For those of you who may have missed it.

Singapore stocks are on fire.

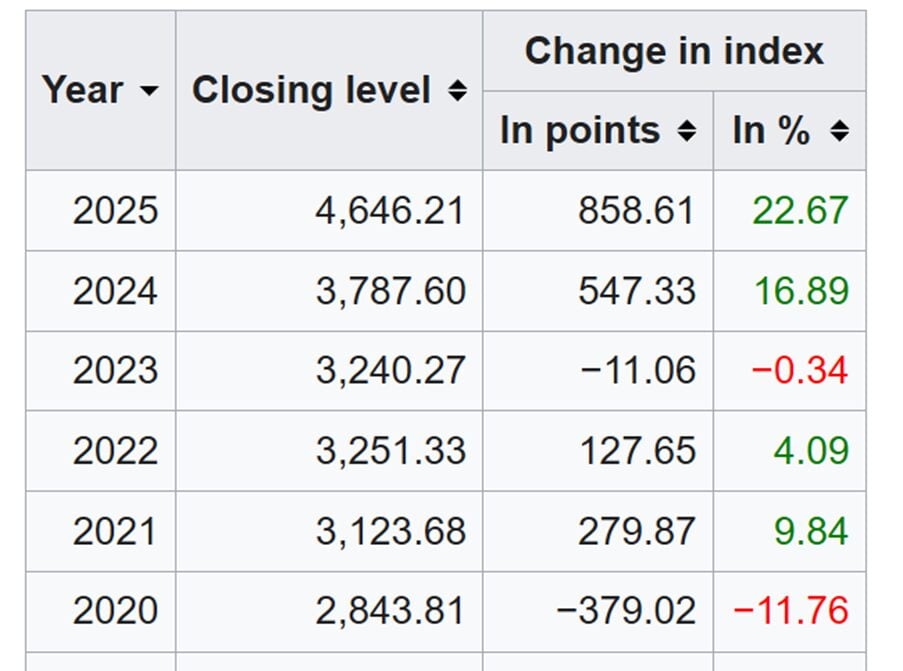

The Straits Times Index (STI) is up a whopping 27% in the past 12 months (30% if you include dividends).

That’s outperforming the S&P500’s 15% by a mile – even more if you factor in the USD depreciation.

That said.

Almost 50% of the STI is the 3 local banks, so a big chunk of this performance is because bank stocks have soared.

With this kind of performance, does it still make sense to buy bank stocks today?

Or will other Singapore stocks have more upside potential in 2026?

Straits Times Index (STI) up 27% the past 12 months

You can see the chart of the STI above.

The STI is up 27% in the past 12 months.

For comparison – the S&P500 was up 15% in the same time period.

Note that the USD was 1.35 in 2025 vs 1.27 today – working out in a 6% depreciation vs the SGD.

And don’t forget the STI has about a 3% dividend yield.

Viewed this way, the STI has pretty much outperformed the S&P500 by almost 20% over the same time period.

All those advice to buy and hold the S&P500?

Turns out you actually would have outperformed in a big way just buying the boring ol STI Index.

Why I’m NOT selling the banks / blue chips – but also not buying in a big way at these levels

That being said.

The STI has had 2 consecutive years of double digit rallies.

And after the huge 2024 and 2025 rally, the blue chip Singapore stocks are no longer “cheap”.

DBS today trades at a 2.5x Price/Book ratio.

And yes I know DBS is a great bank and all – buy buying DBS in a big way at 2.5x book ratio?

That’s just not amazing risk-reward in my view.

Yes it’s a great momentum play and can continue to go higher, but at these valuations there is real downside risk.

Meanwhile other big blue chips like SGX and ST Engineering.

You can see how much they have rallied.

ST Engineering at current prices pays a mere 1.7% dividend yield

Generally speaking I am not selling my core bank holdings (never sell the cash cows), because with this kind of momentum you want to let the price action continue to grind higher.

But I am also reluctant to add to my positions in a big way here.

I just don’t find the risk-reward amazing.

What other Singapore stocks may benefit in 2026? The “EQDP” Effect?

Which brings me to my next point.

The Equity Market Development Programme (EQDP) is a S$5 billion government stimulus package launched by the Monetary Authority of Singapore (MAS) to revitalize the Singapore stock market.

Think of it as “Quantitative Easing” specifically for Singapore stocks—but instead of buying bonds, the government is giving cash to active fund managers with a strict mandate to buy listed Singapore companies.

The S$5 billion is being deployed in waves (tranches) to prevent a sudden market spike.

- Tranche 1 (July 2025):S$1.1 Billion.

- Managers: Avanda, Fullerton, JP Morgan.

- Impact: This stabilized the market in late 2025.

- Tranche 2 (Nov 19, 2025):S$2.85 Billion.

- Managers: Amova (formerly Nikko AM), AR Capital, BlackRock, Eastspring, Lion Global, Manulife.

- Status: This money was announced in late Nov 2025, meaning the actual buying is happening right now (Q1 2026).

What will EQDP buy next? Different mandate

What is EQDP money supposed to buy?

These managers are not supposed to blindly buy the STI ETF.

Their mandate specifically targets:

- Small & Mid-Cap Stocks: Companies outside the 30 STI components to boost broader liquidity.

- Active Selection: They are paid to find undervalued companies with strong fundamentals, not to hug the index.

- IPOs: They can act as cornerstone investors for new listings (reviving the IPO market).

And the reason why it matters is because of the lag effect.

Institutional money takes 2–3 months to set up and deploy. That “deployment window” is opening now.

The EQDP funds are explicitly hunting for liquidity and value in the S$1B – S$5B market cap range.

Is EQDP significant enough to move the Singapore market?

I get many questions on whether EQDP is sufficient to revitalize the Singapore markets.

My initial answer was no.

My original view was that the structure issues hindering the local SGX market, and the poor liquidity, could not be easily overcome by MAS’s efforts.

But recently, I have changed my mind on that somewhat.

Especially after the strong 2025 performance on the STI.

Liquidity begets liquidity, and with 2 consecutive years of strong STI performance, and EQDP coming in, that could actually move the needle.

I got Gemini to crunch the numbers, of whether a $2.85 billion deployment in Tranche 2 can make a difference:

1. The “Small Pond” Effect (Liquidity Ratio)

With daily turnover at just S$50–150 million, S$2.85 billion represents 19 to 57 days of total trading volume. unlike Tranche 1’s “floor,” this magnitude creates a massive “buy wall.” In such a thin market, this forces prices to gap up significantly just to find willing sellers.

2. Market Cap Concentration

The allocation is ~2.9% of the entire S$98 billion index. If managers concentrate this capital into a select S$20 billion basket of high-conviction names, they would absorb roughly 14% of the available float. This scarcity can drive valuations closer to privatization premiums than standard market multiples.

3. The Multiplier Effect

The entry of global giant BlackRock adds a “seal of approval” absent in Tranche 1. This triggers aggressive front-running by global desks tracking BlackRock’s flows, potentially amplifying the effective capital hitting these counters well beyond the initial S$2.85 billion.

As you can see.

$2.85 billion if deployed into a select number of mid cap stocks on the SGX.

Can actually really move the needle once you factor in the fact that:

- These fund managers are likely to reach the same conclusion that the same x number of stocks are a good buy

- The low trading liquidity means when the money gets deployed, it can actually really move the needle

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

What Singapore stocks may benefit from EQDP?

I suppose what I am saying.

Is that if I am right on this.

Then there could be opportunity looking away from the mega-cap stocks like DBS, OCBC, UOB.

And into the small – mid cap space where EQDP will target.

Which brings us to the next question.

Which Singapore stocks may benefit?

I put both the cutting edge models of Claude and Gemini against each other on this one, and the selections are very interesting.

Let me share the selections by both models first, then I’ll share my own thoughts.

Here’s Claude (charts added by me):

The S$5 billion EQDP explicitly targets non-STI small/mid-caps with market caps of S$200m–S$3bn, preference for liquidity improvement, and active fund management. Three stocks positioned to capture disproportionate EQDP inflows are:

CSE Global (SGX: 544)

Data center electrification play with transformational Amazon partnership worth up to US$1.5bn over five years. Recent US$143.5m contract extension validates hyperscaler demand. Trading at 12x P/E with strong order visibility. Core EQDP target at S$600m market cap.

Frencken Group (SGX: E28)

Semiconductor equipment proxy trading at discount to peers despite 47% revenue from semicon. Leveraged to ASML EUV ramp expected in 2H26. Net-cash balance sheet provides downside cushion. Analysts see re-rating potential from current ~14x to 17x P/E as orders recover.

iFAST Corporation (SGX: AIY)

Singapore’s leading fintech platform hitting profitability inflection with 55% YoY profit growth. Multiple engines: Hong Kong eMPF, digital bank breakeven, regional wealth management. Recent Financial Alliance acquisition extends distribution. Premium valuation but justified by 30%+ earnings growth trajectory.

Here’s Gemini:

Pick #1: The Turnaround Titan – Seatrium

The Thesis: The order book is full, legacy issues are cleared. While banks are at ATH, Seatrium is still recovering. It’s a leverage play on the global energy/offshore cycle without the bank valuation risk.

Target: Looking for a breakout above the $2.00 psychological resistance.

Pick #2: The Growth Compounder – iFAST

The Thesis: If the SG market is booming, who sells the shovels? iFAST. A bull market means higher AUA (Assets Under Administration) and trading fees. It is the highest beta play to a rising STI.

Risk: High P/E, but momentum is undeniable.

Pick #3: The “Deep Value” Laggard – OUE REIT (or CDL Hospitality)

The Thesis: While commercial REITs rallied, hospitality/mixed-use has lagged. With rate cuts delayed (the “Double Pause”), you want a REIT with real asset backing trading at a 30-40% discount to NAV.

Yield: Locking in ~6.5% while waiting for the capital recycling catalyst.

Honourable Mentions

And some honourable mentions that came up from both models:

- AEM Holdings

- UMS Integration

- Venture Corp

- Food Empire

My personal thoughts – What Singapore stocks may benefit from EQDP?

For obvious reasons, the list of stocks above is meant to be an initial list for further analysis.

I am NOT saying to go out and buy them tomorrow.

My full portfolio is shared on FH Premium, and for now it’s still primarily weighted towards the blue chips.

I still intend to hold those core positions for now.

But with the current valuations, and after such a strong rally.

I do have my doubts whether they continue to outperform going forward.

Hence for fresh capital, I am inclined to find alternative places to park them.

And per the analysis above, I think the mid cap SGX stocks look interesting, especially with EQDP coming into play, and with the strong STI performance potentially attracting more attention to Singapore stocks.

From the list above, iFast global and the semiconductor names jump out at me at first glance.

They are not cheap, but many of them have strong momentum.

And if the EQDP money starts to crowd into these names, I can potentially see them going higher.

But to be absolutely clear – this is not without risk, and more analysis is required before I pull the trigger.

As always, you can see my full stock watch and what I am buying on FH Premium.

Love to hear what you think on this though.

Would you still primarily allocate to Singapore banks and blue chip stocks?

Or would you focus more capital into mid cap stocks in 2026?

If you enjoy articles like this, do support Financial Horse on FH Premium and get access to premium articles like this, including my stock watch and investment portfolio.

Hi FH,

https://sgwealthbuilder.com/2026/01/31/silver-price-crashed-into-sea/

Is it the right time to enter or should wealth builders bolt for the exit? On 30 January 2026, silver price plunged 31%, falling from a record high of US$120 per troy ounce to US$85 per troy ounce. The stunning reversal of silver price caught many investors by surprise as silver price has been on a relentless form for the past one year, surging by an incredible 4-fold to smash a record high of US$120 per troy ounce on 29 January 2026.

Obviously, what goes up will come down. The rapid decline of silver price vindicated my belief that big boys have been manipulating the market. Although I am convinced at the long-term potential of gold and silver as safe haven, I am skeptical of silver price’s recent explosive runs. This is the reason why I have not entered the market till now.

https://sgwealthbuilder.com/2026/01/31/silver-price-crashed-into-sea/

Actually I have a big position in gold, and in hindsight I regret not buying silver in 2025. It’s the same BTC ETH logic. Once you see BTC (gold) going up in a bull run, you know that will flow over to ETH (Silver) eventually.

That said, with the recent selloff would I add? Gives me a second bite at the cherry, but the recent price action for silver is brutal and suggests the sell-off has not stabilised (yet). Not made up my mind, will monitor the price action.

the average trading volume of SGD150m dont look right. It is probably doing close to SGD1-1.5bn …likely much more in Jan 2026

This makes the liquidity argument from the EQDP funding looks weak.

What will make this more durable is perhaps the drive towards corporate reform creating value from divestment, return of capital, higher ROE etc etc

Good point, I probably underestimated the numbers somewhat. That being said I think the fund managers will still reach the same conclusion that the same few stocks are worth holding. All this liquidity chasing a handful of stocks can make a big move (just like we saw with the 3 local banks).

Hi FH,

https://sgwealthbuilder.com/2026/02/04/ifast-share-price-at-mount-everest/

The view from the top of the mountain must be surreal. iFAST share price captured the imagination of Singapore investors yet again as the counter smashed to a record high of $10.40 in recent days. For the past one year, iFAST share price has surged by an incredible 42%.

Question now is whether iFAST share price is at the cusp of a rally or have reached the peak of Mount Everest. Investors could be forgiven for being sceptical at the sustainability of iFAST share price as the counter has enjoyed similar run in 2020 – 2021 period, only to crash spectacularly within a year. There are certainly similarities between the past and current rallies. And then, there are also things that have changed that could define whether iFAST share price could continue charging forward to hit a new high of $20.

https://sgwealthbuilder.com/2026/02/04/ifast-share-price-at-mount-everest/

iFast did selloff to 9.6 this week though. Are you bullish on FSM mid term?