With the recent drop in T-Bills interest rates to 1.44%, I’ve been getting a lot of questions from readers on where is the best place to park cash while generating a high yield today.

A year-round favourite option are high yield savings accounts.

One great option is DBS Multiplier – where you can earn up to 4.1% p.a. if you transact in multiple categories, such as credit card spend, home loans, insurance or investments.

If you prefer to fulfil a straightforward process of simply crediting your salary and spending, you can earn up to 2.5% p.a. on your first S$100,000.

This is pretty attractive in today’s climate, especially when paired with DBS yuu Card for up to 18% cash rebates or 10 miles per dollar on your daily spend.

Let’s run through how this can work in practice.

Disclosures: This post is sponsored by DBS. All views and opinions expressed in this post are from Financial Horse.

Terms and conditions apply to all promotions stated herein. Please review the provider’s latest official T&Cs before applying or transacting.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

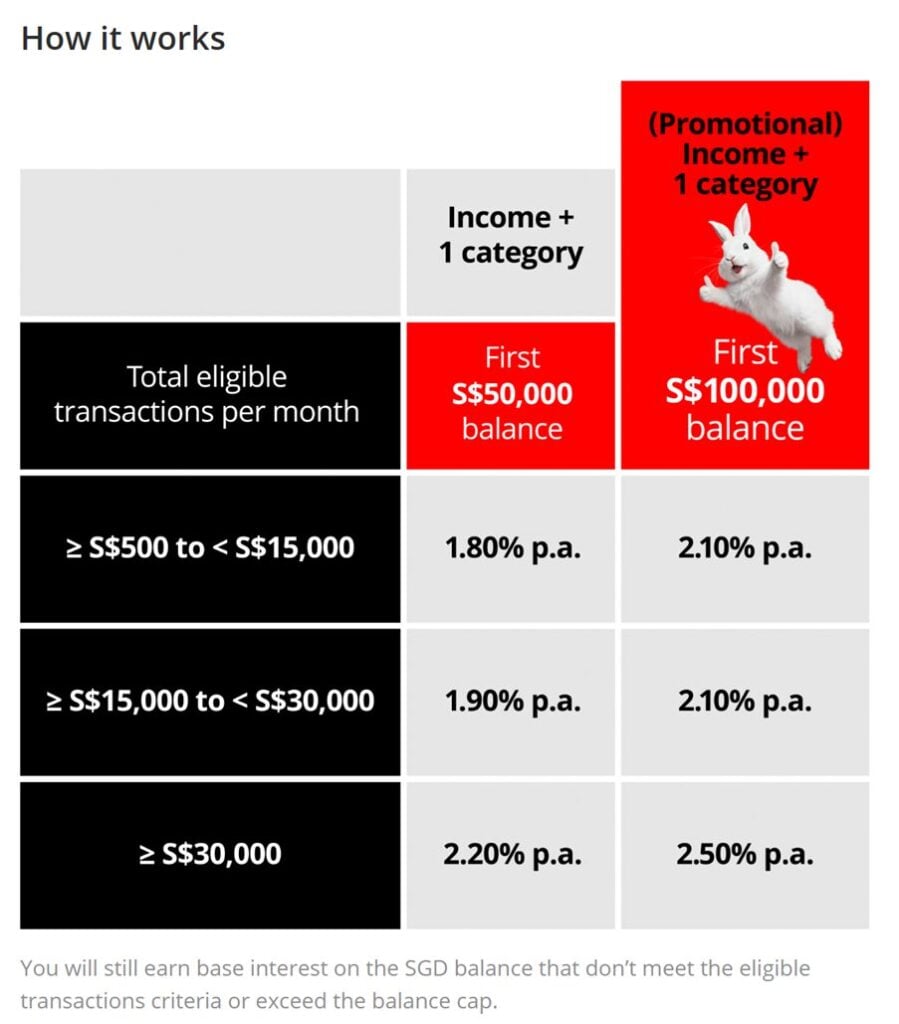

How to earn up to 2.5% p.a. on S$100,000 with DBS Multiplier Account?

If you are new to Multiplier, you can get up to 2.5% p.a. on your first S$100,000 with DBS Multiplier by simply crediting your salary and spending, from now until 31 December 2025.

The table below sets out how it works:

How it works?

- Open a Multiplier account

- Fund your account with fresh funds and maintain S$100,000 daily balance;

- Credit your salary via GIRO to any DBS/POSB account; and

- Transact in 1 of 4 Multiplier categories: Credit Card/PayLah! Retail Spend, Home Loan Instalment, Investment or Insurance

To qualify as ‘Income’ for this promotion, you just need to credit your monthly salary via GIRO with any of your DBS/POSB SGD-denominated accounts.

Of course, do note that these interest rates are accurate as of October 2025, and may be adjusted going forward.

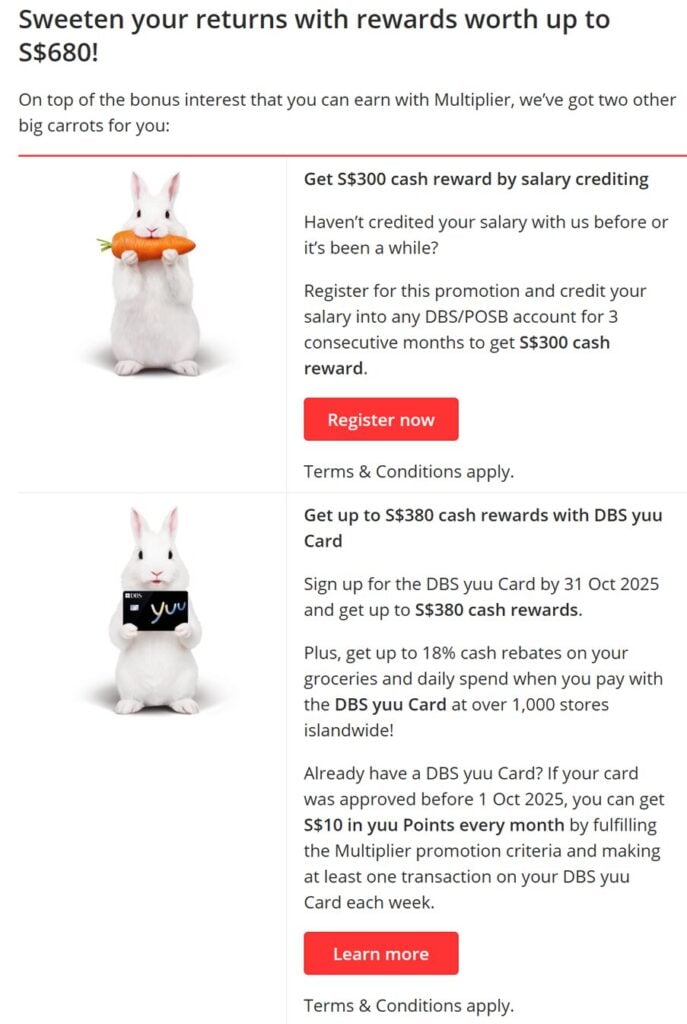

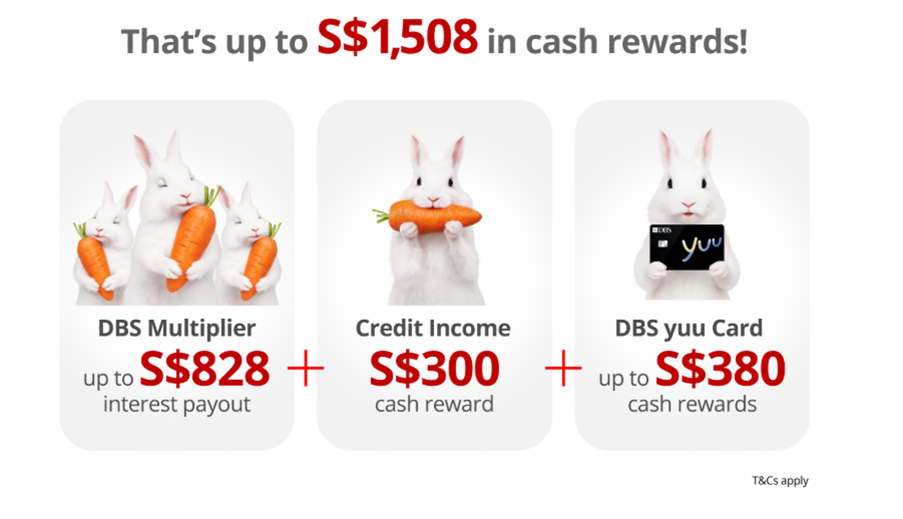

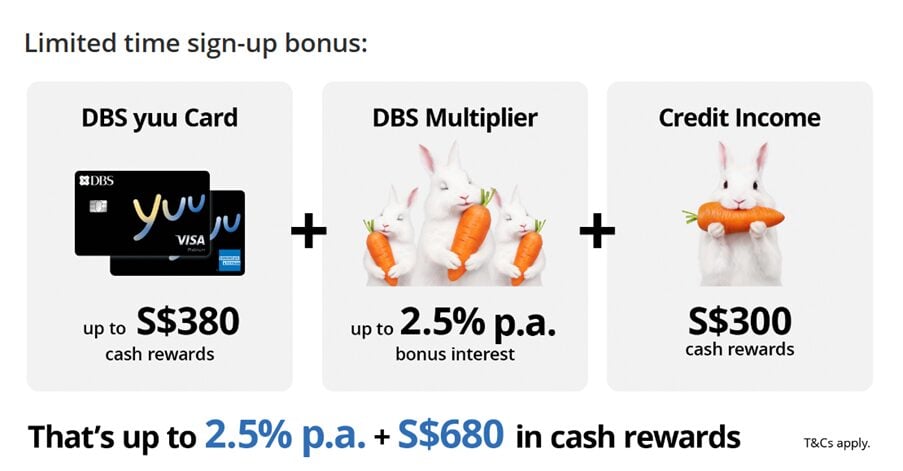

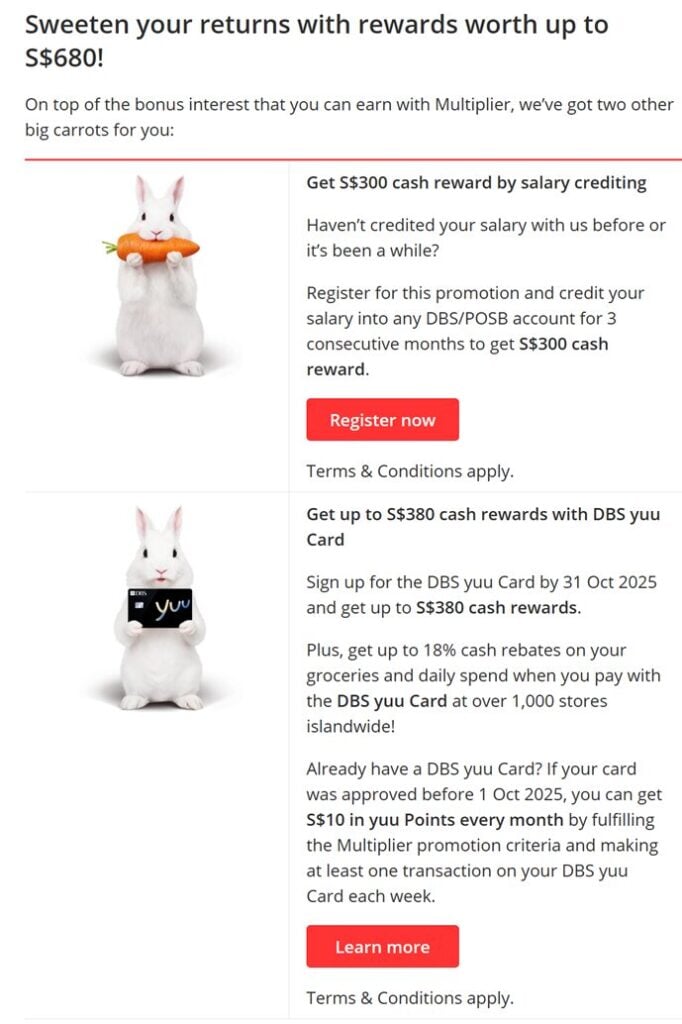

Additional cash rewards with salary credit and DBS yuu Card

In addition to the bonus interest, there’s attractive cash rewards being offered as well.

You can get S$300 cash reward when you credit your salary of at least S$1,600 per month (or S$500 NS allowance for NSF) for 3 consecutive months.

And you can get up to S$380 cash rewards if you sign up for the DBS yuu Card:

– New to DBS/POSB Cardmembers can enjoy S$380 cash rewards with promo code ‘DBSYUU’.

– Existing DBS/POSB Cardmembers can enjoy S$80 Esso Fuel Discount Vouchers. No min. spend and no promo code required.

If you already have a DBS yuu Card – and your card was approved before 1 Oct 2025, you can get S$10 in yuu Points every month by fulfilling the Multiplier promotion criteria and making at least one transaction on your DBS yuu Card each week.

This is definitely a great stacker reward to help sweeten the deal.

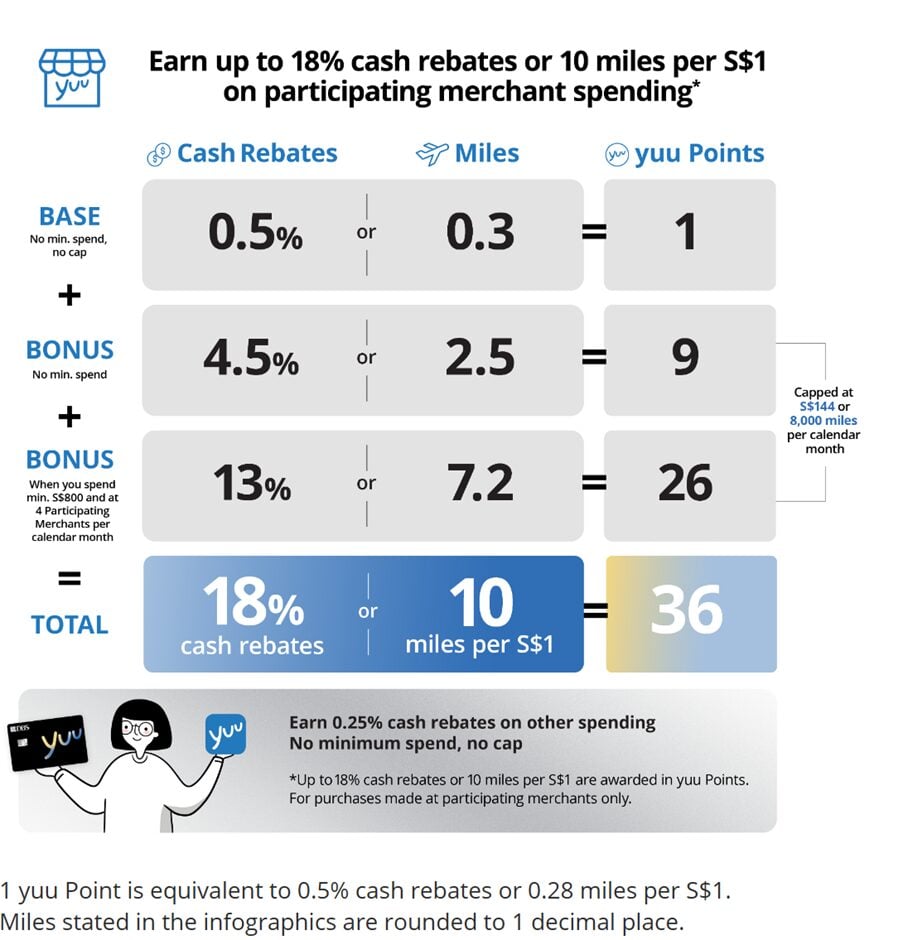

DBS yuu Card is a must have

The other great benefit of the DBS ecosystem is the DBS yuu Card.

DBS yuu Card is a practical must have.

Simply spend regularly at 4 participating merchants each month and meet a min. monthly spend of S$800 on your total card spend to get up to 18% cash rebates or 10 miles per S$1 on participating merchants.

And chances are very high because this includes big names like Cold Storage, Giant, Guardian, 7-eleven, foodpanda, Gojek, CHAGEE and SimplyGo.

Plus, even if you do not manage to meet the minimum spend requirement each month, you get to earn 5% cash rebates or 2.8 miles per S$1, which is really attractive

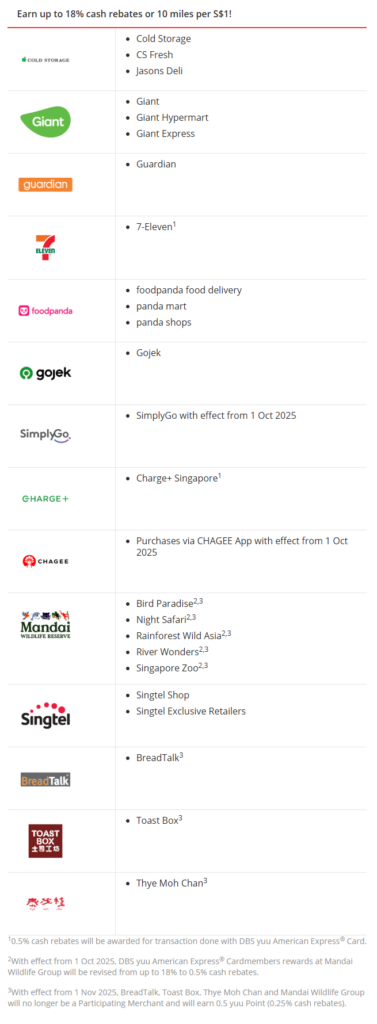

The list of participating merchants are as follows:

How does DBS Multiplier compare vs other Savings Accounts and cash yield options?

Let’s compare DBS Multiplier with other options.

Assuming you can only get a baseline rate of 2.5% with DBS Multiplier, this would be competitive with UOB One and OCBC 360.

If you can hit all the conditions and get 4.10%, then DBS Multiplier becomes best in class in terms of yield.

| Product | Indicative annual rate* | Maximum amount | Liquidity |

| DBS Multiplier | 2.5% p.a. (up to 4.10%) | 100k | Instant |

| UOB One | 2.5% | 150k | Instant |

| OCBC 360 | 2.45% | 100k | Instant |

| 6-month T-Bill | ~1.40 – 1.44% in latest auctions | Up to MAS allotment | Locked ~6 months |

| Singapore Savings Bonds (SSB) | 1.56% first-year; ~1.93% 10-yr average (Oct 2025 issue) | 200k per person | Redeem monthly (T+~1 mth) |

| SGD Money-Market Funds (e.g., Fullerton SGD Cash, LionGlobal SGD MMF) | ~2.0% recent range | No limit | T+1 |

*as of October 2025

Don’t forget that with both UOB One (spend ≥$500 + salary credit) and OCBC 360 (salary + save + spend) there are hoops to jump through too, so it is not a free lunch.

Of course, rates on variable-rate savings accounts and cash products are influenced by central-bank policy and market conditions, and may be subject to change at the provider’s discretion.

How does DBS Multiplier compare vs Fixed Deposits, SSBs, T-Bills and Money Market Funds?

Let’s compare DBS Multiplier with fixed deposits, T-Bills and Money Market Funds (“MMFs”).

Assuming you can hit sufficient conditions to get >2.0%.

Then DBS Multiplier is very attractive as you get (a) higher yields, and (b) instant liquidity.

Don’t forget this is a savings account, so unlike for instance, T-Bills or fixed deposits, which have a lock-up of ~6 months, you can withdraw the money from your multiplier account any time.

This liquidity advantage makes it very convenient as a base for your emergency fund / cash flow needs.

In other words, it would be ideal to use a high yield savings account like DBS Multiplier for your basic cash management needs, and then layer on T-Bills, MMFs, Singapore Savings Bonds etc. accordingly.

SSBs are more liquid than T-Bills or fixed deposits, but require a little more maintenance especially for those who like to ladder their bonds as SSBs reprice monthly.

SGD MMFs trailing gross yield ~1.8–1.9% YTD, and do have T+1 liquidity, but they aren’t SDIC insured.

Generally, compared to the other cash products, you may get a better yield with Multiplier if you’re within the DBS ecosystem and thus reliably fulfil several categories.

In any case, for those who are holding onto larger sums of cash (e.g. above 100k), being able to spread your cash across several cash instruments is a useful option which most people will take advantage of.

Sharing my thoughts on DBS Multiplier – How do I use DBS Multiplier?

Another great option, which I employ personally, is to link your CDP account to DBS, which allows all of your dividends to count as income for DBS Multiplier.

You can also use DBS Vickers Cash Upfront as your primary broker for SGX CDP stocks, which fulfils the investment category.

Layer on the super useful DBS Yuu Card, and this will satisfy the credit card spend category.

This means that in most months with the above set up, you can get 2.20% or 3.00% on S$100,000 with DBS Multiplier.

Depending on the investments I make that month, and whether it crosses the S$30,000 threshold.

This is one set-up that you can consider which is honestly very convenient, as the ecosystem lends itself easily to your everyday savings, spending and investing needs.

On top of that, if you have a mortgage with DBS, or insurance, you can more than easily hit 3+ categories.

In which case, the interest rate can go as high as 4.10%, which is a pretty great deal in my opinion.

Sweeten the deal with cash rewards

For new to DBS Multiplier customers, do take advantage of the promotion until 31 December 2025, to enjoy up to 2.5% p.a. on your first S$100,000 by simply crediting your salary and spending.

Don’t forget the additional cash rewards as well – which applies if you haven’t credited your salary before or it’s been awhile – plus the cash rewards if you sign up for DBS yuu Card!

Find out more here!

Disclosures:

This post is sponsored by DBS. All views and opinions expressed in this post are from Financial Horse.

Terms and conditions apply to all promotions stated herein. Please review the provider’s latest official T&Cs before applying or transacting.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors and monies and deposits denominated in Singapore dollars under the Supplementary Retirement Scheme are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Monies and deposits denominated in Singapore dollars under the CPF Investment Scheme and CPF Retirement Sum Scheme are aggregated and separately insured up to S$100,000 for each depositor per Scheme member. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.