Okay so quite a few of you have asked me for an “urgent” piece on Keppel REIT’s MBFC acquisition, the preferential offering, and my thoughts in general on Keppel REIT after Friday’s 6.8% drop.

So here goes.

Keppel REIT buys 33% of MBFC Tower 3 – Price immediately drops 6.8%

Let’s start with the price action.

Keppel REIT announced that they are buying 33% of MBFC Tower 3, and funding that via equity fund raise (preferential offering).

And on the day the news was released – the share price immediately plunged 6.8%.

From 1.03, to 0.96:

DPU Impact – 6.4% drop in DPU?

Let’s address the elephant in the room.

After the acquisition and after the dilutive preferential offering.

You’re looking at a 6.4% drop in DPU.

It seems that many investors are expressing reservations about this.

MBFC is a strong asset, but the funding approach means unitholders may need to commit additional capital, while the headline projection is for a lower DPU post-acquisition.

Of course, that reported ~6.4% DPU decline depends on assumptions (including interest rates and financing costs) and may change over time.

Still, at a high level, I can see why the market views the optics as less favourable.

This is an FH Premium article I am releasing for all readers. If you enjoy articles like this, do support Financial Horse on FH premium and get access to premium articles like this, including my stock watch.

Why is the acquisition so dilutive?

I suppose in a nutshell, because Keppel REIT is buying “expensive”, and funding that all via the issuance of equity below NAV.

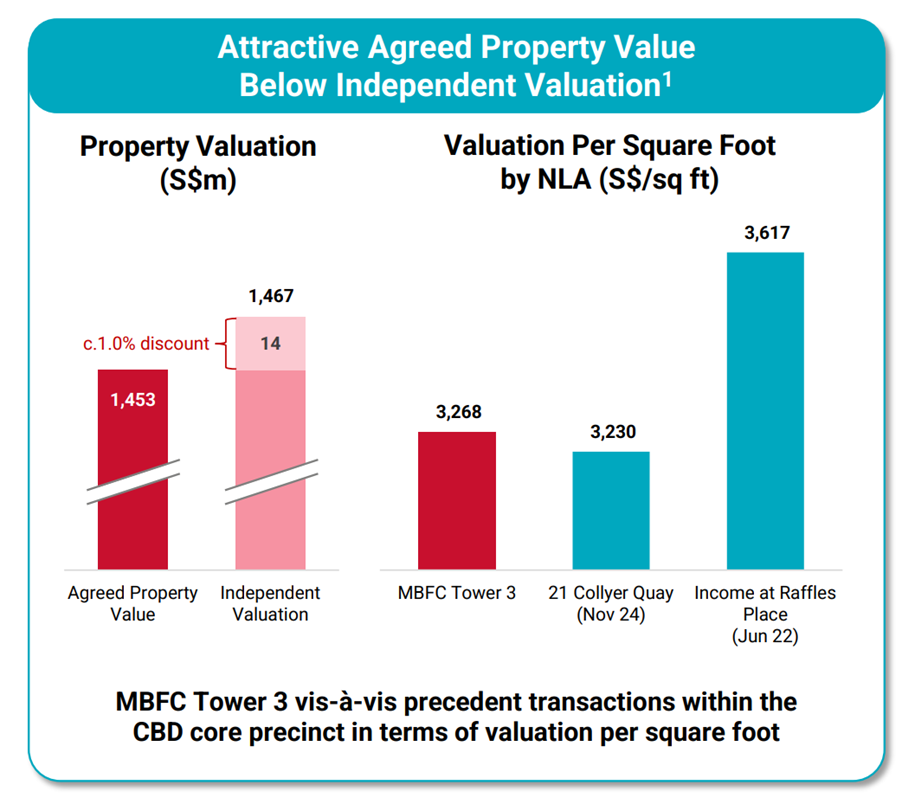

Acquisition price of MBFC Tower 3

Acquisition price is a 1% discount to independent valuation.

It’s slightly higher than 21 Collyer Quay transacted in Nov 2024 (when interest rates were way higher).

But much cheaper than Income at Raffles Place transacted in June 2022 (when interest rates were way lower).

So if you triangulate this way I suppose the valuation is “fair value”.

After all Hong Kong Land (the seller) is also in the same industry and not an idiot, if you low-ball them they’re not going to accept.

And Grade A office space in Singapore today, well it’s just expensive.

It’s more of a store of value than an income asset, and trades at about 3 – 3.5% cap rate today.

In plain English – MBFC is an expensive buy, and the rental income as a percentage of the purchase price, it’s just not that high.

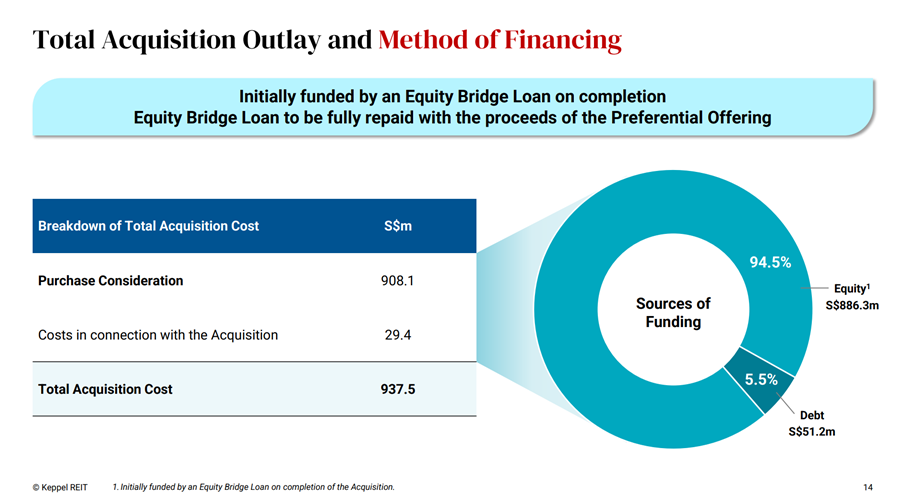

How will the acquisition be financed?

At the same time, Keppel REIT is funding the acquisition via:

- 94.5% Equity (preferential offering)

- 5.5% Debt

That 94.5% equity – works out to $908 million.

Close to a billion SGD, which is a really big sum even in today’s market.

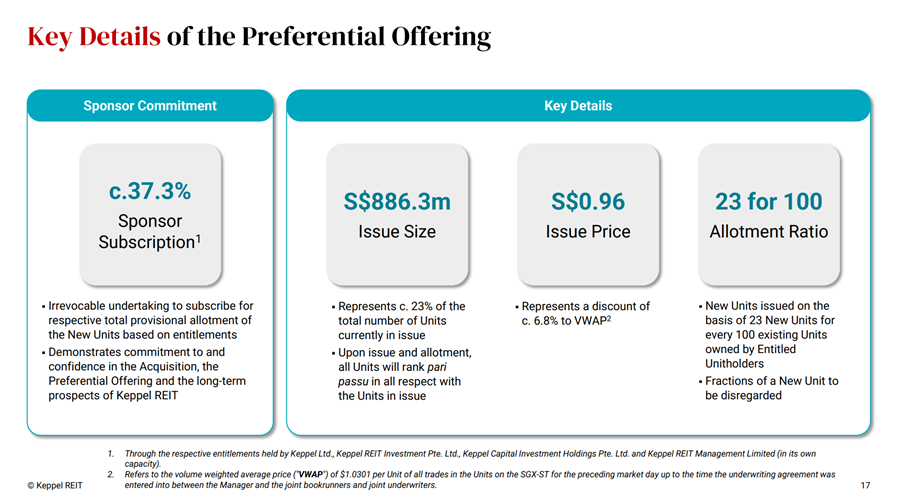

For every 100 units, you will be offered 23 units.

Crunching the numbers, that means for every $9600 you hold based on the latest price, you need to cough up $2208 if you want to participate.

That’s a big capital call from shareholders.

And this is a non-renounceable preferential offering, so if you don’t participate, you cannot sell your rights.

Fundraise is at a discount to NAV

And… the preferential offering is at a huge discount to NAV.

NAV is 1.27, and the units are being issued at 0.96.

You can see how this leads to a fairly large drop in the NAV after the acquisition.

Not great.

Long story short – Keppel REIT is acquiring the asset at a relatively low yield, and is funding part of the purchase by issuing units at a discount to NAV.

As a result, based on the stated terms and assumptions, the transaction is expected to be dilutive to both DPU and NAV for existing unitholders.

Against that backdrop, it’s understandable that some unitholders have mixed views on the deal.

Keppel REIT buys 33% of MBFC Tower 3

Okay let’s take a step back and look at the deal holistically, and see if there’s anything to like about this deal.

Right of First Refusal from Hong Kong Land

The reason why Keppel REIT has to buy now, is effectively because Hong Kong Land wants to sell.

There is a right of first refusal, which means that before Hong Kong Land can sell to a third party they have to first offer it to Keppel REIT.

Which Hong Kong Land did, and Keppel REIT decided to buy.

Rationale of the Acquisition

Here’s the corporate take on the “rationale” of the acquisition.

Let’s go through each.

Rare Opportunity to Increase Ownership in MBFC Tower 3, a Premium Grade A Office Asset.

Grade A office assets in Singapore are prized assets.

If they go onto the market, they are quickly snapped up by other REITs, or large real estate funds.

So even if Keppel REIT chose not to buy, I’m pretty sure someone else would have snapped it up.

And objectively, I do not deny that MBFC Tower 3 is a great asset.

Deepen Keppel REIT’s Presence in Core CBD, Marina Bay Area

True as well – this is pretty much what you want from a Grade A office REIT.

Note that post acquisition, 79% of the REIT’s assets is Singapore real estate.

This is good, I’ve been saying for a while now that with the current macro climate, if I buy a REIT I want it to be predominantly Singapore real estate exposure.

Strong Office Market Fundamentals in Singapore with No Expected New Office Supply in Marina Bay Area

This is fair as well.

Although if you ask me I think the competition isn’t just Marina Bay office space, but office space across Singapore generally.

But I get the point.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Potentially Enhances Keppel REIT’s Market Capitalisation

This one I agree too.

REITs today is a numbers game.

You need to be the biggest to have economies of scale, and to attract investor funds.

So… is this a good deal for Keppel REIT?

At a high level, I can see the strategic rationale for the REIT’s acquisition of MBFC.

However, from a unitholder’s perspective, the funding structure matters.

Given the size of the preferential offering, unitholders who do not subscribe may face dilution, and the transaction is not expected to be DPU-accretive.

So while I understand why they’re doing it, I’m not thrilled about the equity raise and what it means for DPU.

Leverage comes down slightly – but remains high

Post acquisition, leverage does come down slightly, but remains high at 41.9%.

Estimated Distribution yield of Keppel REIT going forward

Crunching the numbers below.

We’re looking at about 5.2 – 5.4% dividend yield for Keppel REIT going forward.

Note that this includes the anniversary distribution, which ends in FY 2026 (being the final year).

If you strip it out, and assume there is no equivalent replacement, then the dividend yield drops to 4.8 – 5.0%

Like I said, this is probably fair value because Singapore Grade A office space is prized so expensively today (kinda like data centres).

But if you’re a yield investor, you do need to factor that in.

| Metric | Estimate (Post-Rights) | Notes |

| Projected DPU (Total) | ~5.05 – 5.20 cents | Reflects 3.6% – 6.4% dilution from FY24/25 base. |

| Unit Price used | S$0.96 | Issue price (Market price has anchored here). |

| Yield (WITH Anniversary Dist) | ~5.2% – 5.4% | Headline yield visible to investors. |

| Yield (WITHOUT Anniversary Dist) | ~4.8% – 5.0% | Underlying operating yield (Net of capital top-up). |

| Anniversary Component | ~0.405 cents | Calculated as S$20m ÷ 4.94b units. |

What will I do? Subscribe for the preferential offering?

The REIT is trading around 0.96.

In many cases, prices can be softer around a preferential offering, and selling during that window may result in a less favourable exit price.

If the unit price remains at or above 0.96 in the coming days, one possible approach is to subscribe at 0.96 and reassess over the following months once the immediate event-related volatility subsides.

After that, you can decide whether to rebalance based on how the position fits within your broader portfolio.

As always, monitor the price action to see how things play out, and decide accordingly.

Is Keppel REIT a good buy?

That said, I’m analysing this as an existing investor.

What about for new investors, or investors looking to invest in Keppel REIT / Grade A office space long term?

Objectively speaking, I do think an opportunity like this to buy 33% of MBFC Tower 3 only comes around once a decade.

And objectively speaking, I do think MBFC Tower 3 can be viewed as *arguably* best in class Grade A office space.

As an asset-accumulating REIT, it’s understandable why Keppel REIT chose to proceed when Hongkong Land presented the opportunity.

That said, funding it through an equity raise is dilutive, and unitholders who don’t participate may see their ownership stake reduced.

Evaluating Keppel REIT objectively at 0.96?

I think Keppel REIT is at best fair value today.

It can make sense if you want the exposure to Grade A office space, and you want the yield (4.8 – 5.0% dividend yield going forward (stripping out the anniversary distribution)).

But it may be a stretch to expect significant capital gains in the near future.

And if interest rates continue to march up, I could see potential downside risk for Keppel REIET.

This is an FH Premium article I am releasing for all readers. If you enjoy articles like this, do support Financial Horse on FH premium and get access to premium articles like this, including my stock watch.

It’s a terrible deal – the share price was trading around 1.07 before this started leaking so a massive drop

To compare against 21 CQ is a stretch, raffles place and 999y leasehold and much smaller bite size nobody was paying this price

Better off buying dpu accretive assets in Australia at step discounts and leveraging the currency and funding arbitrage like their retail aquisition

Well I didn’t want to be too brutal in the public article so I kept the tone more measured. But yeah, as a shareholder I sure was not pleased.

Obviously, no S-Reit unitholders like EFR. In this context, it’s understandable that unitholders of Keppel REIT are boiling over the mega $886.3 million EFR. Imagine having 923 million of new units flooding the market. It will be a miracle if Keppel REIT share price does not dive on 19 January 2026, the day of the listing of the new units. To make matters worse, this mega EFR came right after the $113 million Private Placement in October 2025.

The new units are issued on the basis of 23 new units for every 100 existing units at an issue price of $0.96. Currently, Keppel REIT share price is being traded at $0.97. Following the listing of the new units, there may be a possibility of Keppel REIT share price falling below $0.90 due to short-term negative sentiments.

Generally speaking, investors do not like acquisitions that cause dilution to both unit price and distribution per unit (DPU). Most acquisitions made by S-REITs are DPU accretive. This was the case for Keppel REIT’s Top Ryde City Shopping Centre in Sydney. During the launch of the Private Placement, Keppel REIT stated clearly that that acquisition will be DPU accretive. However, for the latest acquisition, the Manager shared that the pro forma DPU will drop to 4.42 cents from 4.72 cents (excluding anniversary dividend). Net asset value (NAV) will also drop to $1.18 from $1.24.

Fair point. Agree and appreciate very much the sharing Gerald!