Lendlease REIT announced this week that they are buying the remaining 30% of Paya Lebar Quarter that they don’t already own.

And this would be funded via preferential offering.

Now the acquisition and preferential offering itself was announced on 25 February, but since Mid Feb the share price has fallen from 66.5 cents to 57 cents – a whopping 13% decline.

I myself got lucky as I sold most of my Lendlease REIT in the mid 60s when I thought it was fully valued, but I still hold some Lendlease REIT in my SRS account (because it’s just too much trouble to sell SRS stuff).

So this raises interesting questions for me:

- After the 13% decline, is it worth buying back the Lendlease REIT I sold?

- For the Lendlease REIT that I hold in SRS, will I subscribe for the preferential offering?

Lendlease REIT Share price falls 13% in February

This is the part where it gets interesting.

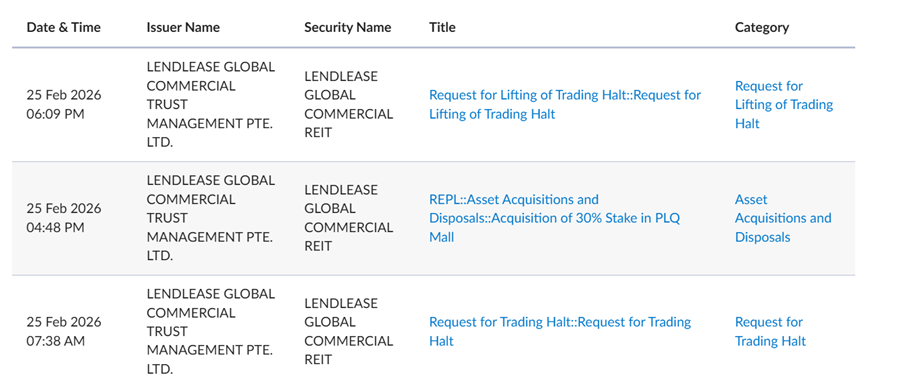

Lendlease REIT called for a trading halt on 25 Feb – and the acquisition and preferential offering were announced on the same day.

But from 11 Feb to 26 Feb, share price fell 13% from 0.66 to 0.575.

With exceptionally high volume on 20, 23 and 24 Feb.

Was this due to broader macro weakness or did people know what was coming?

Frankly I don’t know, but I’ve come to accept that this is just how things are.

But let’s leave this aside for now, and analyse the acquisition.

Lendlease REIT buys remaining 30% in PLQ Mall

Lendlease REIT owns 70% of Paya Lebar Quarter (PLQ) today.

They are now buying the remaining 30% that they don’t already own.

With real estate there are always 3 things you look at:

- Is the property good?

- Is the price good?

- How do you finance the acquisition

Let’s discuss each.

Is Paya Lebar Quarter a good property?

I’m just gonna put it out there and say yes.

My view – Paya Lebar Quarter is a great property to own.

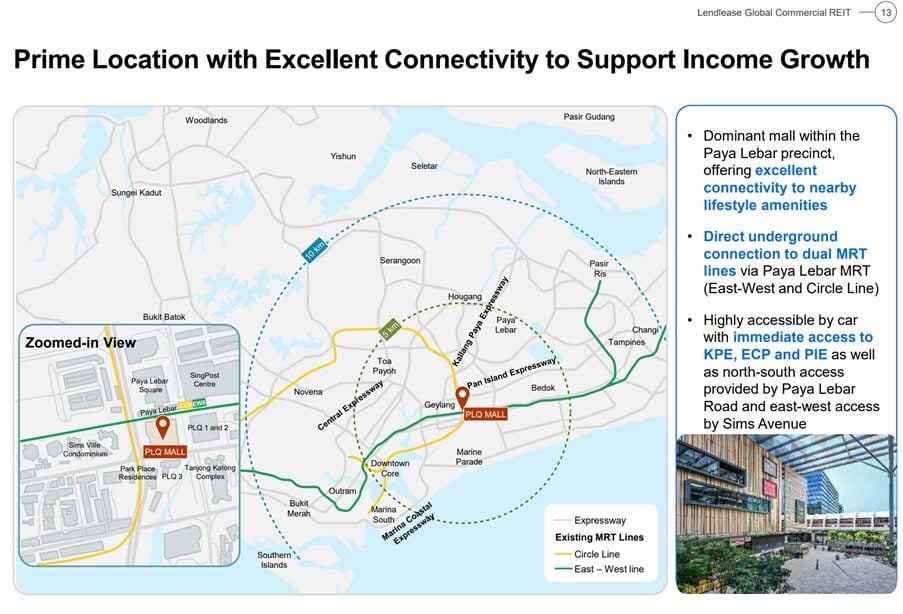

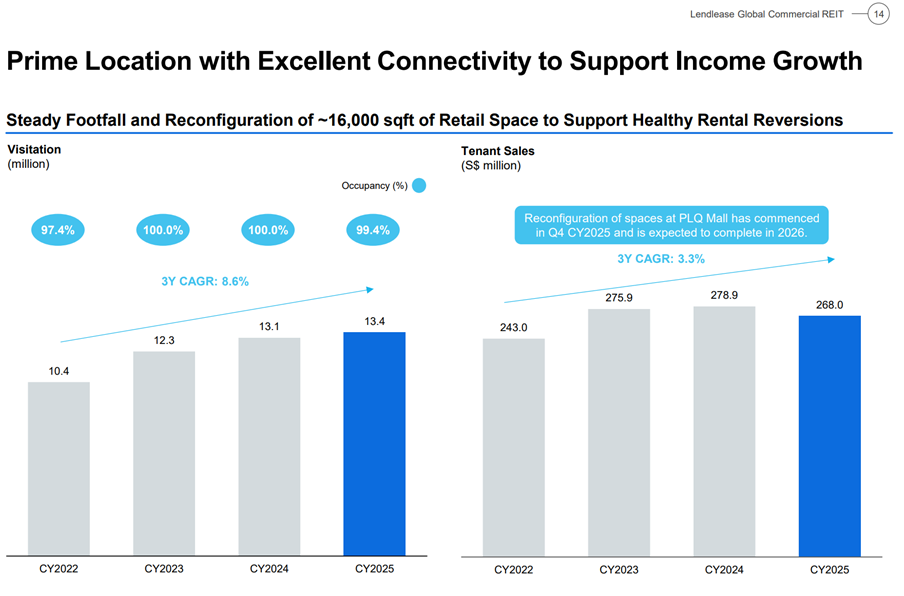

Location wise it’s right smack at Paya Lebar, which has excellent connectivity, and is positioned as a hub in the east.

For those who go to Paya Lebar frequently, you’ll know that there are 3 malls there – PLQ, Singpost centre, and Paya Lebar square.

Although because of the location (most convenient from the MRT being directly connected) and size (larger than Singpost centre and Paya Lebar square).

Every time I’m there I notice that PLQ has the strongest footfall, and it seems to be the more popular mall amongst locals.

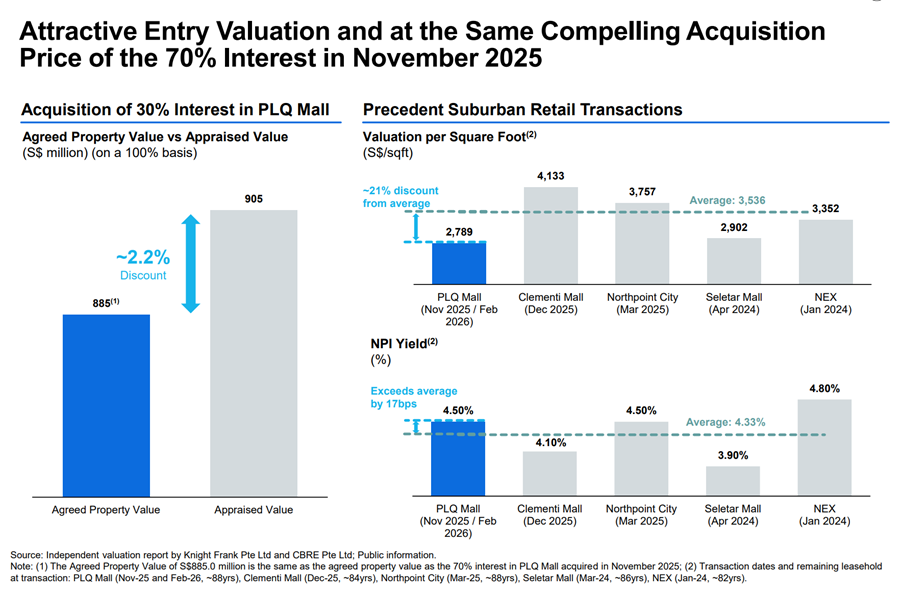

Is the price good?

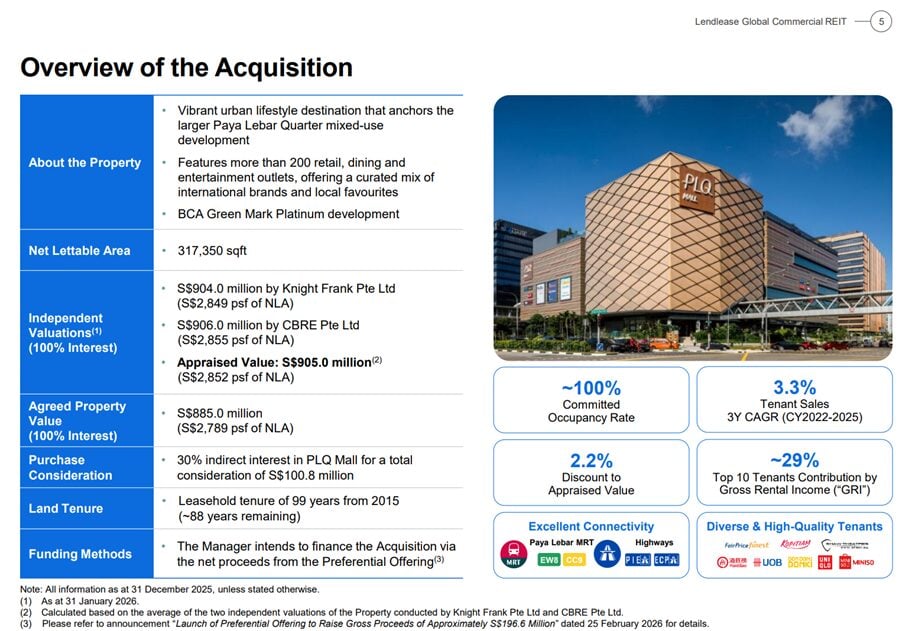

Acquisition price is at the same price at which Lendlease REIT bought in November 2025.

Which works out to roughly a 4.5% NPI yield.

This is more expensive than Nex which was transacted at 4.8% NPI yield.

Although to be fair Nex was done in Jan 2024 when interest rates were much higher – so it’s not exactly a fair comparison.

Comparing with 2025 transactions – the 4.5% NPI yield is cheaper than Clementi Mall (4.1%) and in line with Northpoint City (4.5%).

If you ask me I would say because of the prime location of PLQ Mall, the fact that it’s purchased at a comparable valuation to Clementi Mall and Seletar Mall is a good price.

If there’s one thing I don’t like about PLQ is that I would say PLQ today is a fully mature asset, so don’t expect significant growth going forward.

Although to be fair this is what REIT investing is about, so I can’t really complain.

If you pump in a new asset without strong rentals investors will complain that it’s DPU dilutive, if you pump in a mature asset investors will say no growth.

Can’t please everyone frankly.

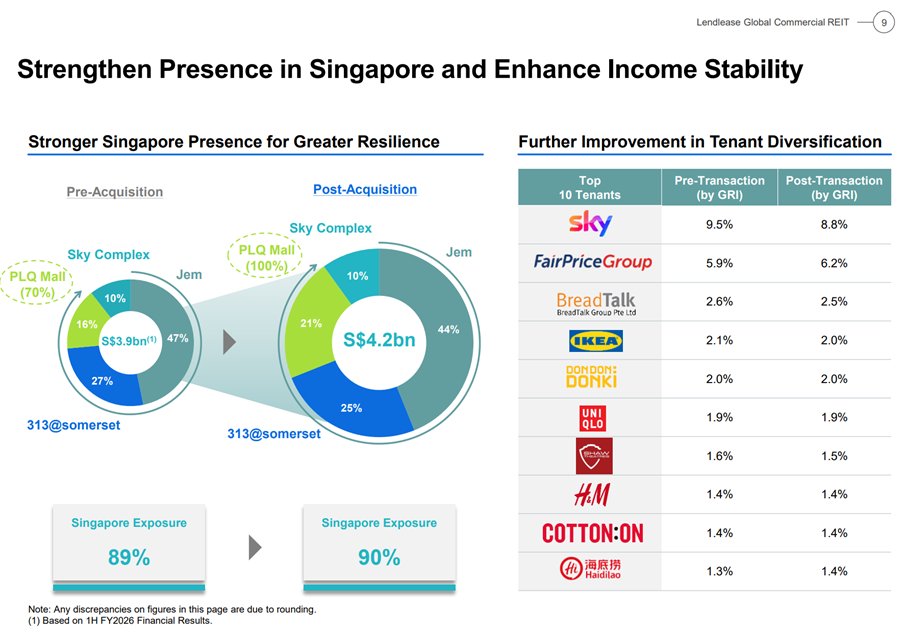

After the acquisition, 90% of the REIT will be Singapore assets in:

- Jem

- 313@Somerset

- PLQ

This is good, as in this more volatile climate I like it when my REITs are predominantly Singapore real estate exposure.

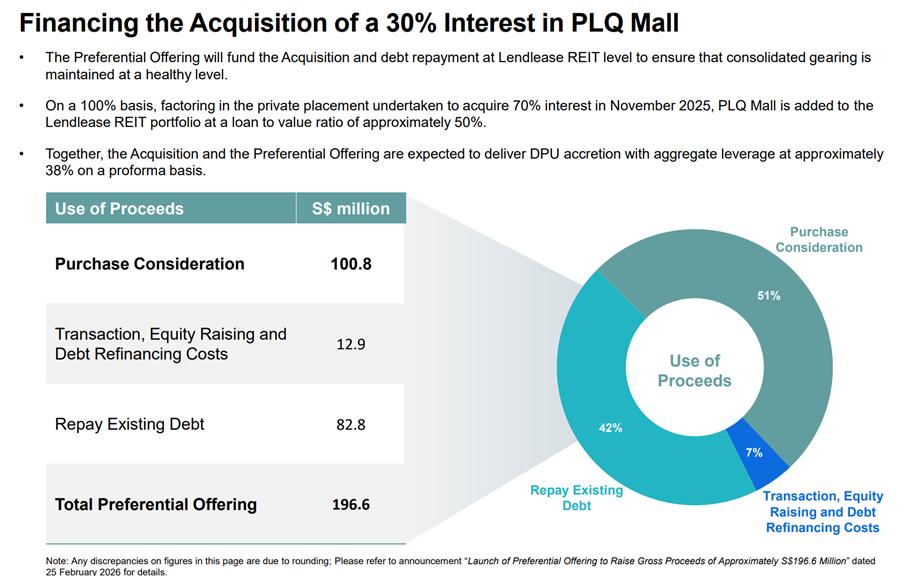

Funding is via a preferential offering

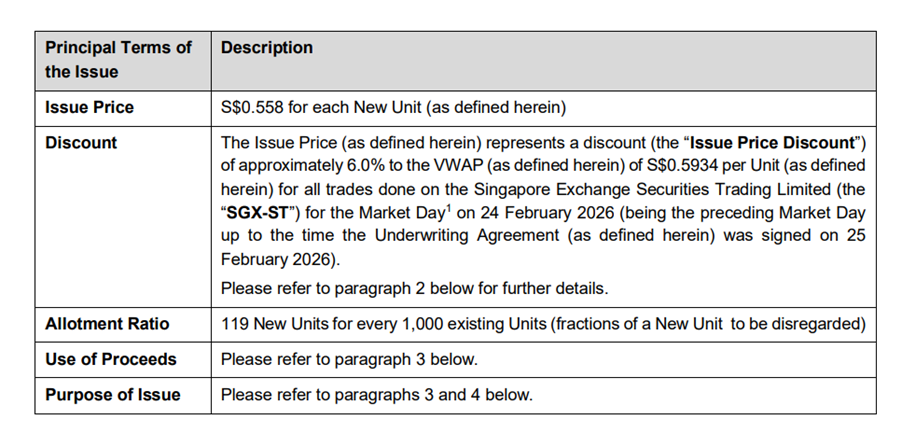

The acquisition will be financed via a $196.6 million preferential offering.

Half of that will be used to pay down debt, and the other half to pay for the acquisition.

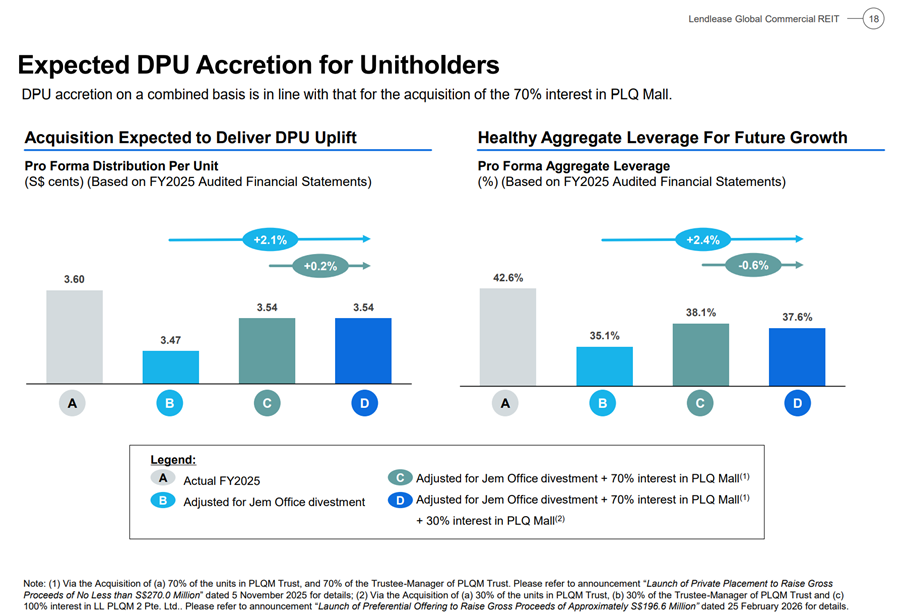

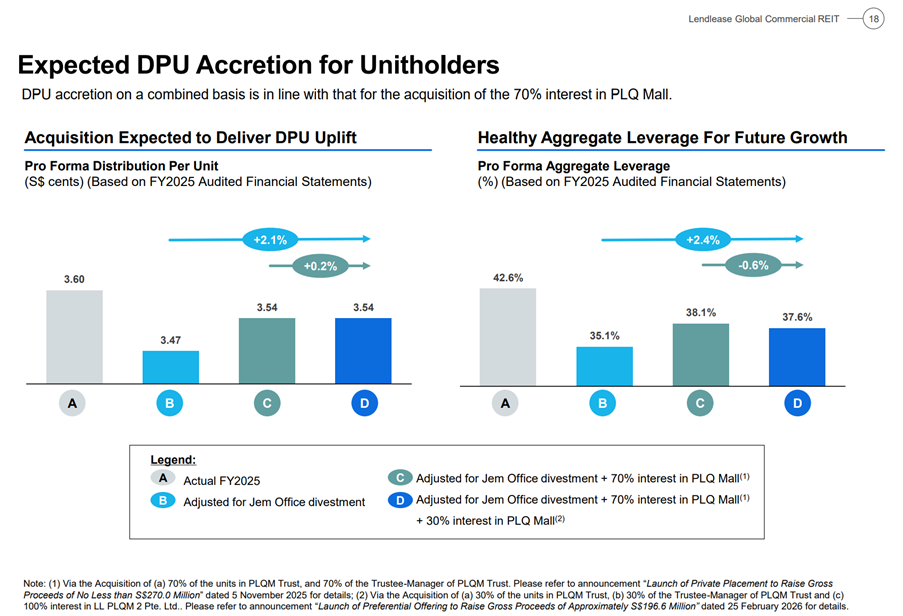

The acquisition is DPU accretive to the tune of 0.2%, which is tiny.

But it’s still a big difference from Keppel REIT where their acquisition of MBFC if you recall was DPU and NAV dilutive.

So can’t complain.

Lendlease REIT has executed a big change in their portfolio over the past year

If you recall, back when interest rates were much higher, there was a lot of concern around Lendlease REIT’s high 42.6% gearing.

Because of that the market punished the share price heavily and share price went into the mid 40s at one point.

To give credit where credit is due.

Lendlease REIT’s management seems to have actually taking this into account.

Because once interest rates started to drop, they made pretty big changes to the portfolio.

They sold Jem office to bring leverage down.

And bought PLQ.

Big picture wise I actually like this.

It’s a case of bringing down overall leverage, while also bringing up the quality of the overall portfolio.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

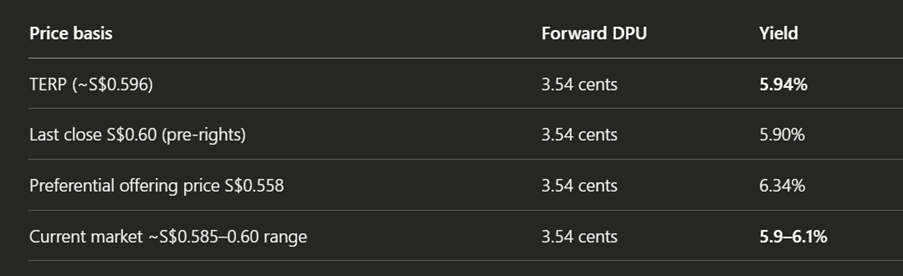

5.9% dividend yield of Lendlease REIT after the preferential offering?

Using the pro forma 3.54 cents DPU.

At the TERP of ~S$0.596, this implies a forward yield of ~5.9%.

Subscribers at the S$0.558 preferential offering issue price get an effective ~6.3% entry yield.

Is the dividend yield of Lendlease REIT attractive?

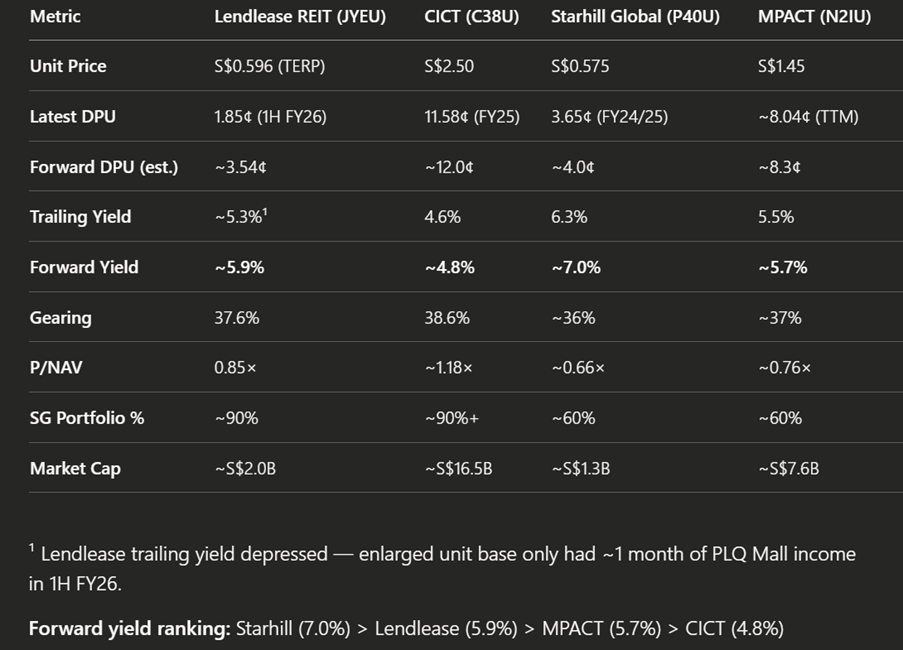

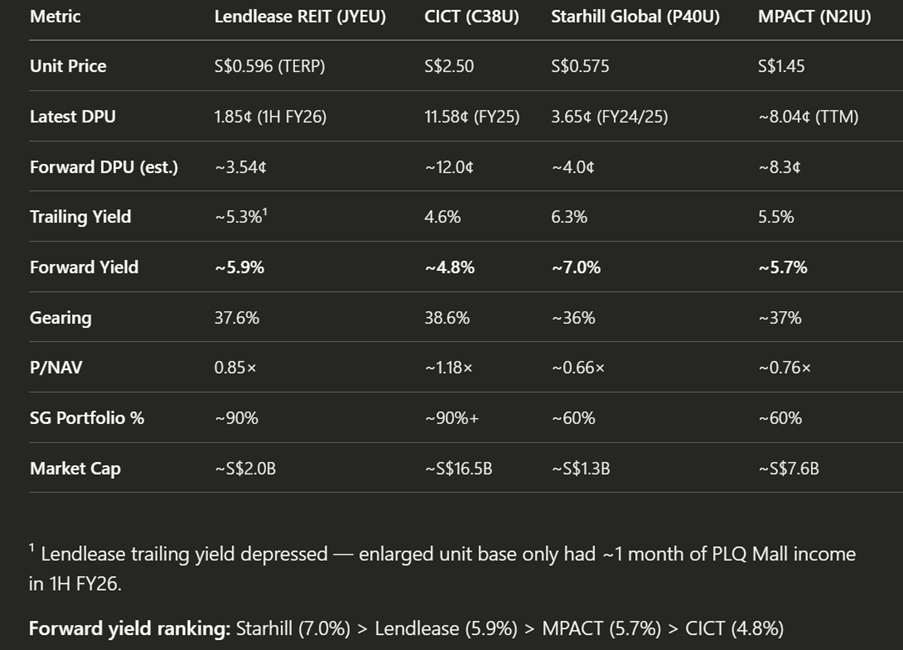

I’ve broadly benchmarked this against some other Singapore retail REITs below.

| Metric | Lendlease REIT | CICT | Starhill Global | MPACT |

| Unit Price | S$0.596 (TERP) | S$2.50 | S$0.575 | S$1.45 |

| Trailing Yield | ~5.3% | 4.6% | 6.3% | 5.5% |

| Forward Yield | ~5.9% | ~4.8% | ~7.0% | ~5.7% |

| Gearing | 37.6% | 38.6% | ~36% | ~37% |

| P/NAV | 0.85× | ~1.18× | ~0.66× | ~0.76× |

| SG Portfolio % | ~90% | ~90%+ | ~60% | ~60% |

| Market Cap | ~S$2.0B | ~S$16.5B | ~S$1.3B | ~S$7.6B |

In terms of yield, it is Starhill (6.3%) > Lendlease (5.9%) > MPACT (5.5%) > CICT (4.6%).

That looks fair to me – Lendlease is more risky than CICT and MPACT being a much smaller REIT, so should trade at a higher yield to them.

And arguably safer than Starhill Global REIT being larger in size and more diversified, so should trade at a lower yield.

At 65 cents, Lendlease REIT traded at a low 5% yield which to me made no sense when I could just buy CICT, Starhill or MPACT for better risk adjusted yield.

But I would say today after the sell-off, Lendlease REIT looks fairly priced.

Will I buy Lendlease REIT / subscribe for the preferential offering?

As shared above, I myself got lucky and I sold most of my Lendlease REIT in early feb in the mid 60s, as I thought Lendlease REIT was fully priced in the mid 60s.

That said, I still hold Lendlease REIT in my SRS account because it’s just too much trouble to sell SRS stuff, and even if I sell SRS stuff there’s not a lot of options to deploy the cash.

So this raises interesting questions for me:

- After the 13% decline, is Lendlease REIT worth buying back?

- For the bit of Lendlease REIT that I hold in SRS, will I subscribe for the preferential offering?

Will I subscribe for the preferential offering?

Let’s deal with the easy one.

Lendlease REIT trades at 0.58 on the open market today.

The preferential offering price is approximately a 4% discount to the current market price.

It’s not fantastic, but it’s probably still worth picking up for me.

So I’ll still subscribe, and I’ll pick up enough excess rights to avoid any odd lots.

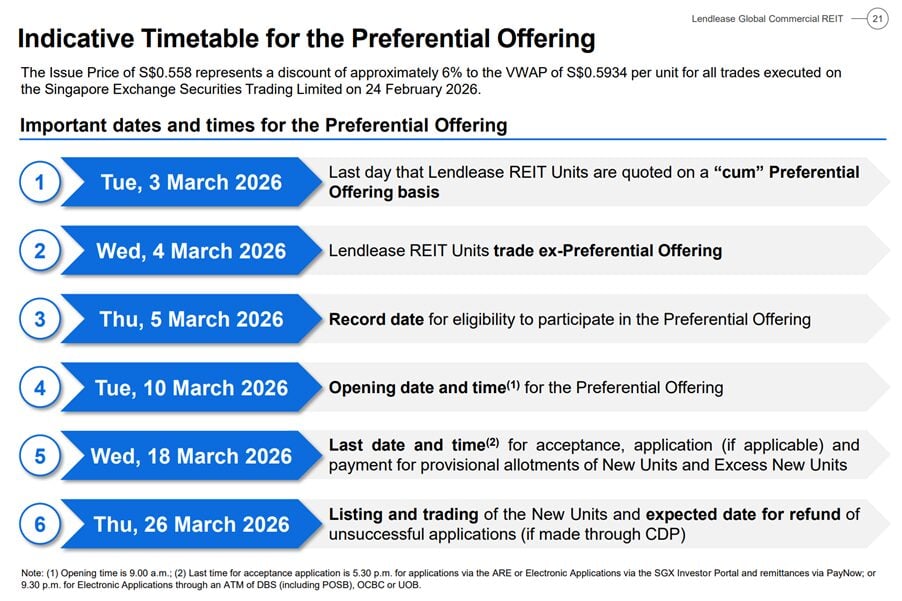

Timeline for the Preferential Offering for Lendlease REIT

For those of you who are looking to subscribe, see the full timeline below.

Lendlease REIT units trade ex rights on 4 March.

And you have until 18 March to “press button” and subscribe for your new units.

Will I buy Lendlease REIT?

If you asked me the same question at 65 cents, I would have said the answer was a resounding no.

At 65 cents, Lendlease REIT traded at a low 5% yield which to me made no sense when I could just buy CICT, Starhill or MPACT for better risk adjusted yield.

But after the 13% sell-off, the calculus definitely changes.

At a 5.9% forward yield, I think Lendlease REIT suddenly looks competitive vs the other 3 REITs below.

Especially because I like what management had done with the REIT over the past year, in bringing leverage down and increasing the quality of the portfolio.

What I don’t like so much about Lendlease REIT, is that this REIT has a frequent track record of equity fund raising:

| Date | Fundraising Type | Issue Price | Gross Proceeds | Primary Purpose |

| Oct 2019 | Initial Public Offering (IPO) | S$0.880 | S$1.03B* | Initial listing and portfolio injection (313@somerset and Sky Complex). |

| Mar – Apr 2022 | Private Placement & Preferential Offering | S$0.725 (Placement) S$0.720 (Pref) | S$648.8M | Funding the S$2.01 billion acquisition of the remaining interest in Jem. |

| Nov 2025 | Private Placement | S$0.602 | S$280.0M | Funding the acquisition of a 70% stake in PLQ Mall. |

| Feb – Mar 2026 | Preferential Offering | S$0.558 | S$196.6M | Funding the S$116.4M acquisition of the remaining 30% stake in PLQ Mall from its sponsor, plus debt reduction. |

Now that PLQ is fully acquired, I suppose the next potential asset in the pipeline would be Parkway – and boy that is not a small asset.

At a time when I’m looking to reduce my overall exposure to REITs, I’m really not a big fan of a REIT that may come to shareholders frequently with equity fundraises.

Whereas compare that to something like Starhill, where I don’t recall ever asking me to cough up cash in all the time I was a shareholder (Full disclosure that I hold a position in Starhill REIT as I like it more than Lendlease – see my full portfolio and watchlist on FH Premium).

So at this price, I’ll take up my SRS rights, but I don’t see myself buying much more of Lendlease REIT.

Unless of course the price continues to drop, then of course you know how the saying in real estate goes –“There’s no such thing as a bad property, only a bad price”.

At the right price – hey I could be convinced to like anything.

This is an FH Premium article that I am releasing to all readers, and will not be updated going forward. My latest macro and stock views are shared on FH Premium, together with my full stock watch and personal portfolio.