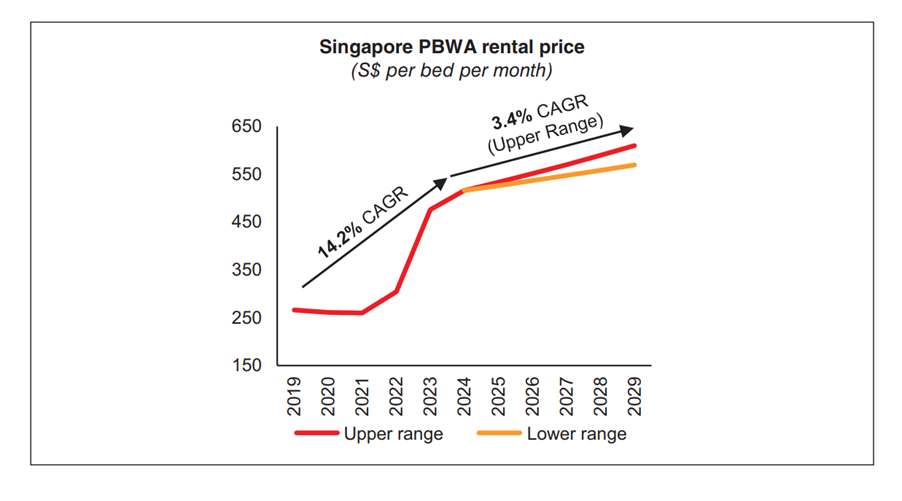

This has led to a massive 14.2% CAGR for the rental price over the same period, and you can see how the bulk of that move kicked in from 2022 – 2024 after the post-COVID demand explosion.

So Singapore workers accommodation did fantastically well in the 2022 – 2024 period, nobody is disputing that.

My Concern – what about the next 5 years?

My concern though, is what happens growing forward.

You can see how the forecasts used in the prospectus below project 2.4% CAGR for work permit holders up to 2029, and a 3.8% CAGR for bed capacity.

That means that the projected bed capacity growth will outpace the work permit holder growth – a stark difference from the situation we saw the past 5 years.

And if there’s one thing I’ve learned from my time being a real estate investor, its that boy you do not want to be holding real estate when supply growth is outpacing demand growth.

Of course there are a million caveats to this, and you may argue that the demand-supply is so imbalanced today that the higher supply going forward will not lead to a crash in prices, but only moderate the price increase.

Definitely possible, but you can also see how the forecasts themselves project a much lower 3.4% CAGR going forward even at the upper range (vs 14.2% the past 5 years).

Definitely something to keep an eye on.

8.11% dividend yield for Centurion Accommodation REIT in FY 2027?

I have mixed feelings about this one.

But I suppose it can go under the what I like bucket.

Projected dividend yield is 7.47% for FY2026, and 8.11% for FY2027.

I suppose this is “good” in that an 8.11% dividend yield in this market is comfortably above other REITs.

The “bad” I suppose, is that we don’t have any other worker & student accommodation REIT in the market to benchmark to today.

And my gut feel is that worker & student accommodation is nowhere as stable as office or retail assets, so you would definitely want to expect a yield premium.

Is the 8.11% dividend yield sufficient risk premium?

And how accurate is the 8.11% dividend yield, given the uncertainty over workers accommodation going forward?

No easy answer – which is why I have mixed feelings on this one.

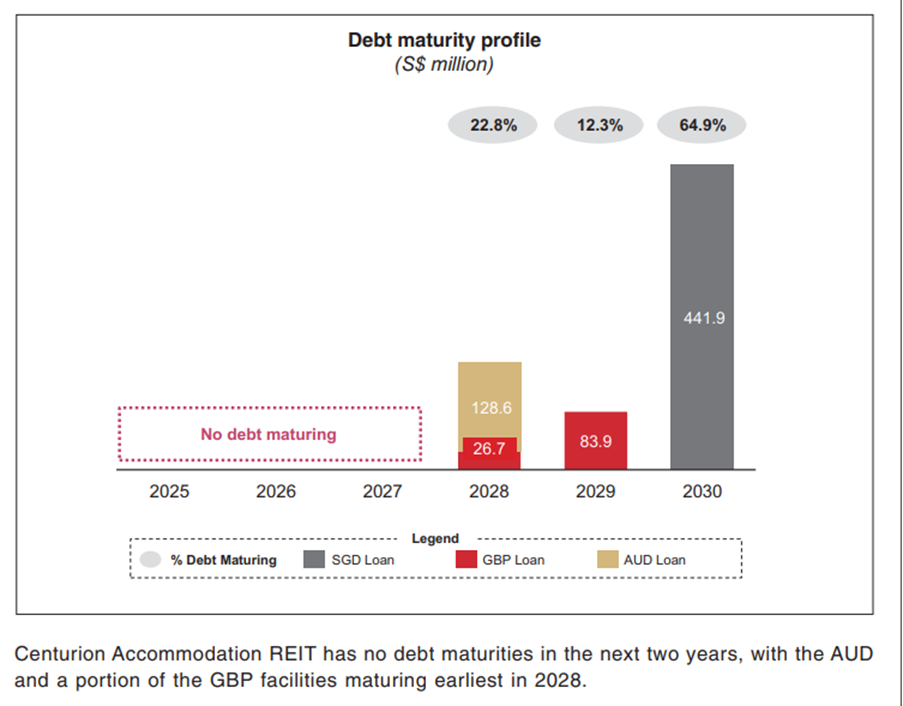

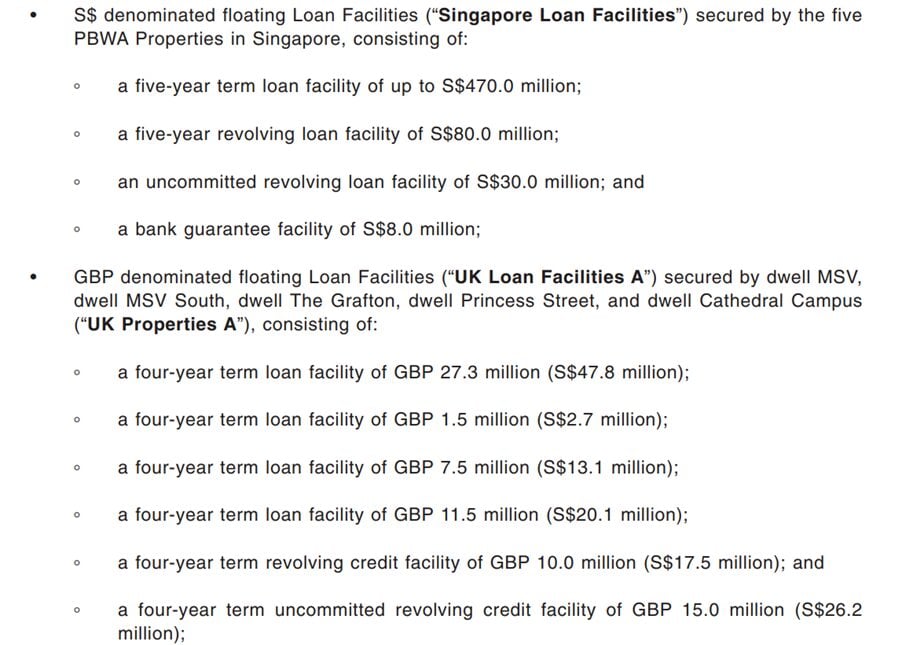

Prudent capital structure with ample debt headroom – leverage ratio of approximately 20.9% at IPO and approximately 31.0% post fully debt funded acquisition of Epiisod Macquarie Park

Gearing at IPO is a very low 20.9%, which is very good.

The purchase of the Australian Student Accommodation is purely funded by debt, which will bring gearing up to 31% post-acquisition.

31% is still on the low side, since most REITs run 35-40% gearing these days.

There’s also litereally no debt maturing up until 2028, which is good.

But… what if interest rates go up?

Based on what I could see, the bulk of the debt taken by Centurion REIT looks to be floating rate debt.

This is good when we are in a declining interest rate environment like we are today.

But note that things can easily change 12 – 24 months down the road, and that floating rate debt could be a problem if not managed well when rates go up.

What I am concerned about with Centurion REIT

Will the demand supply imbalance continue? Depends very much on government policy and factors beyond your control

I talked about my concerns on the outlook for the Singapore workers accommodation going forward, so I won’t belabour it.

Generally similar views for UK and Australia.

Yes there was a huge imbalance in supply demand, that was exacerbated post-COVID.

But now we are 4 – 5 years on from COVID.

Much of the supply imbalance has normalised.

And going forward, is there a risk of an oversupply situation?

Like I said, I’m not an expert on these sectors, but to me that’s the first concern that comes to mind.

Acquisition Strategy of Centurion Accommodation REIT going forward?

Per the prospectus:

Acquisition growth strategy – The Manager will seek to grow the DPU and/or NAV per Unit through effective asset management and also sourcing and acquiring quality income producing real estate assets which are used primarily for PBWA purposes, PBSA purposes or other accommodation purposes from both the Sponsor and third parties. The Manager will adopt a rigorous selection process focused on real estate qualities to ensure that investments can provide attractive, stable cash flows and yields which fit Centurion Accommodation REIT’s investment strategy to enhance future earnings, capital growth and returns to Unitholders. By managing the assets well, DPU and/or NAV growth can be achieved organically

After acquisition of the Australian Student Accommodation, gearing is 31% which actually gives Centurion REIT a lot of room for future growth.

This one is a big question mark for me.

How aggressive will Centurion REIT be on acquisitions, and how will they finance the acquisitions (debt or equity)?

We don’t have any track record from Centurion, so this is frankly a tough one to comment.

Centurion Corporation – Sponsor alignment of interests

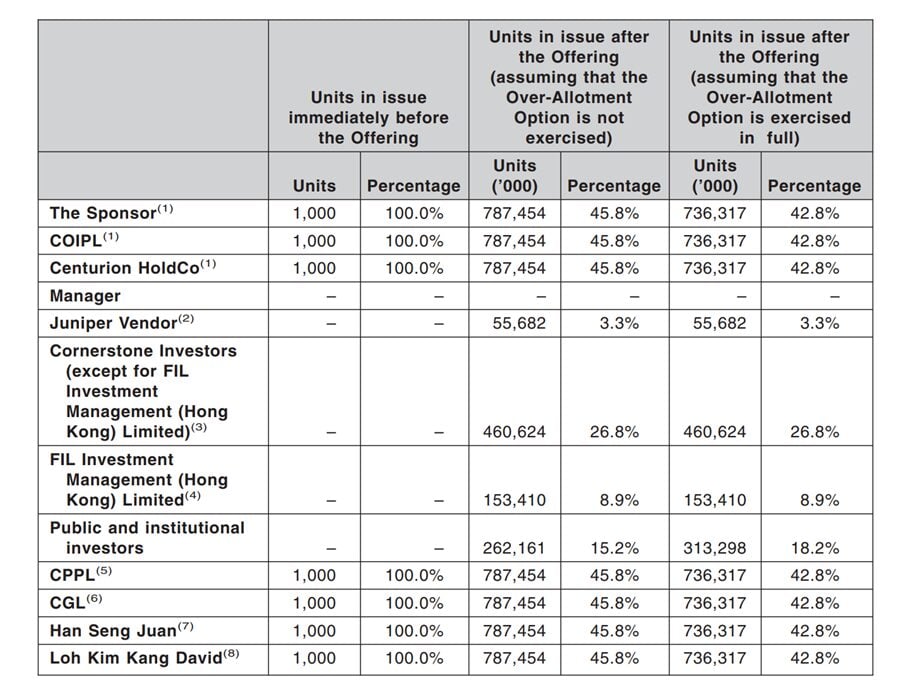

For what it’s worth – the Sponsor will hold more than 40% of the REIT post listing, so there is alignment of interests there.

That said, Centurion Corporation (the Sponsor) has done really well the past 2 years once news of this value unlock came into play.

Which also raises the question of who is the real winner here.

Centurion Corp, or Centurion REIT?

FX Risk for Centurion Accommodation REIT

Note also that as 26% of the REIT is Australia and UK assets, where is AUD and GBP FX exposure respectively.

Both currencies have been quite volatile against SGD, so another point to note.

Is there a need to subscribe for the IPO of Centurion Accommodation REIT? Or wait and see post-IPO performance?

Putting all of the above together, and I have mixed views on Centurion Accommodation REIT.

Yes I get that the bull case is that workers & student accommodation have structural tailwinds, and that this is a unique asset class which provides diversification.

I also get that if the projections hold up, a 8.11% dividend yield is pretty decent.

But at the same time, I also have some doubts over whether a 8.11% dividend yield is a sufficient yield spread given the nature of assets I would be buying into.

And as shared, I also don’t know how the workers & student accommodation market will play out over the next 5 years.

At the right price I could be convinced to take a position, but frankly I just don’t know if this is the right price.

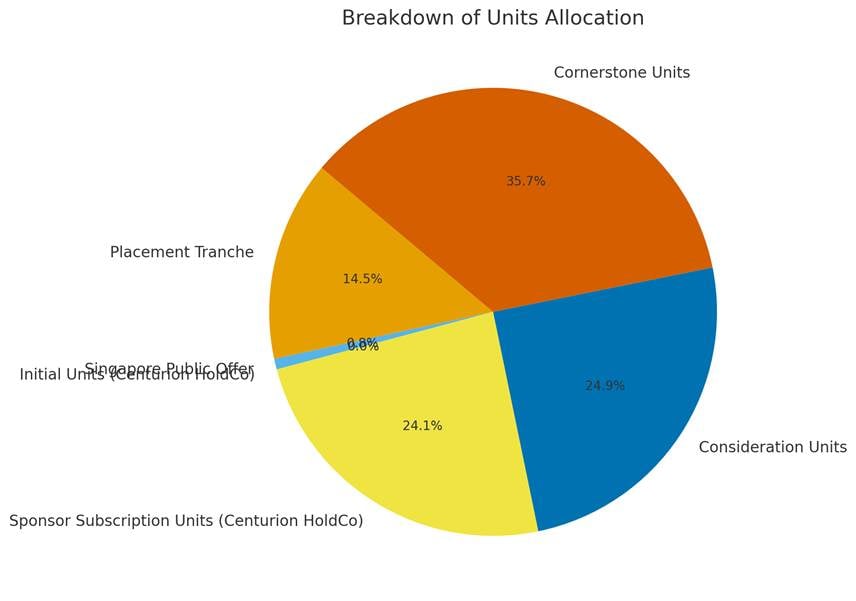

Public offer tranche is miniscule for Centurion Accommodation REIT IPO

Throw in the fact that the public offer tranche is miniscule – 13,200,000 Units to the public in Singapore.

At $0.88 per unit, that’s only $11.6 million worth of units up for grabs.

Visualised below, that’s a tiny 0.77% of the total offer size.

Which means that even if I apply for the IPO, I’m unlikely to get a meaningful allocation.

Even less incentive to subscribe.

| Category | Units | % of Total |

| Placement Tranche | 248,960,900.00 | 14.48 |

| Singapore Public Offer | 13,200,000.00 | 0.77 |

| Initial Units (Centurion HoldCo) | 1,000.00 | 0.00 |

| Sponsor Subscription Units (Centurion HoldCo) | 414,372,100.00 | 24.10 |

| Consideration Units | 428,763,000.00 | 24.94 |

| Cornerstone Units | 614,034,000.00 | 35.71 |

Centurion Accommodation REIT IPO Review – Will I buy this 8.1% dividend yielding worker and student accommodation REIT?

Given all of the above, I’m probably going to give the IPO a miss.

What I really want to do is to watch the post-IPO share price performance.

If we get a huge dip, maybe that could tempt me to pick up a position.

If price stays steady, I probably want to watch the track record of the REIT for a bit before I commit capital (if at all).

Love to hear what you think though – will you be “pressing button” for Centurion Accommodation REIT IPO?

This is an FH Premium article written on 19 Sep 2025 and will not be updated going forward. My latest personal portfolio, stock watch, and macro views are shared on FH Premium.

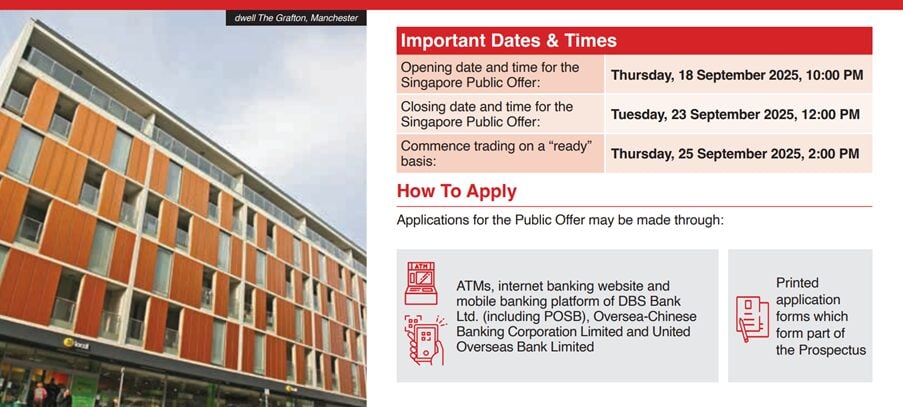

How to subscribe for the IPO of Centurion REIT?

If you are keen to subscribe.

The IPO is already open as of 10pm on Thursday 18 Sep.

And it will close at 12pm on Tuesday 23 Sep.

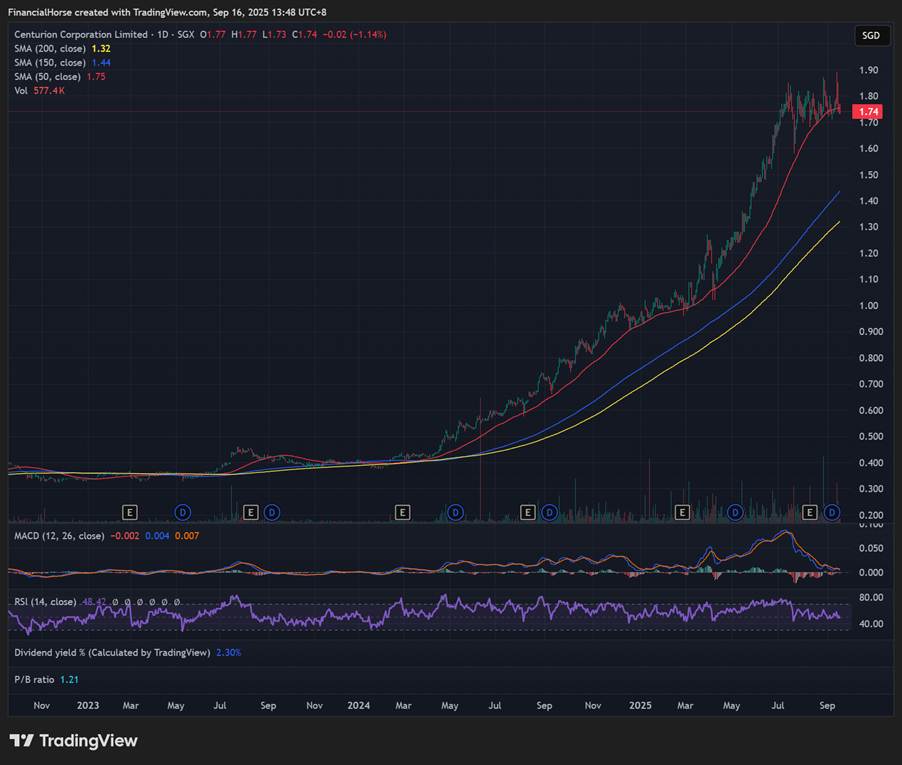

Would it better off buying the parent stock, centurion instead?

They had a huge rally from the lows though. Question is how much further upside is in play at this price.

Thanks for this write up and your views.

I think your assessment of the demand and supply of PBWAs may be too conservative for two reasons:

(a) You are projecting that work permit holders will grow at a slower pace of 2.4% through to 2029. This is at odds with the acceleration in construction demand in the same period. You can already see this in the government increasing the maximum age of workers and expanding the range of countries they come from earlier this year.

(b) The growing 3.8% PBWA supply does not, as you note, account for bed withdrawal. It also does not account for the non-PBWA supply that is coming off the market.

The charts/projections I used are from the IPO prospectus. I didn’t have any specific view on whether they are aggressive/conservative as I dont know enough about this space to make an accurate assessment.

thanks for info.

I suppose, at approximately $1000/lot, it’s worth buying and keeping long term? Buy-and-forget kind of investment.

It turns out the market did find this REIT to be undervalued – hence the huge post IPO jump in share price. Let’s see if this holds, and let’s the the first couple of financial results. Would be interested to see how this one plays out.