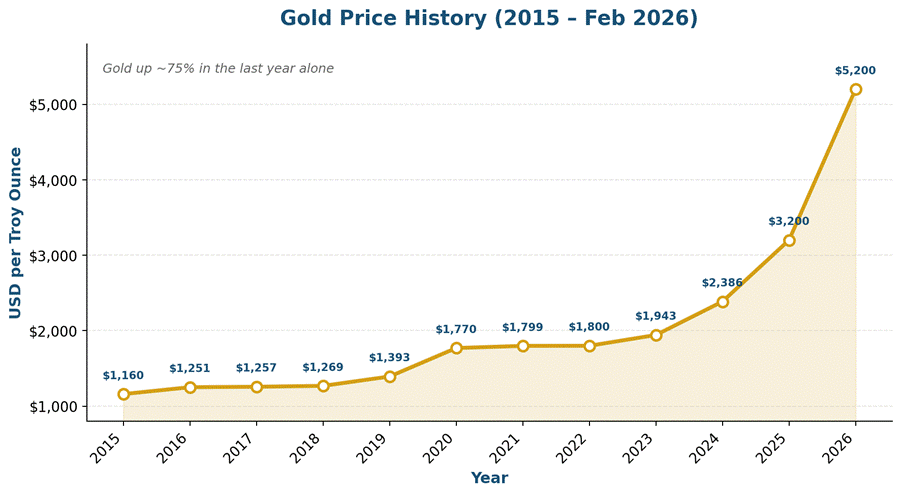

Gold has been on an absolute tear.

As I write this in February 2026, gold is trading at approximately US$5,200 per ounce — up more than 75% from a year ago.

Yes, you read that right. 75% in a year.

You can see the sheer magnitude of the move in the chart below.

I’ve talked about gold before as a hedge against money printing — and boy has that thesis played out.

With gold prices at all time highs, a lot of you have been asking me how exactly you can buy gold in Singapore.

So I figured this was a good time to write a practical how-to guide on the different ways to buy gold in Singapore — from physical gold bars to ETFs to bank savings accounts.

Let’s dive in.

Why buy gold in the first place?

Before we get into the how, let’s quickly address the why.

Long story short — gold is a store of value that has been around for thousands of years.

In the current macro environment where the US is running massive fiscal deficits and the Federal Reserve is keeping monetary policy easy, gold acts as a hedge against money printing.

Gold doesn’t pay a dividend or yield. So you won’t get income from owning gold.

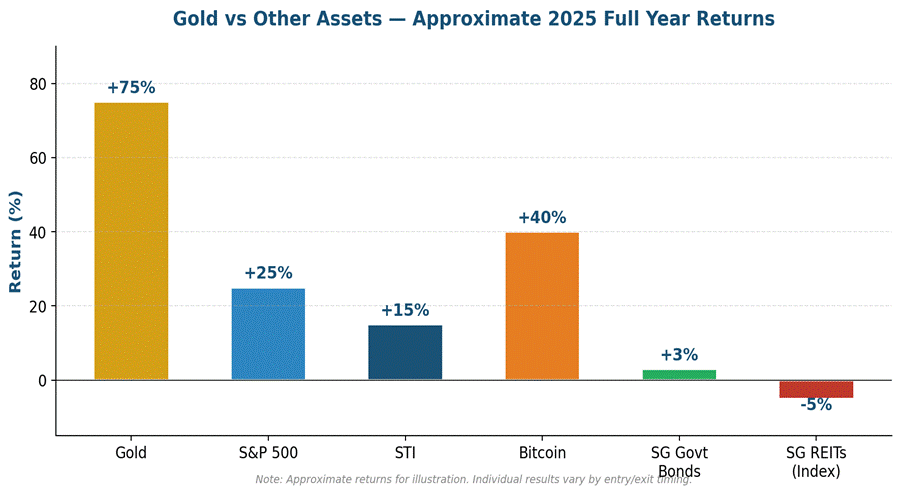

But what gold does give you is a hedge against currency debasement and inflation — which is why you’ve seen gold soar to all time highs.

And you can see from the chart below just how well gold has performed relative to other major asset classes in 2025.

Most advisors recommend a 5% to 10% allocation to gold in a diversified portfolio. Whether you agree with that is up to you, but the point is that gold has a place in a well-constructed portfolio.

Now — how do you actually buy gold in Singapore?

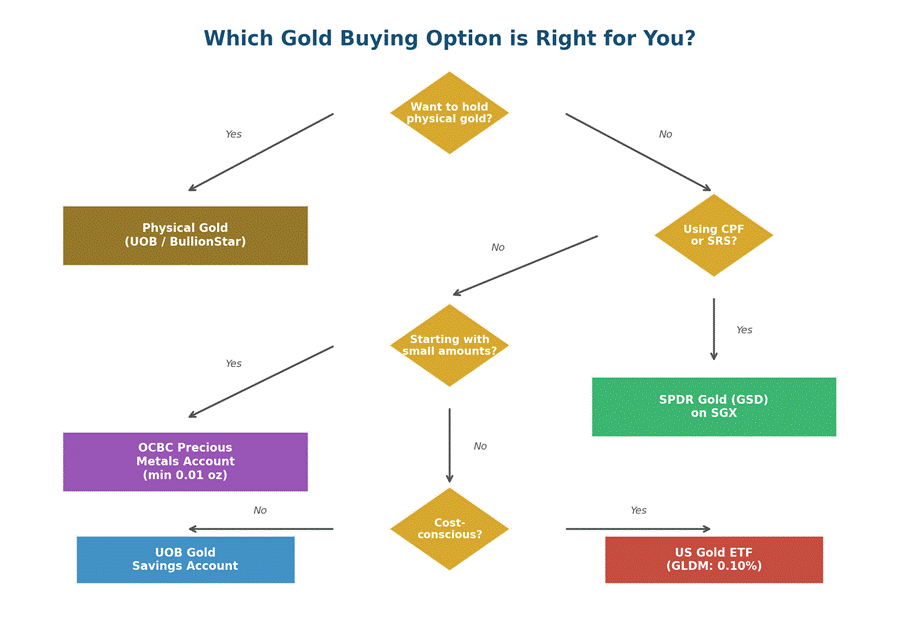

5 ways to buy gold in Singapore

There are broadly 5 ways to buy gold in Singapore:

- Physical gold bars and coins — Buy actual gold you can hold

- Gold ETFs — Buy gold exposure through a stock exchange

- Gold Savings Accounts — Buy gold through a bank account (UOB, OCBC)

- Gold Certificates — Buy certificates representing physical gold

- Gold Futures / CFDs — Trade gold as a derivative (more for active traders)

Not sure which one is for you? This decision flow might help:

I’ll walk through each option below, with the pros, cons, and practical steps for each.

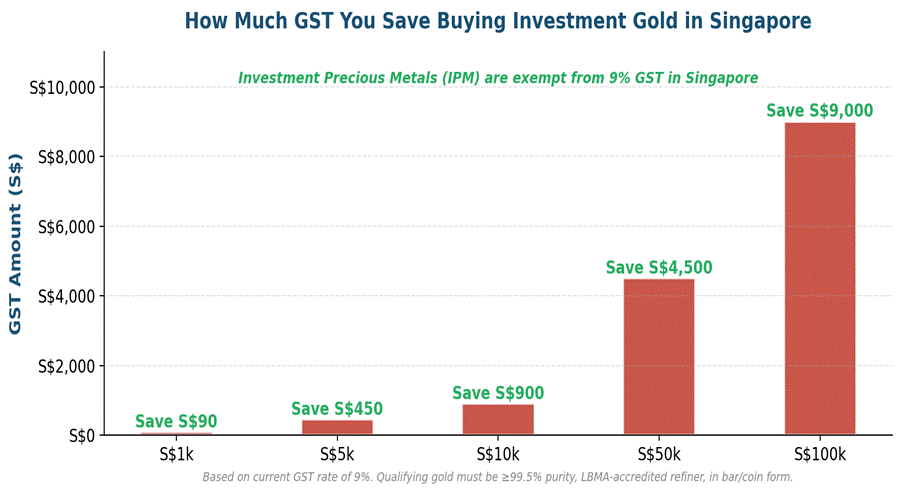

Important: Gold is GST-exempt in Singapore

Before we go further, one big advantage of buying gold in Singapore — qualifying investment-grade gold is exempt from GST (Goods and Services Tax).

Since October 2012, the import and local supply of Investment Precious Metals (IPM) in Singapore are exempt from GST (currently 9%).

To qualify for GST exemption, the gold must meet all of the following criteria:

- Purity: At least 99.5% pure gold

- Form: Bars, ingots, wafers, or prescribed coins

- Refiner: Refined by an LBMA (London Bullion Market Association) accredited refiner

- Not decorative: Must not be a decorative or collector’s item

This is a huge deal. You can see below just how much you save in GST across different investment amounts.

There’s also no capital gains tax in Singapore — so any profits you make from selling gold are tax-free.

That said, gold jewellery does NOT qualify for GST exemption. So if you’re buying gold purely for investment, stick to bars, coins, or financial products.

Option 1: Physical Gold Bars and Coins

This is the OG way to own gold. You buy actual gold bars or coins that you can hold in your hand.

Where to buy physical gold in Singapore:

| Dealer | Products | Min. Purchase | Key Notes |

| UOB Main Branch | Gold bars (1g to 1kg), coins | Varies by product | Appointment-only from Feb 2026. Must be UOB account holder. |

| BullionStar | Wide range of bars and coins from LBMA refiners | No minimum | Walk-in at 45 New Bridge Rd (near Clarke Quay MRT). Also offers vault storage. |

| Silver Bullion (The Safe House) | Gold bars, coins, storage | SGD 5,000 min. transaction | Known for S.T.A.R. segregated vaulting. Located at Millenia Walk. |

| GoldSilver Central | Bars and coins | Varies | Located at Far East Shopping Centre. |

| Indigo Precious Metals | Bars, coins, gram saving plan | Varies | Offers vault storage at Le Freeport Singapore. |

Important note on UOB: Due to massive demand for physical gold, UOB moved to an appointment-only system for physical gold purchases and conversions from 13 February 2026. Walk-ins are no longer accepted. You need to book an appointment via UOB’s website, and slots open at 6pm the previous working day.

UOB is currently the only bank in Singapore that sells and purchases physical gold. So if you want to buy from a bank, UOB is your only option.

Pros of physical gold:

- You own the actual gold — no counterparty risk

- GST-exempt for qualifying IPM in Singapore

- Tangible asset you can hold, gift, or pass down

Cons of physical gold:

- Storage and security — you need a safe or vault

- Higher premiums over spot price compared to ETFs or savings accounts

- Less liquid — selling requires going back to the dealer or bank

- Risk of buying counterfeit gold if you don’t use reputable dealers

- Insurance costs if you want coverage

My view — physical gold makes sense if you want a meaningful allocation and you have secure storage sorted out. For smaller amounts, the other options below may be more practical.

Option 2: Gold ETFs

If you don’t want the hassle of storing physical gold, Gold ETFs are probably the most popular option for investors in Singapore.

A Gold ETF tracks the price of gold, and you buy and sell it on a stock exchange just like you would a stock.

There is currently only one gold ETF listed on SGX — the SPDR Gold Shares. It’s available in two denominations:

- O87 — traded in USD

- GSD — traded in SGD

Both track the same underlying pool of physical gold held in secure vaults by HSBC and JPMorgan. The only difference is the currency denomination.

As of early 2026, the SPDR Gold Shares ETF is the largest ETF on SGX with AUM exceeding S$3.8 billion.

| ETF | Exchange | Currency | Expense Ratio | Key Feature |

| SPDR Gold Shares (GSD) | SGX | SGD | 0.40% | CPF & SRS eligible. No FX risk. |

| SPDR Gold Shares (O87) | SGX | USD | 0.40% | Same ETF, USD denomination. |

| SPDR Gold Shares (GLD) | NYSE | USD | 0.40% | World’s largest gold ETF. Deepest liquidity. |

| iShares Gold Trust (IAU) | NYSE | USD | 0.25% | Lower expense ratio. Lower per-share price. |

| SPDR Gold MiniShares (GLDM) | NYSE | USD | 0.10% | Lowest cost. Great for DCA. |

CPF and SRS eligible: The SPDR Gold Shares (SGX: GSD) is eligible for purchase using CPF-OA funds under the CPFIS scheme, and also eligible for SRS funds. This is a big deal if you want gold exposure within your CPF or SRS portfolio.

How to buy Gold ETFs in Singapore:

- Open a brokerage account — any of the local brokerages work (DBS Vickers, OCBC Securities, UOB Kay Hian, Phillip Securities, FSMOne, etc.)

- For US-listed ETFs, you can use international brokerages like Interactive Brokers, Tiger Brokers, Moomoo, or Saxo

- Search for the ticker (GSD for SGX SGD, O87 for SGX USD, GLD or IAU for US-listed)

- Place your buy order just like you would for any stock

Pros of Gold ETFs:

- Very liquid — buy and sell during market hours

- No storage or insurance needed

- Low cost (expense ratio of 0.10% to 0.40% p.a.)

- Can use CPF/SRS funds (for SGX-listed GSD)

- Backed by physical gold in secure vaults

Cons of Gold ETFs:

- You don’t own the physical gold directly

- Counterparty risk (though mitigated by the physical backing)

- Annual expense ratio eats into returns over the long term

- US-listed ETFs may have US estate tax implications for non-US persons

US estate tax consideration: If you buy US-listed gold ETFs like GLD or IAU, be aware that as a non-US person, your estate could be subject to US estate tax on holdings above US$60,000. The SGX-listed version (GSD/O87) avoids this issue. UCITS-domiciled gold ETFs (listed in London/Europe) are another alternative.

Option 3: Gold Savings Accounts (UOB / OCBC)

If you want something between physical gold and ETFs, a Gold Savings Account could be the sweet spot.

Two banks in Singapore currently offer precious metals accounts:

| Feature | UOB Gold Savings Account | OCBC Precious Metals Account | Notes |

| Min. Purchase | 5 grams | 0.01 troy ounce (~S$65) | OCBC has a much lower entry point |

| Annual Fee | 0.25% p.a. (min. 0.12g/month) | Bank fees and spreads apply | Fees deducted in gold, not cash |

| Online Transacting | Yes — UOB Internet Banking / TMRW app | Yes — OCBC Digital app | Both are convenient |

| Convert to Physical | Yes — 100g bars (appt only from Feb 2026) | No | UOB has an edge here |

| Currency | SGD | SGD, USD, AUD, EUR and more | OCBC offers multi-currency |

| SDIC Covered? | No | No | Important to note |

How to open a UOB Gold Savings Account:

- You need an existing UOB savings or current account

- Visit any UOB branch to open the Gold Savings Account (in person only)

- Minimum first purchase is 5 grams of gold

- After setup, buy and sell via UOB Internet Banking (Investments > Gold and Silver) or UOB TMRW app (Services > Buy Gold/Silver)

- Online transacting available Mon-Fri, 8am to 11pm (excluding SG public holidays)

Pros:

- Very convenient — buy and sell online via app

- No storage or security concerns

- Lower premiums than physical gold purchases

- UOB offers conversion to physical gold bars

Cons:

- Not covered by Singapore Deposit Insurance (SDIC)

- Annual service fees and spreads reduce returns

- You don’t own the physical gold (it’s a book entry)

- Cannot use CPF or SRS funds

Option 4: Gold Certificates (UOB)

UOB also offers Gold Certificates, which represent physical gold stored at UOB.

You purchase in kilobar quantities (each certificate represents 1 to 30 kilobars of gold).

At current prices of about S$225 per gram, a 1kg gold bar runs roughly S$225,000 — so this is clearly for larger investors.

The gold is stored by UOB, so you don’t need to worry about storage. You receive a certificate as proof of ownership, which can be redeemed for physical gold or sold back to UOB.

Option 5: Gold Futures and CFDs (For Active Traders)

This is the more advanced option, and I’d say this is only for experienced active traders.

You can trade gold futures on the SGX or through CFD platforms like IG Markets, CMC Markets, Plus500, or Saxo Markets.

Futures and CFDs allow you to use leverage — meaning you can control a larger gold position with a smaller amount of capital. But leverage cuts both ways.

Do be wary of the risks involved.

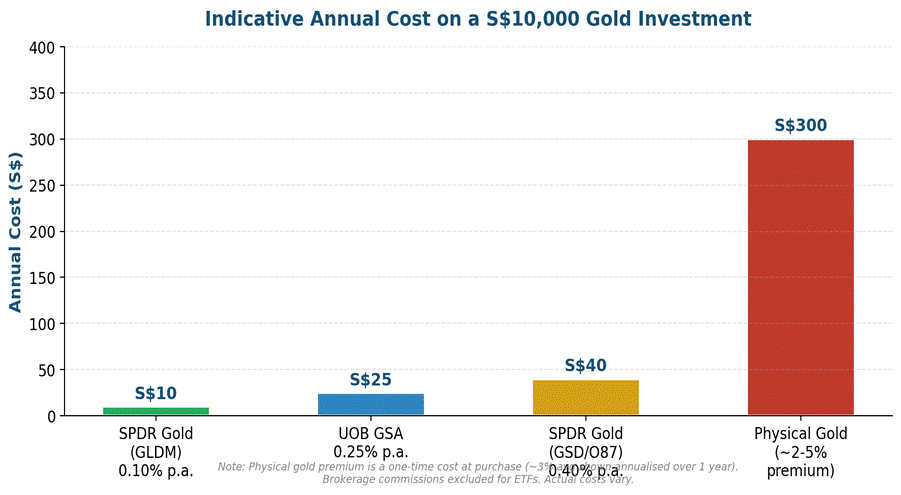

How do the costs compare?

One of the most important things when buying gold is understanding the fees. Here’s a visual comparison of the indicative annual cost on a S$10,000 gold investment:

As you can see, the US-listed GLDM is the cheapest option from a pure fee perspective, while physical gold carries the highest cost due to premiums.

But of course, fees aren’t everything. Tangibility, convenience, CPF eligibility, and counterparty risk all matter too.

Summary: Which option is right for you?

Here’s a quick summary table:

| Option | Min. Investment | Fees | Storage? | CPF/SRS? | Best For |

| Physical Gold | ~S$225+ (1g bar) | Premium over spot | You arrange | No | Long-term holders wanting tangible gold |

| Gold ETF (SGX) | ~S$500+ (1 lot GSD) | 0.40% p.a. | No | Yes | Most investors; CPF/SRS eligible |

| Gold ETF (US) | ~US$50+ (GLDM) | 0.10-0.40% | No | No | Cost-conscious investors |

| Gold Savings A/C | 5g (UOB) / 0.01oz (OCBC) | 0.25% p.a. + spreads | No | No | Beginners; small purchases |

| Futures/CFDs | Varies (margin) | Spreads + overnight | No | No | Active traders only |

My view on how to buy gold in Singapore?

So after all of the above — what do I think?

My simple view.

For most Singapore investors, I think the SPDR Gold Shares ETF on SGX (GSD) is probably the best option.

It’s liquid, it’s backed by physical gold, it has a reasonable expense ratio of 0.40%, and most importantly it’s eligible for CPF and SRS funds.

If you’re cost-conscious and have access to a US brokerage, the US-listed GLDM with a 0.10% expense ratio is very attractive — but do keep in mind the US estate tax implications.

For investors who want to start small, the OCBC Precious Metals Account is a good option with its very low 0.01 oz minimum purchase.

For investors who want physical gold they can hold, the bullion dealers like BullionStar (near Clarke Quay MRT) or UOB’s Main Branch are the way to go.

One thing I would caution — with gold at all time highs above US$5,000 per ounce, I would be careful about going all-in at one price.

Dollar-cost averaging or buying in tranches makes a lot of sense here, just like with stocks.

That’s the risk that I see.

Gold is a great long term store of value and hedge against money printing. But at these prices, there could easily be a short-term pullback of 10-20%.

So position sizing and building a position gradually is key.

Love to hear what you think! How are you buying gold in Singapore?

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi, MariBank offers gold investment as well. Does that fall under ETFs or Gold Savings Account?

I would say ETF as they buy the LionGlobal Singapore Physical Gold Fund Class MariBank SGD Hedged (Acc).

For me this is very interesting and I cannot thank you enough for this article.

I started with phys at Bullionstar (BS), when they had a problem with the Merlion and I lost a 5 figure sum. I changed to Silverbullion (SB), but I have to reduce there. The crazy reason is the way they handle a change of address.

At BS you write the new address in online, attach prove, they check and say a week later “accepted – fine – thanks”. As it took them a week, they even begged pardon for the delay.

At SB they email you a form, this form is valid one month (you must hurry if you live abroad), then both holders must sign it and send it back to them. As my wife and I live / moved to different countries, this is impossible to fullfill. I begged for help – I was ignored – I explained the whole situation and I ask again – they emailed a form – we could not make it in one month – I begged for another form – my email was again ignored…etc pp.

So they forced my wife to buy a plane ticket and visit me for a handfull of days and we hope, SB will send another form tomorrow, as if not, wife paid for nothing. The damage is a plane ticket (guess 1000 Euro), taxis (guess 50), loss of holiday time (what we wanted to do, is impossible now – lack of free days).

I do not remember a more unfriendly system; SB’s people do not read, nor understand, nor care. My wife broke under SB’s ignorance and pressure. I try not to be angry, but it is difficult – I love her (I married her 1st of March 1996 – today is our 30th anniversary and I cannot be with her – as such is our situation).

We had that problem before (we lived in a dangerous country), but a friendly Glenn, helped. This help is gone, which means people like us, who move internationally into regions, which do not work like Singapore (are not first world) should not consider Silverbullion. I still cannot believe their unhuman almost zero action (some weeks after our escape, bombs were thrown on our last home town and the president was kidnapped – ever heard of such a story?). There is no empathy, no understanding, no nothing. We had so many problems the last six months. How to get out? Where to? We needed to migrate into two countries, which means a hell of paperwork and explanations. I can understand these countries, but Silverbullion’s way to treat their customers is a shock.

-> If you live in Singapore and move from apartment 101 into apartment 102, I think there would be no problem at all.

But in case you come into real problems, I promise you, you need URGENTLY understanding.

Finally someone promised to call – but the person had a hospital situation and nobody was informed – no call came – so after another week of nothing, wife said: “I must reduce problems – I cannot have more – I bought a flight!”

I do write this to complain, but to express this HUGE difference between BS and SB, which after a lot of not ending stress broke my wife into compliance.

Sometimes it is the little things…

-> Do I prefer one over the other today? I tend to BS, as the SB system sends back frequently “a problem happened – but our people are informed” (I cannot enter then), while the BS system is stable all the time.

It feels as if BS learns from errors, while SB does not. I can only hope they send this (one month valid) form tomorrow to my wife.

Wow appreciate very much the in depth sharing from personal experience. I am sorry to hear about your situation, and I hope you manage to sort it out soon!