With the latest 6-month T-Bills yielding at 1.60%, a lot of readers have been asking how to invest smarter instead of leaving everything in “safe but stagnant” cash.

A common question: How should an investor who’s willing to take some risk—but doesn’t want to actively babysit their portfolio—invest for returns to achieve their financial goals?

From parking to progressing?

For the past couple of years, holding cash and T-Bills made a lot of sense as yields were attractive, and there was plenty of uncertainty about inflation, rates and geopolitics.

However, cash and T-bills have limitations:

- No long-term growth – they protect capital, but they don’t compound like equities over a 5 – 10 year horizon;

- Reinvestment risk – when interest rates fall, you face lower yields while markets may have already moved.

For those who don’t know, DBS regularly publishes their Chief Investment Office (CIO) insights, and this is available for free on the DBS website or via the DBS digibank app.

The CIO view today is that we’re past peak rates, with a slower but still positive growth backdrop.

That’s usually when it makes sense to gradually shift from “parking” in cash to “progressing” with a diversified portfolio.

Why is a diversified portfolio important? Time in the market vs Timing the market?

In a world like today, diversification has become a key risk management tool for every investor.

You want your money spread across different asset classes (stocks, bonds, REITs, maybe a bit of alternatives) and different regions (US, Europe, Asia), so any single event, country or sector doesn’t torpedo your entire net worth.

At the same time, unless you’re actively trying to time macro and central banks, it’s very hard to justify sitting out of markets completely.

As Warren Buffett has been famously attributed to saying, time in the market beats timing the market.

So for most investors, the answer probably isn’t “all-in stocks” or “all-in T-Bills”.

It’s some equity exposure, sized to your risk appetite, and balanced with bonds and cash:

- Own stocks for higher long-term return potential – accepting higher volatility.

- Hold bonds and high-quality income products to dampen drawdowns and provide stability.

- Keep 6–12 months of expenses in cash/T-Bills so you’re never a forced seller during a downturn.

- Phase your entry (say, 3–6 tranches or monthly DCA) to reduce the risk of going in right before a correction.

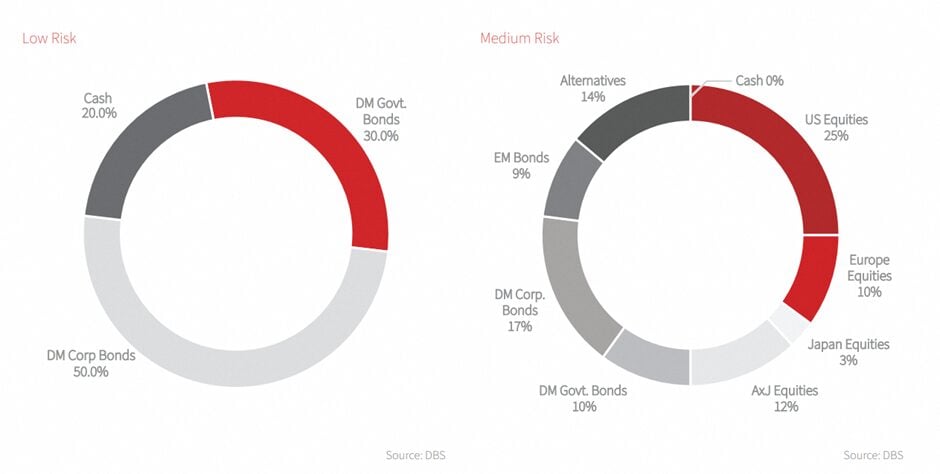

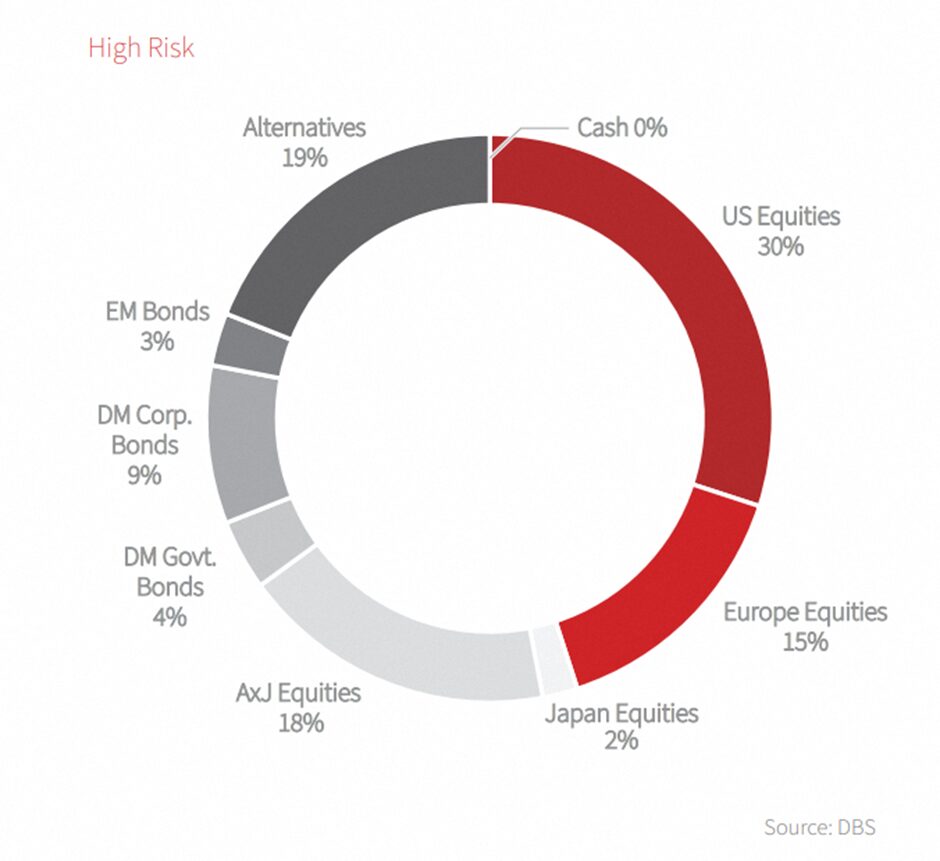

DBS CIO Insights asset allocations for low medium and high risk are set out below – and this gives you an idea of what it means by diversification across asset classes and geographies.

What is DBS CIO Insights Funds?

DBS developed CIO Insights Funds to give investors an easy and effective way to build a diversified portfolio using a curated list of high-conviction investment ideas, without having to stock pick and monitor/compare funds themselves.

CIO Insights Funds brings together both single funds and expertly managed ready-made portfolios in one place.

Everything on the list is handpicked and curated by DBS’s investment team.

Investors can then mix and match depending on whether they want core exposure, income, ETFs or more thematic ideas.

This means an investor can:

- Use the portfolios as a core foundation; and

- Add selected funds/ETFs from the CIO list on top, to tilt towards income, a specific region (like Asia or US), or a theme (like gold).

Curated for you – so you don’t have to stock-pick and compare funds

Instead of researching hundreds of funds, CIO Insights Funds gives you a shortlist that’s:

- Curated by DBS CIO as high-conviction ideas investors can use to build their portfolios;

- Categorized into Core, Income, and Thematic building blocks;

- Reviewed and refreshed over time (vs a static / fixed fund list);

So you’re not buying random funds, you’re plugging into a CIO-driven asset allocation framework.

In short: CIO Insights = the thinking and market roadmap, while CIO Insights Funds are the implementation tools that put that roadmap into practice.

All of which are fully accessible in digiWealth, within DBS digibank:

Disclosures: This post is sponsored by DBS. All views and opinions expressed in this post are from Financial Horse.

How can a long-term investor use CIO Insights Funds?

DBS CIO Insights Funds are designed as building blocks for a diversified portfolio.

For a long-term investor, they are grouped into three practical roles:

- Core holdings for broad market exposure;

- Income funds for stability and cashflow; and

- Thematic ideas for targeted opportunities.

Let’s unpack each step further.

1. Use core funds as the backbone

Investors can start by anchoring your portfolio with a core layer of diversified funds such as:

- Global & Asia portfolios – give broad exposure to US, Europe and Asia in one line item, via low-cost ETFs.

- Retirement portfolios – automatically blend equities and bonds and adjust risk over time through a glide path strategy (i.e., gradually reducing equity exposure and increasing bond exposure over time to reduce risk).

Using core funds as the backbone of your portfolio can help investors:

- Capture long-term global growth

- Reduce single-country or single-stock risk

- Keep you invested through cycles with one or two “core” positions

For a typical diversified investor, this might reasonably be 40–70% of risk assets (exact weight depending on risk profile and horizon).

Some examples of specific funds/portfolios include:

- Global Portfolio Plus / Global Portfolio/ Retirement Portfolio – ETF or UT-based portfolios diversified across US, Europe and Asia, with equity–bond mixes matched to risk level or life stage.

- AB Low Volatility Equity – global low-volatility equities to dampen swings.

- CIO Liquid+ Fund – short-duration bond fund aiming to beat money-market returns (useful as a “cash-plus” core holding).

- First Eagle Amundi Income Builder, Schroder Asia More+ – multi-asset or Asia-tilted funds that mix bonds and equities.

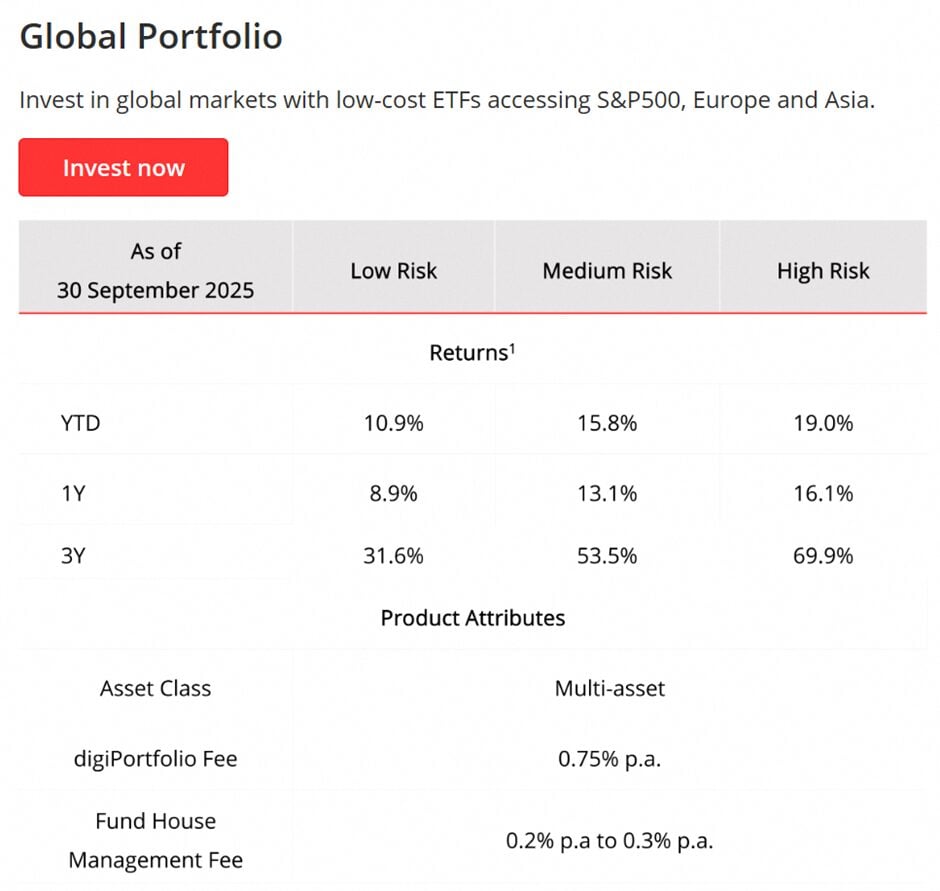

DBS Global Portfolio

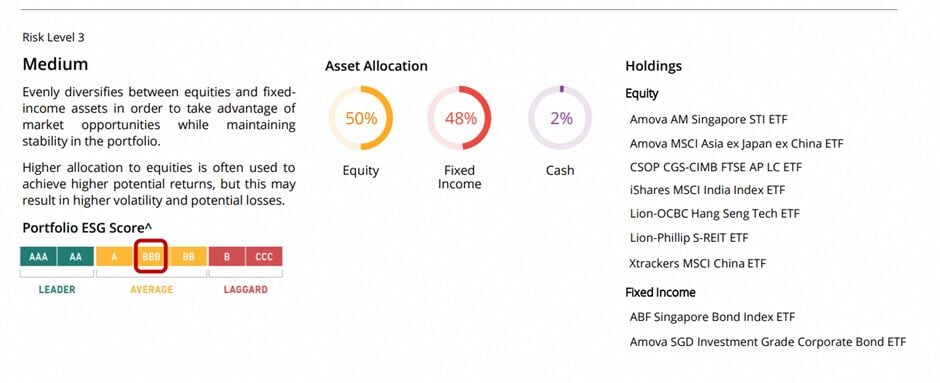

The DBS Global Portfolio allows you to access global markets like S&P500 and Asia with low-cost equity and bond ETFs, from as little as US$1,000.

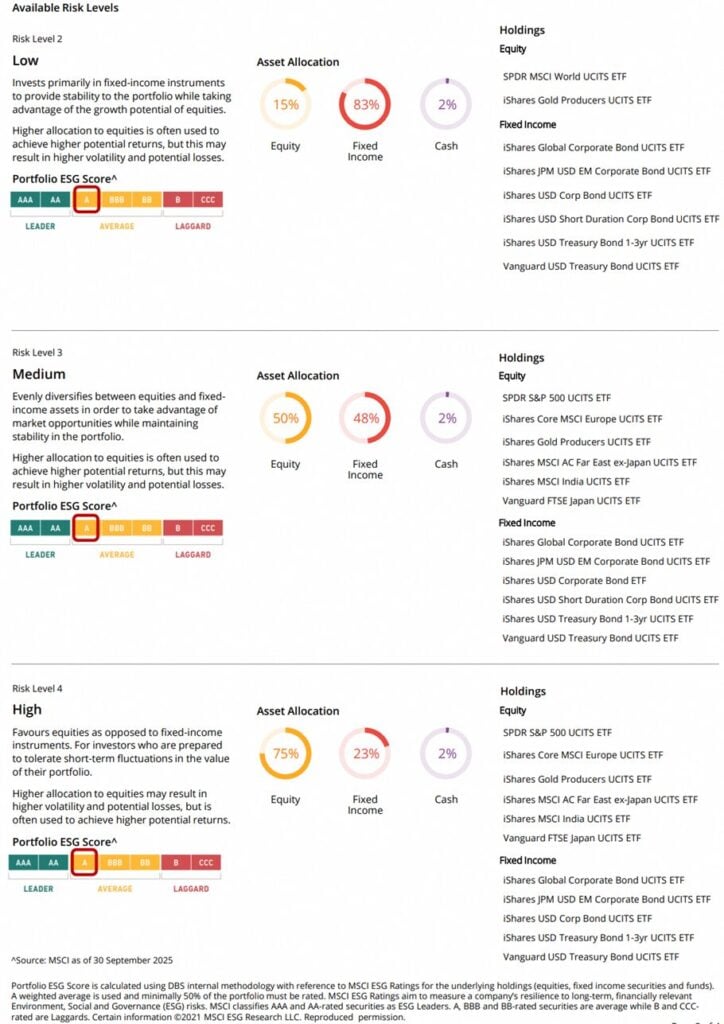

You can choose the portfolio that matches your risk appetite – low risk, medium, risk and high risk.

Low risk portfolio has a 15% tilt to equity, 83% fixed income and 2% cash.

Medium risk portfolio has a 50% allocation to equity, 48% fixed income and 2% cash.

High risk portfolio has a 75% allocation to equity, 23% fixed income and 2% cash.

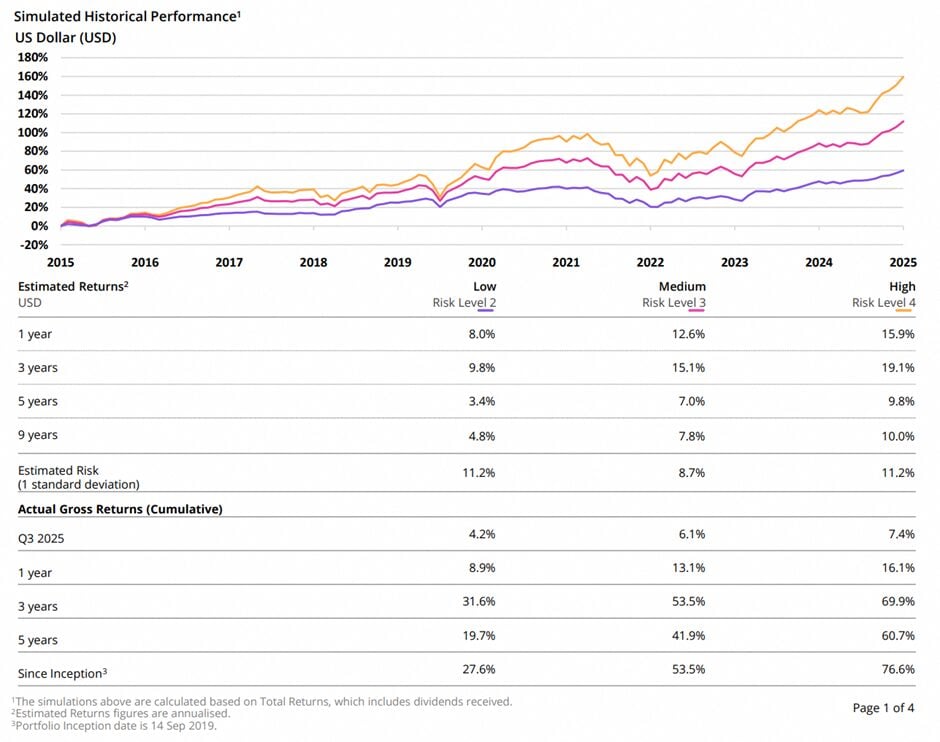

As of 30 September 2025, DBS reports for the Global Portfolio (medium risk) a 1-year cumulative total return of 13.1% in USD and a 3-year cumulative total return of 53.5% in USD, gross of fees.

The key advantage is it’s a convenient, globally diversified ETF portfolio in USD with automated rebalancing and a solid track record so far.

Your money is spread across major markets (US, Europe, Asia, etc.), so you’re not betting everything on Singapore or any single country/sector.

Plus, it uses low-cost ETFs.

The DBS team decides how much goes into equities vs bonds and rebalances for you – so you don’t need to monitor markets or tweak allocations yourself.

The minimum investment for the Global Portfolio is around US$1,000, making diversification accessible even for younger or smaller-ticket investors.

You also have daily liquidity with no lock-in. You can invest or redeem via digibank whenever needed.

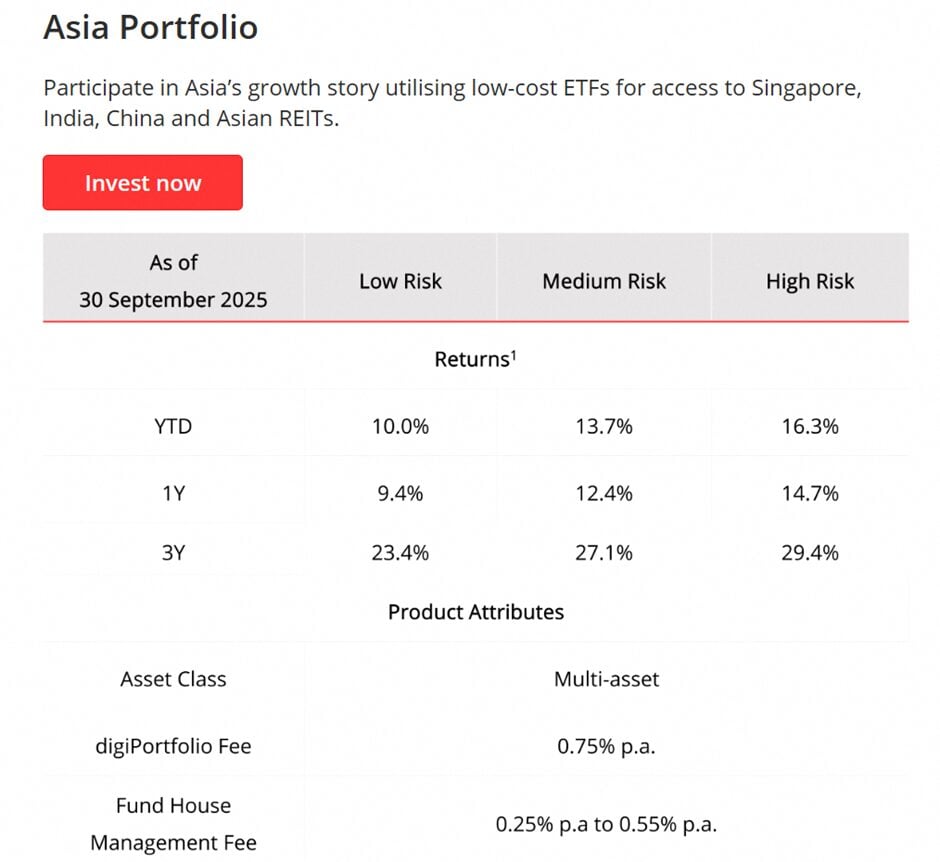

DBS Asia Portfolio: exposure to Singapore, India, China and Asian REITs

Or if you’re bullish on Asia and want to invest specifically in Asia.

The DBS Asia portfolio offers exposure to Singapore, India, China and regional Asia ex-Japan, plus some Asian REITs / fixed income via low-cost ETFs to reduce volatility.

You can again choose from 3 different risk levels.

The medium risk portfolio is a 50-50 split between equities and bonds.

Returns are pretty decent. As of 30 September 2025, DBS reports for the Asia Portfolio (medium risk) a 1-year cumulative total return of 12.4%, in SGD and gross of fees.

Your money is spread across Asian equities and bonds, so you get exposure to faster-growing economies like China, India and ASEAN, while bonds help to smooth out volatility.

You get to invest across multiple Asian countries, sectors and asset classes (equities and bonds), so you’re not all-in on any single market.

Instead of buying multiple Asia funds/ETFs yourself, and having to stock-pick or monitor markets daily, you can use this as a single, packaged way to get Asian exposure.

And like the other portfolios above, you can enter or exit via DBS with no lock-in, from as low as S$1,000.

2. Add Income funds for stability and payouts

Next, layer in CIO Insights income funds.

Bond and dividend-focused funds designed to pay regular distributions, will help provide a smoother ride during equity volatility.

They can also fund regular withdrawals without having to sell growth assets in a downturn.

They are positioned to benefit from today’s still-elevated yields, with potential price upside if rates drift lower over the next few years.

For a diversified investor, income funds might be 20–50% of the portfolio, depending on how important steady cashflow vs growth is.

Examples in the CIO Income sleeve:

- BGF Asian Tiger Bond – Asian investment-grade bonds

- Fidelity Global Dividend – global dividend equity fund

- PIMCO GIS Income – global multi-sector bond fund focused on delivering stable income

- Income Portfolio – mixed equity–bond fund designed to pay out regular income

How a long-term investor can use income funds:

Accumulation phase (still working)

- Allocate, for example, 20% of the portfolio to income funds.

- Set payouts to reinvest, so distributions buy more units and compound over time.

Pre-retirement / retirement

- Gradually shift more from Core into Income.

- Switch to cash payouts to help fund living expenses.

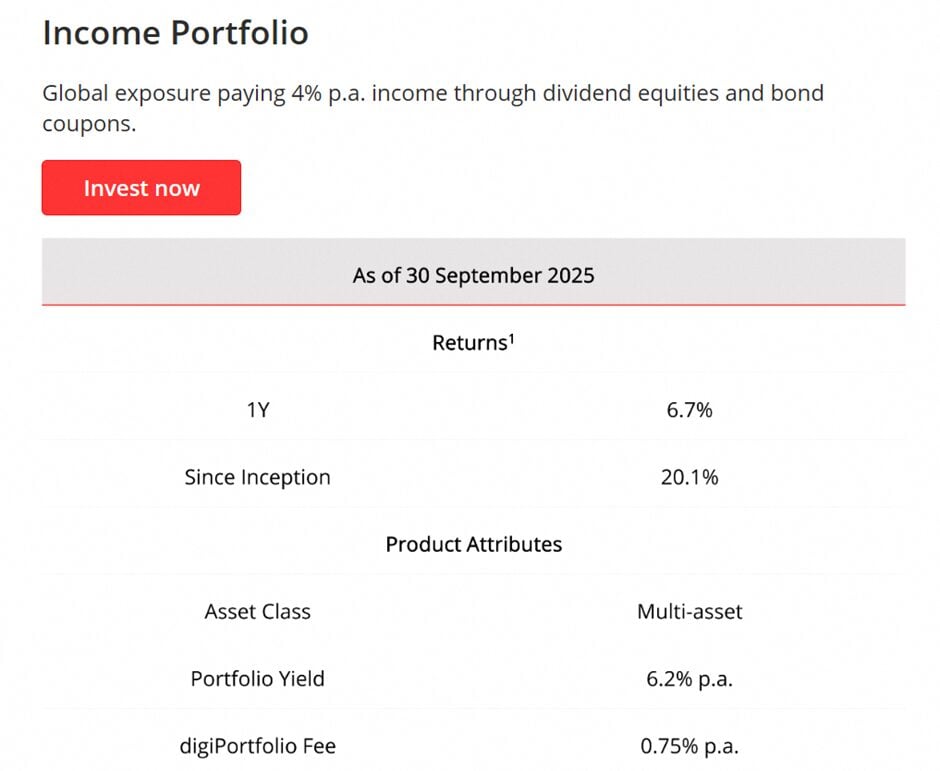

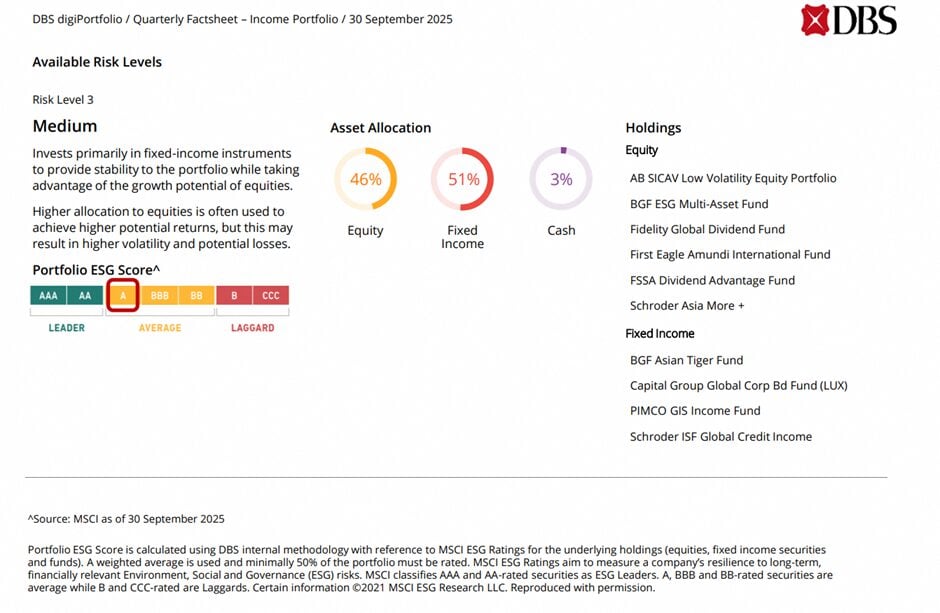

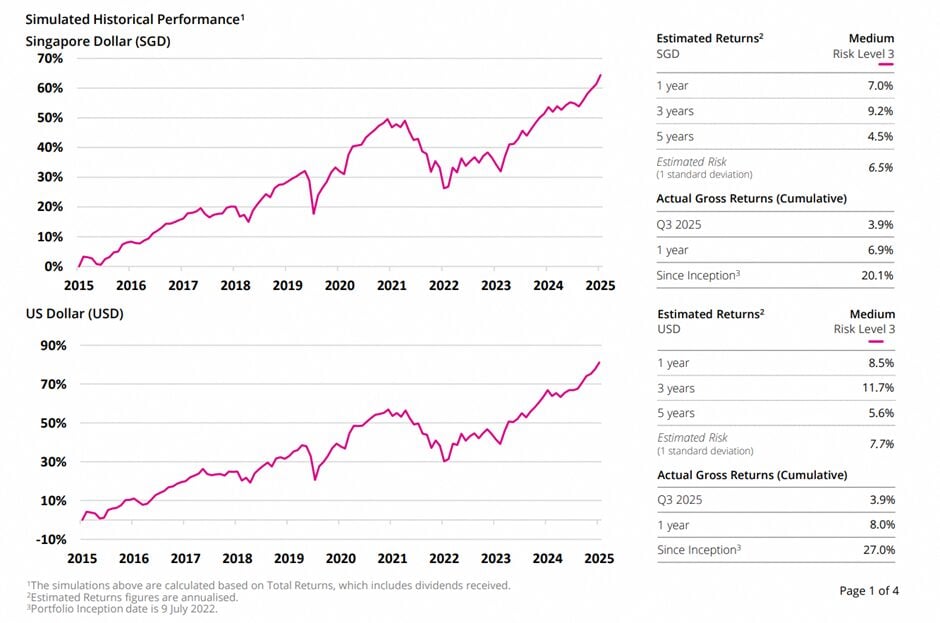

DBS Income Portfolio: 4% target payout with 50-50 bond equity mix

DBS Income Portfolio targets a 4.0% annual dividend payout (paid quarterly).

You can invest from as little as S$100.

Asset allocation is about an even split between fixed income and equities (rebalancing is done automatically so no need for investors to manage this yourself).

As of 30 September 2025, DBS reports that the Income Portfolio has delivered a 1-year cumulative return of 6.9%.

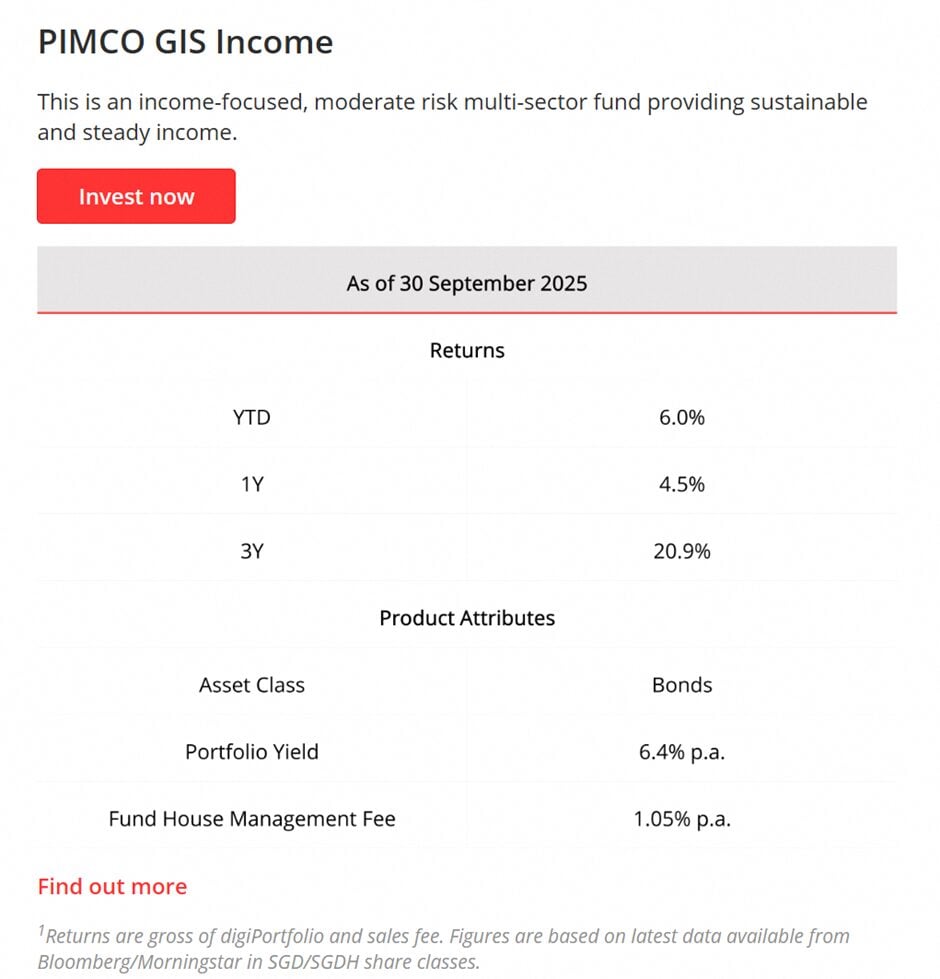

PIMCO GIS Income: global multi-sector bond fund

PIMCO GIS Income fund is another good option within DBS CIO Income sleeve.

The fund’s primary objective is high current income, with capital appreciation as a secondary goal.

You get broad, flexible global bond exposure across sectors and ratings, actively managed by a top-tier fixed income house. PIMCO is one of the world’s largest bond managers.

It references the Bloomberg US Aggregate for comparison but is not constrained to track it, allowing the managers to hunt for yield wherever risk-reward is attractive.

For income-focused investors, you get monthly distributions, with historically competitive yields.

It has shown a track record of resilience across rate cycles, with 10+ years of history and risk that’s generally below equities.

It’s also available in SGD-hedged distributing share classes, making it easy for Singapore investors to tap global bond markets without taking on full USD currency risk.

3. Use thematic funds for growth opportunities

Finally, CIO Insights thematic funds let you express targeted views – technology, AI, healthcare, or gold and commodities.

A long-term investor can:

- Tilt your portfolio towards structural trends that the DBS CIO favours

- Add a diversifier like gold, which has historically helped in drawdowns and policy shocks

Because themes are more volatile and cyclical, DBS CIO explicitly frame them as satellites, not the main course – typically 0–15% of the portfolio, sized to be meaningful but not portfolio-breaking.

Examples:

- Ninety One Global Gold – invests into gold miners

- Capital American Balanced – US-focused balanced fund

How a long-term investor can use thematic funds:

- Cap total thematic exposure at ~5–15% of your portfolio.

- Tilt modestly toward themes you understand and can hold through volatility

- Express a CIO house view (e.g. gold as diversifier, tech as long-term growth)

Putting it together – How CIO Insights Funds can benefit long-term investors

In previous years, parking funds in cash and T-Bills when rates were high and markets were choppy made sense.

This risk now is staying there too long and missing the next leg of growth as rates trend lower.

So for a long-term investor who have thought this through and decided that you do want to take on some risk for higher returns – but you don’t want to spend your nights comparing funds and stock-picking – this is where the DBS CIO Insights Funds can help.

Put simply: if you believe in diversification + time in the market, but don’t want portfolio management to become a second job, the DBS CIO Insights Funds can be a useful solution.

For a broadly diversified, medium-risk investor, a simple CIO Insights portfolio could look like:

- Core CIO funds (Global + Asia, retirement portfolios): ~50–60%

- Income CIO funds (bonds + dividend strategies): ~25–35%

- Thematic CIO funds (tech / AI / gold, etc.): ~5–15%

Investors can then rebalance annually or when DBS CIO house views shift, by adjusting weights rather than timing the markets.

DBS CIO Insights Funds emphasizes long-term participation in the markets and diversification rather than timing every correction.

Access CIO Insights Funds via digiWealth + boost DBS Multiplier interest tier

All of the DBS CIO Insights Funds can be invested via digiWealth, within DBS digibank, which makes the process easy and efficient.

Also, you can earn more on your savings with the DBS Multiplier Account as CIO Insights Funds contribute towards the ‘investments’ category.

DBS Multiplier rates are one of the highest in the market for the first S$50k without any minimum spend.

The current effective rates on the first S$50K are about 1.8%–2.2% p.a., and up to 2.1%–4.1% p.a. on the first S$100K, depending on how many categories you qualify for.

| Grow Your Wealth with Us Alternatively, learn more about CIO Insights Funds here. |

Disclosures:

This post is sponsored by DBS. All views and opinions expressed in this post are from Financial Horse.

Terms and conditions apply to all promotions stated herein. Please review the provider’s latest official T&Cs before applying or transacting.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

The article herein is published by Financial Horse and is for general information only and should not be relied upon as financial advice. This article may not be reproduced, reposted or communicated to any other person without the prior written permission from DBS Bank.

This information does not take into account the specific investment objectives, financial situation or needs of any particular person. Before entering into any transaction involving any product mentioned in this information, where applicable, you should seek advice from a financial adviser regarding its suitability for your own objectives and circumstances. If you choose not to do so, you should make an independent assessment and do your own due diligence on the product.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The information herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.

DBS Bank, its related companies, their directors and/ or employees may have positions or other interests in, and may effect transactions in the product(s) mentioned in this article. DBS Bank may have alliances or other contractual agreements with the provider(s) of the product(s) to market or sell its product(s). Where DBS Bank’s related company is the product provider, such related company may be receiving fees from investors. In addition, DBS Bank, its related companies, their directors and/ or employees may also perform or seek to perform broking, investment banking and other banking or financial services for these product providers.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment.

Any past performance, prediction, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment.

Hi FH,

https://sgwealthbuilder.com/2025/12/13/gold-price-in-super-bullish-form/

So far, all my gold investments were made with UOB Bank. These included physical gold and gold savings account. When buying physical gold from UOB Bank, it is important to note that you must ensure that the physical gold is in its original sealed condition and the original UOB invoice must be presented. In addition, with effect from 30 November 2023, customers must be a UOB account holder in order to purchase physical gold from UOB.

My approach towards gold investment is that of a pragmatic one – buy low and sell high. Given the current bullish gold price, I feel that the risk is high to enter now. Then again, trying to forecast the trend of gold price is becoming more and more challenging nowadays. Previously, I had made the bold call of gold price hitting US$3000 per troy ounce in 2023. That obviously did not happen despite the Ukraine-Russia and Israel-Hamas conflicts in 2023. Gold price managed to clear the US$3,000 threshold only in March 2025. Since then, nothing seems to hold back gold price as the yellow metal raced past the record US$4,245 in October 2025.

https://sgwealthbuilder.com/2025/12/13/gold-price-in-super-bullish-form/

Regards,

Gerald

https://sgwealthbuilder.com

Makes sense – appreciate very much the share!

Hi FH,

I know this is a sponsored post. But I wanted your views on the pros and cons of using a solution like DBS’s, or doing it yourself in IBKR with a three fund portfolio (i.e. VWRA/STI ETF/AGGG) and rebalancing it yourself every year.

Thanks!

I think it depends on what you’re going for. If you want something that is just fire and forget, the DBS option is worth checking out as its pretty much all managed for you. If you’re prepared to spend time to research, analyse, rebalance, and continually improve, then DIY could make sense. But don’t underestimate the time and effort with the DIY option though (not to mention returns may not even outperform).

No right or wrong here, it depends on what you’re looking for.