I’ve been getting a lot of questions on private credit.

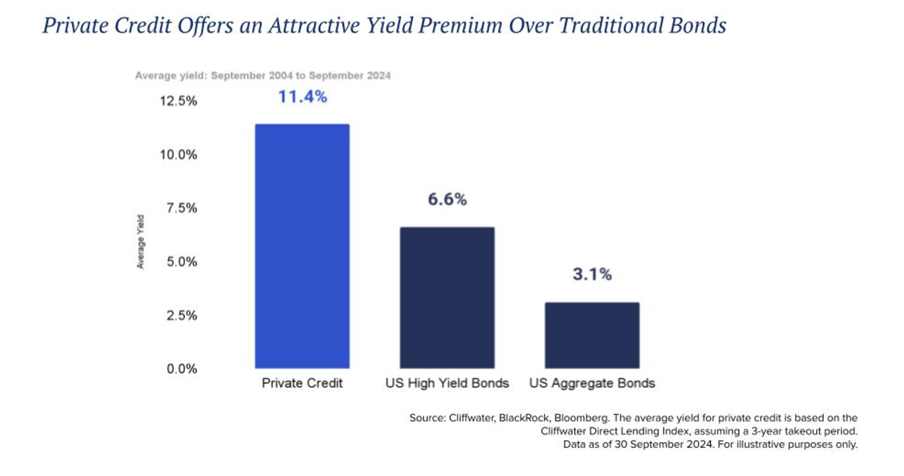

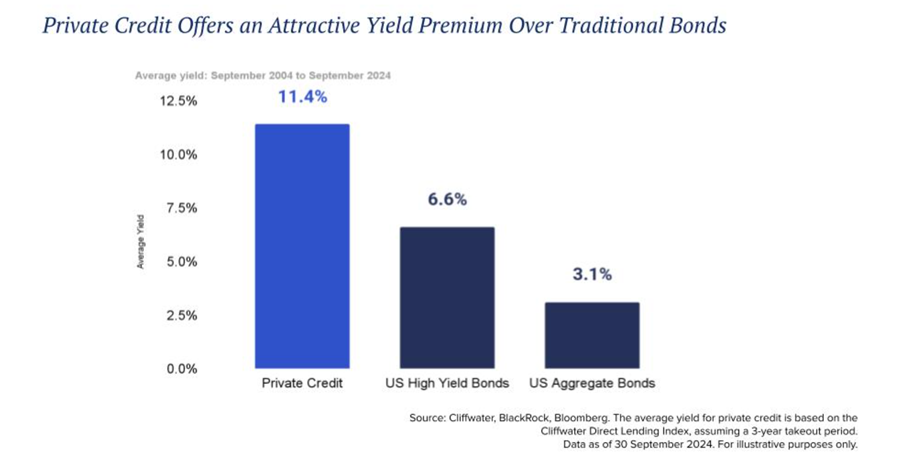

Private credit in Singapore can net 8–12%.

BUT – risk management is key.

The yield alone is meaningless, to get true returns you need to control things like seniority, cash flow, and legal enforceability—coupon alone is meaningless.

Your edge isn’t “deal flow”; it’s structure: first-lien security, real cash control, tight covenants, clear intercreditor rights etc.

So I wanted to spend some time discussing this further.

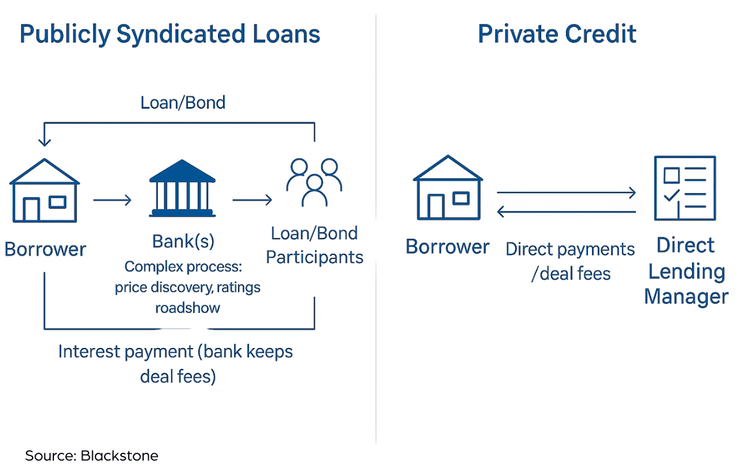

What is Private Credit?

Private credit is simply lending outside public markets—bilateral loans, club deals, privately placed notes, or funds that originate and hold loans.

Borrowers pay up because they need speed, flexibility, or capital that banks won’t provide.

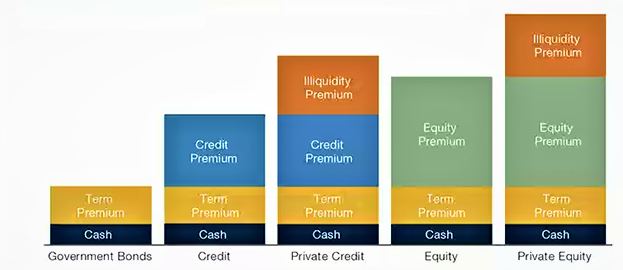

For Singapore-based accredited investors, the prize is the illiquidity and complexity premium.

The trap is thinking the premium lives in the coupon. It doesn’t. It lives in your ability to enforce claims, control cash, and exit when things wobble.

The opportunity today is practical: you can build a diversified, institutional-style private credit sleeve that targets 8–12% net in SGD or USD, with drawdowns that are tolerable and reversible. That outcome doesn’t require heroics or lucky cycles.

It requires a process you can repeat.

Where the return really comes from for private credit?

A private loan’s economics are set long before you wire money.

First, seniority beats yield. A first-lien loan with real collateral and covenants will often beat a “juicy” second-lien because losses are smaller when things go wrong.

Second, cash control turns paper priority into actual priority. If the borrower can move cash freely, your lien is worth less than it looks.

Third, the intercreditor deed decides who gets paid and in what order; a weak deed can prime you overnight.

Finally, information rights matter more than investors realise. Monthly management information—P&L, cash runway, borrowing-base tests, receivables ageing—lets you act before a breach crystallises.

Think of return as: coupon minus expected losses and frictions.

If a loan pays 12% but you realistically expect a 5% default probability with 40% loss given default, that’s a 2% drag.

Add fees, FX hedge cost, and some liquidity friction, and your true net may be closer to 8–9%.

And note that this is assuming you diversify.

If you do 100 loans with a 5% default probability, 5 loans probably go bad.

If you do 1 loan, there’s a 5% chance you lose all your money.

So be ruthless with risk management when it comes to illiquid investments like private credit.

If a deal can’t clear that bar after honest adjustments, pass. There will always be another deal.

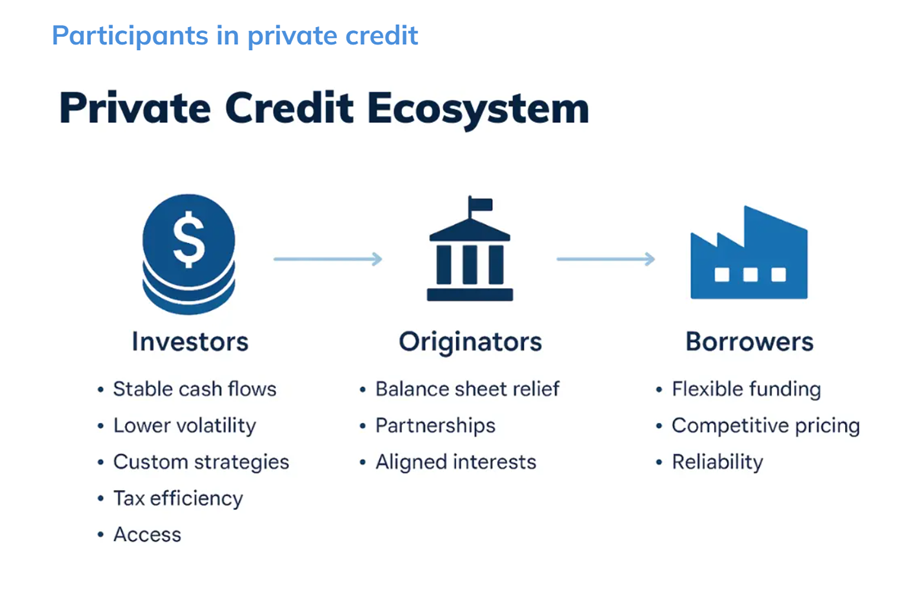

How to access private credit as a Singapore investor

For most Accredited Investors in Singapore, your practical entry points are funds, co-investments alongside those funds, and curated direct deals via private banks or external asset managers.

Each path trades off control, workload, and fees.

Start with clarity on your constraints: currency (SGD vs USD), lock-ups you can live with, and the maximum drawdown you’ll tolerate from credit events.

With that set, here’s how access typically works in real life:

1) Funds (the default route).

Expect a Singapore VCC or Cayman/Delaware LP with quarterly NAV and a lock-up.

Minimums often start in the low six figures (USD). The fund originates or buys senior secured loans, asset-backed facilities, and occasionally mezz/unitranche.

You get diversification, professional workout capability, and reporting. You pay for it via management and performance fees.

The key to making funds work for you is a side letter: fee break at your ticket size, “most favoured nation” on economics, monthly data-room access (not just quarterly PDFs), co-invest rights, and protections against strategy drift or key-person risk.

For example, here’s one such fund offered via Syfe Private Credit (to be clear – this is NOT a Syfe sponsored post, nor am I endorsing them. Just giving an example):

Syfe Private Credit: Curated Access with Global Partners

To make private credit more accessible to accredited investors in Singapore, Syfe has partnered with BlackRock, the world’s largest asset manager.

Through this partnership, Syfe offers institutional-grade private credit opportunities that were once only available to large institutions, now at minimum investment sizes of US$50,000.

Key Features:

- Target Net Returns: 10%+ per annum

- Focus: Lending to US middle-market companies

- Manager: BlackRock, Monroe Capital, Silverdale

- Lock-up Period: 1 year, with flexible withdrawal options thereafter

These curated products give accredited investors in Singapore an efficient, lower-barrier entry point into premium private credit strategies, offering high yield and low correlation to public markets.

Syfe’s rigorous due diligence and exclusive partnerships with globally respected managers ensure that every private credit product meets high standards of quality, transparency, and investor protection.

…

To join Syfe Private Wealth, you’ll need to first qualify as an Accredited Investor and fulfill 2 other criteria:

- Minimum AUM of S$500K

- Minimum investment of US$50K into AI-only offerings.

2) Co-investments/sidecars (more control, more work).

When a fund leads a deal, you may be invited to take a slice on the same terms.

This is where you pick your battles: first-lien, real collateral, clean intercreditor deed, and visible cash control.

Turnaround times are short; you must be willing to read documents and wire quickly.

Use co-invests to tilt your portfolio toward your best ideas without taking fund-level style drift.

3) Private bank/EAM pipelines (curated flow, watch fees).

Banks and external asset managers can present club deals and notes, sometimes with security packages already diligenced.

This is convenient but can layer fees and create custody/operational complexity.

Ask, in plain English: who gets paid what, from where, and when?

Confirm whether your position is truly senior and secured in the same way the deck implies.

4) Direct/club deals (maximum control, maximum responsibility).

Here you (and a few peers) lend directly to a borrower.

Only pursue this if you will actually monitor monthly MIS, enforce covenants, and fund a workout if needed.

The upside is bespoke terms—tight covenants, conservative leverage, and genuine cash dominion.

The downside is concentration and the need to act like a lender, not a passenger.

5) SME/marketplace platforms (small tickets, higher dispersion).

These are useful for learning and for a speculative satellite sleeve, not for core income.

The underwriting depth, collections muscle, and legal security vary widely.

Treat headline coupons as marketing until you’ve verified recoveries through a full cycle.

Is the risk-reward of Private Credit worth it—and how I would do it as a Singapore Investor

Personal view – I don’t think Private Credit is for everyone.

The risks are very real, and this is an illiquid asset class, where you cannot get your money back easily.

But like any investment, if you understand and appreciate the risks, apply ruthless risk management, and have a strong process in place, you can get good returns.

The 8–12% “headline” is real, but it’s earned by structure: perfected security across the right jurisdictions, true cash control, a clean intercreditor deed, and relentless monthly monitoring.

If you won’t insist on those, take the lower but safer yield in public bonds and sleep well.

If you will, private credit can have a place in HNWI income sleeves.

My view on sizing for Private Credit.

For an investor living in SGD with a balanced wealth plan, a 10–30% allocation of the income sleeve (not total net worth) is sensible, calibrated to liquidity needs.

Conservative investors sit near 10–15%; investors with stable cashflow and higher tolerance for illiquidity can run 20–30%.

The hurdle is loss-adjusted 8–10% net at the portfolio level after fees and FX.

Note that this is for more sophisticated, accredited investors, and sizing numbers above are only as a percentage of the income portfolio (not total net worth).

If you’re just starting out in investing, I would say just skip this asset class and stick to more plain vanilla assets with daily liquidity – until you build up more capital and familiarity with investing.

How I would evaluate and pick private credit deals?

Assuming I am picking private credit deals directly (and not via a fund).

Then I want to see perfected security, genuine cash control, monthly data, and a clean intercreditor deed.

Otherwise, I’ll pass—no matter the coupon.

There will always be another deal.

That discipline, more than the brochure yield, is what turns private credit from a marketing promise into a durable, repeatable source of income for a Singapore investor.

Ticket sizing and pacing

Stage commitments over 6–12 months so you don’t buy everything at one macro moment.

Cap any single manager at 15% of the sleeve; any single borrower at ~3%.

That way, one mistake cannot move overall portfolio NAV by more than a small % in a year.

Of course, this requires a large enough portfolio size, otherwise you’re better off just skipping private credit.

What a good private credit deal looks like

A strong deal is boring in the best way.

Security is perfected in every relevant jurisdiction, with filed charges, share pledges, and legal opinions that an external counsel is happy to put their name on.

Cash sits in controlled accounts; a waterfall directs receipts to senior lenders first, with triggers that sweep more cash when metrics deteriorate.

The intercreditor deed is specific about ranking, cure rights, and standstills.

Covenants aren’t there to punish— they exist to surface trouble early: leverage caps, borrowing-base tests, and monthly information rights.

The sponsor has real equity at risk and a track record of supporting businesses through cycles, not just raising new funds when old ones are still smouldering.

Building a private credit portfolio that survives the interest rate cycle

Start by fixing your constraints: currency, lockup tolerance, and the maximum annual drawdown you will accept from credit events.

Then shortlist three to five managers who don’t source from the same pond.

You want diversity by borrower type and by collateral—senior secured corporate loans, asset-backed facilities (receivables, inventory, equipment), conservative real-estate bridge loans at sensible LTVs, and a small sleeve of venture debt for upside if you can stomach the volatility.

Stage your commitments over six to twelve months so you aren’t buying the entire book at one macro moment.

Cap any single manager at 15% of your private credit sleeve and any single borrower exposure at roughly 3%. A simple rule that works: no individual impairment should be able to move your overall portfolio by more than 0.5% in a year.

Keep a cash or T-Bill reserve—around 10% of the sleeve—to meet capital calls and opportunistic add-ons without forced selling.

Match hedge tenors to loan duration; short-dated hedges invite rollover risk right when spreads widen and the currency moves against you.

Monitoring that actually adds value

The easiest alpha in private credit is early action.

Insist—contractually—on monthly data. Read it. Look for slippage in interest coverage, leverage that inches up, receivables that age in place, inventory that bloats, and covenant waivers that become “serial.”

Two waivers in a row without a credible cure plan is a stop sign: halt reinvestment in that sleeve, escalate to the workout plan you pre-agreed, and assume things get worse before they get better.

When a problem appears, act like a lender, not a hopeful equity holder. Tighten cash controls, reduce availability on borrowing bases, and focus on time-to-cash in recoveries rather than theoretical enterprise values.

Remember – when you invest in debt, its all about the numbers.

When you invest in equity, its all about the story.

With private credit – don’t believe the story, believe the cash flow.

Red flags worth walking away from

If security interests aren’t filed locally “yet,” they may never be. If the intercreditor deed is “in progress,” you don’t have it.

If management won’t provide monthly statements, you will learn bad news from rumours, not numbers.

If a platform touts a first-loss buffer, demand proof that it exists, is locked, and is structurally subordinate; marketing slides are not subordination.

If valuations are signed off by the manager but not an external administrator, assume they are optimistic.

If a fund suddenly migrates from senior secured to mezz to chase yield, your risk just changed even if the brochure didn’t.

Bottom line with private credit? Will I invest in private credit?

The spread is real, but you earn it by doing boring, repeatable, institutional work—perfecting security, controlling cash, enforcing covenants, and acting early.

And with any illiquid asset class – risk management is key.

If a deal smells bad, don’t be afraid to walk.

There will always be another deal down the road.

Personal view – I don’t have any exposure to private credit today, but that’s not to say that I think it’s a bad investment.

I just don’t want to invest the time and effort to monitor and maintain a private credit portfolio.

I want to spend that time on my equity investments instead.

With my income portfolio, I want things that are ultra low risk (T-Bills, Fixed Deposit etc), or liquid enough for me to get out any time (REITs, bond funds).

But hey that’s just me – love to hear what you think!

This article is written on 25 Sep 2025 and will not be updated going forward. My latest personal portfolio, stock watch, and macro views are shared on FH Premium.

That’s a good overview of Private Credit. Personally, still on the fence on this. Will get some allocation when/if I have new funds.

Thanks – glad you found it useful.