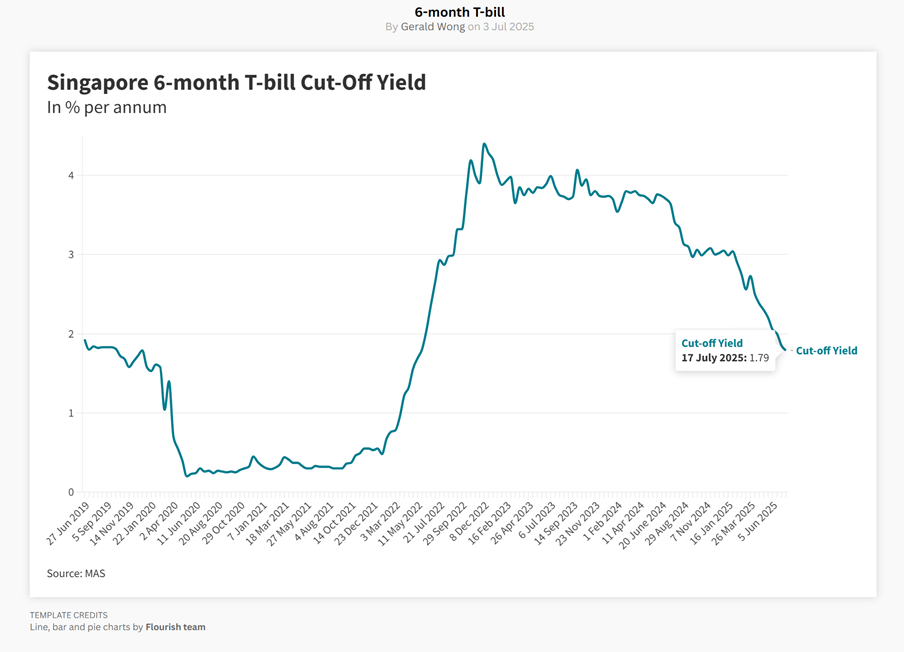

I’ve been getting a lot of questions on where to park cash for yield, given the sharp drop in Singapore interest rates.

After all, the latest 6-month T-Bill yields fell to 1.79%, which is a far cry from the 4%+ we saw in late 2022.

In this environment, REITs start looking pretty attractive again.

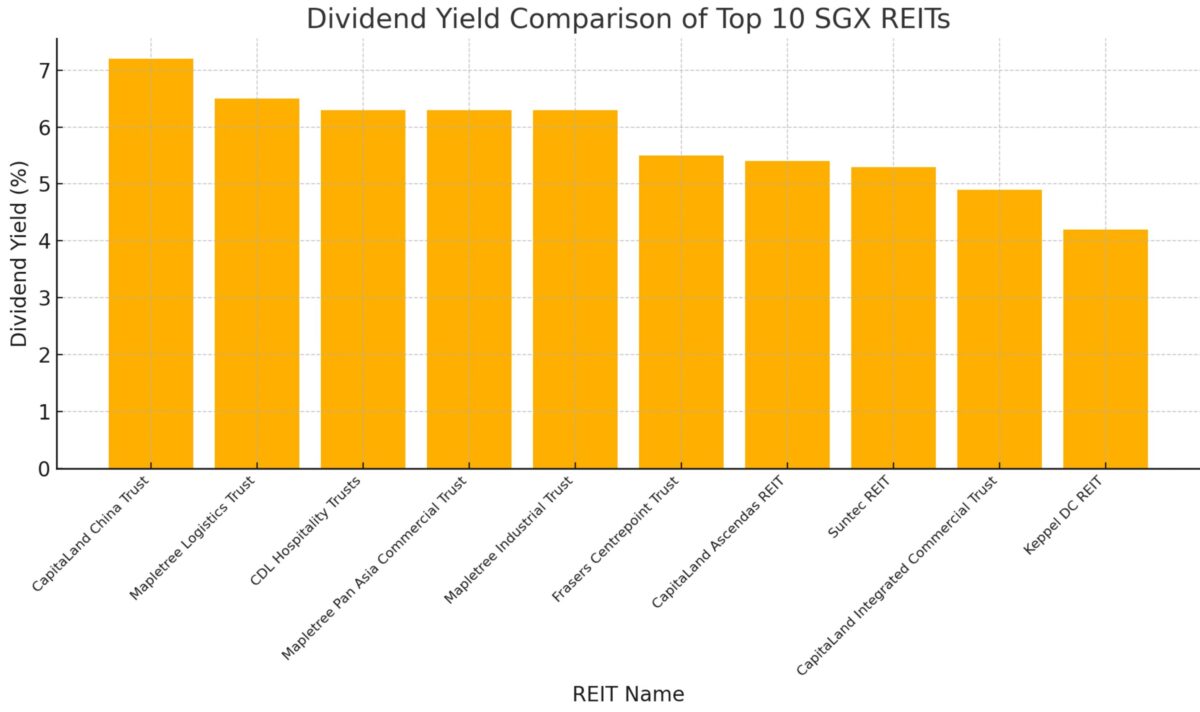

And with the help of AI, I compiled a list of the Top 10 highest dividend yield SGX blue-chip REITs below.

And I wanted to take some time to go through the list, and discuss which of these REITs I would consider buying for my own portfolio today.

Highest-yield SGX blue-chips REITs — ranked (close 23 July 2025)

All ten counters are large-cap, SGX-listed S-REITs backed by investment-grade sponsors (think CapitaLand, Mapletree etc).

Here’s the full list (in picture form):

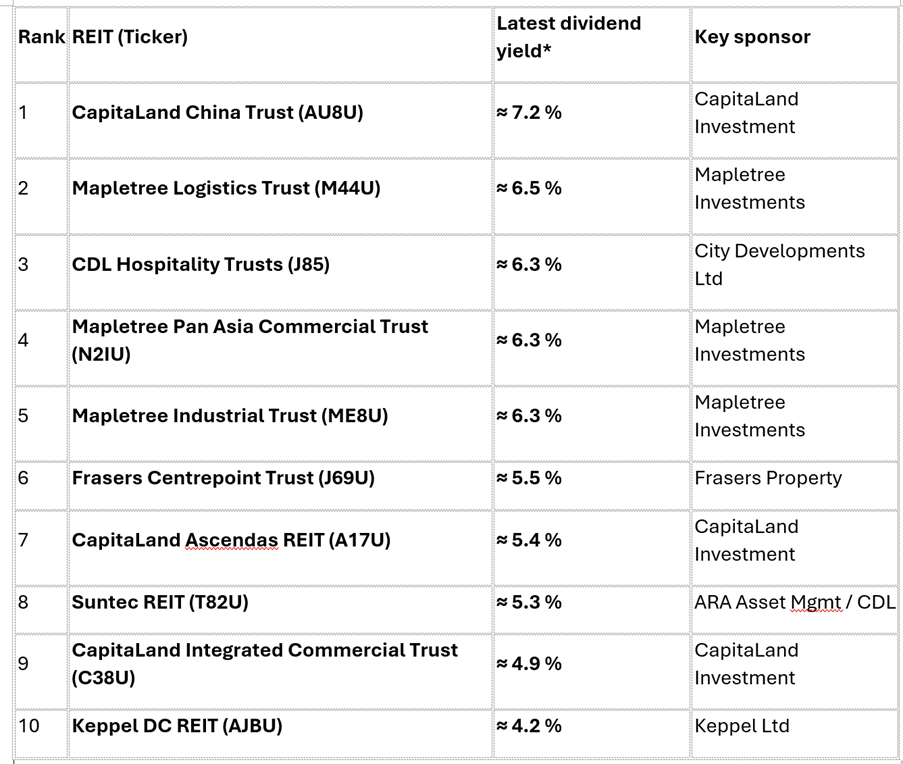

And in text form:

| Rank | REIT (Ticker) | Latest dividend yield* | Key sponsor |

| 1 | CapitaLand China Trust (AU8U) | ≈ 7.2 % | CapitaLand Investment |

| 2 | Mapletree Logistics Trust (M44U) | ≈ 6.5 % | Mapletree Investments |

| 3 | CDL Hospitality Trusts (J85) | ≈ 6.3 % | City Developments Ltd |

| 4 | Mapletree Pan Asia Commercial Trust (N2IU) | ≈ 6.3 % | Mapletree Investments |

| 5 | Mapletree Industrial Trust (ME8U) | ≈ 6.3 % | Mapletree Investments |

| 6 | Frasers Centrepoint Trust (J69U) | ≈ 5.5 % | Frasers Property |

| 7 | CapitaLand Ascendas REIT (A17U) | ≈ 5.4 % | CapitaLand Investment |

| 8 | Suntec REIT (T82U) | ≈ 5.3 % | ARA Asset Mgmt / CDL |

| 9 | CapitaLand Integrated Commercial Trust (C38U) | ≈ 4.9 % | CapitaLand Investment |

| 10 | Keppel DC REIT (AJBU) | ≈ 4.2 % | Keppel Ltd |

*Yields use the most recent forward or trailing-12-month distribution per unit divided by the latest traded price (22 July 2025 close). Prices – and therefore yields – move daily, so treat these figures as snapshots rather than fixed coupons.

Quick takeaways

- Yields north of 6 % cluster around the Mapletree and CDL names. These sponsors have kept gearing moderate while still delivering steady DPU growth.

- Don’t chase yield in isolation. Check leverage, interest-coverage ratios, and upcoming refinancing before deciding that an extra 50 bp is worth the risk.

Top 10 highest dividend yield REITs on SGX – Which would I buy? 5% dividend yield minimum?

What does ChatGPT think is the best buy?

So I decided to ask ChatGPT which of the 10 REITs does it think is the best buy?

Here’s the answer:

| Pick | Why now? | Ideal holding lens |

| Mapletree Logistics Trust (MLT) | Rare combo of near-7 % yield and 96 % occupancy backed by secular e-commerce logistics demand. Sponsor still buying assets at 5–6 % NPI yields → accretive once debt costs normalise. | Income core; drip into weakness, hold 5+ yrs. |

| Mapletree Industrial Trust (MIT) | You’re paying mid-6 % for a half-data-centre landlord—cheapest “AI infrastructure” exposure on SGX. Ongoing non-core disposals recycle capital into higher-margin U.S. hyperscale assets. | Growth & income; accumulate before next DC acquisition. |

| CapitaLand Ascendas REIT (CLAR) | Lower headline yield, but fortress balance-sheet and diversified tenant base position it to scoop distressed industrial deals as smaller players refinance. | Safety play; buy-the-dip candidate on rate scares. |

| Keppel DC REIT (KDC) | A pure play on Asia’s surging data-centre demand; Maybank just slapped a fresh “buy” on it citing AI workload migration tailwinds. Debt headroom ample after 2024 equity raise. | High-conviction growth; expect volatility but double-digit DPU CAGR potential. |

What do I think is the best buy?

You know what – I actually disagreed with Chatgpt on this one.

The way I see it.

If I buy REITs today, I am using them primarily as a bond proxy.

As a way to get higher income / yield on a low risk bond like instrument.

If I really wanted to take on risk, I would probably be buying equities instead for the higher upside potential – not REITs.

Because of that, I actually prefer to stick primarily to blue-chip REITs that hold primarily Singapore real estate today.

Simply because to me that’s just the lower risk play in this market.

And then with my risk portfolio, I buy stuff like US tech stocks, crypto, China and so on.

With that in mind, which of the Top 10 blue-chip REITs would I consider buying?

With that in mind?

Looking at the list of REITs below?

That ones that caught my eye are bolded below.

Frasers Centrepoint Trust, CapitaLand Ascendas REIT, and CapitaLand Integrated Commercial Trust.

Those I can see myself buying.

| Rank | REIT (Ticker) | Latest dividend yield* | Key sponsor |

| 1 | CapitaLand China Trust (AU8U) | ≈ 7.2 % | CapitaLand Investment |

| 2 | Mapletree Logistics Trust (M44U) | ≈ 6.5 % | Mapletree Investments |

| 3 | CDL Hospitality Trusts (J85) | ≈ 6.3 % | City Developments Ltd |

| 4 | Mapletree Pan Asia Commercial Trust (N2IU) | ≈ 6.3 % | Mapletree Investments |

| 5 | Mapletree Industrial Trust (ME8U) | ≈ 6.3 % | Mapletree Investments |

| 6 | Frasers Centrepoint Trust (J69U) | ≈ 5.5 % | Frasers Property |

| 7 | CapitaLand Ascendas REIT (A17U) | ≈ 5.4 % | CapitaLand Investment |

| 8 | Suntec REIT (T82U) | ≈ 5.3 % | ARA Asset Mgmt / CDL |

| 9 | CapitaLand Integrated Commercial Trust (C38U) | ≈ 4.9 % | CapitaLand Investment |

| 10 | Keppel DC REIT (AJBU) | ≈ 4.2 % | Keppel Ltd |

What about the other REITs on the list?

Let me share some high level thoughts below.

China / HK exposed REITs

CapitaLand China Trust and Mapletree Logistics Trust – those have big China / HK exposure.

And frankly I’m just not super excited about China real estate at the moment. The oversupply in the China market, that’s going to take years to work off, during which time this could be dead money.

Better to look elsewhere for now, and if I really wanted China exposure I would focus more on consumer, tech or advanced manufacturing plays.

Hong Kong real estate – I don’t need to tell you about all the structural difficulties facing Hong Kong real estate today and how much cheaper and better it is just to go to neighboring Shenzhen.

Mapletree Pan Asia Commercial Trust on the other hand is in a weird place.

I hate the Hong Kong exposure for MPACT, but I love the best in class Singapore exposure (Vivocity and Mapletree Business City).

Because of that I have a position in MPACT, but frankly I do think the Hong Kong exposure will cap the upside potential.

Data Centre REITs

Mapletree Industrial Trust – I’ve never been a big fan of MIT ever since they went heavily into US data centres.

US real estate is a tough market to compete it, and real estate is a local business.

Just didn’t see the advantage that Mapletree can bring to the table.

I mean it’s probably a decent buy, but I exited most of my position in MIT shortly after that announcement.

Keppel DC REIT on the other hand – now that’s a REIT I really like.

Singapore Data Centres are a very scarce asset class, and I added heavily during the sell-off in late 2024 after the bankruptcy of the Guangzhou tenant.

But at today’s price and a 4.2% yield?

I thought it was pretty fully valued so I took profits in this REIT, and I no longer hold a position today.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

Any other REITs not on the list that I like?

A big one that I liked, but wasn’t on this list?

Starhill Global REIT.

Yes I know it’s not the most sexy REIT out there.

But at almost 7% yield, holding pretty decent property in Ngee Ann City and Wisma Atria (forming 50% of the portfolio).

It’s one of those fly under the radar REITs that I really liked.

Keppel REIT and Lendlease REIT too.

I mean again both have their own pros and cons, but worth considering as well.

You can see my full REIT watchlist, and my target pricing, on FH Premium.

Outlook for REITs the next 12 – 24 months?

One last point that we haven’t exactly touched on in this article.

The outlook for REITs going forward?

I asked ChatGPT o3, and this was the answer:

“12-to-24-month sector outlook

- Rates backdrop finally tilting benign. Economists now see the Fed cutting once or twice by end-2025, with the July FOMC expected to hold. MAS in April signalled a slower S$NEER appreciation path, a subtle ease that lowers local funding costs.

10-year SGS yields have already slipped to ~2.1 %, their lowest since early 2022. - Inflation looks tamed. Core CPI is tracking 0.6 % y/y, the softest in three years, giving MAS room to stay accommodative.

- Fundamentals improving:

- Industrial & logistics: tight supply pipelines and positive rental reversions persist (MLT 96 % occupancy)

- Data-centre: hyperscaler AI demand is accelerating; Keppel forecasts >60 % of AI workloads moving to large clouds by 2030.

- Retail & hospitality: suburban malls steady; tourist arrivals closing in on pre-Covid highs, lifting hotel RevPAR (CDLHT).

- Headwinds remain:

- Gearing for some names (Suntec, MPACT) sits above 40 %, limiting acquisition capacity.

- China sentiment is a swing factor for CCRT and MPACT.

- Office supply glut in SG CBD and HK could cap rental upside.

Base-case view:

With funding costs peaking and asset values largely “marked-down”, the sector should transition from rate-pressure to earnings-grind mode. Expect mid-single-digit DPU growth for the better-capitalised REITs and modest re-rating (50-100 bp cap-rate compression) as safe-yield differentials over SGS bonds widen again.

Bottom line: 2024 was about surviving higher rates; 2025-26 looks set to reward the landlords that kept leverage in check and leaned into structural tailwinds like logistics and data-centres.”

My personal views on REITs?

You know what?

I generally agree with the big picture view from ChatGPT.

Market is pricing in a lot of interest rate cuts from the Feds (assuming that Trump is going to replace Jerome Powell with someone who delivers on rate cuts).

And look at that drop in Singapore 10 year yields.

From 3.5% this time in 2024, to 2.0% today.

That’s just a stunning drop in interest rates – which if this keeps up, is going to be a powerful boost for REITs (both from lower financing cost, and as a bond proxy).

This has indeed led to a rally in REITs so far, but as you can see from the chart below.

The rally in REITs is nowhere near the same level as the drop in interest rates above.

Which means that if rates continue to stay low, there could be upside especially for REITs that show stable / growing earnings.

My thoughts on REITs today? What would I buy?

You can see my full personal portfolio on FH Premium.

The way I think of REITs today.

I just think of them as an alternative to bonds, with daily mark to market pricing, and without a maturity date (more like a bond fund that continually rolls).

Because of that, I stick mainly to low risk blue-chip REITs from a strong sponsor, with a strong balance sheet, and holding primarily Singapore real estate.

And I see that as part of my cash/yield portfolio – sitting on the high risk end opposite from risk free T-Bills/fixed deposit/Singapore savings bonds.

Which I want to keep generally low risk, yet generating a decent blended yield.

And then on the other hand of the barbell I will have my risk portfolio.

Stuff like US tech stocks, Singapore stocks, China stocks, crypto and so on.

Which I count on to deliver the real returns.

On that basis I really don’t need to take a lot of risk with REITs, I just want a slightly higher yield than the risk free rate, without taking on too much risk.

And on that basis, I think REITs are still a pretty decent buy today, even after the rally in prices – simply because interest rates have fallen so much.

But hey that’s just me, and I would love to hear what you think.

As always, you can see my full personal portfolio, and my full stock / REIT watchlist, on FH Premium.

Unlock Your Financial Edge with FH Premium

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea.

Hi FH

Why not OUE Reit, which has 100% exposure to Singapore? The reit under its current CEO (appointed in Feb 2022) had obtained a credit rating sometime back to lower its interest cost and divested its China property last year.

Thanks

Thanks

Personally not the biggest fan of OUE. But if you like the REIT, don’t let me stop you!

Maybe not overthink & CFA at 5.8%

Fair enough – works perfectly too!

ChatGPT actually makes for a scarily good investment analyst…

I find it can do 80% of the heavy lifting. But the last 20% of judgment – you still need to do it yourself.

FH, the RTS link is going to badly affect local retail significantly. How will that impact your picks, i.e., Starhill, Lendlease, Frasers Centrepoint and CICT?

Is it confirmed the RTS link will impact local rents significantly? I think the jury is still out on that one. In any case real estate goes goes back to first principles – buy high quality real estate in good locations. with as big a margin of safety as you can.