In the recent FH Premium portfolio update, I shared my views that we may be rapidly approaching a blow off top in the next 4 – 8 weeks.

Reasons that made me nervous are:

- We’re starting to see signs of exuberance in the market (look at US AI Tech and Crypto generally)

- Valuations across the board are no longer cheap after the huge post-April rally

- Market pricing in a Sep Fed rate cut as all but guaranteed makes me nervous that this is a sell the news kind of event (but with a potential rally heading into the rate cut)

Of course, we all know that you don’t want to sell too early because you miss out on those juicy late cycle exponential gains.

But at the same time, nobody times the top perfectly, and if you sell too late you also lose a good chunk of paper gains.

Because of that, I shared that depending on how the rally plays out (if at all), I may look to lock in some profits, and rotate the funds into “cheaper” areas where valuations are less stretched.

This led to the following great question from a reader:

Could you advise potential options to buy in USD after taking profit from US Tech/AI stocks? Given the drop in USD this year, I don’t want to realize my Forex loss and hence looking to deploy the USD for other safer US choices. Thank you.

This is an FH Premium article written in early Aug – I am making this available to all so that you are aware of my general macro view on markets.

For my latest macro views, and what I am buying/selling, check out FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

What to invest in as a Singapore Investor – other than “expensive” US AI Tech or Crypto?

As you would now by now, I like to plug the question into AI to get a quick and dirty high-level answer.

This was what I got:

If you think US AI/crypto are bubbly, rotate USD into:

(i) value-heavy non-US equities (UK, Europe ex-US, Brazil, selective China/HK),

(ii) real assets (energy, gold miners), and

(iii) duration (USTs 5–10yr).

Barbell structure

- 40–55% quality value equities: UK (core), Europe ex-US, Brazil, and a measured China/HK sleeve. Tilt toward cash-rich, buyback-heavy names; avoid deep cyclicals without balance-sheet cover.

- 25–40% duration ballast: 5–10yr USTs (IEF) as your primary hedge; add a smaller TIPs sleeve if you’re worried about inflation surprise.

- 10–20% real assets: energy equities + gold miners for inflation/ geopolitical convexity.

The UK large value market (FTSE All-Share / FTSE100, via EWU/ISF LN) is trading at around 12–12.5x forward P/E with a forward dividend yield of ~3–4% (June–July 2025). Upside drivers include high buyback yields, energy and financials strength, and listings reform attracting renewed foreign inflows. Risks come from sterling strength denting USD returns and commodity income weakness. Risk-reward is balanced: mid-discount could narrow, but downside cushioned by income.

Europe ex-UK broad value (STOXX 600, via IEUR/VGK US) sits at ~14.2x forward P/E with ~3.4% forward dividend yield (July 2025). Catalysts are banks re-rating, defence capex, reshoring, and persistent discounts to the US. However, tariff/currency swings and earnings downgrades are risks. Risk-reward is moderate: less discount than UK, more macro noise.

Brazil broad/value (EWZ/IBZL) is at ~9.5x forward P/E with ~6–7% forward dividend yield (July 2025). Upside comes from a rate-cut cycle, commodity leverage, and fiscal discipline. Key risks are policy volatility and BRL FX. The risk-reward is attractive: cheap entry point, but carry/FX drives outcomes.

China/HK broad value (MSCI China/HFI + deep-value sleeves) trades at ~12.0x forward P/E with ~2.6% forward dividend yield (July 2025). Upside rests on policy support, SOE dividends, antimonopoly overhang easing, and global positioning. Risks are policy execution, geopolitics, and property downside. Risk-reward is barbell-shaped: big upside if reforms follow through, but meaningful tail risks.

Singapore REITs (income) (SRT/SRU, BYJ) are trading at ~0.88x P/NAV with ~7.3% forward dividend yield (July 2025). Tailwinds include peaking rate cuts, lower funding costs, and high cash yields. Risks come from office oversupply and SGD FX vs USD. The risk-reward is carry-led: attractive income now, but de-rating if costs materialize.

Gold miners (GDX/GDXJ) are trading at discounts to spot gold, with strong free cash flow margins on record bullion (Feb–Apr 2025). Upside stems from operating leverage to gold, buybacks, and balance sheet repair. Risks are cost inflation, single-asset exposures, and jurisdictional risk. Risk-reward is convex: cheap optionality on bullion staying high.

Finally, US duration (ballast) (USTs – 10yr, IEF; 30yr, TLT) offers ~4.2–4.4% carry income (June–July 2025). Upside is driven if growth cools, Fed cuts, and equities diversify. Risks are sticky inflation repricing and the associated term premium. Risk-reward is asymmetric: carry is strong, but inflation cuts the upside.

My personal views?

For what it’s worth, I didn’t super like this answer from AI.

I thought about it a bit more, and I narrowed it down into 3 key areas that I would consider rotating cash into if I were to take profits in US Tech and Crypto on the basis that they are bubbly:

- US value stocks – Biotech, Consumer stocks etc

- China

- Singapore

Let’s talk about each of them.

US value stocks – Biotech, Consumer stocks etc

US stocks are split into 2 right now – MAG7 and AI related stocks are flying.

While everything else isn’t doing so great.

You can refer to the FH Stock Watch for views on single names.

But there are a whole bunch of Biotech and Consumer stocks that I think are pretty cheaply valued.

Of course, this definitely goes into the realm of stock picking.

If you didn’t want to stock pick?

Then I may consider just using any big rally to reduce US exposure, and rotate into China or Singapore.

At least until we see valuations / exuberance come down.

Sidenote – Luxury stocks offer good risk-reward?

On that note – another sector that I’ve been following for a while and find attractive for longer term investors is luxury.

Think names like LVMH (almost an ETF of the world luxury brands) or Richemont (owns Cartier and VCA).

Both are down massively from highs, and trade at 20x trailing P/E today.

Largely because of weak China consumer sentiment (almost 30% of global luxury demand today), and weak global consumer sentiment (due to a weaker global economy and inflation).

Yes look at the charts and it’s fairly obvious they’re still trending down so it’s still too early to buy.

But take a longer term 5 – 10 year view, and I’m pretty sure demand for luxury goods will come roaring back some time in the next 5 – 10 years.

So this is another area I’m keeping a very close eye one, but with the knowledge that it’s probably still trending down for now.

China stocks – cheap valuations, decent dividend yield

On China – with the huge rally in US stock valuations.

I’m starting to find China interesting again.

The thought process goes like this:

- China stocks are very cheap today – so if there is a meaningful turnaround in China you get strong upside

- Of course, you don’t know when the turnaround will happen, so you focus more on dividend paying stocks (where the dividend provides some returns while you wait)

- And because valuations are generally cheap across the board, this does cushion downside risk in the event that China stocks continues to underperform.

AI gave a very good summary on how to play the China exposure – this playbook I really liked:

Executive Summary (3 lines):

- Barbell China exposure:

- 40–55% SOE high-dividend value

- 25–35% selective growth

- 10–20% compute/power infra;

- optional 0–10% EV value chain.

- Rationale: policy alignment (Two Sessions fiscal push, SOE “market-value management”), strong carry while waiting for macro turn.

- Avoid for now: private property developers; generic solar manufacturers (overcapacity).

Core SOE Dividend Value (40–55%) — income + policy tailwind

- Telecoms: China Mobile, China Telecom, China Unicom. Stable cash flows, rising dividends/buybacks, AI/DC connectivity optionality.

- Energy: CNOOC, PetroChina. 6–8% yields, strong FCF, payout discipline.

- Large Banks (measured weight within sleeve): ICBC, CCB. Quasi-bond yields; supported by rate cuts/national team; cap property/NPL risk by sizing smaller than telcos/energy.

Platforms & Domestic Demand (25–35%) — recovery beta + buybacks

- Internet platforms: Tencent, Alibaba, Meituan. Easing policy tone, profit discipline, heavy repurchases; sensitive to consumption cycle/competition.

- Travel/Retail (small satellite): China Tourism Group Duty Free; cyclical, higher beta.

Compute & Power Infrastructure (10–20%) — “new productive forces”

- Grid upgrades, power equipment, utilities adjacencies leveraged to AI/data-centre demand; prefer diversified baskets/strong SOEs; watch DC overbuild cleanup.

EV Value Chain (0–10%, trading sleeve)

- Only top winners (e.g., BYD). Policy support vs. EU/US trade defence; keep tight sizing.

Why this works (2025 policy & macro):

- Fiscal expansion (incl. ultra-long bonds) + KPI pressure for SOEs to lift dividends/buybacks = carry-led return with policy support.

- If demand stabilises, platforms and travel lead early rebound; infra benefits from compute/power buildout even as overcapacity is managed.

Risk–reward (12–24m):

- Upside: stimulus follow-through; sustained dividend hikes/buybacks; property stabilisation; AI/power capex pull-through.

- Downside: property drag/deflation; tariff/geopolitics; capex/energy costs hurting FCF; industry overcapacity clean-ups.

- Outcomes (indicative):

- Bull: SOE value +20–30% incl. yield; platforms +40–60%.

- Base: SOE value +10–20%; platforms +10–30% (dividends dominate).

- Bear: SOE value –5–15%; platforms –20–35%; EV worse.

Implementation (SG investor):

- Prefer HK lines; simple route via SGX ETFs (HST/HSS for tech; JK8/VK8 for A-leaders; CSI Dividend via SSE-SGX link).

- Currency: HKD peg reduces CNH risk; hold some USD for flexibility.

- Entry: DCA in 3–6 tranches or buy on clear inflection (e.g., home-price YoY improves).

- Risk controls: Single-name cap 5–7%; adhere to sleeve caps; keep avoid sectors minimal.

Uncertainties to watch: tariff path; timing of property trough; pace/ROI of compute-power buildout amid DC glut management.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

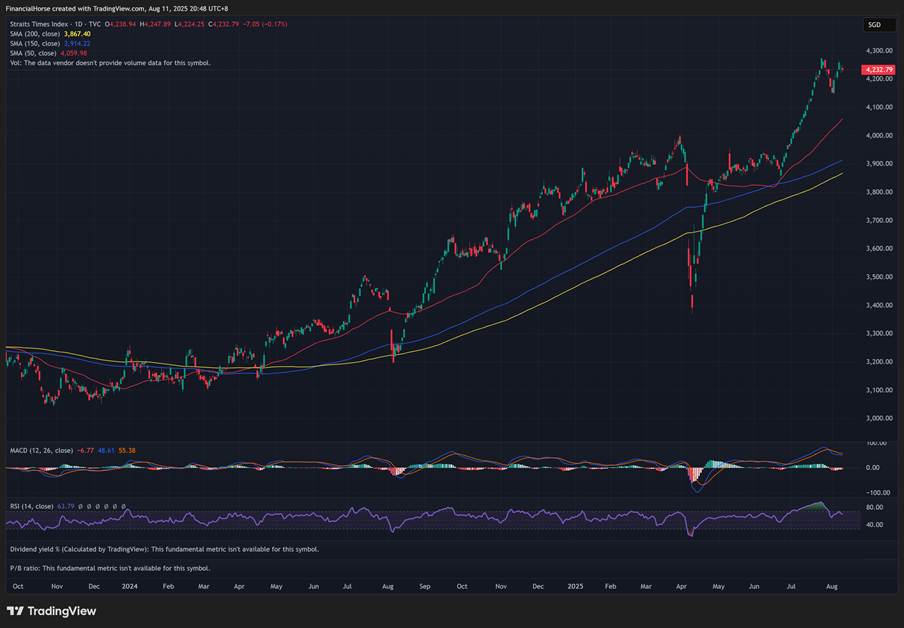

Singapore stocks – no longer cheap after the rally, but still offer decent dividend yields at a fair price

And then we have Singapore.

When the chart for STI ETF looks like this (massively outperforming the S&P500), you know something is up.

Singapore stocks were attractive for the simple reason that they are a safe haven from US-China trade war, and at the start of the year they offered attractive dividend yields and cheap valuations.

With the huge rally in SGX stocks this year, dividend yields sit around 5% today which is not longer as attractive.

But still a decent spread vs the risk free when you consider that the SG 10 year yield sits at 1.9%.

If you think the US is expensive, I still think there is value to be had in the SGX (comparatively speaking).

On how to build Singapore exposure, this was what AI gave:

Executive Summary (3 lines)

• Best SG beta: Banks, Energy/Infra platforms (Keppel, Sembcorp), Offshore/Marine (Seatrium); balance with DC/Logistics REITs, Aviation services (SIAEC/SATS), SGX, and Defensive consumer (Sheng Siong).

• Setup: growth positive but moderating; MAS easing bias; rates drifting lower → support for REITs/cyclicals; banks’ dividends cushion NIM drift.

• Key risks: global trade/tariffs, China demand, oil/shipping cycles. Size with defensives and strict single-name caps.

High-level allocation (12–24m; illustrative, not advice)

Core (50–60%)

- Banks (30–35%) — DBS/OCBC/UOB mix for carry + fee recovery; keep position caps 8–10% each.

- Energy/Infra platforms (15–20%) — Keppel/Sembcorp for renewables & data-centre build-out, asset recycling.

- Market infrastructure (5%) — SGX as volume/derivatives beneficiary.

Cyclical alpha (20–25%)

- Offshore & marine (10–12%) — Seatrium; backlog visibility, margin normalisation; watch delivery milestones.

- Aviation services (8–12%) — SIAEC/SATS over airline to reduce yield volatility; levered to tourism/MRO recovery.

Yield ballast (15–20%)

- DC REITs (8–10%) — e.g., KDCREIT; rate tailwind + structural demand.

- Logistics REITs (7–10%) — e.g., MLT; diversified APAC exposure; focus on gearing/hedging.

Satellite growth/defensive (5–10%)

- Semi-services (AEM/Venture) for AI/automation cycle optionality (higher risk).

- OR Defensive consumer (Sheng Siong 0–5%) as downturn hedge.

Cash (0–5%) — dry powder for volatility.

Rationale by bucket (why this mix)

- Banks: cornerstone income (5–7% yields) + buybacks; downside mainly NIM compression/credit costs.

- Keppel/Sembcorp: platform exposure to secular infra/renewables/data-centre capex; execution/FX policy are main risks.

- Seatrium: multi-year orderbook and operating leverage; oil/CapEx delays are swing risks.

- REITs: easing rates stabilise DPU; secular DC/logistics demand; watch refinancing, FX, WALE.

- Aviation services: tourism normalisation without airline yield risk; SATS integration and cost inflation are watch-outs.

- SGX: benefits from regional volatility and derivatives growth.

- Semi-services/Defensive consumer: barbell for upside optionality vs shock absorber.

Sizing & risk controls

- Cap single-name ≤8–10%; pair cyclical bets (Seatrium) with defensives (REITs/Sheng Siong).

- Stage entries around earnings, ex-div dates, FPSO deliveries, and REIT funding updates.

- Monitor dials: MAS policy statements, banks’ NIM/credit costs, REIT debt costs/hedging, STB arrivals.

- Exit/trim on guide-downs, project slippage, or rising funding costs.

My thoughts?

For what it’s worth, I didn’t like the AI answer as much as I did the China one.

I thought if it were me, I would allocate the bulk of the portfolio into Singapore banks / REITs, for a blended 5-6% dividend yield.

You’re basically paid to wait, and any capital gain is pure upside, while any capital loss is cushioned by the yield.

Then with the rest I would allocate into cyclical / growth plays via stock picking.

Think names like Sea Ltd, SIA, SGX, Keppel/Sembcorp, Singtel, SATS, and so on.

Closing Thoughts?

Just to be absolutely clear, I am not saying to sell all your US tech / Crypto and buy US value stocks, China stocks and Singapore stocks.

I am saying that where we sit today, I think US tech / Crypto looks somewhat exuberant, with a chance of a blow off top as we head into the Fed rate cut.

If indeed this happens, I would probably want to dial back on my exposure to those 2 sectors.

And because I don’t want to go fully into cash, I may consider deploying those funds into the 3 sectors shared above.

That being said, I would love to hear what you think though.

Any other sectors you think look attractively valued today?

This is an FH Premium article written in early Aug – I am making this available to all so that you are aware of my general macro view on markets.

For my latest macro views, and what I am buying/selling, check out FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Inverse equity ETFs ?

Perhaps at the right time…

Hi FH, thanks for the insightful piece. In your view, are Singapore banks still a good buy given elevated valuation?

Just shared views in the latest article – let me know if that addresses!