In case you’ve missed it.

Global stock markets are in a sell-off mode for anything that is remotely software, or software as a service (SaaS) related.

The narrative is that AI is going to disrupt software writing, and therefore software related companies are going to be in a world of pain.

Or at least that was the original narrative that triggered the selling, and then the selling took on a life of its own, and now even things like Gold and Bitcoin are selling off too.

Whatever, the case, the market is starting to look like it’s throwing the baby out with the bathwater here.

For investors prepared to stock pick, I think there is plenty of opportunity with the current sell-off.

Sea Limited is a stock that has been on my watchlist for a while now (full disclosure that I hold a position).

And with the recent sell-off, Sea Limited is down a whopping 50% from its cycle highs of $200.

With this sell-off, will I buy the owner of Shopee, Garena and Maribank?

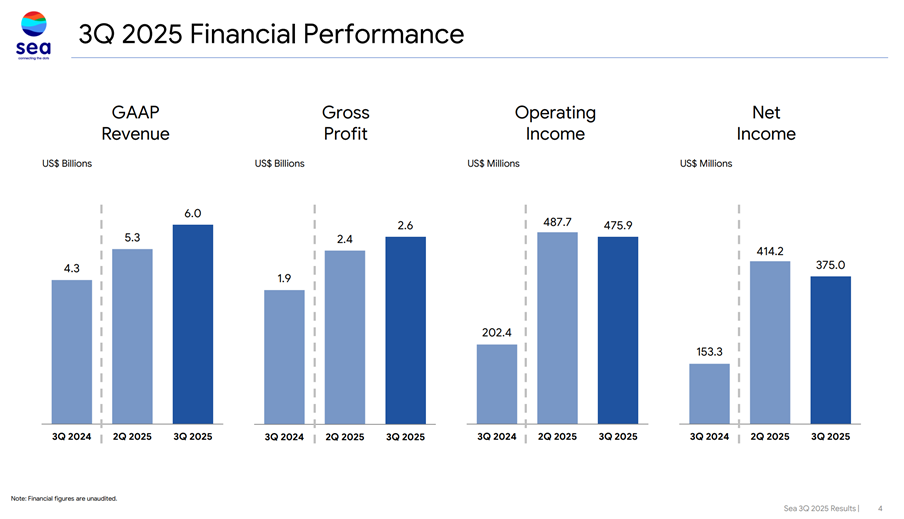

Financial Results of Sea Limited

Let’s look at the financial results.

Big picture wise, the 3Q financial results are decent.

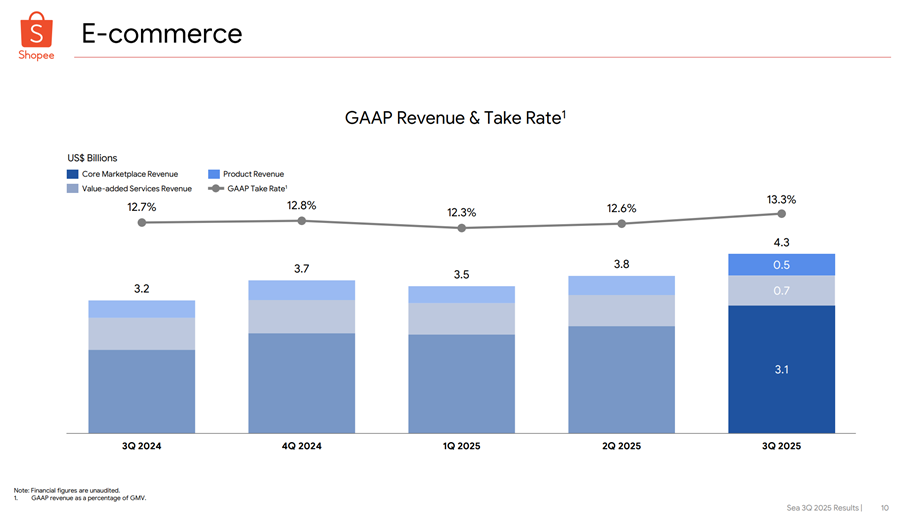

Topline revenue growth is growing across all 3 key business segments.

It’s when we look at profitability that things get a bit more mixed.

Yes, Gross Profit is up quarter on quarter.

But Net Income is down quarter on quarter.

Indicating that despite the revenue growth, Sea Limited is actually not making money on that higher revenue.

What’s driving this?

Let’s break it down by each of the 3 business segments:

- E-Commerce (Shopee)

- Fintech (Monee, MariBank)

- Gaming (Garena)

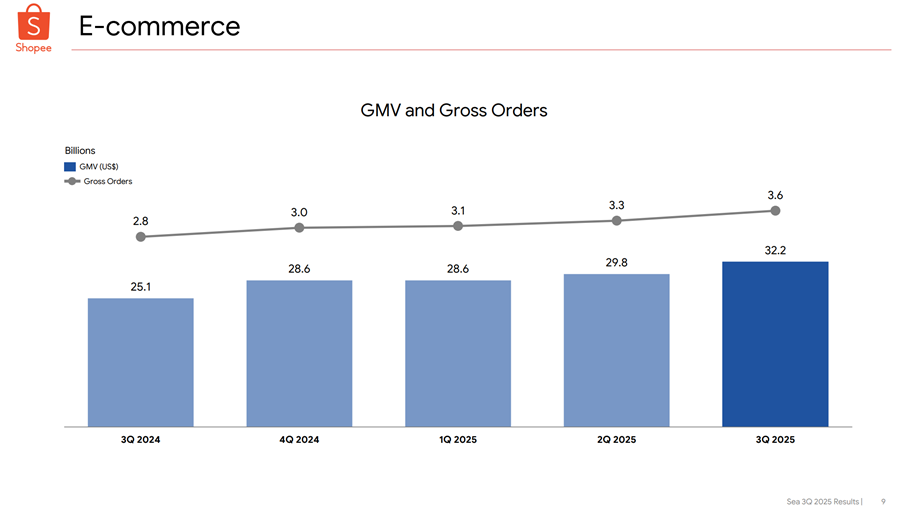

Shopee’s – Growing GMV, but declining profits?

GMV, or Gross Merchandise Value, is the total monetary value of all goods sold through the Shopee e-commerce platform before deducting fees, discounts, or returns.

You can see how that continues to grow nicely.

Per management:

“We now expect Shopee’s full-year 2025 GMV growth to be more than 25%”

Which is very solid growth.

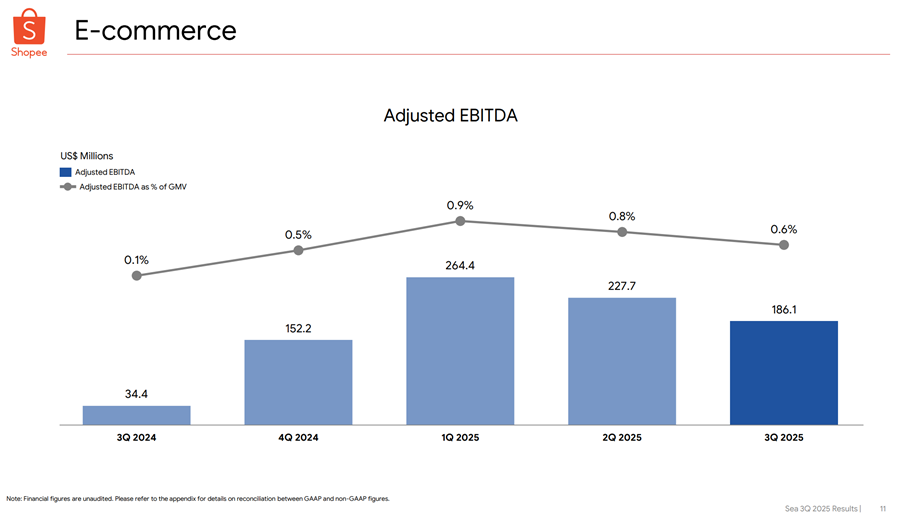

That said – that strong growth in GMV, is not backed up by a strong growth in profits.

Despite the growth in GMV, Adjusted EBITDA margins have fallen from 0.9% in 1Q, to 0.6% today.

And Adjusted EBITDA is down 30% from 1Q 2025.

This suggests that a decent proportion of the GMV growth is coming at the expense of subsidies / discounts – hence the lower profits.

Which begs the question of how sustainable it is.

My personal view – there’s nothing scarier than an eCommerce player that needs to give out discounts to grow market share.

We’ve seen this with Alibaba in China, that when eCommerce players go into a mode like that they can really incinerate cash without much to show for it.

And this isn’t the 2010s era of free money anymore.

Burn cash to grow market share, and the market will punish you for it – as you can see with the current market sell-off.

With Shopee’s track record in 2022 – 2024, they’ve shown that they can switch to profit making mode when they need to.

But for now at least, the declining eCommerce margins are worrying.

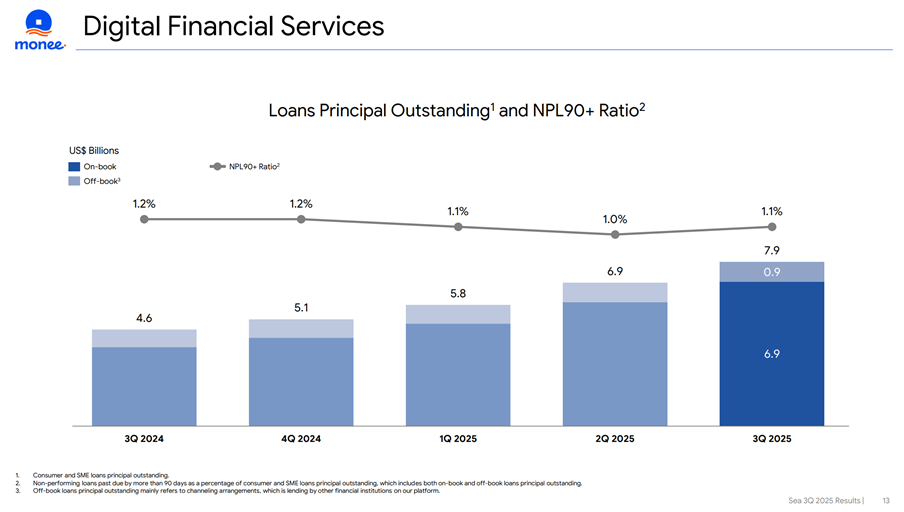

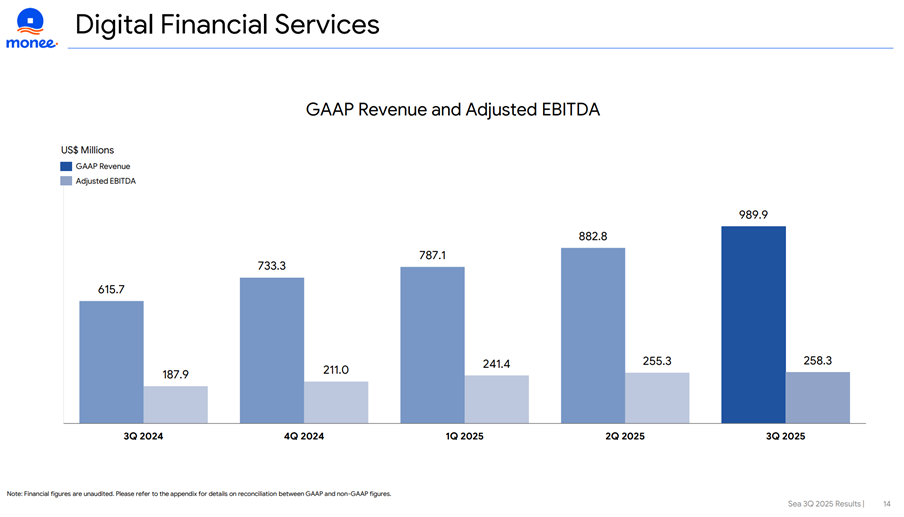

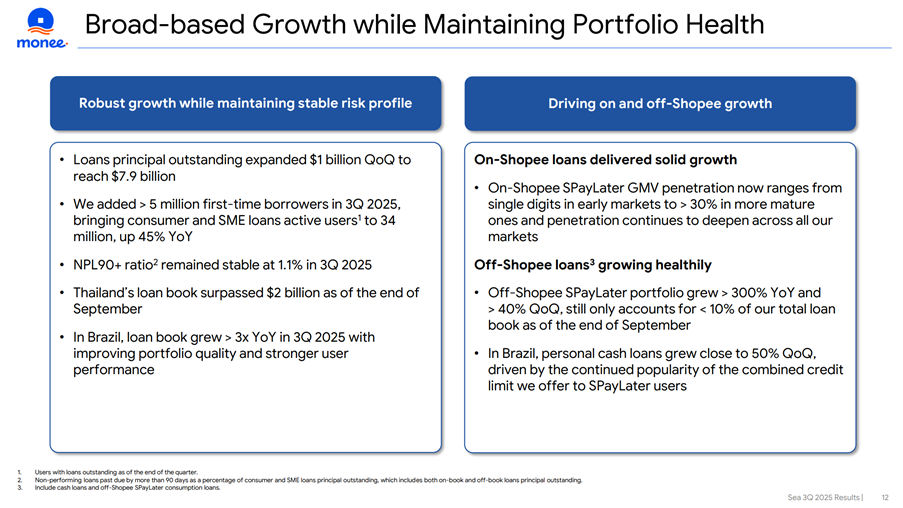

Monee – Fintech a ticking time bomb or a money printer?

Monee is the fintech banking arm of Sea Limited, which Singapore investors will know as Maribank.

Loans outstanding is growing very nicely, while non-performing loans are low.

Revenue is growing very nicely, but Adjusted EBITDA (a proxy for profits) is flat.

Which raises the same question as e-Commerce.

Yes the topline growth is strong.

But when the time comes, can Sea Limited actually make money from this?

Based on track record I would say the answer is a cautious yes, but for now all this growth without profitability has the market nervous, and it’s not helping the sell-off one bit.

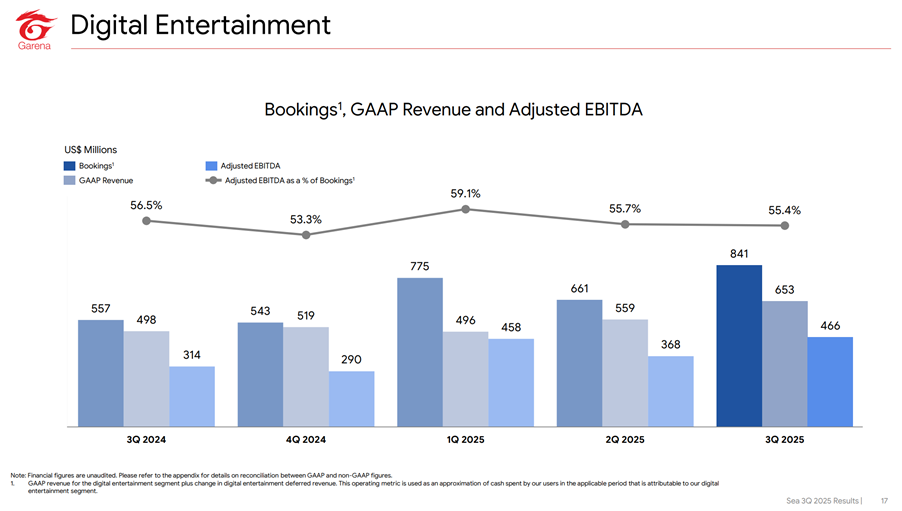

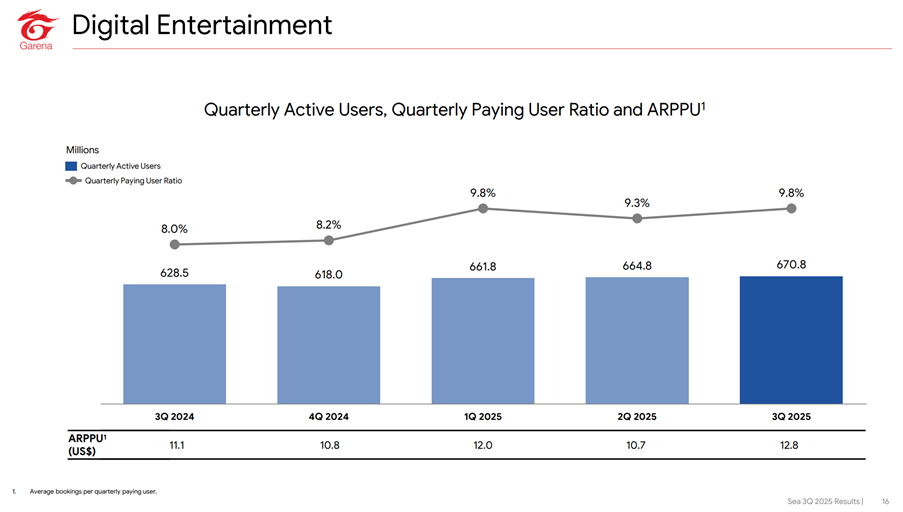

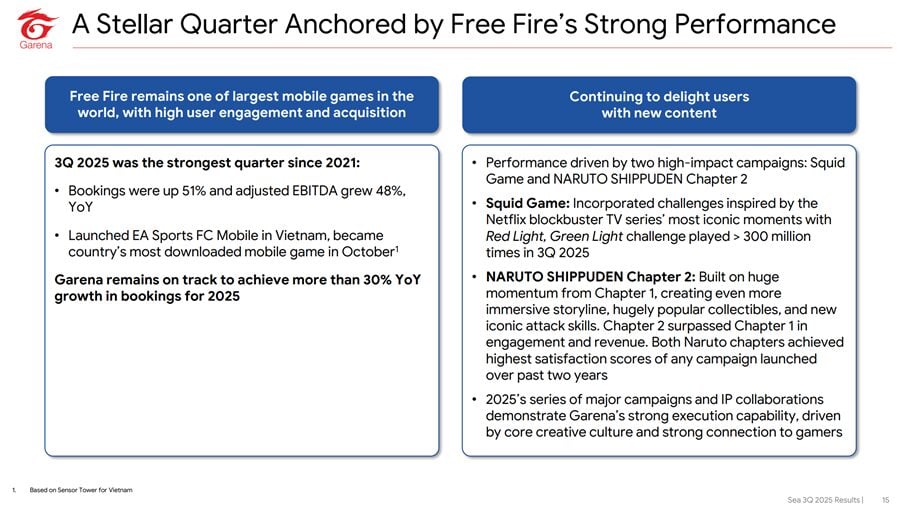

Garena – Free Fire remains a cash cow, but a one-trick pony?

And then we have Garena, the gaming business which historically has been the cash cow.

Here you can see that Adjusted EBITDA is actually up on a quarter on quarter basis, which is really nice to see.

This comes despite quarterly active uses staying roughly flat.

So the reason why Garena has been able to make more.

Is by squeezing more out of the existing customers.

More customers are paying, and each paying customer is spending more.

If Sea Limited can replicate this with e-Commerce and Fintech, the stock will truly fly.

That said the problem with Garena is that that ultimately the entire business is being carried by one game – Free Fire.

And Free Fire is an 8 years old Battle Royale, released in Dec 2017.

The fact that Sea Limited has been able to squeeze so much out of Free Fire, is itself very strong execution.

But definitely there is concentration risk here, and this is a very mature business with a limited runway left.

The strategy for now is to take the profits from Free Fire and invest in (a) new games, (b) Shopee, and (c) Fintech.

But per the analysis above, these other businesses need to deliver strong profitability at some point for the stock to recover.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Balance Sheet of Sea Limited is very strong

The bright side though, is that Sea Limited has a rock solid balance sheet.

They are currently free cash flow positive.

Coupled with a $10.5 billion cash position on the balance sheet.

Sea Limited is rock solid at the moment.

Short of them entering into a massive discount war in E-Commerce, they are in no immediate needs to raise cash or financing.

What is the risk with Sea Limited stock?

So what’s the biggest risk with Sea Limited stock today?

If you ask me, I think the single biggest risk is TikTok Shop’s structural disruption of Shopee’s e-commerce dominance.

Tik Tok is a fundamentally different discovery model.

Instead of going in to buy what you want, you discover what you want through others.

And TikTok with Tokopedia is a genuinely formidable competitor in Shopee’s key Indonesia market.

If Shopee loses Indonesia (or a good chunk of it) to Tik Tok, that just fundamentally changes the story for the stock.

Secondary risks include Monee credit cycle exposure (70% loan growth into a potential macro slowdown) and Free Fire concentration in Garena.

All three risks are correlated to execution in a highly competitive environment.

Much will come down to the ability of Forrest Li and his team to execute in the face of very strong competition.

Track record though – has been very strong.

For those old enough to remember, Forrest Li started from Garena as a gaming platform (back when Garena was a Warcraft III Lan platform, boy I still remember connecting to Garena to fire up a Dota game), and built Sea Limited into the juggernaut that it is today.

My personal view is that as long as Forrest Li stays at the helm, I think they can navigate the challenges.

Founder led companies like Sea Limited and Facebook are just different like that.

Risk-Reward of Sea Limited stock?

I crunched the numbers on the risk-reward of Sea Limited stock, assuming a $107 entry.

| Scenario | Probability | FY28E Rev ($B) | FY28E Adj. EBITDA ($B) | Exit Multiple | Target Price | Return vs. $107 |

| Bull | 25% | $42B | $7.5B | 22x | $260 | +143% |

| Base | 50% | $34B | $5.5B | 18x | $170 | +59% |

| Bear | 25% | $26B | $3.0B | 12x | $65 | -39% |

| Weighted Avg | 100% | — | — | — | $186 | +74% |

Based on this, there is decently asymmetric risk-reward, in that you make more when you’re right, vs how much you lose when you’re right.

You can see the various assumptions I used below, and of course feel free to disagree.

Bull Case (25% probability, +93% upside to $260)

Thesis: Shopee entrenches dominance in SEA & Brazil; Monee becomes a scaled fintech franchise; Garena stabilizes as a cash cow.

- Revenue CAGR: ~25% (2025-2028) → $42B by FY28

- EBITDA Margin: Expands to ~18% as Shopee reaches 3%+ EBITDA/GMV margin and Monee scales

- Exit Multiple: 22x (premium for durable growth + fintech optionality)

- Catalysts:

- Shopee commanded 52% of Southeast Asia e-commerce GMV in 2024, up from 48% in 2023, reaching $66.8B. Management targets Shopee EBITDA/GMV margins of 2-3% long-term.

- SEA e-commerce penetration was just 12.8% of retail in 2024, with estimates that AI and logistics improvements could unlock an additional $130B in GMV by 2030.

- TikTok Shop faces regulatory headwinds (Indonesia restrictions, US uncertainty)

- Monee achieves bank-like returns on equity as credit portfolio matures

Base Case (50% probability, +26% upside to $170)

Thesis: Solid execution continues but competition intensifies; profitability improves modestly.

- Revenue CAGR: ~18% → $34B by FY28

- EBITDA Margin: ~16% (current ~15% expands slightly as logistics costs decline)

- Exit Multiple: 18x (in-line with growth-adjusted peer average)

- Key assumptions:

- E-commerce revenue expected to grow by 25% in 2025 and 19% in 2026; Gaming revenue forecast to increase by 16% in 2025 and 10% in 2026; digital financial services revenue projected to grow by 29% in 2025 and 24% in 2026.

- Shopee holds ~50% market share but growth decelerates as market matures

- TikTok Shop has surged to 41% market share in Vietnam (vs Shopee’s 56%), posting 69% growth while Shopee’s growth slowed to 4% in Q3 2025 in that market.

Bear Case (25% probability, -52% downside to $65)

Thesis: TikTok Shop gains substantial share; Monee credit quality deteriorates; Garena revenue declines; multiple compression.

- Revenue CAGR: ~8% → $26B by FY28

- EBITDA Margin: Contracts to ~12% due to renewed price wars

- Exit Multiple: 12x (de-rated to Alibaba/JD levels)

- Key risks:

- TikTok Shop has emerged as a disruptive force, challenging the longstanding duopoly of Shopee and Lazada with “shoppertainment” models anchored in livestreaming and short-form video.

- Macro slowdown in SEA/Brazil pressures consumer spending and credit quality

- Monee NPLs spike above 3% if economic conditions deteriorate

- Free Fire engagement declines; new game launches fail

Valuations of Sea Limited stock at $107

At $107, SE trades at a 40% discount to MELI on forward EBITDA despite similar growth rates and market position. This is unusual and reflects either:

- Legitimate concern about margin sustainability (fair)

- Excessive pessimism driven by recent drawdown (opportunity)

| Metric | SE @ $107 | MELI | Coupang | JD.com |

| EV/TTM EBITDA | ~16x | ~30x | ~25x | ~8x |

| EV/FY26E EBITDA | ~12x | ~20x | ~18x | ~6x |

| Revenue Growth (TTM) | 38% | 40% | 25% | 5% |

| Profitable | Yes | Yes | Yes | Yes |

In plain English – valuations are cheap.

Yes you can argue that Sea Limited has a good chunk of gaming revenue which deserves a lower multiple.

And sure you’re not wrong, but then there is also the Fintech arm that deserves a higher multiple.

Valuation is an art not a science, and I would say at current valuations, Sea Limited is “cheap”.

But ultimately it’s all going to come down to execution.

That said – no doubt Sea Limited is a falling knife at the moment

Technical analysis – boy the chat is as ugly as it gets.

Price is trading below all key moving averages.

It also broke the 120 support level.

In a clear downtrend.

This is probably the very definition of a falling knife.

The only saving grace is that if $100 holds that *could* be a strong support level.

But yeah with this kind of chart, just let the price action play out.

Unless the price gets to an unbelievable level where I can just close my eyes and buy.

I’m going to let the price action stabilize before I make any decision on buying (if at all).

Sea Limited shares fall 50% to April 2025 lows – Will I buy Shopee stock?

So… knowing all that I know above.

Will I buy Sea Limited stock?

I think my answer is a qualified yes – for the simple reason that I believe in Forrest Li.

Call me a sucker, but I think founder led companies are just different from manager led companies.

There’s a kind of raw drive and grit, that money can’t buy.

Sea Limited faces massive competition in its key markets and they are currently sacrificing profitability to grow market share.

Will the be able to defend market share and profitability longer term?

That ultimately depends on Forrest Li and his team.

Numbers wise – the valuations are cheap, but much will come down to execution ability.

If the management team can execute, I could easily see this stock going to $200 or more.

If they can’t, and competition erodes market share and profitability, you’re probably looking at $60 or below.

That said, that looks like asymmetric risk reward to me.

If I’m wrong I lose 50%ish.

If I’m right I could make up to 100% or more.

That said, this stock is definitely not without risk, so position sizing matters.

No matter how confident I am on a stock, I size the position such that if I am completely wrong, I can take the loss.

And of course, this is clearly a falling knife at the moment, so that needs to factor into the decision making process.

For what it’s worth, I think with the recent sell-off in software and crypto, there are plenty of opportunities in this market if you stock pick.

You can see my full stock watch, and my regular portfolio updates on FH Premium if / when I decide to buy or sell Sea Limited stock (or other stock).

Love to hear what you think though – will you buy Sea Limited stock?

If you enjoy articles like this, do support Financial Horse on FH Premium and get access to premium articles like this, including my stock watch and investment portfolio.

well the question is why should i bother with Sea when Amazon just sold off due to massive AI capex, which ought to be a good thing

Eh… that’s AWS capex. Sea has no cloud computing arm.

so ur point being we shouldn’t compare these 2, or a gaming arm is better than cloud arm for a e-commerce company?

I guess my point is more that it’s not a direct apples to apples comparison. Amazon’s core e-commerce business in NA/EU is money making, a very different market from the brutally competitive SEA/Brazil market that Shopee operates in. And Amazon has AWS as a cash cow (which has a long runway ahead, but requires a lot of capex), Sea has Garena (where free fire is clearly in the later stages of its cycle). So while some lessons can be drawn from Amazon’s earnings sell-off, there are also some key differences between the 2 companies.

OK good points. Maybe a deep dive into another local nasdaq listing – Grab Holdings?

Sure – let me do a piece on Grab.