In my recent article on how to invest $1 million at a 6% portfolio yield.

I proposed the following asset split:

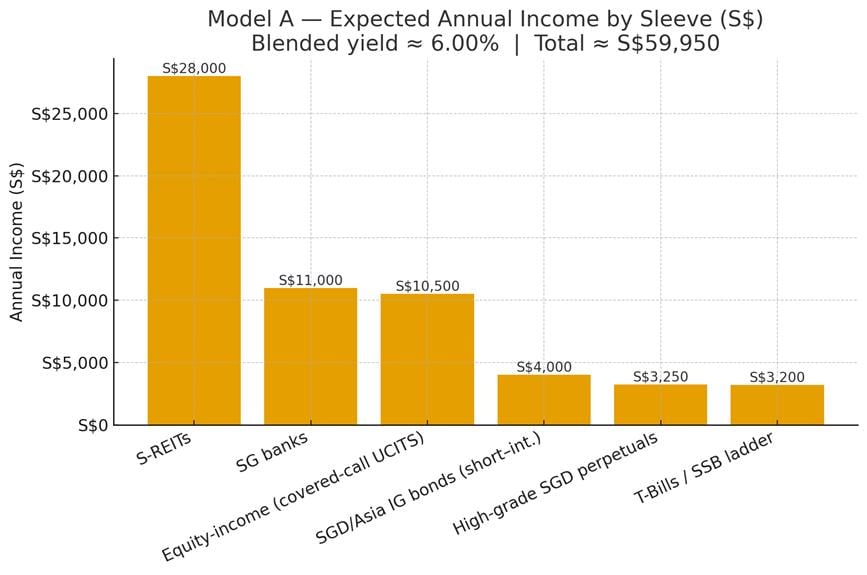

| Sleeve | Weight | SGD | Assumed Yield | Notes |

| Diversified S-REIT basket | 40% | 400,000 | 7.0% | Mix of large-cap industrial/logistics/data-centre/retail REITs or an SG/Asia REIT ETF |

| SG banks (DBS/UOB/OCBC) | 20% | 200,000 | 5.5% | Equal-weight; dividend + special/capital-return optionality |

| Equity-income (covered-call UCITS) | 15% | 150,000 | 7.0% | Irish-domiciled global equity premium income strategies; lower vol than equity beta |

| SGD/Asia IG bond ETF/fund (short–duration) | 10% | 100,000 | 4.0% | Corporate IG bias; short duration to limit rate risk |

| T-Bills / SSB ladder | 10% | 100,000 | 3.2% | 6-mo T-Bills rolled; SSB rung ladder for flexibility |

| High-grade SGD perpetuals | 5% | 50,000 | 6.5% | Select bank/Temasek-linked issues; size deliberately small |

| Total | 100% | 1,000,000 | ≈6.0% | Blended yield ≈ 5.995% on assumptions |

This led to a lot of great input from readers on how exactly to invest the S-REITs portion, and asking for a Part II to elaborate.

So that’s exactly what I wanted to discuss today.

How I will invest $1 million in REITs at 5.5% dividend yield – $4500 passive income a month?

I like to start big picture by throwing the question to a friendly neighbourhood LLM.

I find LLMs these days get you 80% of the answer, and then you layer on the final 20% of the more nuanced analysis yourself.

This was the answer given to me:

- Allocate S$1M across 7 core, 3 satellite S-REITs with a 5% cash reserve; target a mid-5% portfolio cash yield with low–moderate risk.

- Phase entries over 8–12 weeks in 4 tranches using limit ladders; cap office/DC/China exposures and rebalance annually.

- Focus on large, liquid names with prudent gearing, high fixed-rate debt, and stable WALE; reinvest distributions until goal yield is met.

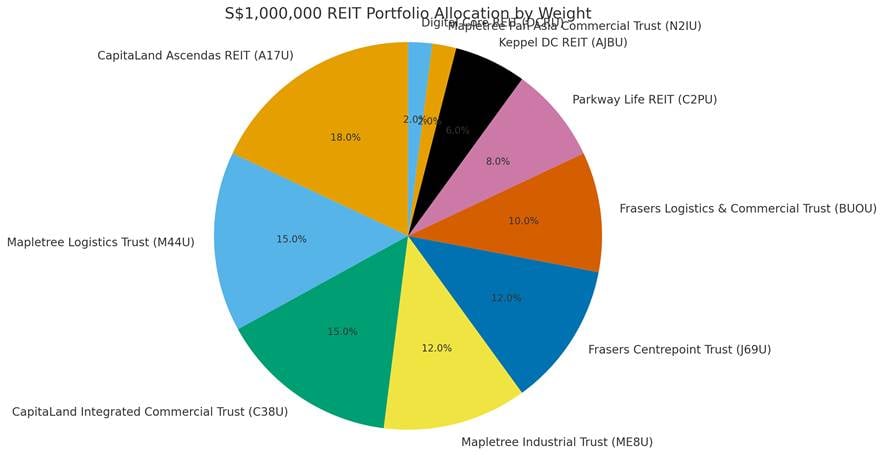

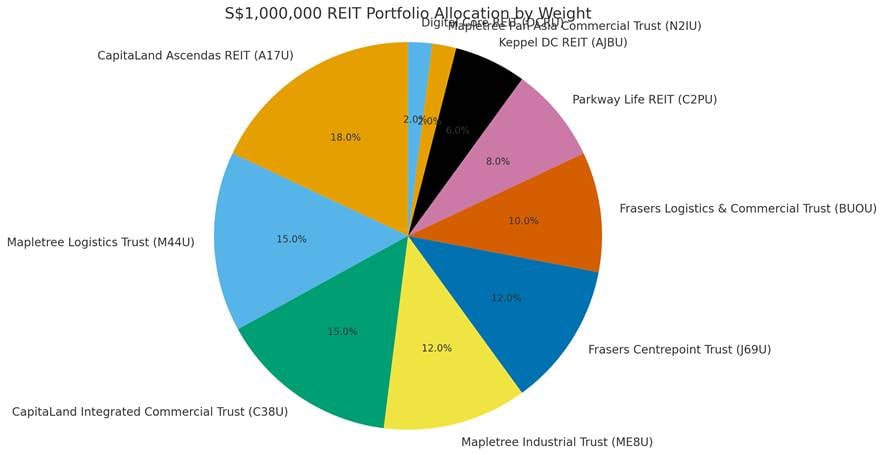

LLM suggested REIT portfolio (low–moderate risk, S$1,000,000)

And the suggested REIT portfolio?

| Bucket | REIT (SGX) | Asset Type / Footprint | Weight |

| Core (80%) | Ascendas REIT | Industrial/Business Parks & DCs, SG & developed markets | 18% |

| CapitaLand Integrated Commercial Trust – CICT | SG retail + office (integrated commercial) | 15% | |

| Mapletree Logistics Trust – MLT | Asia logistics (SG, JP, CN, etc.) | 15% | |

| Frasers Centrepoint Trust – FCT | SG suburban malls | 12% | |

| Mapletree Industrial Trust – MIT | Hi-tech/industrial + US DC JV | 10% | |

| Parkway Life REIT – PLife | Healthcare (SG, JP nursing homes) | 5% | |

| Frasers Logistics & Commercial – FLCT | AU/EU logistics + light commercial | 5% | |

| Satellite (15%) | Keppel DC REIT | Data centres (global) | 7% |

| Mapletree Pan Asia Commercial Trust – MPACT | VivoCity + SG/HK commercial | 5% | |

| (Optional) Digital Core REIT (DCRU) or add to A-REIT/MLT | US DC (higher beta) | 3% | |

| Cash/Opportunistic (5%) | SGD cash/T-Bills | — | 5% |

Notes: Expect a mid-5% cash yield for this mix at typical entry levels; exact yield depends on live prices/FX. Keep any single issuer ≤20%, office ≤12%, data-centre ≤12%, China exposure ≤10% of portfolio.

Reasoning (how this was REIT portfolio built)

Stability first: Overweight large, liquid, diversified S-REITs with strong sponsors (CapitaLand/Mapletree/Frasers/Keppel). These exhibit better access to funding and lower operational volatility.

Rate exposure managed: Mix of industrial/logistics (A-REIT, MIT, MLT, FLCT) + suburban retail (FCT) + healthcare (PLife) dampens rate/tenant shocks versus office-heavy portfolios.

Yield vs. defensiveness: CICT/FCT/A-REIT/MLT/MIT anchor the yield; PLife lowers beta; a small DC sleeve (KDC, optional DCRU) adds long-term growth with controlled size.

Concentration guardrails: Office/DC/China caps reduce tail risks (vacancy cycles, power/lease repricing, policy).

Cash buffer: Preserves flexibility for rights issues or market dips without forced selling.

Dividend yield of this $1 million REIT portfolio?

Broken down by the dividend yield of each REIT below.

Using the suggested weights gets a blended yield of approximately 5.5% dividend yield.

Which on a $1 million REIT portfolio, works out to about $54,900 dividend income a year.

Or $4,575 a month.

| REIT | Ticker | Weight | Est. Fwd Yield* | Est. Cash/yr (S$) |

| CapitaLand Ascendas REIT (industrial) | A17U | 18% | 5.5% | 9,900 |

| Mapletree Logistics Trust (APAC logistics) | M44U | 15% | 6.5% | 9,750 |

| CapitaLand Integrated Commercial Trust (SG prime retail/office) | C38U | 15% | 4.8% | 7,200 |

| Mapletree Industrial Trust (industrial + DCs) | ME8U | 12% | 5.8% | 6,960 |

| Frasers Centrepoint Trust (suburban retail) | J69U | 12% | 5.4% | 6,480 |

| Frasers Logistics & Commercial Trust | BUOU | 10% | 6.5% | 6,500 |

| Parkway Life REIT (healthcare ballast) | C2PU | 8% | 3.2% | 2,560 |

| Keppel DC REIT (data centres) | AJBU | 6% | 4.9% | 2,940 |

| Mapletree Pan Asia Commercial Trust | N2IU | 2% | 6.6% | 1,320 |

| Digital Core REIT (US DCs, satellite) | DCRU | 2% | 6.5% | 1,300 |

| Portfolio | 100% | ~5.5% | ~54,900 |

You can also see a further breakdown of the gearing ratio, interest coverage ratio (ICR – higher is better), and percentage of fixed debt of each REIT below:

| REIT | Gearing (Agg. Leverage) | ICR (x) | % Debt Fixed/Hedged |

| A-REIT | ~37.4% | 3.7x | ~76% fixed |

| CICT | 37.9% | 3.3x | 81% fixed |

| MLT | ~41% | ~2.9x | 84% fixed/hedged |

| MIT | ~40% | ~4x | ~78% fixed |

| FCT | 42.8% | 3.39x | 76% fixed |

| FLCT | 36.1% | 4.5x | 69.7% fixed |

| PLife | 35.4% | 9.1x | 97% fixed |

| KDC | 30.7% | 5.9x | 76% fixed |

| MPACT | 37.9% | 2.9x | ~78% fixed |

| DCRU | 38.3% | n/a (not disclosed same way) | 85% hedged |

My views on this REIT portfolio? What is the main risk?

As always, LLM gets you 80% of the way there, but you do need to layer on the final 20% of the analysis yourself.

2 big points that jumped out at me.

A lot of overseas exposure to China, US, Australia – FX and Overseas property exposure

The first is that this REIT portfolio actually carries a fair bit of overseas exposure in the form of MLT, MIT, FLT, Parkway Life, Digital Core REIT.

This exposes you to both FX risk, and the uncertainty over how those overseas real estate markets play out.

The benefit though, is that you do get a higher yield to compensate for the higher risk taken on.

But personal view.

If I’m building a REIT portfolio today I would want it primarily to be a bond proxy, and I don’t want exposure to too much risk.

And I’m comfortable with a lower yield because of that.

If I want equity style risk, I would just buy stocks instead – that’s just how I see it.

So if this were me, I probably would take out most of the overseas exposure, and limit it to REITs holding primarily Singapore real estate.

| REIT | Ticker | Weight | Est. Fwd Yield* | Est. Cash/yr (S$) |

| CapitaLand Ascendas REIT (industrial) | A17U | 18% | 5.5% | 9,900 |

| Mapletree Logistics Trust (APAC logistics) | M44U | 15% | 6.5% | 9,750 |

| CapitaLand Integrated Commercial Trust (SG prime retail/office) | C38U | 15% | 4.8% | 7,200 |

| Mapletree Industrial Trust (industrial + DCs) | ME8U | 12% | 5.8% | 6,960 |

| Frasers Centrepoint Trust (suburban retail) | J69U | 12% | 5.4% | 6,480 |

| Frasers Logistics & Commercial Trust | BUOU | 10% | 6.5% | 6,500 |

| Parkway Life REIT (healthcare ballast) | C2PU | 8% | 3.2% | 2,560 |

| Keppel DC REIT (data centres) | AJBU | 6% | 4.9% | 2,940 |

| Mapletree Pan Asia Commercial Trust | N2IU | 2% | 6.6% | 1,320 |

| Digital Core REIT (US DCs, satellite) | DCRU | 2% | 6.5% | 1,300 |

| Portfolio | 100% | ~5.5% | ~54,900 |

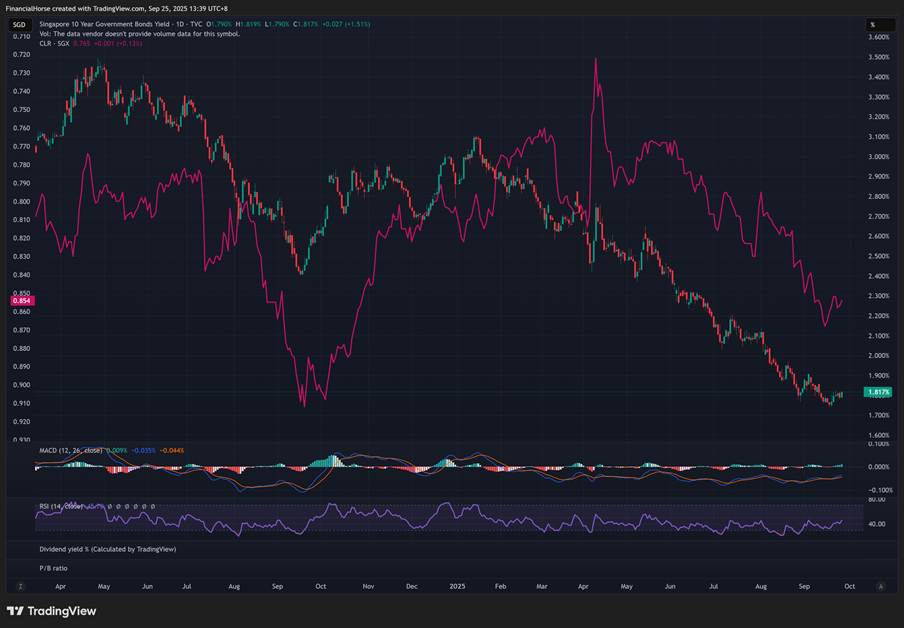

Interest rate increase will be bad news for a pure REIT portfolio

The second point is probably not entirely fair.

But it is that if you drop $1 million into REIT today.

After Singapore 10 year interest rates have plunged from 3.5% to 1.8% in the span of slightly over a year.

Your biggest risk going forward is that if interest rates go back up.

You could see a fair bit of capital losses on the REITs that you hold.

I’ve charted the SG 10 year yield against Lion Phillip S-REIT ETF (inverted) below.

You can see how REIT prices have rallied since April together with the fall in interest rates.

If (when) interest rates pick back up, that could be bad news for a pure REIT portfolio.

But that being said, I do get that this point is not entirely fair because the point of this article is how to invest into REITs today.

If you choose to invest purely in REITs, that’s just the risk you have to be comfortable with.

Follow Financial Horse on Telegram or Facebook to get latest financial insights!

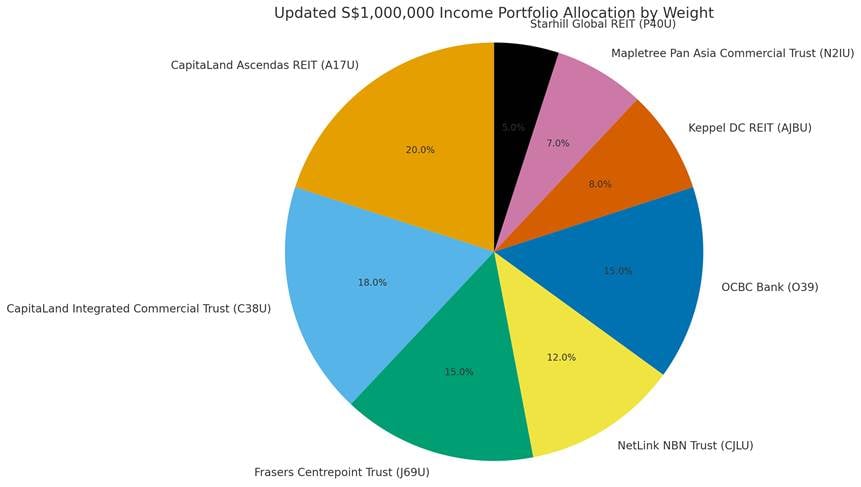

What would I do differently with the REIT portfolio?

But assuming I had my way?

I think what I would do is that I would probably strip out most of the overseas exposure.

And to keep the yield attractive, I would add in some smaller caps like Netlink Trust and Starhill Global REIT.

And I would throw in some bank exposure to provide some diversification / hedge in the event that interest rates go up again.

This is what it might look like:

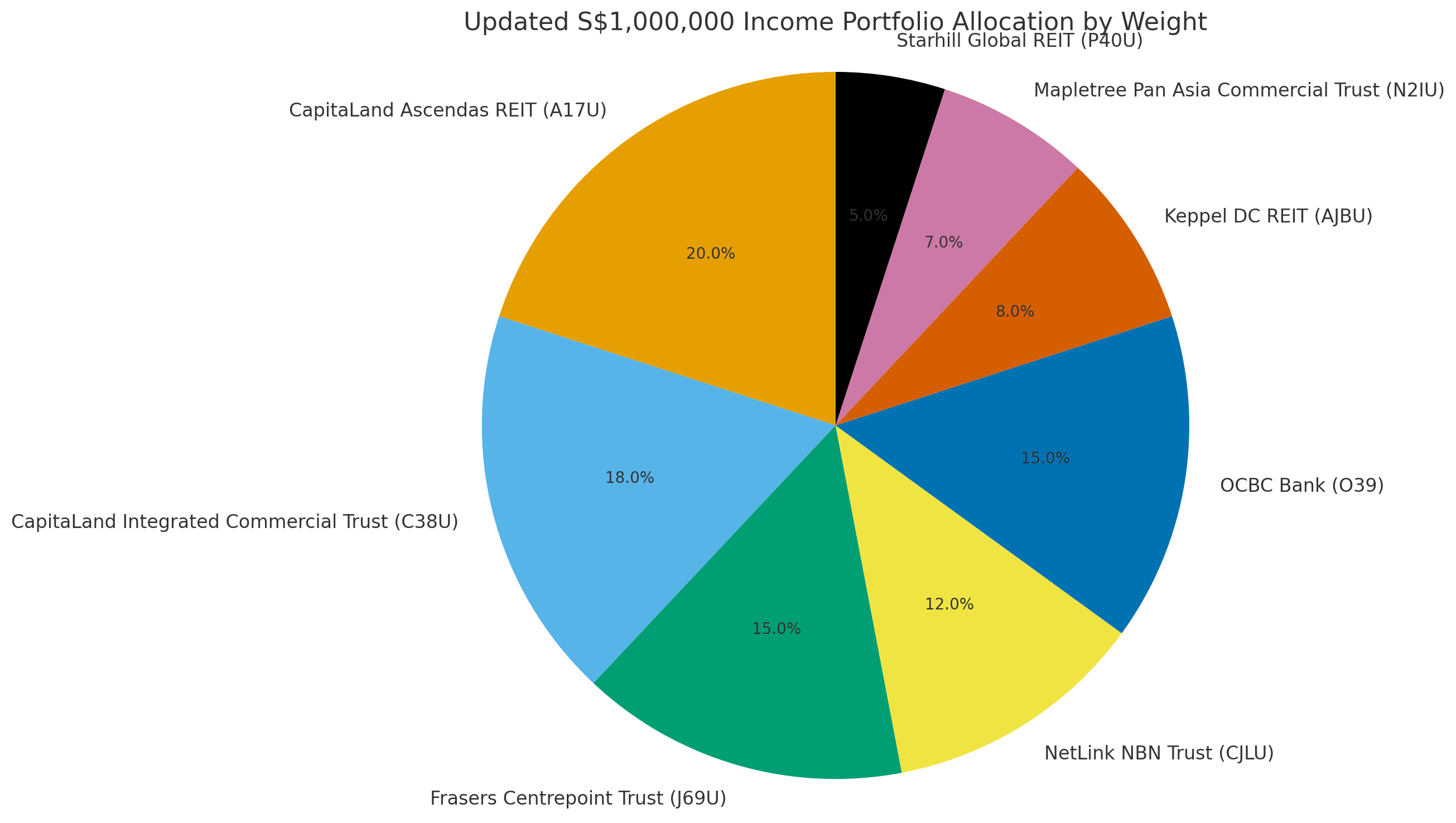

| Name | Weight | Est. Fwd/Current Yield* | Est. Cash / yr (S$) |

| CapitaLand Ascendas REIT | 20% | ~5.4% | 10,800 |

| CapitaLand Integrated Commercial Trust | 18% | ~4.5% | 8,100 |

| Frasers Centrepoint Trust | 15% | ~5.3% | 7,950 |

| NetLink NBN Trust | 12% | ~5.7% | 6,840 |

| OCBC Bank | 15% | ~5.8% | 8,700 |

| Keppel DC REIT | 8% | ~4.5% | 3,600 |

| Mapletree Pan Asia Commercial Trust | 7% | ~6.6% | 4,620 |

| Starhill Global REIT | 5% | ~7.3% | 3,650 |

| Portfolio | 100% | ~5.4% | ~54,260 |

Blended dividend yield stays at about 5.4%.

But the portfolio is now primarily Singapore real estate.

And includes some bank exposure for diversification as well.

Other alternatives to consider to the REIT portfolio

Some further variations to play around with include:

- More defensive: Shift 2–3% from Starhill/MPACT into NetLink or CICT (yield −0.1–0.2ppt; smoother).

- More income: Move 3–5% from OCBC/CICT to Starhill/MPACT (yield +0.2–0.3ppt; higher retail/office cyclicality).

- Diversification: Increase the allocation to OCBC (or UOB / DBS), or add in other dividend stocks

But… these changes don’t fully solve interest rate risk of the REIT / dividend portfolio?

And yes I know some of you will point out that a 15% allocation to OCBC Bank doesn’t fully solve the interest rate risk.

If interest rates go back up to 3.5%, that 15% allocation isn’t going to save you.

I suppose to solve this, you can either increase the bank allocation to 30 – 50% of the portfolio.

Or you can add in other dividend stocks, say names like Singtel or Keppel or Sembcorp for further diversification.

But the latter would bring down the overall yield of the portfolio, so there is a tradeoff.

And even if you do this, it wouldn’t solve capital markets risk.

In the sense that if the stock market as a whole falls, none of this is really going to help you much.

If you really wanted to solve that risk, you probably need to mix in other asset classes like T-Bills, bonds, gold and so on, which goes way beyond the scope of this article (my full portfolio breakdown is shared on FH Premium if you are interested).

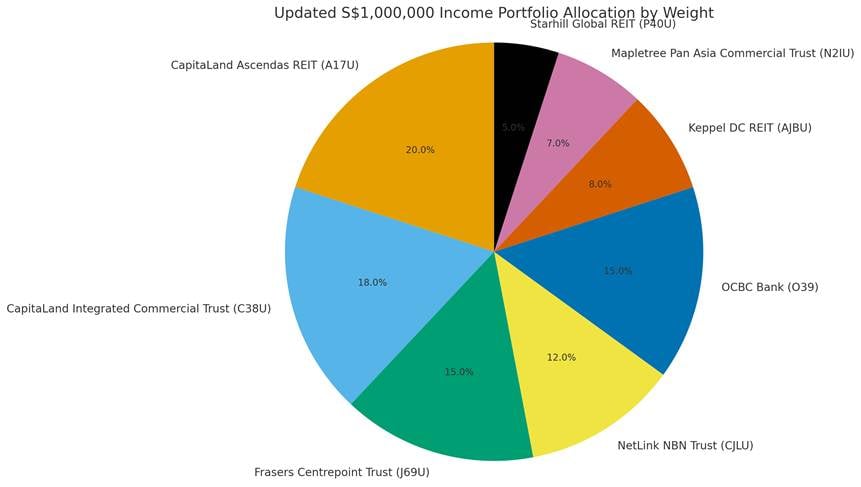

How I will invest $1 million at 5.5% dividend yield – $4500 passive income a month from REITs?

That said, all things considered.

I actually quite like the portfolio below.

| Name | Weight | Est. Fwd/Current Yield* | Est. Cash / yr (S$) |

| CapitaLand Ascendas REIT | 20% | ~5.4% | 10,800 |

| CapitaLand Integrated Commercial Trust | 18% | ~4.5% | 8,100 |

| Frasers Centrepoint Trust | 15% | ~5.3% | 7,950 |

| NetLink NBN Trust | 12% | ~5.7% | 6,840 |

| OCBC Bank | 15% | ~5.8% | 8,700 |

| Keppel DC REIT | 8% | ~4.5% | 3,600 |

| Mapletree Pan Asia Commercial Trust | 7% | ~6.6% | 4,620 |

| Starhill Global REIT | 5% | ~7.3% | 3,650 |

| Portfolio | 100% | ~5.4% | ~54,260 |

With interest rates at cycle lows (and REITs at cycle highs) some averaging in would make sense – buy in tranches, and opportunistically on pullbacks.

Barbell it with some equity exposure, and supplement with some bonds.

And maintain a cash allocation for emergency expenses.

That could form the base for a pretty solid investment portfolio.

Love to hear what you think though!

What would you change with this REIT portfolio?

This article is written on 25 Sep 2025 and will not be updated going forward. My latest personal portfolio, stock watch, and macro views are shared on FH Premium.

Do you think that interest rates are already at cycle lows, given that the US federal reserve has only just begun cutting rates?

Yes – I have considered this possibility too. Definitely possible and I did wonder if the Fed rate cut would be a sell the news event.

With this many reits and this many flagships, why not go for an etf to keep it simple?

Perfectly fine as well!

Maybe one idea for a separate post: Why is capital ascendas reit underperforming for the last few years. Dividend near the same, stock price flat.

One theory is that institutional investors dont like A-REIT so much because industrial properties are viewed as riskier, and have shorter remaining lease tenures. That said it did do well the past week though!

True, but besides the share price the dividend pershare hasn’t moved much over the last few years.