A bond ladder staggers maturities so you always have money arriving when you need it.

CPF maps neatly onto this concept if you assign roles to each bucket.

For example.

Cash, MMFs and 6-month T-Bills cover the next 3–12 months.

Singapore Savings Bonds (SSBs) and rolling T-Bills span 1–5 years.

CPF—especially SA today and RA later—becomes your 5-to-20-year “long rung” with government backing and a floor on interest rates (to prevent cases where rates go back to zero).

MediSave sits alongside as your healthcare endowment, often with attractive implicit returns, and should be filled methodically to cap (BHS) before you chase yield elsewhere.

I’ve been getting some questions on this concept of how does CPF fit into your portfolio as a “Bond Ladder”, so I wanted to spend some time to explore the thought process.

Think of it as liability-matching.

Price in your next 12 months of spending, upcoming 1–5 year “lumps” (tuition, car, reno), and only then commit long-term capital to SA/RA where compounding can work uninterrupted for decades.

Basics Principles for CPF (to frame the discussion)

Let’s start with the basic principles for CPF.

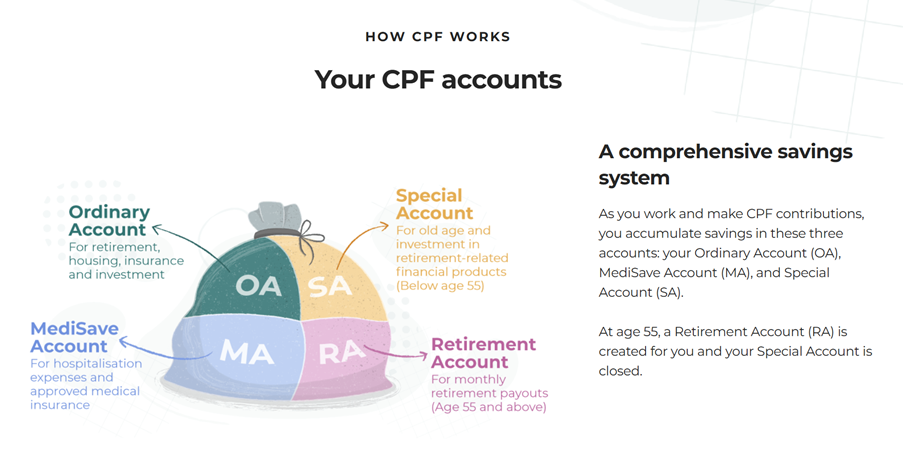

CPF Account Structure

- Ordinary Account (OA): Flexible use (housing, education, investments).

- Special Account (SA): Higher interest, meant for retirement.

- Medisave Account (MA): Strictly for healthcare expenses/insurance premiums.

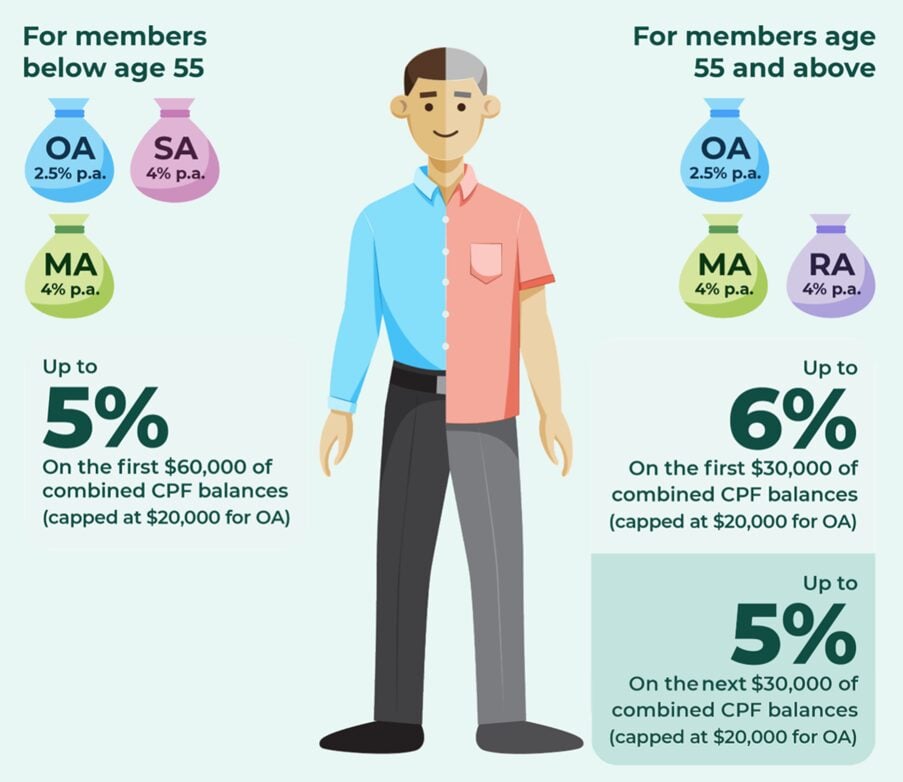

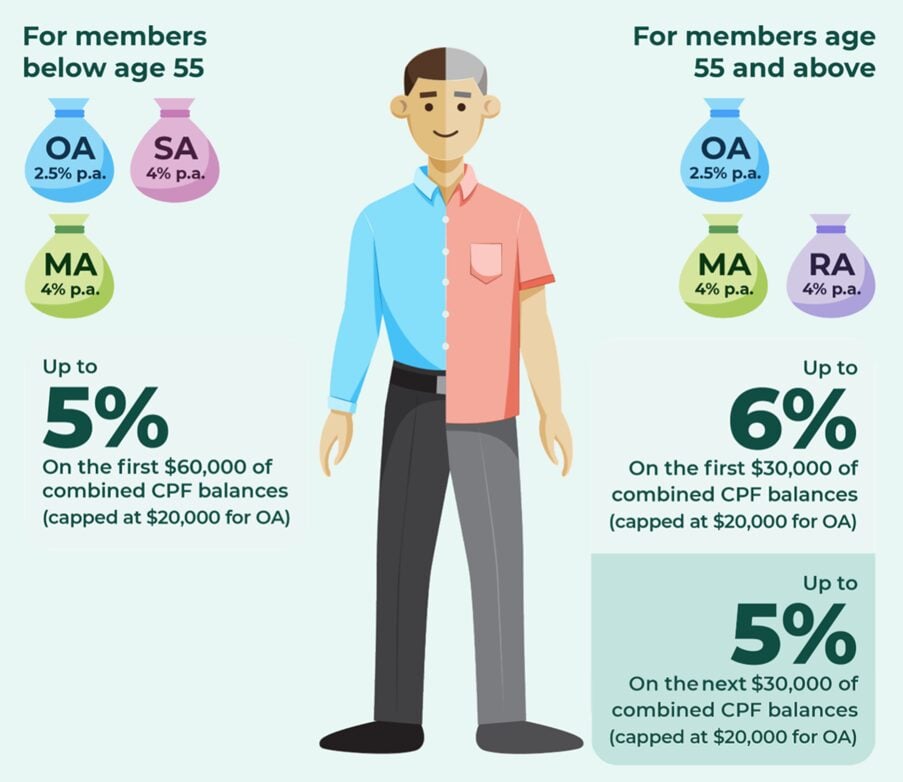

CPF Interest Rates

OA earns 2.5% p.a., SA/MA 4% p.a. (plus extra 1%–2% for first S$60k combined balances).

CPF Withdrawal Rules

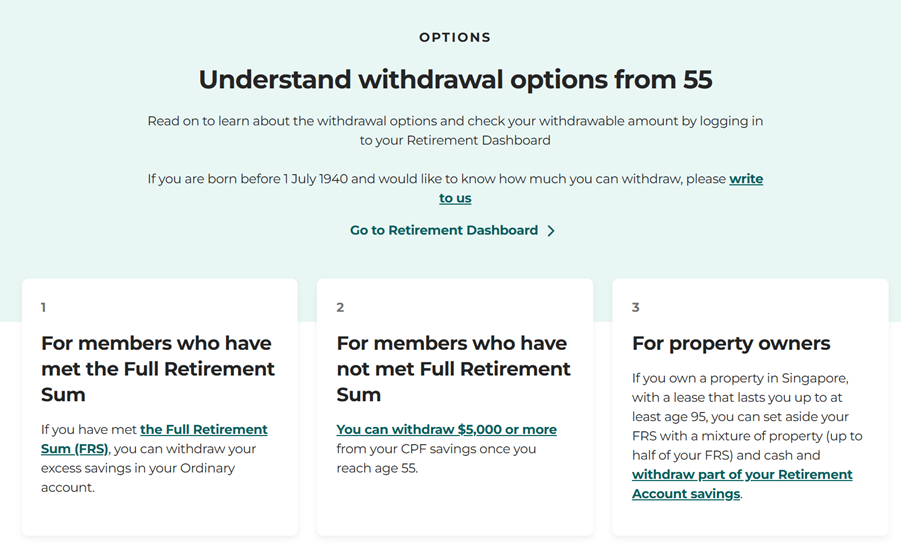

- Cannot freely withdraw until statutory retirement age.

- Minimum Sum / Retirement Account (RA) is created at age 55, pooling SA + OA (subject to Basic/Full/Enhanced Retirement Sum).

- Excess above this can be withdrawn.

CPF Usage

- Housing: OA can fund HDB/loan repayments.

- Education: OA for approved tertiary courses.

- Healthcare: MA for MediShield Life, Integrated Shield premiums, hospitalization.

CPF Top-ups & Tax Reliefs

Voluntary top-ups to SA/RA/MA are tax-deductible (subject to annual limits below).

Cash top-ups to CPF now give up to S$16,000 tax relief per YA: S$8,000 (self) + S$8,000 (family), and this single cap combines RSTU (SA/RA) and MediSave top-ups.

Relief is still subject to the overall S$80k personal relief cap, BHS/FRS limits, and the CPF Annual Limit (S$37,740) for voluntary contributions.

Key 2025 numbers: BHS S$75,500, OW ceiling S$7,400/mth, annual salary ceiling S$102k; spouse/sibling income threshold for family-top-up relief is S$8k (YA2025+)

Core principles for CPF as a Bond Ladder (in plain English)

I’ve split into 3 buckets:

- <12 months

- 1 – 5 years

- >5 years

<12 months

Start with liquidity: ringfence 12 months of essential spending outside CPF.

If your household spends S$8k a month, your bare-minimum cash runway is S$96k.

Keep 3–6 months instantly accessible in cash/high-yield accounts or MMFs, and push the rest into a simple 6-month T-Bill ladder so one tranche matures every auction cycle (although use some discretion here – if your high yield account yields more than T-Bills and you have excess room, just leave it there).

This is money you can tap without touching CPF, and should be the baseline before you move to other levels.

1 – 5 years

Once this is out of the way, then you can move to the 1–5 year layer.

What would make sense here is Singapore Savings Bonds: capital is redeemable (with modest friction) and coupons step over time.

If you are comfortable with some risk, you can consider investment grade bonds like the Astrea series, or a bond fund.

Some investors keep unused OA as a mid-duration buffer; that’s fine if you value the optionality for property prepayment or a future purchase, but recognise OA’s yield is typically lower than SA.

>5 years

Only when the 0–5 year runway is fully funded should you lean into SA top-ups and MediSave to BHS.

This sequencing matters.

SA and RA are superb long rungs precisely because they’re hard to raid in a moment of panic.

That “illiquidity” is a feature—once you’ve protected near-term cash needs.

How to actually build the CPF bond ladder —narrative walkthrough

Bond Ladder =/= stock or growth portfolio

Just to be absolutely clear, this bond ladder concept is meant as a way for cash management.

It is not a replacement for a stock or growth portfolio.

So the way it usually works in practice is that you use this bond ladder concept to manage your cash and liquid funds.

And on top of that you run a stock / equity portfolio to take higher risk for higher potential returns, with the understanding that market volatility would mean those funds are more volatile.

So this bond ladder is a complement to a stock portfolio, and not a replacement.

Practical examples for how the CPF bond ladder would work in practice (30s, 40s, 50s)

Example A — 34, first home in 2–3 years

Lynn earns S$9k monthly; net household spend is S$5.5k.

She wants optionality to buy a S$800k apartment in 24–36 months, and is tempted by SA top-ups.

The safe move is to protect optionality first.

Lynn builds a S$66k 12-month runway:

- S$20k in cash/MMF for emergency access

- S$46k in a 6-month T-Bill ladder

She then accumulates S$120k in SSBs over the next 18 months for the downpayment buffer—redeemable if she buys, recyclable if she doesn’t.

Only after this does she start small, regular SA top-ups (say S$500/month) to keep compounding without jeopardising the purchase.

If plans change and she decides to rent longer, she can scale SA top-ups to S$1.5–2k/month. OA remains largely untouched so she can service the eventual mortgage at lower effective cost.

Example B — 41, kids’ education in 3–5 years

Amar and Priya spend S$8k/month and expect S$120k of education costs starting in three years.

They already own their home and are not moving.

They keep a S$96k 12-month runway:

- S$32k cash/MMF

- S$64k in a four-tranche T-Bill ladder

For the 1–5 year sleeve, they build an SSB core to S$150k over 24 months.

Each SSB application is planned so a chunk crosses the 3-year mark before redemption, giving them the option to avoid early tenure exits.

With the mid-term funded, they max MediSave to BHS annually, then run steady SA top-ups for compounding and potential tax relief. If markets wobble in year 3 and they need the first S$40k for tuition, they redeem that month’s SSBs and roll maturing T-Bills into cash instead of reinvesting.

Their SA remains intact and growing; equities don’t need to be sold at bad prices.

Example C — 53, approaching 55 and payout planning

Jia Min is 53, kids are independent, mortgage is small.

She has 18 months to plan for RA creation.

Step one is to determine her target payout at 65 and whether she’s aiming for BRS, FRS or ERS.

Step two is ensuring she has 2–3 years of cash needs outside CPF before starting CPF LIFE payouts (sequence-of-returns insurance). She lifts her liquid runway to 24 months by expanding T-Bills and SSBs.

Step three is sequencing contributions: she fills MediSave to BHS each year; any overflow routes per prevailing rules; she makes final SA top-ups inside the relevant caps.

If considering shielding, she rehearses the exact dates and amounts on a one-page checklist and keeps a plain-vanilla fallback: if any step can’t be executed, proceed without shielding.

At 55, she forms RA per plan and keeps the external 24-month buffer until payouts start.

CPF mechanics you must understand (without the jargon)

Extra interest rules mean the first slices of your CPF often earn more—where that extra interest is credited matters.

BHS (for MediSave) as well as FRS/ERS (for retirement) tend to rise over time; starting early avoids year-end scrambles.

Employer contributions count toward annual limits, so synchronise your own top-ups to avoid disappointment on tax relief.

If you’ve used OA for property, remember accrued interest mechanics: when you sell, money flows back into OA before excess cash reaches you—model that before committing to renovations or an investment property.

Finally, RA timing is an execution process with windows and formality; treat it as a project with dates, amounts, and back-up plans rather than a last-minute decision.

Common mistakes—and simple fixes

The classic error is over-locking into SA in your early 30s and then needing funds for a home, forcing awkward workarounds. Solve it by filling the 0–5 year rungs first, then scaling SA top-ups.

Another frequent issue is ignoring caps and assuming tax relief that doesn’t arrive; the fix is a December reconciliation of employer contributions versus your own. Running an all-cash emergency fund is a slow leak; keep a working float and push the rest into a rolling 6-month T-Bill ladder.

Near 55, mis-timed RA actions can cost you optionality; put a calendar reminder at 53 to begin planning.

And above all, don’t design a plan that only works if rules never change. Build slack: a larger SSB sleeve than you think you need, and never rely on a single tactic like shielding to “make the numbers work.”

Stress-testing your bond ladder

Pretend you just lost your job.

With your current setup, can you cover 12 months without touching CPF?

If equities fall 25% next quarter, can you still fund the child’s year-3 tuition from SSB/T-Bills alone?

If you had a health event tomorrow, would MediSave and insurance cover deductibles, or would you be forced to redeem investments at poor prices?

Walk through these scenarios once a year.

A good ladder is boring in good times and decisive in bad times because the steps are pre-written.

Why this approach works (reasoning)

Matching assets to liabilities reverses the usual “rate-chasing” mistake.

You’re not asking, “What yields the most this month?”

You’re asking, “What pays the next bill, and what can be locked for 20 years without regret?”

CPF’s structure—sovereign backing, policy floors, extra-interest tiers, and annuitisation at RA—makes it an ideal long rung.

SSBs and T-Bills provide the release valve in the middle.

When you respect that order—0–12 months, then 1–5 years, then 5–20 years—you cut the probability of forced selling, tax surprises, and behavioural errors.

Add annual automation and a calendar review, and you replace ad-hoc tinkering with a system that compounds quietly in the background.

Alternatives worth considering

If you expect to emigrate or need maximal flexibility, keep CPF top-ups modest and run a non-CPF ladder instead (SSBs, T-Bills, investment-grade bond funds, short-duration ETFs).

If your mortgage rate is structurally above your assumed SA/RA return, prepayment can act as your “bond”: compare apples-to-apples after tax and liquidity needs.

If you already have a robust CPF long rung and want income growth, overlay a diversified equity-income sleeve (banks/REITs/global dividend ETFs)—but only after the 0–5 year ladder is watertight.

Closing thoughts: Action plan to consider for a CPF bond ladder

- Size your 12-month runway and fill it: cash/MMF for 3–6 months, the rest in a 6-month T-Bill ladder.

- Build a 1–5 year sleeve with an SSB core sized to specific goals; top up with rolling T-Bills. You can consider investment grade bonds, but only if you are comfortable with risk.

- Each year: fill MediSave to BHS first, then make SA top-ups within caps, coordinated with employer contributions.

- From age 53: decide BRS/FRS/ERS, map RA creation steps, and keep 24 months of cash needs outside CPF until payouts begin.

- Calendar a 60-minute annual review to refresh numbers, maturities, and rules; automate everything else.

Bottom line: Treat CPF as your 20-year bond rung—powerful, steady, and deliberately hard to touch—only after you’ve secured 0–5 years of liquidity outside it. Do that, and “4%+ for 20 years” becomes a plan you can actually live with, not just a number on a spreadsheet.

Love to hear what you think!

This article is written on 19 Sep 2025 and will not be updated going forward. My latest personal portfolio, stock watch, and macro views are shared on FH Premium.

Hi

Don’t really understand the part about RA and shielding. And your comments that “near 55, mis-timed RA actions can cost you optionality”. Can explain abit more?

Similar question as Yvonne. Any diff between transferring monthly CPF from OA to SA instead of MA? No loan and near 55 but SA yet to reach FRS.

It’s the same 4% yield + tax relief. But benefit is that with MA you can use it for medical expenses (SA much harder to use). And once you hit BHS, all future contributions autoflow into SA anyway. So main benefit to topping up MA to BHS first is optionality.