As you guys have probably heard by now.

UOB One Account’s interest rates will be dropping once again.

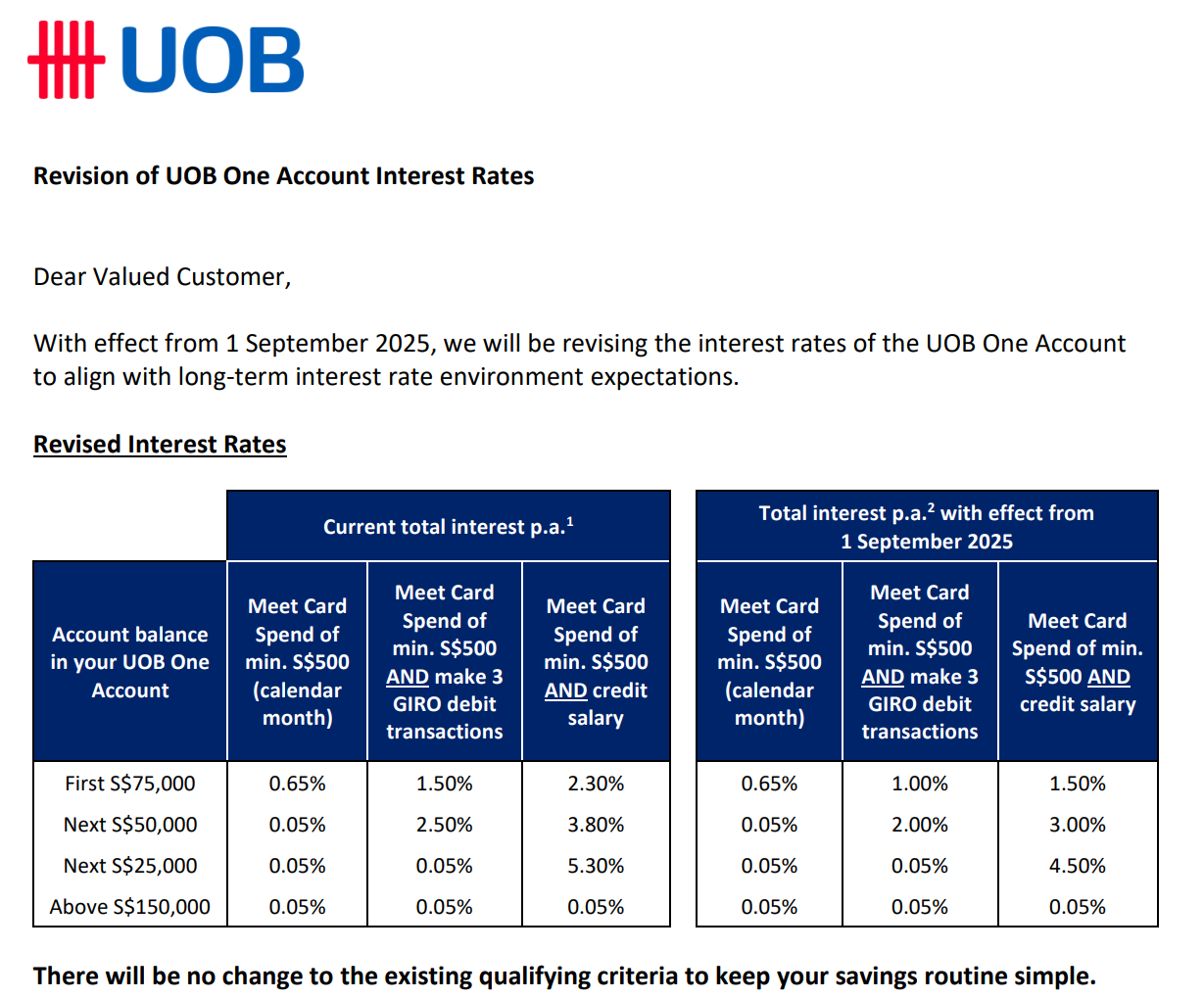

From 1 Sep 2025, UOB One’s max effective interest rate (EIR) drops to 2.5% if you hit $500 card spend + salary credit, with weaker tiers below that.

Given that most of us (myself included) park the max $150,000 in UOB one for the higher interest yield.

I wanted to take some time out to discuss this nerf, and whether it would make sense to park cash in a mix of SGD money market funds (MMFs) + fixed deposits (FDs) + selective T-bill/SSB ladders vs parking everything in UOB One.

What exactly changed? UOB One drops effective interest rates to 2.5%

UOB has nerfed the One Account rates yet again:

I ran the numbers to compute the effective interest rates – both before and after:

| Balance tier | New: spend $500 + salary | Effective Interest Rate (New) | Effective Interest Rate (Old) |

| First $75k | 1.50% | 1.50% | 2.30% |

| Next $50k | 3.00% | 2.10% | 2.86% |

| Next $25k | 4.50% | 2.50% | 3.21% |

| > $150k | 0.05% |

Long story short:

- Max effective interest rate (EIR) falls from ~3.3% to ~2.5% (requires $500 eligible spend + ≥$1,600 salary credit; cap $150k).

- Meet only spend + 3 GIRO? Your EIR on $125k is about ~1.4% now.

- Meet only spend? ~0.65% on $75k.

- Criteria are unchanged (card spend $500; salary credit via accepted channels).

Bottom line: It’s another nerf to a popular “do-everything” cash hub.

The real question: should UOB One still be your main cash park?

Because this is a fairly big nerf.

I would say UOB One is no longer a must use – and other options become a lot more competitive.

I would say keep with UOB One if (a) you already route salary there and (b) you value one-account convenience for bills, GIROs and cards.

Otherwise, there are better risk-adjusted homes for surplus cash today.

Let’s compare by risk, liquidity and realistic net yield.

Your menu of cash options (as of mid-Aug 2025)

Head-to-head: UOB One vs alternatives (today’s snapshot)

| Option | Indicative yield today | Liquidity | Insurance | When it’s best |

| UOB One (spend + salary) | Up to ~2.5% EIR on first $150k | Daily | SDIC (only $100k per bank) | If you want one-account convenience & already salary-credit there |

| SGD Money Market Funds (MMFs) | ~2.0%–2.7% gross (net slightly lower) | T+0/T+1 | No SDIC | Flexible core for idle cash; daily accrual |

| Fixed Deposits (FDs) (6–12m) | ~1.5%–2.45% | Locked | SDIC | For certainty; ladder across banks/tenors |

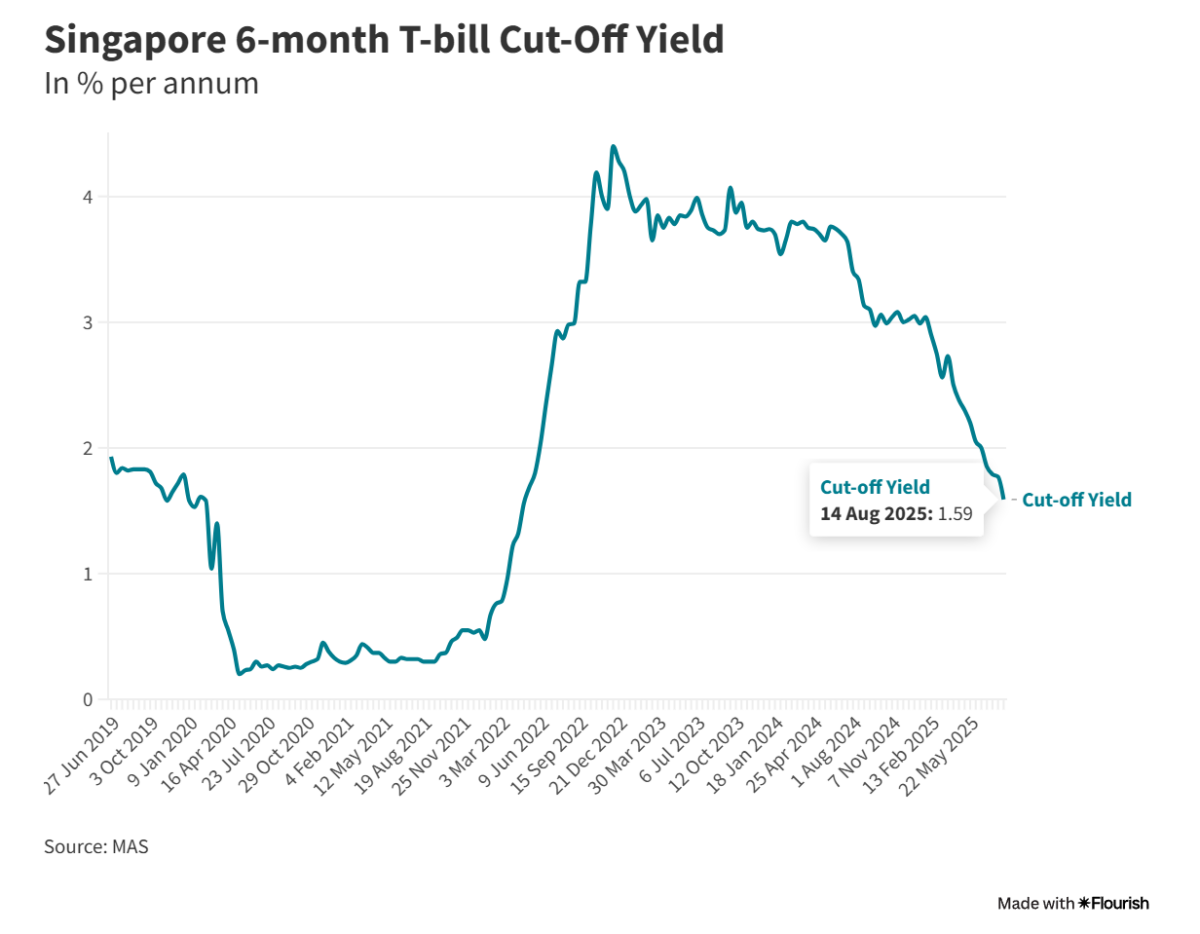

| 6-m T-bill | ~1.77% (last cut-off) | Locked | Gov’t | Ladder if auctions pay a premium vs MMFs/FDs |

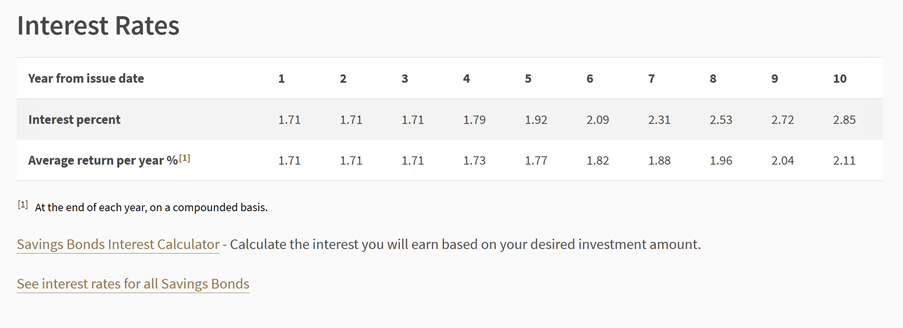

| SSB (Sep 2025) | 1-yr ~1.7%; 10-yr avg ~2.1% | Monthly redeem | Gov’t | Long emergency fund / rate-lock optionality |

Yields are indicative and move with market rates.

1) SGD Money Market Funds (MMFs) — my workhorse pick for idle cash

- Indicative yield: roughly ~2.0%–2.7% gross across the largest SGD cash/MMF products. Net yield is slightly lower after fees. Yields float with interbank/SORA.

- Liquidity: typically T+0 / T+1 depending on platform.

- Risk/coverage: Unit trust risk investing in short-dated deposits/bills; not SDIC-insured.

- Why I like it now: Daily accrual, easy in/out, and currently beats UOB One’s 1.5% on the first $75k if you don’t (or can’t) salary-credit. If rates keep easing, MMF yields will drift—but so will bank account rates.

Reality check: MMFs aren’t fixed; yields can slide further if the rate-cut cycle accelerates. I use MMFs as the liquid core, then layer FDs/T-bills for certainty.

2) Fixed Deposits (FDs) — certainty at the cost of flexibility

- Indicative promos (Aug 2025): roughly ~1.5%–2.45% depending on bank and tenor.

- Liquidity: Locked till maturity (break costs apply).

- Risk/coverage: SDIC-insured up to $100k per depositor per bank.

Where FDs fit: If you can lock 6–12 months and want fixed certainty, they complement MMFs nicely. On current quotes, top FDs can beat UOB One’s weighted average if you can’t meet salary+spend.

3) 6-month T-bills — risk-free but yields have rolled over

- Latest cut-off (end-Jul 2025): about ~1.77%.

- Liquidity: Technically tradeable, but retail secondary liquidity is thin; assume hold-to-maturity.

- Risk: Singapore Government credit.

Where T-bills fit: Great to ladder term certainty (especially if you won’t need the cash for 6 months). At recent levels, they don’t clearly beat MMFs or the best FDs—so bid only if the auction premium looks attractive that week.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

4) Singapore Savings Bonds (SSBs) — flexible 10-year parking with step-up

- Latest issue (Sep 2025): 1-yr ~1.7%, 10-yr average ~2.1%. Redeemable any month at par + accrued interest; $2 fee.

- Use-case: Long-dated rainy-day fund with optionality. If you think rates trend lower into 2026, locking some 10-year ladder now has value—even if the 1-year is meh.

5) CPF top-ups/transfers (not “cash”, but worth a mention)

- OA: 2.5% floor; SA/RA/MA: 4% floor (currently extended through end-2025).

- Trade-off: Excellent risk-free yield, but note the lock-up period. Use only for funds you can accept the lock-up period.

6) USD MMFs (optional diversifier)

- Indicative yields hover around ~4% on large USD government MMFs, but FX risk dominates the decision. Sensible if you already spend/invest in USD or want USD dry powder.

Where I would park my cash today?

I split it up into a couple of options below.

A) You want max convenience (one main bank, minimal admin, maximum yield) – Probably what I would do

If you already credit your salary into UOB One today, and have no problems hitting the $500 monthly card spend.

And you have $150,000 lying around.

Then I would say stick with UOB One, as 2.5% effective interest rate on cash you can withdraw any time is still unbeatable in this market.

The risk of course is that if interest rates continue falling, the UOB One may see a further cut in interest rates, so you can mix in some 6 – 12 month Fixed Deposits or Singapore Savings Bonds to lock in some yield.

And anything above $150,000, I would probably park in a SGD money market fund for liquidity.

If you’re comfortable with some risk + duration, bond funds, REITs, can be considered too.

B) You want higher yield with flexibility – or don’t want to jump through hoops for a savings account

But note that UOB One only makes sense if you hit the $500 monthly spend and credit your salary, and hit the full $150,000.

If you don’t fulfil either, the effective interest rate drops drastically, and I don’t think it’s that attractive anymore.

| Balance tier | New: spend $500 + salary | Effective Interest Rate (New) | Effective Interest Rate (Old) |

| First $75k | 1.50% | 1.50% | 2.30% |

| Next $50k | 3.00% | 2.10% | 2.86% |

| Next $25k | 4.50% | 2.50% | 3.21% |

| > $150k | 0.05% |

If that is you, then I would probably:

- Core: Park the bulk in SGD MMFs via your preferred platform.

- Add certainty: If a bank runs a good promo (≥2.2% for 6–12m), ladder FDs across two banks.

- Optional: Bid T-bills or Singapore Savings Bonds only when auction yields look competitive vs your MMF/FD blend – as a way to lock in some yields.

Why: You get near-daily liquidity and generally better net yield than UOB One’s first tier, without fiddling with bank rules.

C) You want optionality over many years

- Build/maintain a Singapore Savings Bonds ladder (monthly slots) to lock a portion of 10-year yield (even if it’s just ~2.1% now).

- Keep 3–6 months of expenses in MMFs for liquidity, and use FDs tactically.

Why: If rates fall further in 2026, you’ll be glad part of your cash is locked at higher coupons with penalty-free monthly redemption.

FAQs on UOB One Account’s drop in interest rates

For those of you with questions on UOB One Account’s drop in interest rates, I set out my thoughts on the more common questions below:

1) Is UOB One Account “bad” now?

Not “bad”—just less special. If you won’t salary-credit or don’t want to juggle GIROs, ~0.65%–1.4% on large balances is hard to justify.

If you do salary-credit and like the One Card ecosystem, ~2.5% on $150k is fine for a set-and-forget hub—but it’s not the highest cash yield around.

2) Are MMFs safe?

They’re designed for capital stability (short-dated deposits/SG bills), but they are unit trusts—not SDIC-insured and not principal-guaranteed.

Across cycles, drawdowns have been tiny versus bond/equity funds.

Stick to the big houses and keep it simple, and it should be low risk.

But just to be clear, Money Market Funds are not risk free.

3) Why not just buy T-bills?

At ~1.77%, recent 6-month T-bills don’t decisively beat the better MMFs/FDs. If auction yields rebound, sure—ladder them.

Otherwise, you’re trading flexibility for a similar (or lower) return.

4) Should I max SSBs now?

I’d fill some quota if you have none, but pace yourself—new tranches every month.

If projections keep slipping, you can ladder gradually rather than all-in at ~2.1%.

What would I do? Deciding whether to use UOB One or not? (FH’s simple plan)

Decide if you will salary-credit at UOB One, and will spend $500 a month.

Yes: Keep it as your daily-use hub, and cap $100k if SDIC coverage matters to you. If you want the full ~2.5% on $150k, accept that $50k is uninsured.

No: Treat UOB One as a transactional shell (~0.65% is a rounding error). Move surplus to the blend below.

Build a two-bucket cash stack:

Bucket A (liquid core): SGD MMFs for daily access; target 2–6 months of expenses + near-term plans.

Bucket B (term certainty): FDs (6–12m) where promos are good; top up with T-bills only if auction yields beat your MMF/FD blend.

Optional long-term ballast:

SSB ladder a fixed monthly amount to lock some 10-year yield with penalty-free monthly exits. Don’t chase—just ladder.

If comfortable with some risk and duration, consider higher risk options like bond funds or REITs (but note not risk free).

Review quarterly.

Cash products move with policy rates. If MMF yields slide below good FD promos, roll more into FDs. If T-bill auctions pop back up, ladder them. Keep the hub account for bill-pay and card rewards—not for warehousing every dollar.

This post is written on 15 Aug and will not be updated going forward.

For my latest macro views, and what I am buying/selling, check out FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).