It’s been quite a while since I wrote on everyone’s favourite bank stock – DBS Bank.

DBS bank today trades close to all time highs at S$50.8.

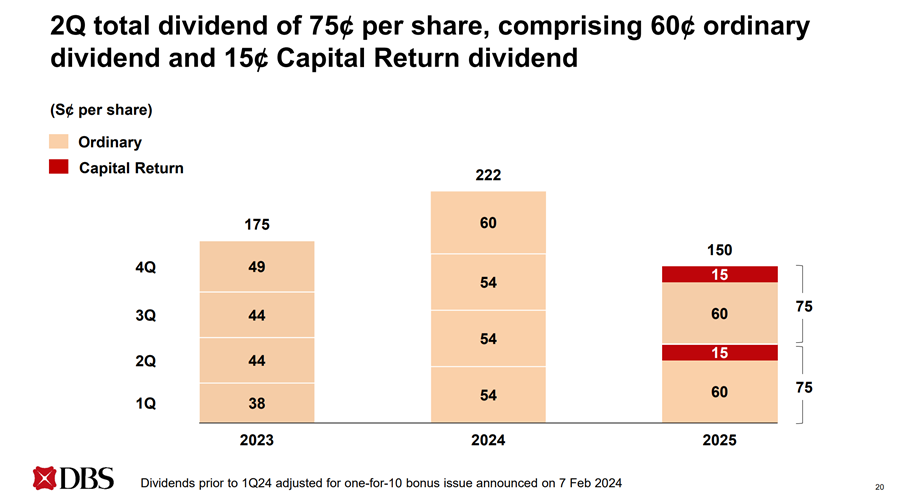

And yet if you count the 60 cents ordinary dividend together with the 15 cents capital return dividend, DBS Bank actually still pays a 5.9% dividend yield.

That being said – you’ve probably seen sweeping interest rate cuts by Singapore banks by now.

Is DBS Bank still a good buy at all time highs?

Dividend Yield of DBS Bank – 5.9% dividend yield, even at all time highs

DBS pays a:

- 60 cents ordinary dividend

- 15 cents capital return dividend

If you assume the capital return dividend will be retained going forward.

That’s a 75 cents quarterly dividend.

Which works out to a 5.9% dividend yield at latest price.

Dividend Payout Ratio of DBS Bank?

Which of course begs the question.

How sustainable is this dividend yield?

Crunching some numbers on the dividend payout ratio:

| Basis | EPS used | Payout ratio = $3.00 ÷ EPS |

| Forward (consensus-implied) | $3.90 (from price $50.54 ÷ forward P/E 12.97) | ≈ 77% |

| Trailing (FY2024 actual) | $3.98 (S$11,289m net profit / 2,838m shares) | ≈ 75% |

Ex-capital-return (ie, $0.60 × 4 = $2.40): payout would be ~62% forward / 60% trailing.

In plain English.

If you count the capital return dividend – DBS pays out about 77% of its profits.

If you exclude the capital return dividend – DBS pays out about 62% of its profits.

How sustainable is DBS Bank’s dividend yield?

A ~77% total payout is definitely on the high side, which suggests that DBS has already squeezed a lot of juice out of this.

It’s definitely sustainable if the earnings hold up.

And if earnings continue to grow, there could be room for further increases.

But if earnings start to dip, then at 77% payout ratio looks awfully high and at risk of a dividend cut.

Breaking down the financials of DBS Bank – Interest income flat, non-interest income strong

Per DBS Bank’s latest financial results:

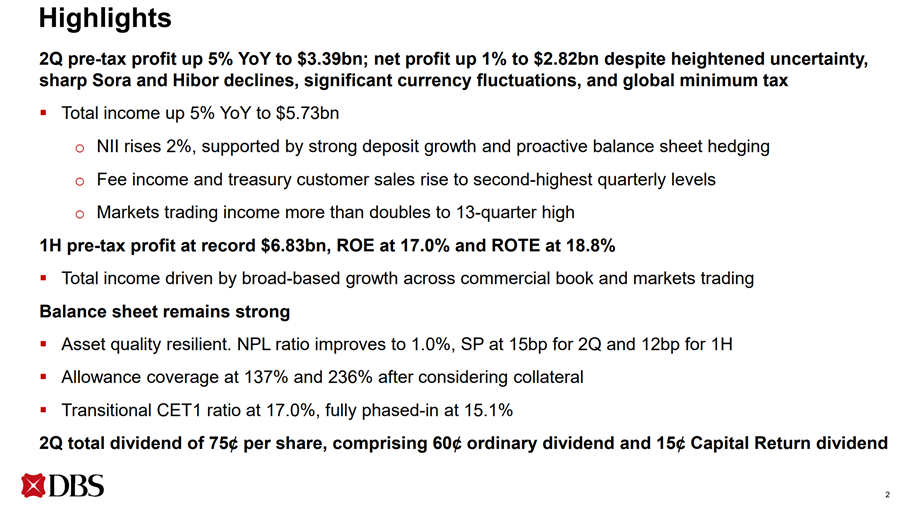

“2Q pre-tax profit up 5% YoY to $3.39bn; net profit up 1% to $2.82bn despite heightened uncertainty, sharp Sora and Hibor declines, significant currency fluctuations, and global minimum tax

Total income up 5% YoY to $5.73bn

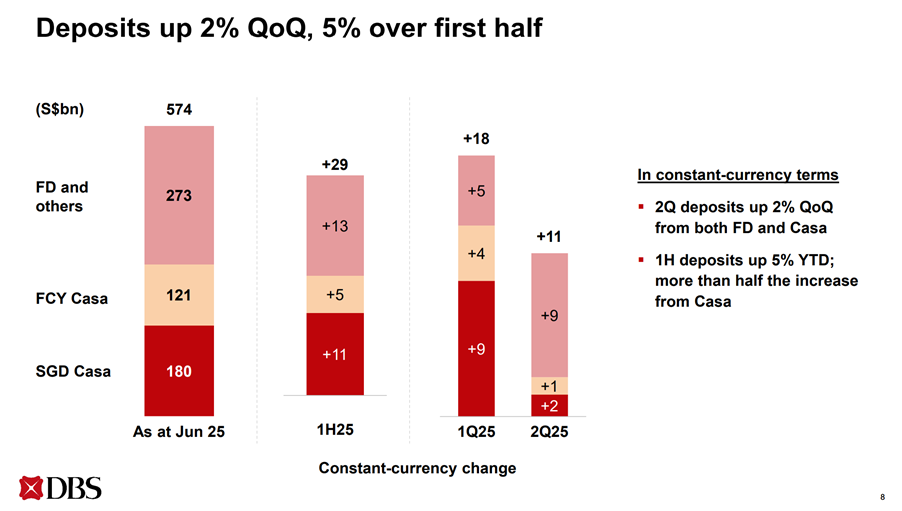

- NII rises 2%, supported by strong deposit growth and proactive balance sheet hedging

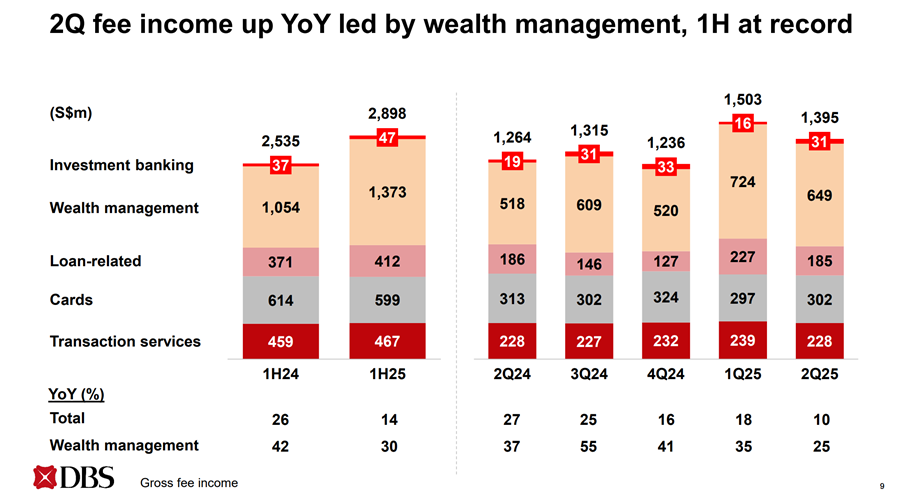

- Fee income and treasury customer sales rise to second-highest quarterly levels

- Markets trading income more than doubles to 13-quarter high

1H pre-tax profit at record $6.83bn, ROE at 17.0% and ROTE at 18.8%

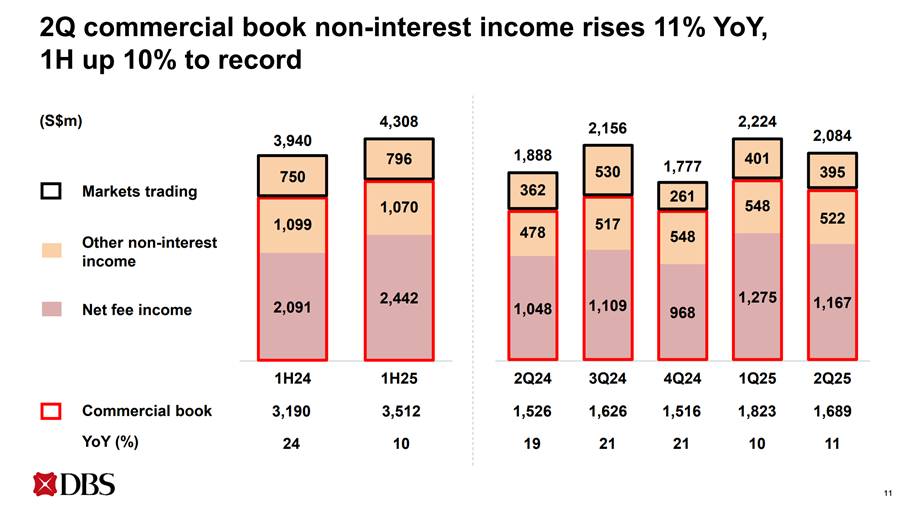

- Total income driven by broad-based growth across commercial book and markets trading

Balance sheet remains strong

- Asset quality resilient. NPL ratio improves to 1.0%, SP at 15bp for 2Q and 12bp for 1H

- Allowance coverage at 137% and 236% after considering collateral

- Transitional CET1 ratio at 17.0%, fully phased-in at 15.1%”

In plain English.

There’s a reason why DBS Bank share price is at all time highs, while UOB and OCBC bank are not.

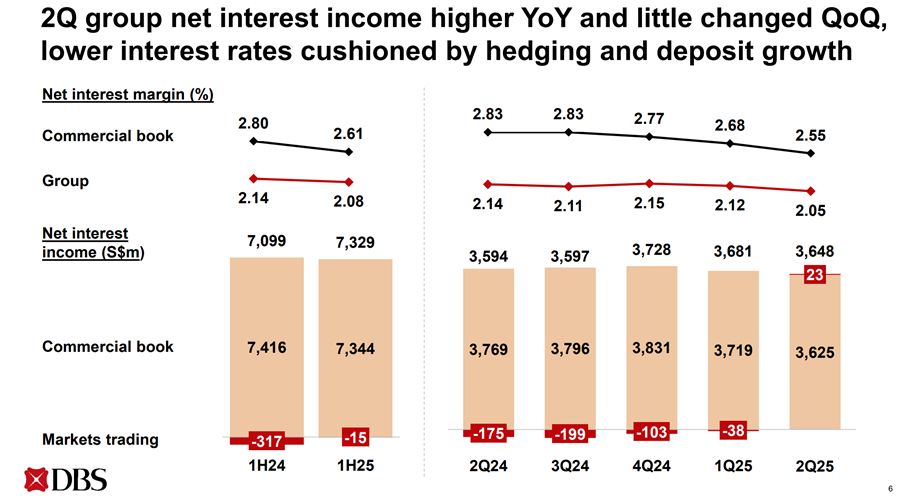

Because while UOB and OCBC bank are showing weakness in their core lending business, DBS Bank actually manages to keep net interest income steady.

And on top of that, DBS Bank is showing very strong fee income growth, which offsets the slower growth from the core lending business.

Core lending business of DBS Bank – Net Interest Income is flat

Doing a deeper dive into each segment.

Net interest income is up year on year, but flattish quarter on quarter.

Compared to OCBC and UOB bank though, this is still pretty impressive.

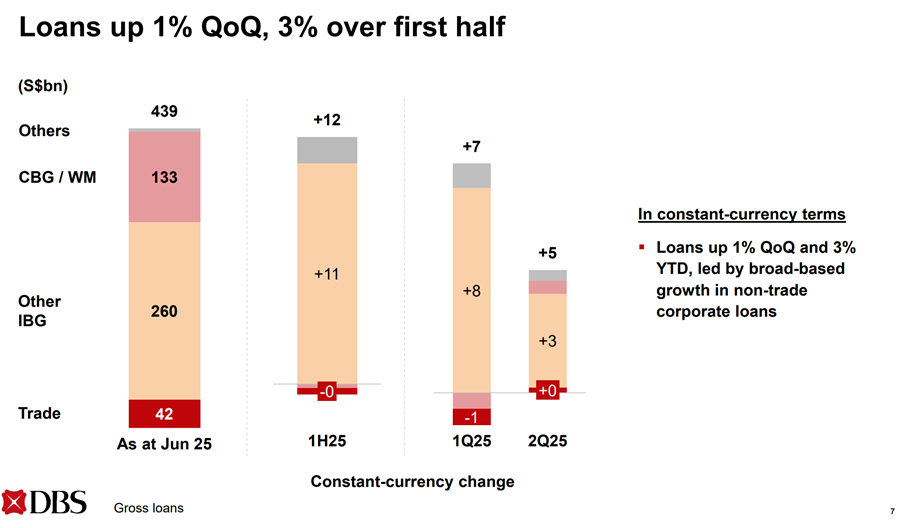

Under the hood, we see 1% quarter on quarter loan growth.

While customer deposits remain stable despite the sharp drop in interest rates (that they pay).

Fee Income performing well

While the core lending business remains resilient.

I suppose the star of the show is the fee income business – up 10% on a year-on-year basis.

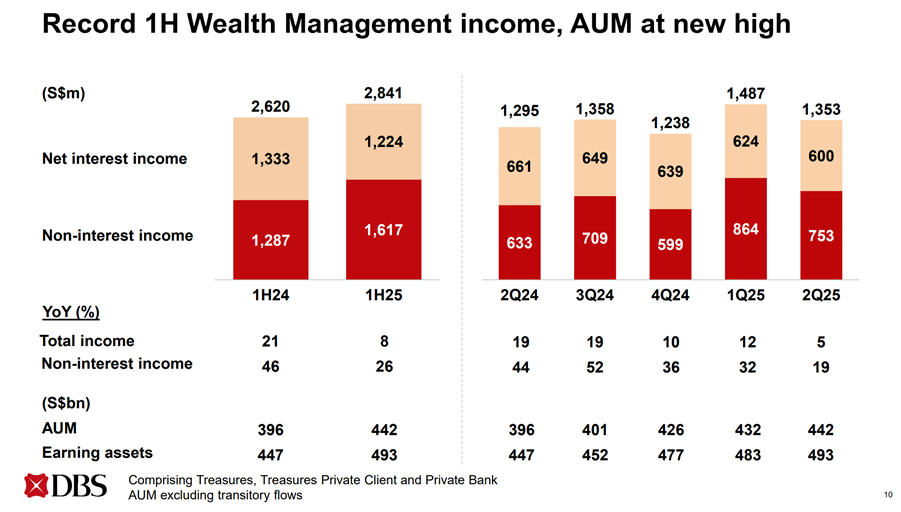

But under the surface, the outperformer is wealth management, up 25% year on year.

And now forming 46.5% of the fee income business.

Wealth management is starting to look like a meaningful contributor to the bottom line here.

Question of course, is whether DBS bank can keep this up going forward.

What happens next for DBS Bank?

As the quote by Stanley Druckenmiller goes:

“You don’t buy a stock for what it is today, but where it will be in 18 months”.

I get that DBS bank is firing in all cylinders here, with a resilient core lending business, and a very strong performing wealth management business.

But what do things look like 18 months from today?

What is likely to play out in reality, vs what is already priced into the stock?

My gut feel is that a lot of optimism has already been priced into the stock today.

It’s not to say that the stock cannot go higher.

It’s that for it to go higher, the stock needs to beat already pretty lofty expectations priced in.

And at a 77% dividend payout ratio, it just takes a small wobble in earnings and there could be a fair bit of downside on the table.

So I bounced some ideas off AI and this was the response I got:

Executive take: At S$50.54 (Sep 4), DBS is top-tier but priced close to fair value. Ordinary forward yield ≈4.8% (≈5.9% incl. 2025 capital-return dividends); P/B ≈2.12× vs NBV S$23.82. Base-case risk-reward is mediocre; better entry <S$48.

Verdict: HOLD / buy on dips. Upside exists if ROE holds ~17% and capital returns persist; downside if NIM compresses faster or credit costs normalise from ultra-low levels.

Bottom line: Exceptional franchise, bulletproof capital, reliable dividends—but at ~2.1× P/B the market already prices that. Hold / buy on dips to skew risk-reward in your favour.

Reasoning (step-by-step)

- Where we are now. Price S$50.54; 1H25 ROE ~17%, group NIM 2.08% (2Q25: 2.05%), NPL 1.0%, CET1 17.0%. NBV/share S$23.82 ⇒ P/B ≈2.12×. Ordinary DPS is S$0.60/qtr; DBS is also paying capital-return S$0.15/qtr in 2025. Ordinary yield ≈4.75%; incl. 2025 capital-return ≈5.94%. 1H payout ≈60% on ordinary (≈75% incl. capital-return).

- Quality is high. Fee franchises and deposit growth cushioned lower rates; asset quality resilient; allowance coverage 137% (236% on unsecured). Balance sheet strength limits tail risk.

- But profitability is easing. ROE/NIM are drifting lower YoY; management guides 2025 NII slightly above 2024, but net profit slightly below—consistent with lower margins and higher taxes/credits.

- Valuation framework. For banks, P/B anchored by sustainable ROE vs COE. Using ROE 15-17%, COE ~10-11%, growth 3-4%, fair P/B bands cluster around ~1.7×–2.1×—i.e., today’s ~2.1× already discounts premium returns. (My inference based on Gordon-type logic using reported ROE/NBV.)

- Key risks. Faster-than-guided NIM compression; cyclical uptick in credit costs from very low 12–15 bp; and any tech/disruption relapse (MAS sanctions lifted in Apr-2024, but a fresh outage occurred Mar-2025).

- Key supports. Dividend/capital-return cadence (S$0.60+0.15/qtr YTD), strong CET1, and fee growth (WM/treasury) provide floor.

DBS Bank pays a 5.9% dividend yield – Will I buy Singapore’s biggest bank in 2025? (at all time highs)

And you know what?

I think that’s just pretty spot on as a summary of my views.

I genuinely think DBS bank that DBS is a best in class stock, firing on all cylinders.

My only concern is that a lot of that has already been priced in today.

And all you need is a small wobble in the global macro climate, or the earnings picture, and you could see quite material downside.

So yes I know that some of you will say that this is about buying a great company at a fair price, and holding long term.

And you get a 5.9% dividend yield on top of that while you wait.

I don’t disagree with that.

But the way I see it.

The way the macro is set up – interest rate risk points to the downside here.

And with a 77% dividend payout ratio, it wouldn’t take a big earnings miss to see a trim back on the dividend.

I don’t want to say DBS Bank is priced to perfectly, but I would say it is quite fully priced here.

So… Buy DBS Bank or not

Full disclosure that I hold positions in Singapore bank stocks, but DBS Bank is not specifically one of those positions as I took profit in DBS a while back.

Would I buy more today?

Probably not frankly.

Fundamentally I see the 3 local banks as the same macro play, albeit with some flavour differences between them.

With my bank positions, I already have exposure to this industry.

And at these prices, sure the dividend yield is still nice, and there could be upside if earnings continue to grow.

But risk-reward is just fairly balanced in my view – hardly a compelling must buy.

Love to hear what you think though!

Would you buy more DBS Bank at close to all time highs, at a 5.9% dividend yield?