In last week’s FH Premium article on the US-Iran situation, I wrote that the chances of a US attack on Iran is higher than the markets may be expecting.

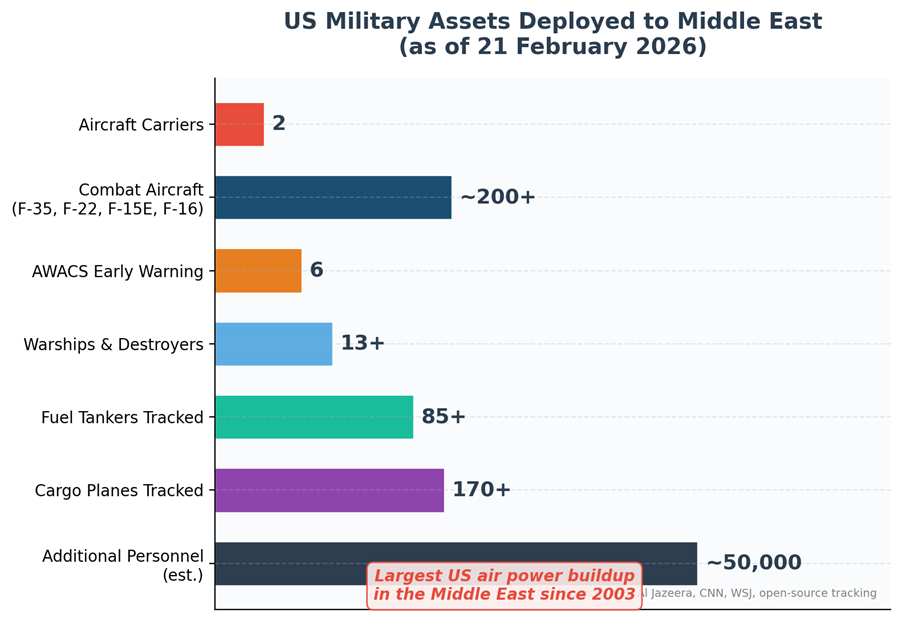

For the simple reason that the US has amassed significant military assets in the area — including not just 2 carrier groups but also crucially logistical support infrastructure required to sustain a prolonged air campaign, and anti-missile capability required to defend against any Iranian response.

Which goes beyond what you need for a bluff.

Well, that unfortunately turned out to be the case because over the weekend we saw US-Israel airstrikes against Iran.

I know many of you have asked for my views on the software sell-off, but I figured the Iran situation is the more urgent one (I will write on software separately).

In this article I wanted to discuss:

- Latest update on the US-Israel-Iran war

- How this likely evolves going forward?

- What this means for markets? And how I will position my portfolio?

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Latest update on the US-Israel-Iran war

On Saturday – Trump announced that the US had launched “major combat operations” in Iran alongside Israel. The US aimed to destroy Iran’s ballistic missile and nuclear programs, while Israel targeted political and military leaders.

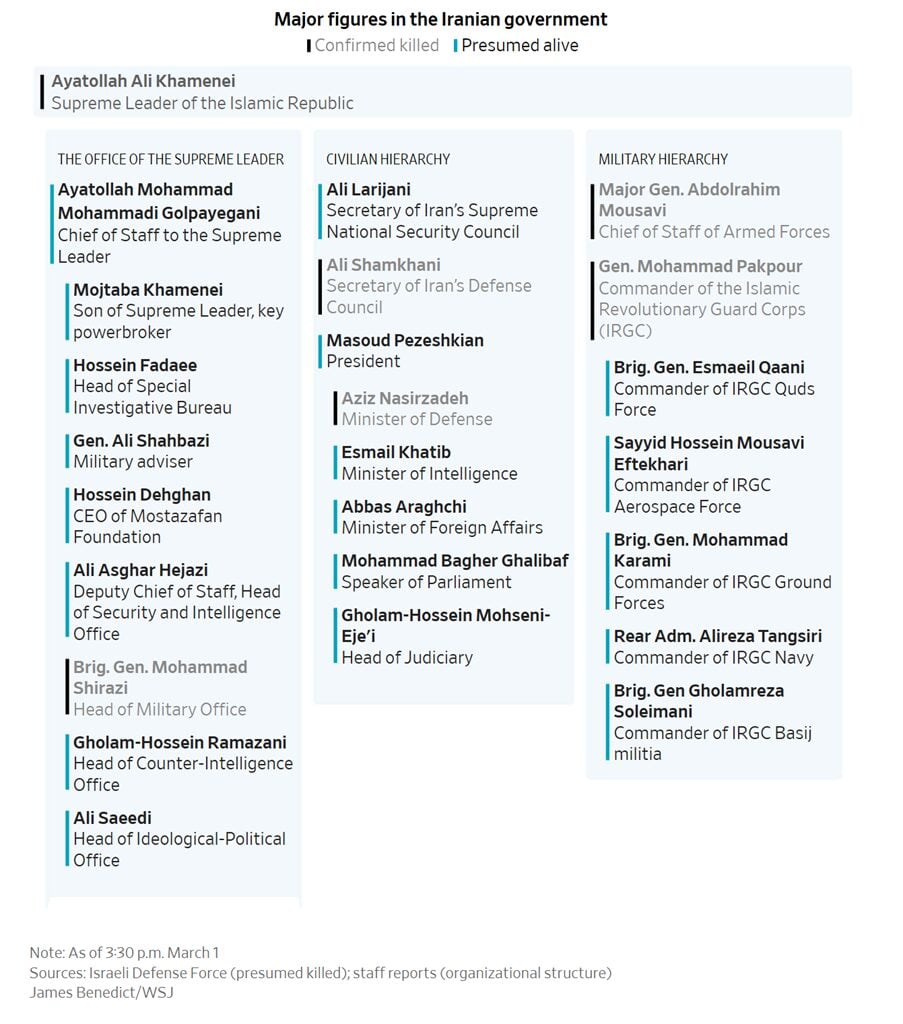

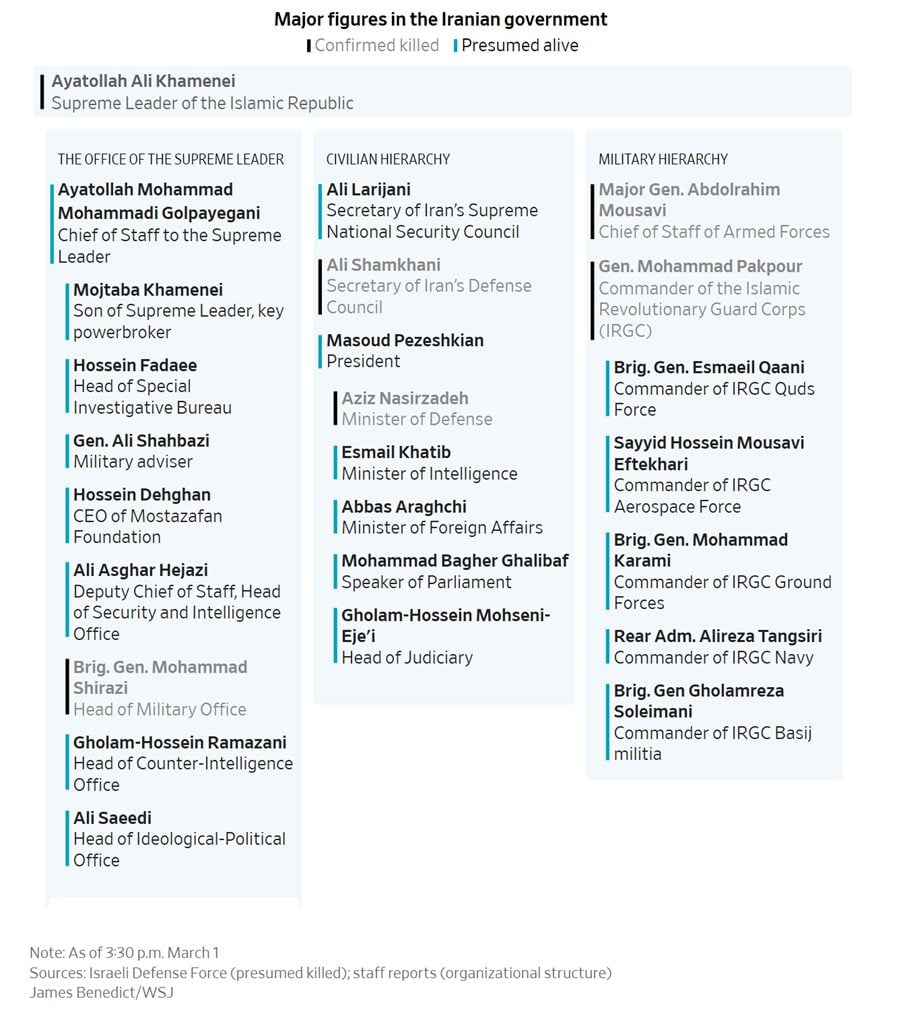

Decapitation achieved. Iranian state media confirmed the death of Ayatollah Ali Khamenei, killed in the opening strikes on his compound in Tehran. An airstrike on a meeting of Iran’s defence council killed the army chief of staff, the defence minister, the IRGC commander, and security adviser Ali Shamkhani. CBS News reported that approximately 40 Iranian officials were killed.

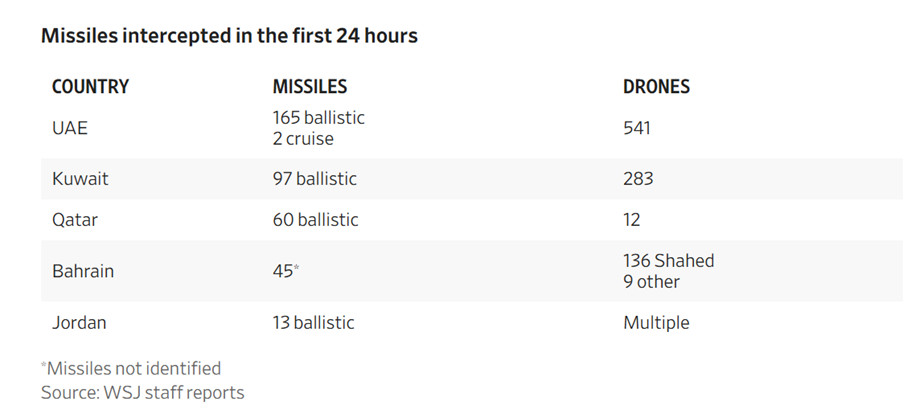

Iran is retaliating broadly. Iran launched missiles and drones toward Israel, UAE, Qatar, Kuwait, Bahrain, Jordan, and Saudi Arabia, including strikes on the US Fifth Fleet headquarters in Bahrain and civilian airports in Kuwait and the UAE. The IRGC has pledged the “most ferocious” operation in history. Iran also struck British military bases in Cyprus.

What Has Changed in the Last 24 Hours – the Conflict Has Escalated, Not Stabilised

Unfortunately, this has only escalated in the past 24 hours.

US CENTCOM confirmed it has struck more than 2,000 targets in Iran in two days, including ships, submarines, missile sites, communications links, and IRGC command-and-control centres. This is a full-spectrum degradation campaign, not limited strikes.

Trump told the New York Times the operation could continue for four to five weeks and that it “won’t be difficult” for the US and Israel to sustain the bombardment.

US casualties confirmed. CENTCOM confirmed three American service members killed and five seriously wounded. Trump told the New York Times he expects “quite a bit higher” casualties based on Pentagon projections.

Iran’s Retaliation is Broader Than Any Prior Scenario

Iran is striking across the entire region simultaneously:

- Israel: Iranian missiles hit residential buildings in Beit Shemesh, killing six Israeli civilians and wounding 23.

- Gulf States: Explosions heard in Dubai, Abu Dhabi, and Doha. The Port of Jebel Ali in Dubai was struck. Dubai International Airport had 70% of flights cancelled — 747 flights in a single day.

- US Bases: Iran targeted facilities in Bahrain (Fifth Fleet HQ), Qatar, Kuwait, Jordan, and Iraq. Two drones targeted US Victory Base near Baghdad International Airport.

- Lebanon: Hezbollah has officially entered the conflict, launching rockets at Haifa and the Upper Galilee. Israel declared it “an official declaration of war by Hezbollah.” This opens a second front.

The Strait of Hormuz Is Effectively Closed (for now)

This is the critical development for markets. While Iran has not issued a formal legal closure, the operational reality is that the Strait is shut:

No traceable passings by major crude tankers through the Strait of Hormuz since Saturday night. Only 19 total vessel transits on Sunday, compared to the daily average of 107 cargo-carrying vessels. 90% of Sunday’s transits were eastbound (i.e., vessels leaving the Gulf, not entering).

At least three tankers have been struck by missiles or drones. The Joint Maritime Information Center found “no association that would make these vessels a viable candidate for targeting,” meaning merchant ships of any flag now face indiscriminate risk. JMIC elevated the regional threat level to CRITICAL — its highest classification.

Steamship Mutual issued a formal Notice of Cancellation of War Risks coverage for the Persian/Arabian Gulf, effective 72 hours from 0000 GMT on March 1. Without war risk insurance, most commercial operators cannot legally sail.

Hapag-Lloyd has suspended all vessel transits through the Strait. CMA CGM ordered all vessels to shelter, suspended Suez Canal transits, and is rerouting via Cape of Good Hope. MSC instructed all Gulf-region vessels to proceed to safe shelter areas.

At least 150 tankers, including crude oil and LNG vessels, have dropped anchor in open Gulf waters beyond the Strait.

Iran’s semi-official Mehr News Agency reported that a tanker struck Sunday after attempting “unauthorized passage” through the Strait was sinking. This is a direct warning shot at any vessel attempting transit.

Bottom line on Hormuz: The Strait is not formally closed, but it is operationally closed. Insurance cancellations, tanker attacks, and shipping line suspensions have achieved a de facto blockade without Iran needing to lay a single mine.

Oil infrastructure has been hit

An Iranian drone also hit Saudi Aramco’s Ras Tanura refinery – which is one of Saudi Arabia’s primary oil refining and export hubs.

So far at least, indications from Iran suggest that nothing is off limits – demonstrating a willingness to hit neighboring countries, airports, tankers in the Strait of Hormuz and oil infrastructure.

Diplomatic Channels Have Collapsed

Ali Larijani, now heading Iran’s interim leadership council, has stated that Iran “will not negotiate” with the US and refuted claims of any fresh push to resume nuclear talks.

Iran’s top official said Tehran “will not negotiate” with the US. This is a complete reversal from the Geneva talks just 12 days ago.

Pentagon briefers acknowledged to congressional staff that Iran was not planning to strike US forces unless Israel attacked Iran first, undercutting the administration’s claim of an imminent threat as justification for strikes. This is politically significant — it undermines the legal basis for the operation and strengthens the Congressional war powers challenge.

How This Evolves From Here

In last week’s article, I wrote that if war breaks out, there are 3 potential outcomes:

Tier 1: Limited Strikes

This would resemble an expanded version of Operation Midnight Hammer in 2025— targeted strikes on remaining nuclear infrastructure, missile production facilities, IRGC command nodes, and air defences. The force structure deployed supports this. Iran would likely retaliate with ballistic missiles against US bases in the Gulf (as it did in June 2025, striking Al Udeid Air Base in Qatar), and possibly with asymmetric actions against shipping in the Strait of Hormuz. This scenario is bounded and likely lasts days to weeks.

This is the best case outcome – and probably leads to a relief rally across markets.

Tier 2: Sustained Air Campaign

A broader campaign targeting regime infrastructure, IRGC military-industrial capacity, and potentially leadership targets (decapitation strikes). The appointment of Ali Shamkhani to head Iran’s Defence Council suggests Tehran is already preparing for this scenario. Iran’s response would be more severe — likely including attempts to disrupt Strait of Hormuz traffic through mines, anti-ship missiles, and fast-attack craft. Proxy forces in Iraq could target US personnel. This could last weeks to months.

This one is tricky for markets – much will depend on the extent and severity of the response from US and Iran.

Tier 3: Full Regional Conflagration

The highest-impact but lowest-probability scenario. This involves Iranian missile strikes on Gulf state infrastructure (oil facilities, desalination plants), a sustained closure of the Strait of Hormuz, and potential involvement of Iranian proxy networks across the region. Iran has explicitly warned that regional hosts of US forces will be targeted. The June 2025 experience showed Iran is willing to strike US bases directly. This scenario would constitute a major disruption to the global economy.

One critical variable is whether Iran attempts to close the Strait of Hormuz. The Strait handles approximately 20 million barrels of oil per day (20% of global consumption) and 22% of global LNG trade. Iran has never fully closed the Strait, though it mined it during the 1980s. The IRGC’s recent naval exercises and temporary closure of the Strait for “security precautions” on 18 February were a clear signalling exercise. IRGC Rear Admiral has confirmed the force is prepared to close the Strait if ordered. However, a full closure would also shut down Iran’s own oil exports, its primary revenue source — making it a high-cost, high-risk option of last resort.

This obviously is the worst case outcome for markets and you will likely see a broad risk-off event.

As you can see from the events over the past 48 hours, we are beyond Tier 1 now.

And we are looking at a potential Tier 2 / 3 scenario.

If you ask me, the conflict will eventually settle into one of three states:

- Ceasefire + new nuclear/security deal — the best-case market outcome. Requires a new Iranian leadership willing to negotiate. Oil returns to $60-70 or lower if Iranian sanctions are dropped.

- Sustained low-intensity conflict — ongoing drone/missile exchanges, Strait partially disrupted, elevated but not catastrophic oil prices ($85-100). Resembles a “new normal” akin to the Houthi Red Sea disruption but more consequential.

- Full regional war — Gulf state infrastructure damaged, Strait closed, energy crisis. Oil $120+. This is the tail scenario that would trigger recession in import-dependent economies (Japan, South Korea, India, China, much of Europe).

As of today, it is not immediately obvious which of the 3 outcomes we will see.

What I would add:

A couple of points I would add, which to be clear goes into speculation territory so take this with a pinch of salt:

- Better the enemy you know…

- Iranian pain threshold here is asymmetric

- Is this US’s Ukraine?

Better the enemy you know…

This one might be controversial, but I’m not sure killing Khamenei was the best idea.

All this does is to get rid of the devil you know, and open the pandora’s box on whoever takes over.

And unless US/Israel is willing to commit boots on the ground (so far signs are that they are not willing to), I’m not sure they will be able to have a whole lot of control over what happens next in terms of leadership transition.

This playbook worked well with Venezuela, but Iran is a very different country, with a 90 million+ population and a very long and rich history as the Persian empire.

Just look at how previous attempts are “regime change” in Afghanistan, Iraq etc went.

It’s not to say that this is a bad thing, it’s just that when you take out the leader like that it’s very hard to say what happens next.

Maybe you get a US friendly leader who implements freedom and democracy, but maybe you get a hardline religious leader that decides to incite a regional war.

Iranian pain threshold here is asymmetric

This is the same logic as the Russia-Ukraine war.

Ukraine (and now Iran) is fighting in their homeland, for their survival.

Which by its very nature means their pain threshold is much higher than the US.

And their timeframe is very different.

In plain English – Oil going to $100 and beyond, and a war that lasts for months / years, is not a problem for Iran because they are fighting for their survival, at home.

US, Europe, Saudi Arabia etc – can they stomach the same pain if this goes on?

Every day that this war goes on – the costs start to mount for US and the Middle East. But that doesn’t matter one bit for Iran, and in fact is what they are counting on.

Is this US’s Ukraine?

It is very, very early days.

But gun to my head?

I think the chances of the US getting sucked into a regional conflict has gone up materially with latest developments.

Just like how Ukraine has turned out to be a long, grinding war of attrition for Russia.

It would be in the interests of US’s adversaries to do the same with Iran.

The more resources that US commits to Iran, the longer that this war drags on, the more that US gets bogged down and drains its resources just like Russia in Ukraine.

Which if you’re Russian or China, isn’t too bad an outcome frankly.

Sure, maybe Trump started this with the intention of a purely air campaign.

But Iran is a very different animal from Gaza or Venezuela.

I think this could last longer and get messier than what Trump expected when he started this war.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Market Positioning — What happens next to markets?

What I wrote last week:

What would hedge a major US-Iran conflict?

Oil for one.

Gold could be another.

USD would also benefit from a safe haven bid, given the US is a net energy exporter.

But Asia as a whole will suffer because Asia is a net energy importer, and the bulk of Asian oil flows comes via the Strait of Hormuz.

Anything that is interest rate sensitive – tech stocks, REITs will probably suffer as well, as the higher inflation means less rate cuts.

To be absolutely clear – it is not certain that we are going to have a major US-Iran conflict.

But let’s take a look at each of these assets so far (these are hourly charts).

The most immediate reaction is in oil – which has jumped from $4 from $73 to $78.

To be honest, this is quite a muted response, which suggests that the market is pricing in a relatively contained conflict that is over quickly without significant damage to middle east oil infrastructure.

Gold as you would expect has jumped up on the geopolitical uncertainty, sitting around 5400 now:

Interestingly Bitcoin jumped over the weekend on initial news of bombing.

If you ask me this made sense as the initial reports on an air strike taking out top Iranian leadership, suggested that this might be a short conflict.

But as the Iranian response played out, it started to point towards a more protracted conflict – hence the mild selloff in bitcoin since then.

USD has jumped from the bid to safety – boosted by the fact that the US is a net energy exporter and therefore relatively immune to any jump in oil prices:

US 10 year yield are still relatively flat, suggesting the market is not pricing in any big pickup in inflation from higher oil prices.

US futures are pointing towards a decline, but it doesn’t look too ugly at the moment.

So… what happens next for markets? How will I position my portfolio?

My personal view – there is no point calling what happens next with a great degree of certainty, because it’s all going to come down to how the war plays out:

- Ceasefire + new nuclear/security deal — the best-case market outcome. Requires a new Iranian leadership willing to negotiate. Oil returns to $60-70 or lower if Iranian sanctions are dropped.

- Sustained low-intensity conflict — ongoing drone/missile exchanges, Strait partially disrupted, elevated but not catastrophic oil prices ($85-100). Resembles a “new normal” akin to the Houthi Red Sea disruption but more consequential.

- Full regional war — Gulf state infrastructure damaged, Strait closed, energy crisis. Oil $120+. This is the tail scenario that would trigger recession in import-dependent economies (Japan, South Korea, India, China, much of Europe).

A Scenario 1 – and any dip would be a buying opportunity. Medium term if Iranian sanctions are dropped and Iran oil enters the global market, that would lead to a sharp drop in oil prices, allowing for rate cuts. This is what Trump wants, and would be a good outcome for risk assets. He goes down as the guy who negotiated a deal with Iran and stock prices go up.

But like I said, I don’t think Iran is Venezuela or Gaza.

This is a country of 90 million people, which used to be part of the Persian empire.

If Iran doesn’t go down as easily as Trump is expecting, then you have a problem.

If on the opposite end of the spectrum we get a Scenario 3, boy we could really see a broad risk-off for risk assets.

As of today, you really cannot call which of these outcomes we will see, because it will depend on how the war evolves in the days ahead.

What I would say is that you want to be flexible and open minded to what happens next.

If indications suggest a relatively contained, low intensity conflict, I would buy the dip.

If tensions don’t boil over and start to escalate, then the outcomes start getting ugly.

At always – will share updated views on FH Premium as this develops, including my updated views on asset prices (what looks attractive and what doesn’t).

Love to hear what you think though!

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.