As you’ve probably heard by now.

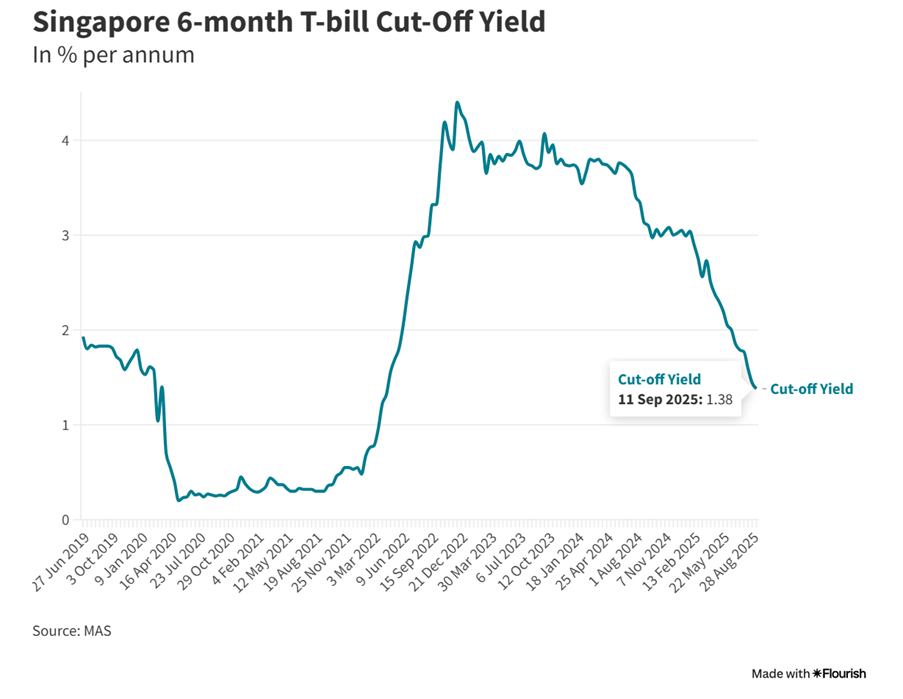

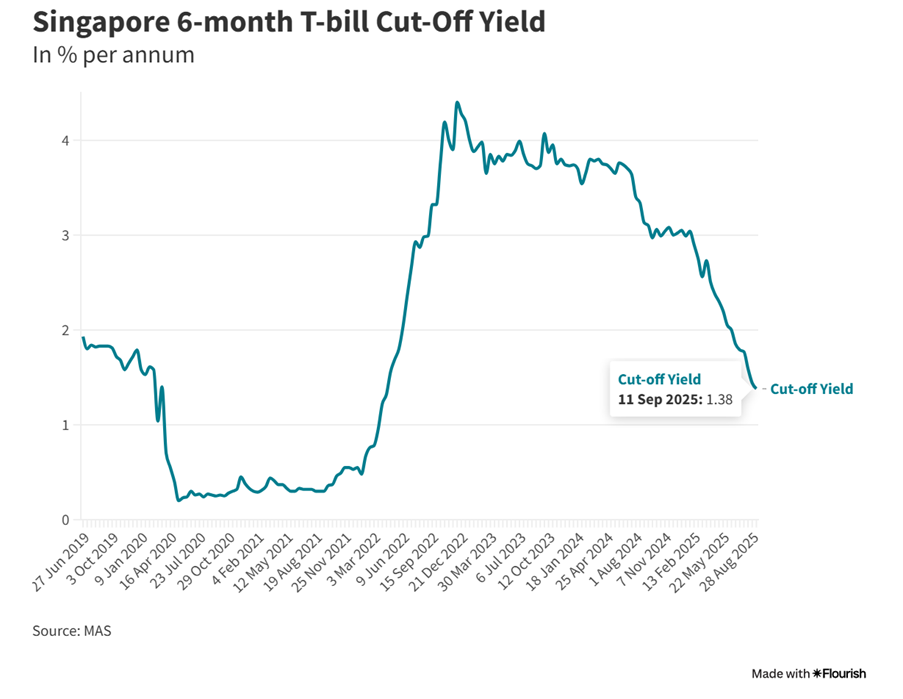

The latest 6-month T-Bills fell to an abysmal 1.38%.

That’s just flat out terrible.

What’s a dividend investor looking for income to do in times like that?

Let’s say I have a $1 million portfolio.

Is it still possible to invest at a 6% dividend yield to get a $5000 dividend income a month ($60,000 a year)?

Crunching some numbers – $1 million portfolio at 6% dividend yield?

So I crunched some numbers below with the help of a friendly LLM.

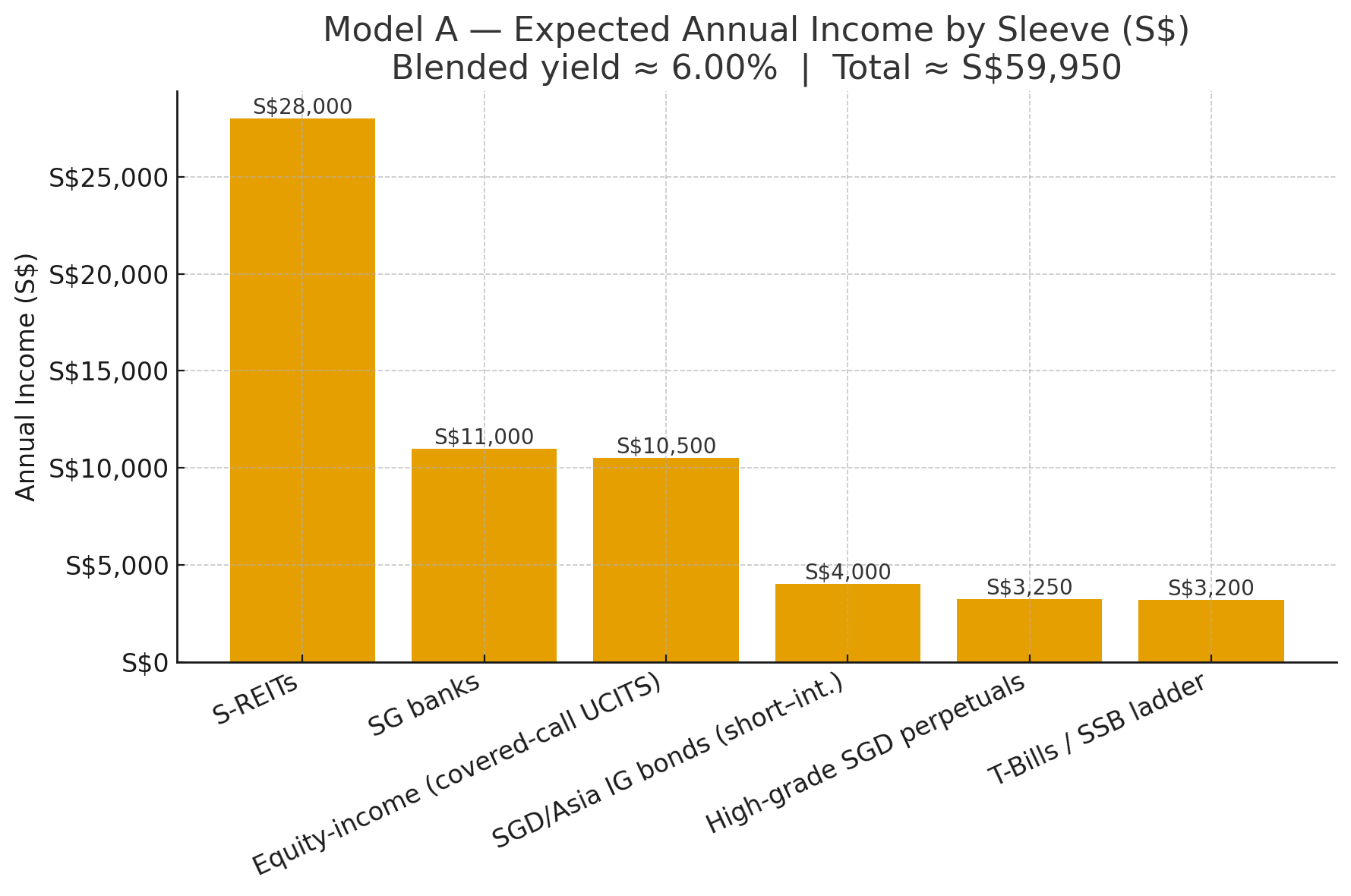

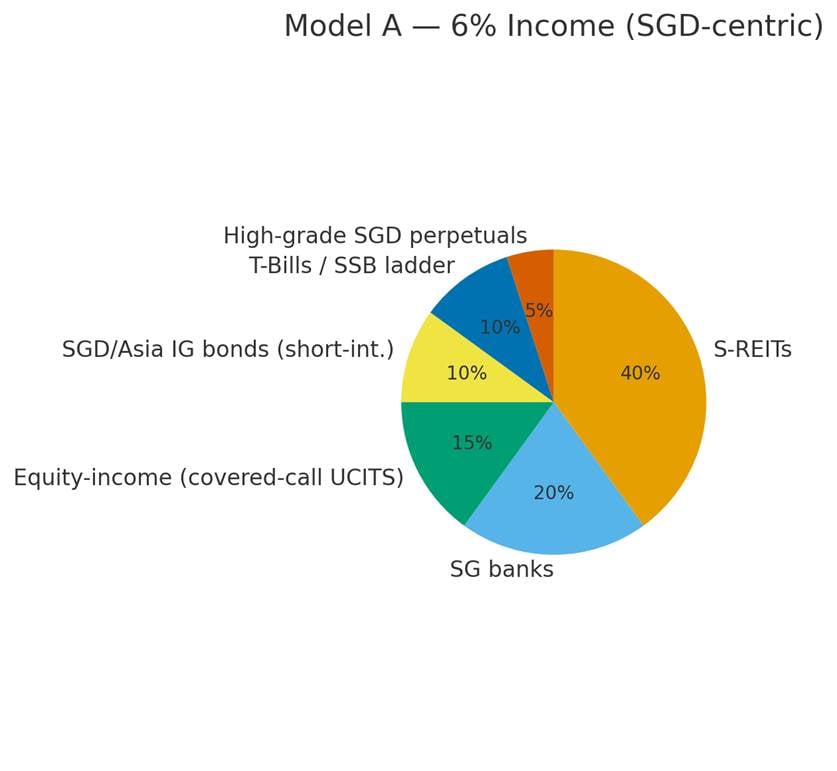

Model A Dividend Portfolio — “6% Income” (medium risk, SGD-centric)

Below is a concrete SGD 1,000,000 allocation that targets ~6.0% portfolio yield using conservative yield assumptions. It’s “medium” risk (not low): equity drawdowns are possible, but income should remain resilient across cycles.

| Sleeve | Weight | Assumed Yield | Notes / Vehicles (examples, not exhaustive) |

| Diversified S-REIT basket | 40% | 7.0% | Mix of large-cap industrial/logistics/data-centre/retail REITs or an SG/Asia REIT ETF |

| SG banks (DBS/UOB/OCBC) | 20% | 5.5% | Equal-weight; dividend + special/capital-return optionality |

| Equity-income (covered-call UCITS) | 15% | 7.0% | Irish-domiciled global equity premium income strategies; lower vol than equity beta |

| SGD/Asia IG bond ETF/fund (short–duration) | 10% | 4.0% | Corporate IG bias; short duration to limit rate risk |

| T-Bills / SSB ladder | 10% | 3.2% | 6-mo T-Bills rolled; SSB rung ladder for flexibility |

| High-grade SGD perpetuals | 5% | 6.5% | Select bank/Temasek-linked issues; size deliberately small |

| Total | 100% | ≈6.0% | Blended yield ≈ 5.995% on assumptions |

Key guardrails

- Single REIT ≤ 5% of portfolio; any one issuer (incl. perps) ≤ 3%.

- Perps cap ≤10% (we use 5%).

- No leverage/margin. Maintain 12 months expenses in T-Bills/SSB if you rely on the income.

Reasoning (how this hits 6% with controlled risk)

- Reality check: Truly low-risk SGD instruments (T-Bills, SSBs, IG bonds) don’t reach 6% cash yield. Hitting 6% requires equity income (REITs, banks) and a small credit sleeve (perps).

- Income resilience: Large-cap S-REITs and SG banks have defensible earnings/dividends through cycles; covered-call UCITS funds dampen volatility and convert more return into cashflow.

- Rate sensitivity barbell: REITs benefit if rates fall; banks cushion if NIMs stay elevated; short-duration IG bonds/T-Bills reduce NAV swings.

- Tax/estate efficiency: Prefer Irish-domiciled UCITS for foreign equity income to lower US dividend WHT and avoid US estate-tax exposure.

- Sizing risk: Equity-like sleeves (40% REITs, 20% banks, 15% equity-income) are what mathematically lift yield to ~6%—hence “medium” risk label. The bond/T-Bill anchor and tight position limits control tail risk.

How accurate are the assumption for this dividend portfolio?

There are 2 big points that jump out for me.

The first – is that if you want to achieve 7% dividend yield on a diversified S-REIT portfolio today.

You do need to take on a decent bit of risk.

After the rally – a blue chip REIT like CICT or Frasers Centrepoint Trust pays a low 5% dividend yield.

Which means you won’t hit 7% blended yield unless you mix in some small caps / higher risk REITs.

That’s a pretty big point, which means suddenly you’re no longer running a low risk portfolio, but what could be a pretty volatile portfolio with equity style risk.

The second point of course, is that getting 3% yield on a mix of T-Bills and Singapore Savings Bonds today is just not realistic – given the sharp fall in interest rates.

Because of that, frankly my gut feel is that this portfolio is not too realistic in today’s climate.

| Sleeve | Weight | Assumed Yield | Notes / Vehicles (examples, not exhaustive) |

| Diversified S-REIT basket | 40% | 7.0% | Mix of large-cap industrial/logistics/data-centre/retail REITs or an SG/Asia REIT ETF |

| SG banks (DBS/UOB/OCBC) | 20% | 5.5% | Equal-weight; dividend + special/capital-return optionality |

| Equity-income (covered-call UCITS) | 15% | 7.0% | Irish-domiciled global equity premium income strategies; lower vol than equity beta |

| SGD/Asia IG bond ETF/fund (short–duration) | 10% | 4.0% | Corporate IG bias; short duration to limit rate risk |

| T-Bills / SSB ladder | 10% | 3.2% | 6-mo T-Bills rolled; SSB rung ladder for flexibility |

| High-grade SGD perpetuals | 5% | 6.5% | Select bank/Temasek-linked issues; size deliberately small |

| Total | 100% | ≈6.0% | Blended yield ≈ 5.995% on assumptions |

Model B Dividend Portfolio — “Safer Income” (lower volatility; ~4.8–5.3% cash yield)

Another model was proposed to me.

This one was pitched as being “safer”, but the downside being that the yield drops to 5%.

If you really want to hit 6%, then you need a bit of active management to sell a bit from your winners each year.

| Sleeve | Weight | Yield Assumption | Comment |

| S-REITs | 25% | 6.8% | Tilt to stronger balance sheets |

| SG banks | 20% | 5.5% | |

| SGD/Asia IG bonds | 20% | 4.0% | Short–int., diversified |

| T-Bills / SSB ladder | 15% | 3.2% | Liquidity buffer |

| Global dividend UCITS | 10% | 4.5% | Non-US domiciled |

| Cash/MMF | 10% | 3.0% | Dry powder / rebalancing |

Blended yield ≈ 4.8–5.3%. To net 6%, add a 1.0–1.2% annual sell-rule (e.g., quarterly pro-rata) from winners—historically improves sustainability vs chasing higher coupons.

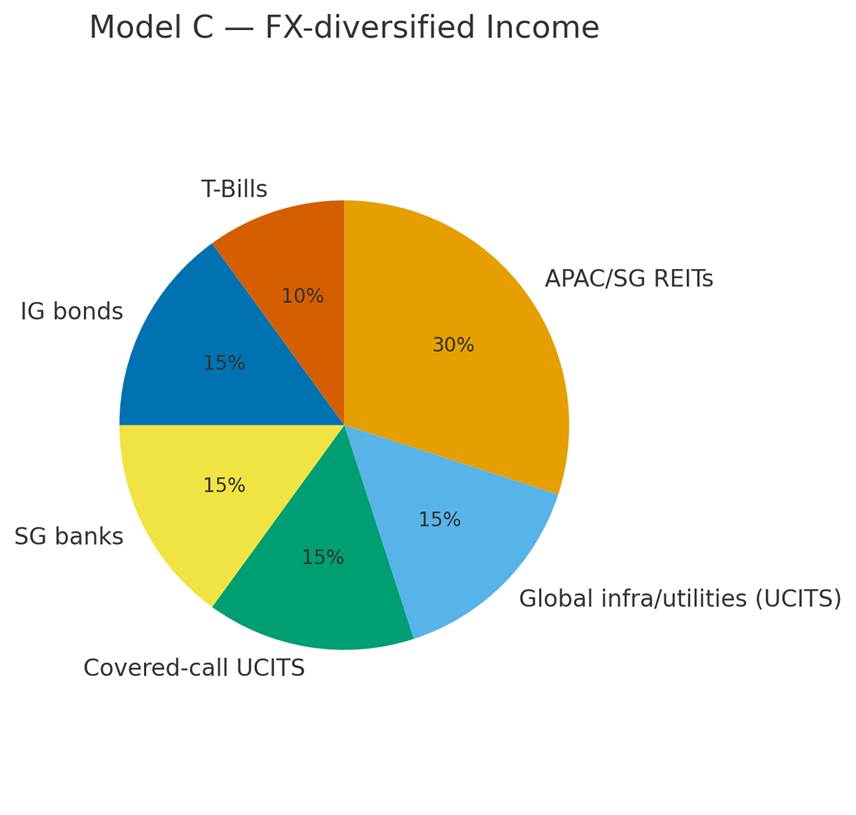

Model C Dividend Portfolio — “FX-diversified Income” (~5.5–6.0% target, more global)

Yet another variant – is that if you’re afraid of too much exposure to Singapore.

You can do a much higher global tilt like the below:

- 30% APAC/SG REITs, 15% global infra/utilities (UCITS), 15% covered-call UCITS, 15% SG banks, 15% IG bonds, 10% T-Bills.

- Hedge half of USD exposure if SGD strength matters to you. Yield near 5.6–6.0% depending on vehicles/FX.

Action Plan for the Dividend Portfolio (practical checklist)

This was the “instructions” given to me together with the model portfolio above.

Which actually does provide pretty useful guidance and colour.

Design & governance

- Define income need vs volatility tolerance: if 6% is a hard floor, use Model A; if drawdowns worry you, use Model B + 1% sell-rule.

- Set position limits (issuer ≤3%, single REIT ≤5%, perps ≤10%).

- Decide FX policy (unhedged vs 50% USD-hedged for global funds).

Implementation

- Open/confirm an SG broker with access to SGX + LSE (UCITS).

- Build over 3–6 tranches (e.g., monthly) to reduce timing risk; place T-Bill/SSB ladder monthly.

- For REITs: pick 6–10 names across industrial/logistics, DCs, retail, office, hospitality; bias to lower gearing, long WALE, positive reversion.

- For banks: equal-weight DBS/UOB/OCBC; reinvest specials if any into bonds/T-Bills to stabilise income.

- Equity-income sleeve: choose Irish-domiciled, distributing covered-call strategies; prefer global diversified mandates.

- IG bonds: use short-duration SGD/Asia IG ETFs/funds; avoid concentrated single-issuer SGD bonds.

- Perps: restrict to Tier-1 local credits; stagger call dates; size small (5%).

Ongoing controls

- Rebalance annually back to target weights; reinvest excess into the lowest sleeve.

- Stress test: assume REIT dividends −15% and bank dividends −10%; confirm portfolio still covers your income needs.

- Track 3 risks quarterly: (i) rate path (REIT sensitivity), (ii) credit spreads (perps), (iii) FX (if unhedged USD).

Notes on assumptions & uncertainty

- Yields quoted are conservative estimates, not guarantees, and will move with rates, rents, FX, and credit spreads.

- Foreign-listed funds may suffer withholding taxes and tracking differences; check KIDs/fact sheets before execution.

- If you require very low volatility, accept a lower cash yield and supplement via a disciplined sell-rule rather than loading up on higher-risk coupons.

How I will invest to get $5000 dividend income a month? $1 million portfolio at 6% dividend yield?

I think generally speaking.

It looks like with the fall in interest rates.

You’re not going to be able to build a 6% dividend yield portfolio, unless you’re comfortable with a fair bit of risk.

5% is a more realistic target today, without taking on too much risk.

If this were me though – unless I really need the income.

I would probably mix in some growth potential.

Building a pure dividend portfolio in this climate feels very one-sided, and I would really want some growth exposure.

But I’m also conscious valuations are very expensive, and things are close to all time highs here.

So I would average in over a period of time especially for growth plays.

What if I want to mix in some growth potential into the investment portfolio?

Here are the amended models proposed to me, to mix in some growth exposure.

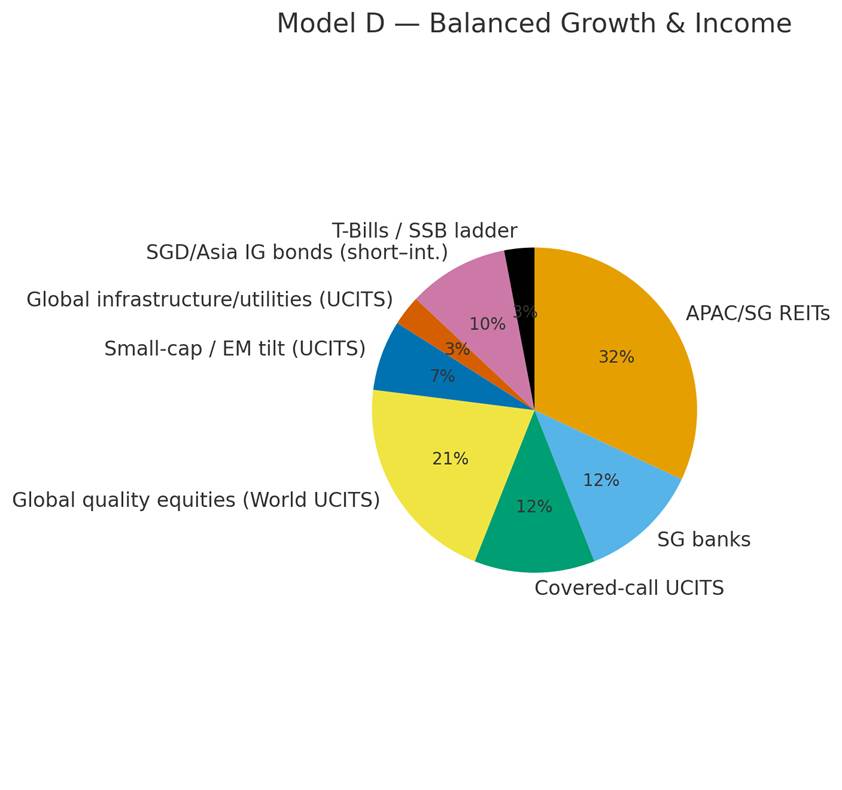

Model D Dividend / Growth Portfolio — Balanced Growth & ~4.8–5.0% yield

| Sleeve | Weight | Assumed Yield | Est. Annual Income (S$) | Role / Examples |

| APAC/SG REITs (diversified) | 32% | 6.8% | 21,760 | Large-cap industrial/logistics/retail REIT mix |

| SG banks (DBS/UOB/OCBC) | 12% | 5.5% | 6,600 | Core income + upside if NIMs persist |

| Global equity premium income (covered-call UCITS) | 12% | 7.0% | 8,400 | Smooths cashflow; trims upside |

| Global quality equities (World UCITS) | 21% | 1.6% | 3,360 | Long-run growth engine (e.g., IWDA/SWDA, CSPX-type) |

| Small-cap / EM tilt (UCITS) | 7% | 2.0% | 1,400 | Diversifies factor/region (e.g., WSML, EIMI) |

| Global infrastructure/utilities (UCITS) | 3% | 4.0% | 1,200 | Defensive, inflation-linked assets (e.g., INFR) |

| SGD/Asia IG bonds (short-int.) | 10% | 4.0% | 4,000 | Rate/credit ballast (e.g., ABF SG Bond A35; SGD IG ETF) |

| T-Bills / SSB ladder | 3% | 3.2% | 960 | Liquidity buffer |

| Total | 100% | — | ≈ 47,680 (≈4.77% yield) |

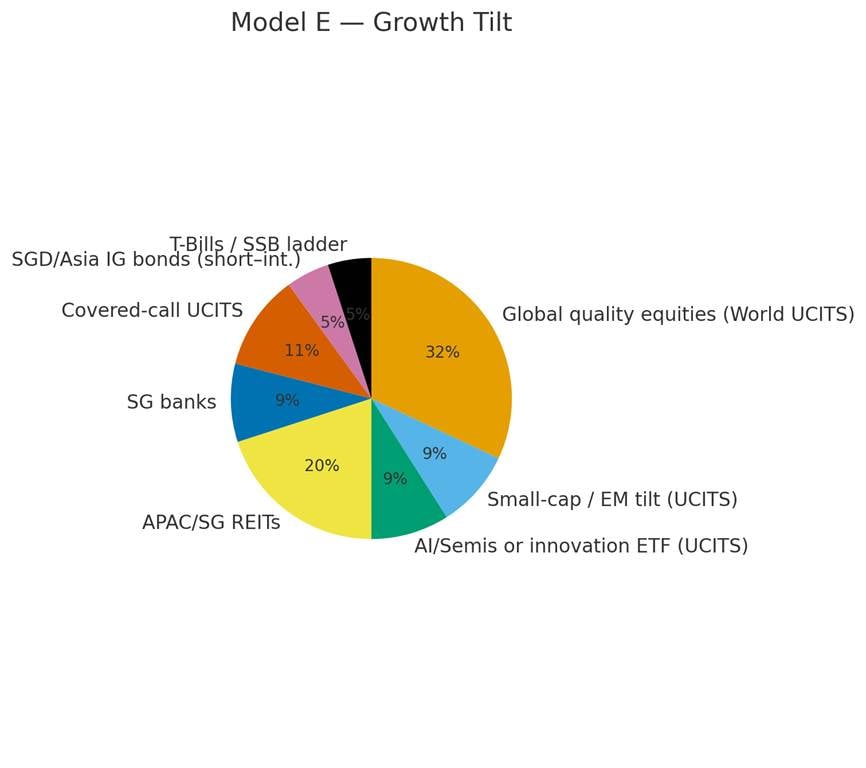

Model E Dividend / Growth Portfolio — Growth Tilt & ~3.7% yield (higher upside, more NAV swings)

| Sleeve | Weight | Assumed Yield | Est. Annual Income (S$) | Role / Examples |

| Global quality equities (World UCITS) | 32% | 1.6% | 5,120 | Core growth |

| Small-cap / EM tilt (UCITS) | 9% | 2.0% | 1,800 | Cyclical beta |

| AI/Semis or innovation ETF (UCITS) | 9% | 0.5% | 450 | Thematic upside; minimal yield |

| APAC/SG REITs | 20% | 6.8% | 13,600 | Income anchor |

| SG banks | 9% | 5.5% | 4,950 | Rate-cycle hedge |

| Global equity premium income (covered-call UCITS) | 11% | 7.0% | 7,700 | Cashflow cushion |

| SGD/Asia IG bonds (short-int.) | 5% | 4.0% | 2,000 | Stability |

| T-Bills / SSB ladder | 5% | 3.2% | 1,600 | Liquidity |

| Total | 100% | — | ≈ 37,220 (≈3.72% yield) |

Notes on implementation for the Dividend / Growth Portfolio (SG investor):

And here are the “instructions” provided:

- Prefer Irish-domiciled UCITS for foreign equity exposure (tax/estate efficiency).

- Use distributing share classes for income sleeves; accumulating for growth sleeves (add a quarterly 1% sell-rule if you need more cashflow).

- Keep any single issuer ≤3% of the portfolio; single REIT ≤5%; perps optional and capped ≤5% if you re-add them later.

Reasoning (why this balances growth with income)

- Shift from income-only to total-return: You still harvest reliable income (REITs/banks/covered-call) but reallocate ~28–50% into global growth engines (quality, small/EM, infra), improving long-term CAGR and inflation defense.

- Barbell volatility: REITs/banks/calls dampen cashflow volatility; global equities and a small thematic sleeve drive upside.

- Drawdown math: With ~50–60% equity beta, expect -15% to -25% peak-to-trough every few years; bond/T-Bill sleeves cushion the worst episodes.

- Rate/path neutrality: REITs win if rates fall; banks help if rates stay higher; short-duration IG limits duration pain.

- FX & domicile: Global funds introduce USD/EUR/JPY; hedge 0–50% of bond/infra sleeves if SGD volatility bothers you; leave equities mostly unhedged for long-run growth.

How I will invest to get $5000 dividend income a month? $1 million portfolio at 6% dividend yield?

Gun to my head – if you made me choose one of the 5 portfolios above?

I think it would be a toss up between D and E for me.

It all goes back to how important is the dividend income in my view.

If you absolutely need the 6% dividend yield, then you have no choice but to go out the risk curve and focus purely on income plays.

Bit if you don’t absolutely need the dividend yield, I think D and E are much more balanced portfolios.

Personally I quite like the look of Portfolio E, and I think it’s the closest to my current portfolio today.

But if you want an income tilt, then frankly Portfolio D might be a pretty decent alternative too.

Love to hear what you think though!

Which portfolio do you find the most attractive for your own situation?

This article is written on 12 Sep 2025 and will not be updated going forward. My latest personal portfolio, stock watch, and macro views are shared on FH Premium.

5% each in these 8 stocks of United Hampshire, Keppel Pacific Oak, PRIME US, Fraser logistics commercial trust, asian pay tv trust, Link REIT, NTT DC reit, ST Engineering

10% each in ocbc and uob

50% in the new lionglobal Singapore short term duration bond fund of 3%

This should do the trick in creating a 7% dividend yielder

Some of those REIT names look pretty high risk, I’m not sure I would view them as suitable for a low – medium risk portfolio.

But I guess thats the drawback of trying to hit 7% dividend yield – no realistic way of hitting that number without some risk.