A lot of you probably saw the headlines this week about DBS Bank profits falling 10%.

This led to a lot of discussion as to whether DBS profits are topping out – and whether it is time to take profit in DBS Bank.

I myself hold both OCBC and UOB bank but no DBS Bank.

But given that any macro weakness for DBS Bank will probably spell trouble for OCBC and UOB as well.

I wanted to take a closer look at DBS Bank’s Q4 profits.

And ask whether it is time to take profit in DBS Bank?

Or whether it is worth buying DBS Bank at the current 5.6% dividend yield.

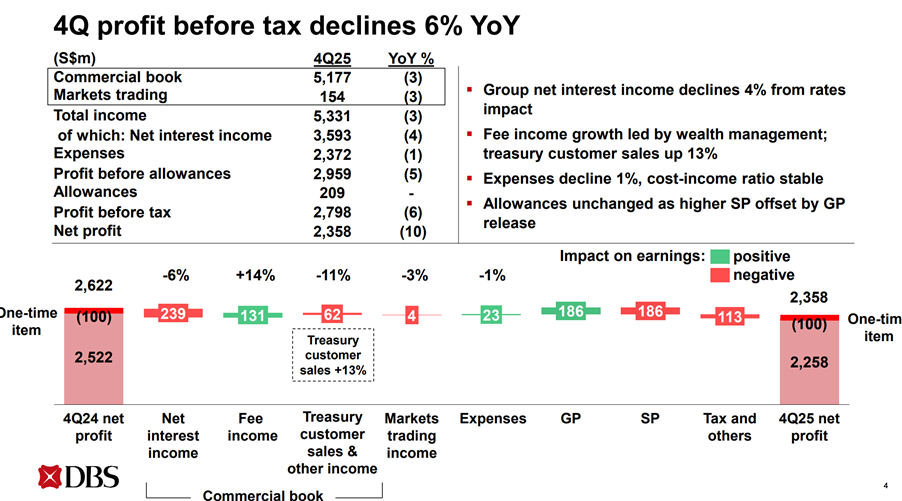

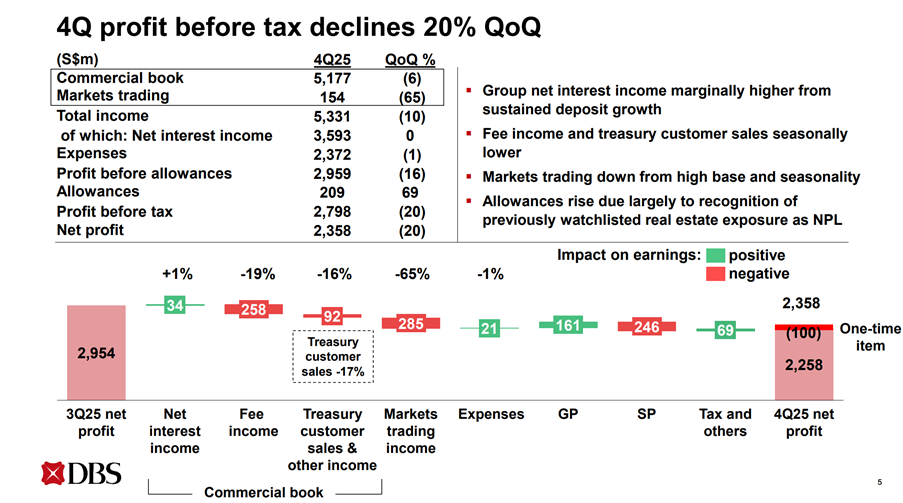

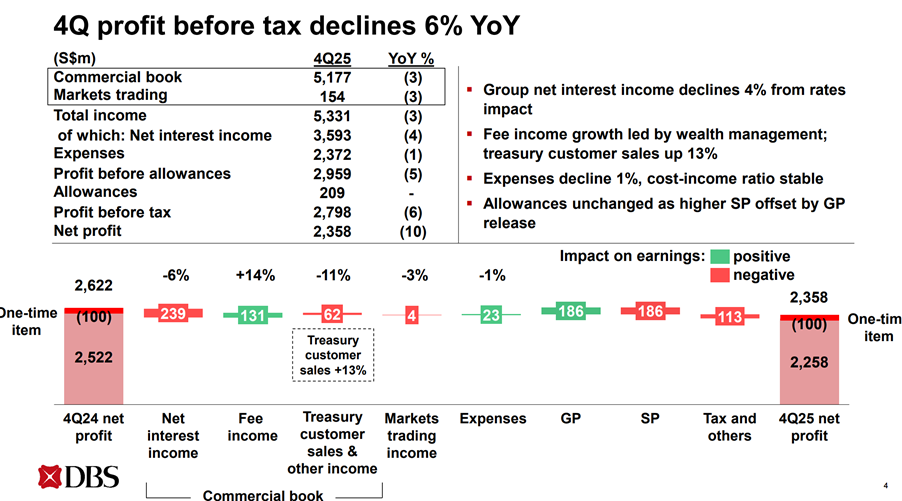

DBS Bank profit falls 10% YoY – and 20% QoQ

DBS Bank’s Q4 profits are extracted below.

You can see the Q4 net profit is down 10% on a year on year basis.

And down 20% on a quarter on quarter basis.

So the headline number optics wise is terrible.

A 20% quarter on quarter drop in profits is never pretty.

BUT – if you look under the surface, it’s not actually that bad

But if you look under the surface and really understand what is behind this large drop in profits.

Frankly it’s not actually as bad as the headline number suggests.

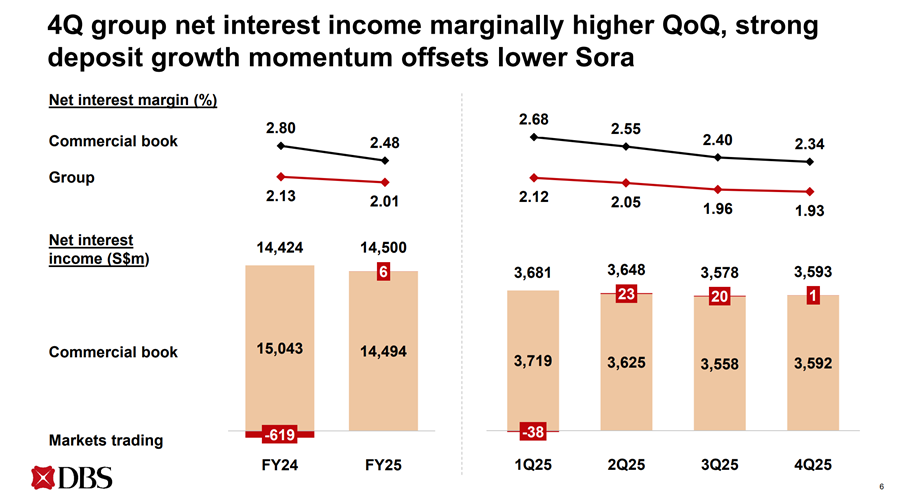

Net Interest Margin continues to decline on lower interest rates

First off – the bad.

Net interest margin continues to decline to 1.93% — the lowest of the year — dragging net interest income down 4% YoY.

DBS offset some of this with massive deposit gathering, but not all of it.

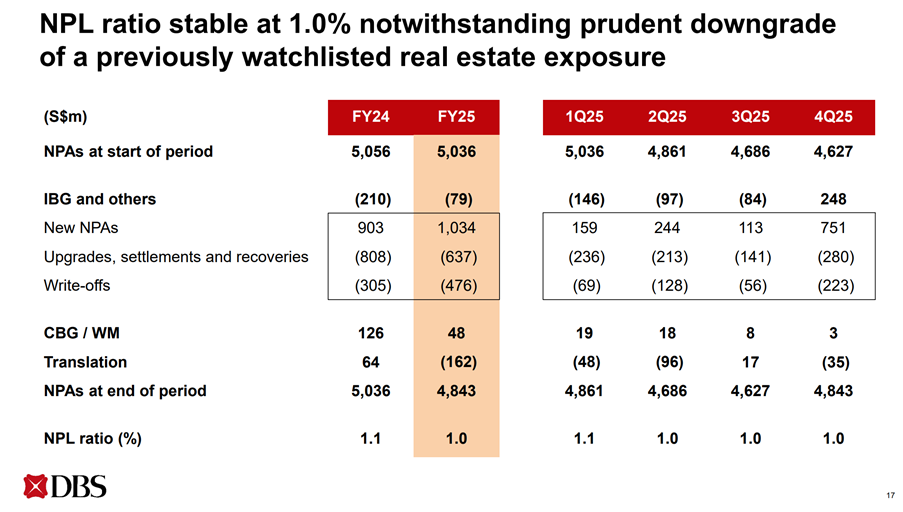

One big bad loan surfaced

More bad stuff.

A Hong Kong real estate exposure that management had been watching for a while was formally classified as non-performing.

That single downgrade drove Q4 new non-performing assets (NPAs) to S$751m — roughly triple the prior quarters — and pushed specific provisions to 36bp, more than double the run-rate.

Accordingly to management, this is a one-off reclassification, not a sign the loan book is deteriorating broadly.

That being said, you’ll note that UOB also recently booked a large allowance due to Hong Kong real estate weakness.

So… one-off or more to come?

The prior year had one-time gains that didn’t repeat

Then we have the good stuff.

Q4 2024 included non-recurring items that flattered that quarter’s result.

Stripping those out, the underlying decline is less dramatic than the headline –10% suggests.

Higher taxes

The global minimum tax (Pillar Two) kicked in during 2025, permanently raising DBS’s effective tax rate.

This shaves a few hundred million off net profit annually — pre-tax profit was actually only down 6%, but net profit fell 10% because of the higher taxes.

This is good in that it suggests the underlying business is actually okay as the impact was due to tax.

But it’s also bad because tax on profits is still something that results in less profits to shareholders.

So… the underlying business remains solid?

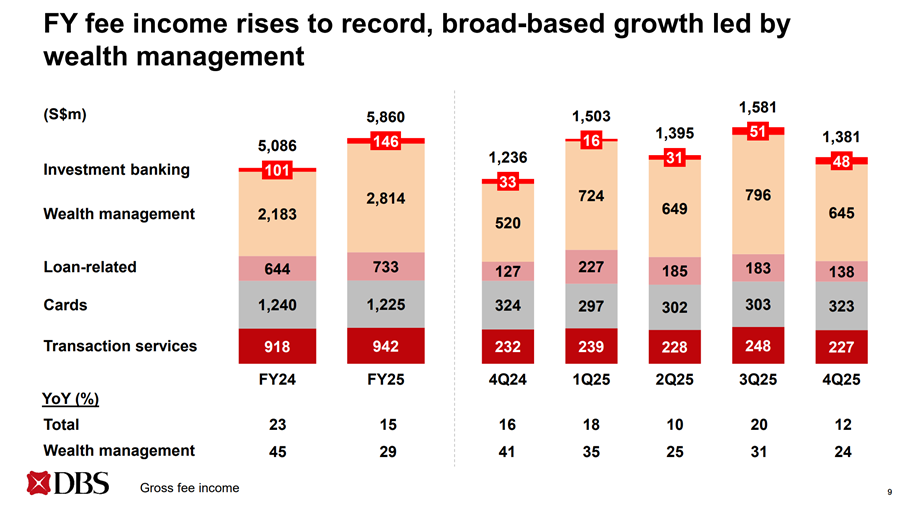

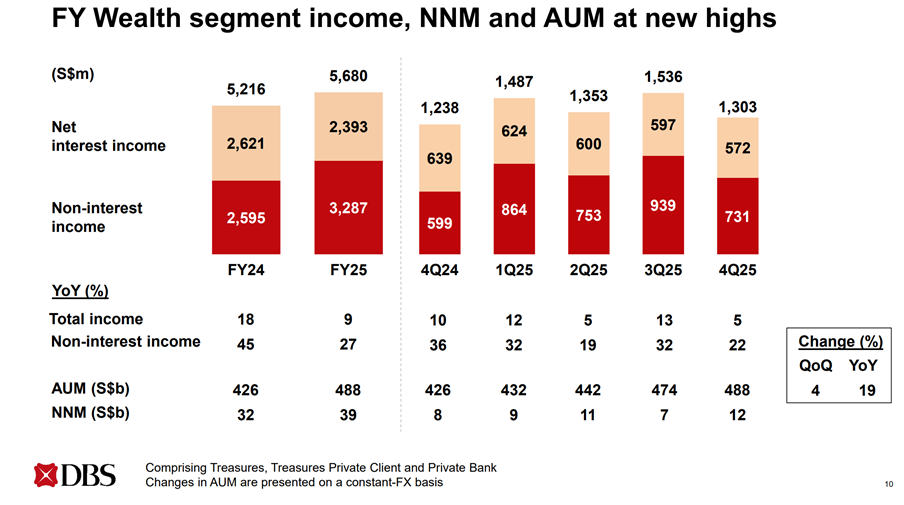

Meanwhile, the underlying non-lending business — fees, wealth management, deposit growth, cost control — was actually fine.

Wealth fees grew 24% YoY even in Q4, and deposits kept surging.

It’s the combination of rate headwinds, one chunky provision, disappeared one-offs, and a new tax regime that made the quarter look worse than the core business actually performed.

DBS share price sold off slightly – but remains very strong and trending up

The share price reaction?

We had about a 5% sell-off in the share price since the earnings result.

Taking the stock right below the 50 day moving average.

That said, you could argue some of this was due to the broader market sell-off and not because of the earnings, and that’s a fair point.

Generally I would say the share price remains in a strong uptrend, but the dip below the 50 DMA is something worth monitoring.

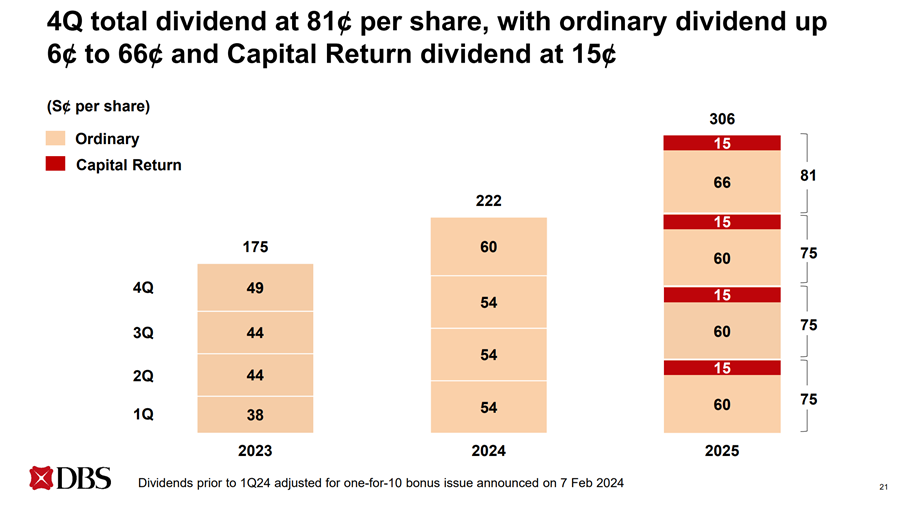

DBS pays a 5.6% Dividend Yield at this price

Assuming the 66 cents ordinary dividend continues.

And a capital return dividend of 15 cents.

You’re looking at a 5.6% dividend yield for DBS Bank at today’s price.

It’s definitely not as strong as when the share price was much lower.

But that’s still in line with the dividend from blue chip REITs from CapitaLand and Mapletree.

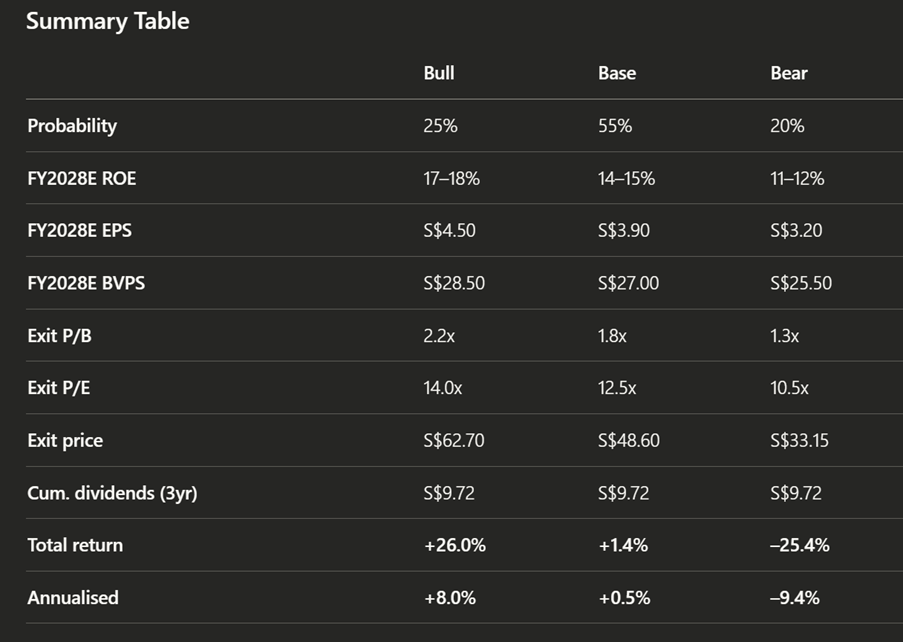

Risk-reward of DBS Bank at $57

I crunched the numbers on the risk-reward of DBS Bank at today’s price.

You can see my assumptions for the bull, bear and base cases below:

Bull Case (25% probability)

Thesis: NIM troughs in H1 2026 and stabilises as rate cuts slow or reverse; wealth management fees sustain mid-teens growth, compounding AUM toward S$600B+; bolt-on M&A (Malaysia/Indonesia) executes cleanly; MAS lifts the 1.8x operational risk capital multiplier; ROE re-accelerates to 17–18%.

Base Case (55% probability)

Thesis: NIM compresses further in 2026 then stabilises around 1.8–1.9%; fee income grows at high single digits (not mid-teens) as wealth management growth normalises; ROE settles at 14–15%; cost discipline holds; credit quality sound with SP at 17–20bp as guided. DBS becomes a reliable but slow-growth income stock. Market gradually de-rates the P/B as investors recognise ROE has structurally stepped down from the 2023–2024 peak.

Bear Case (20% probability)

Thesis: Aggressive rate cuts compress NIM below 1.7%; China/HK real estate NPLs escalate beyond the single exposure already flagged (note: Q4 new NPAs of S$751m were 6.6x the Q3 run-rate — what if more follow?); regional macro slowdown (China hard landing, trade war escalation) hits loan growth and credit quality; major tech outage triggers fresh MAS penalties; ROE falls to 11–12%.

This is what the upside / downside looks like in each of the scenarios:

If you simplistically add up the Probability-Weighted Expected Return, it gets you:

(0.25 × 26.0%) + (0.55 × 1.4%) + (0.20 × –25.4%) = 6.5% + 0.8% + (–5.1%) = +2.2% over 3 years (~0.7% annualised)

But to be absolutely clear – “Probability-Weighted Expected Return” is just a hypothetical number.

In reality, what will actually happen is that you will not have all 3 scenarios materialize – only 1 of the scenarios will materialize.

So please take this probability weighted number with a pinch of salt.

It’s that joke about how you shoot a bullet to the left and a bullet to the right, and on average you hit the target.

Real life doesn’t work like that.

Either DBS delivers the bull case, or it does not.

DBS profit falls 10% – Is it time to sell DBS Bank? Or buy more at 5.6% dividend yield?

So… is DBS worth a buy?

What I like about DBS today, is that you are getting:

- A 5.6% dividend yield with strong near-term visibility (capital return committed through FY2027)

- Best-in-class franchise quality (deposit growth, wealth AUM, digital banking)

- The earnings trough is approaching, not accelerating — NIM compression is decelerating

- Fortress capital position (CET1 17%) provides buffer against adverse scenarios

What I don’t like about DBS Bank, is that:

- 2.4x P/B is the 95th percentile of global banks — you’re paying for perfection

- ROE is declining (18.0% → 16.2% → guided lower) and the premium P/B assumes it won’t

- NIM compression is ongoing with at least two more Fed cuts priced in

- Global minimum tax permanently lowered the earnings run-rate

- GP reserves are being drawn down, not built up

And as you can see from my simplistic bull and bear cases.

I think the risk-reward is roughly symmetric here.

It’s a heads I win moderate amounts, tails I lose moderate amounts kind of scenario.

That being said, I’ve not been enthusiastic about the risk-reward on DBS since the high 30s, and yet the share price has marched 50% higher since then.

And if you look at the charts, the trend of DBS is still quite strong (leaving aside the current dip below the 50 DMA).

What I would say is that when a stock is trending up like that, you generally don’t want to fight the trend.

If I have a position in DBS Bank today, I’ll probably just continue to hold and ride the trend up, until such time as the trend changes.

But for new capital – boy I really have second thoughts about buying DBS Bank at 2.4x book value.

At 2.4x book value, DBS Bank trades at the same Price/Book as JP Morgan.

Like I said, sure it can continue to go higher.

But the risk-reward looks symmetric here.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

What about UOB and OCBC Bank?

If DBS Bank is fully priced.

What about UOB and OCBC Bank?

I’ve charted the price action for UOB and OCBC in 2026 below.

You can see how UOB is the strongest performer in 2026 so far with a 10% performance.

OCBC comes in second at 7%.

And DBS is last at a measly 2%.

Which means that so far in 2026 at least, you would have made more by owning UOB and OCBC.

From a valuations perspective, I crunched the numbers below:

| Metric | OCBC | UOB | DBS (for reference) |

| Price | S$21.30 | S$38.85 | S$57.50 |

| P/B (current) | 1.60x | 1.28x | 2.37x |

| P/B vs. 13-yr median | 48% premium | 15% premium | 74% premium |

| P/B percentile (13-yr) | ~95th | ~80th | ~99th |

| TTM ROE | ~13% | ~12–13% (normalised) | 16.2% |

| NPL ratio | 0.9% | 1.6% | 1.0% |

| NPA coverage | 160% | 88% | 130% |

| CET1 | 17.0% | 14.6% | 17.0% |

| Forward dividend yield | ~4.7–4.9% | ~4.4–5.0% | 5.3–5.6% |

| Prob-weighted 3yr return | +0.5% | +9.4% | +2.2% |

I fed this analysis into Claude, and it gave me this:

UOB has the most attractive risk-reward profile of the three Singapore banks today. This is a somewhat contrarian call, so let me explain the reasoning:

1. UOB’s valuation discount is under-appreciated. At 1.28x P/B, UOB trades at only a 15% premium to its 13-year median, versus 48% for OCBC and 74% for DBS. This means much less multiple compression risk in the base case. Even if ROE stays at a mediocre 12%, UOB’s P/B is roughly fair at current levels — you’re not paying for outperformance that may not materialise.

2. The base case for UOB is surprisingly good. At 1.28x P/B with a ~4.5–5.0% dividend yield, UOB doesn’t need a re-rating to deliver decent returns. Simply holding book value and collecting dividends gives you ~13% over 3 years. In contrast, OCBC’s base case delivers essentially zero because it needs its elevated 1.6x P/B to hold — and that premium is vulnerable if the capital return programme isn’t extended post-2026.

3. UOB’s bear case is less severe than OCBC’s or DBS’s. Because you’re entering at a lower multiple, the downside to trough valuation (0.9x P/B) is –15% vs. –25% for OCBC and DBS. The floor is closer.

4. The S$615m pre-emptive provision is a hidden asset. UOB’s management effectively front-loaded pain in Q3 2025. Those general provisions sit on the balance sheet and can be written back if asset quality holds. This is the opposite of DBS’s Q4 HK real estate reclassification, which was a negative surprise.

5. The ASEAN optionality is real but unpriced. With 82% of PBT from ASEAN, UOB is the purest play on trade rerouting, supply chain diversification away from China, and ASEAN demographic growth. This is a multi-year structural tailwind that the market is currently discounting due to near-term trade war fears.

The counterargument for OCBC: OCBC has a cleaner balance sheet (0.9% NPL, 160% coverage, CET1 17%), a more diversified revenue mix through insurance, and the best private banking platform of the three (Bank of Singapore). The 60% payout commitment through 2025 is also a concrete near-term catalyst. But at 1.6x P/B, you’re paying a meaningful premium for these advantages, and the probability-weighted return of +0.5% over 3 years is essentially a rounding error.

| Rank | Bank | Verdict | Prob-weighted 3yr return | Best for |

| 1 | UOB | Most attractive | +9.4% | Value investors willing to accept near-term noise; ASEAN growth conviction |

| 2 | DBS | Hold, don’t chase | +2.2% | Existing holders who want income and franchise quality |

| 3 | OCBC | Fairly priced | +0.5% | Those who want best-in-class balance sheet and insurance diversification |

If forced to buy one today: UOB. The entry multiple provides the widest margin of safety, the base case delivers meaningful positive returns, and the asymmetry (2:1 upside vs. downside) is clearly the best among the three. The key risk — higher NPLs and thinner coverage — is partially mitigated by the S$615m pre-emptive provision buffer.

My personal thoughts?

Claude’s conclusion was really interesting for me.

But to be absolutely honest, I’m not sure I agree.

I think Claude is looking at it simplistically from a pure valuations perspective, and isn’t properly accounting for the strength of each respective business.

It also doesn’t account for momentum and inflection points – that stuff that is doing well continues to do well for a long period of time, until the market finally wakes up to the fact that fundamentals have changed.

So if you ask me I think DBS and OCBC bank are a lot more attractive than Claude is letting on, while Claude is overplaying how attractive DBS Bank is.

Closing Thoughts – Is it time to sell DBS Bank? Or buy more at 5.6% dividend yield?

Coming back to the original question.

With a chart like that, I think if I had a position, I would just let it continue to run, until such time as the trend reverses.

But with new capital, boy I would be a lot more cautious buying DBS at a 2.4x book value.

It’s not to say that it’s a bad buy because a 5.6% dividend from a best in class bank that is trending up is actually a great buy.

It’s just that the valuations are rich, which means any wobble and you could get a meaningful sell-off.

Which makes the risk-reward roughly balanced in my view – you’re risking $1 to make $1.

So it depends what you’re looking for in a stock.

A fair value compounder with an attractive dividend, DBS Bank could be it.

An asymmetric risk-reward play that could triple your money if you’re right, with 50% downside if you’re wrong.

This probably isn’t it.

If you enjoy articles like this, do support Financial Horse on FH Premium and get access to premium articles like this, including my stock watch and investment portfolio.

Hi FH,

Gong xi fa cai!

https://sgwealthbuilder.com/2026/02/21/dbs-group-holdings-share-price-to-hit-70/

Looking back, my last article on DBS Group Holdings share price in 2024 was a tribute to former CEO Piyush Gupta. Back then, I had forecast that it would be difficult for the stock to reach $50 unless DBS listed its international transfers platform, Remit. Indeed, DBS Group Holdings share price did not reach $50 in 2024 nor did it list Remit. However, the counter exceeded my expectations when it managed to cross the magical $50 in 2025. What has exactly changed that moved the needle for DBS Group Holdings share price.

Previously, I have maintained that based on business fundamentals alone, it would be difficult for DBS Group Holdings share price to smash past $50. To unlock value, it was essential for DBS to list its digital assets. What I did not foresee was the MAS’s Equity Market Development Programme (EQDP) introduced in February 2025 as part of the Equities Market Review Group’s recommendations to revive SGX. In February 2026, MAS has expanded the EQDP from $5 billion to $6.5 billion.

Although MAS did not disclose whether the funds released to the asset managers has been used to purchase DBS shares, the matter of fact is that DBS Group Holdings share price enjoyed a splendid rally, surging from $38.10 in April 2025 to the record high of nearly $60 in February 2026. The explosive rally of DBS Group Holdings share price was the longest in recent memory.

Of course, there are those who would argue that the rampant form of DBS Group Holdings share price in 2025 was largely attributed to the series of shares buybacks conducted by the bank. To this end, I do not disagree but it is also important to note that the last shares buybacks took place 11 July 2025. Since then, the counter kept rising till February 2026. On this note, shares buybacks should not be the only major catalyst driving DBS Group Holdings share price to record highs in 2025.

Given that MAS has only released about half the funds for EQDP, I believe there is still potential upside for DBS Group Holdings share price in 2026. Furthermore, DBS has only done about $370 million of shares buybacks out of the total $3 billion buyback programme (about 12%). So yes, I do think that the best is yet to be for DBS Group Holdings share price. In this article, I will share my insights on the outlook for DBS in 2026.

https://sgwealthbuilder.com/2026/02/21/dbs-group-holdings-share-price-to-hit-70/