A question that I regularly get on Financial Horse is whether to take a fixed or floating rate mortgage.

And how long to lock it in for.

This answer changes on a regular basis, depending on where interest rates are trading, and the interest rate outlook.

Today, fixed rates (1.3%–1.8%) now match or undercut floating (SORA + 0.25%–0.40% ≈ 1.4%–1.6%) after SORA collapsed from 3% to ~1.2%.

The gap between fixed and floating has narrowed to 20–50 bps—the tightest spread in years.

For most borrowers, a short-tenor fixed (2-year) offers near-optimal value with payment certainty, while floating is a modest bet on further Fed cuts that markets view as limited.

If you ask me, I think the fixed is the better choice today, but let’s walk through the full analysis below.

The Interest Rate Environment Has Fundamentally Changed

If you took out a mortgage in 2022–2023, you remember the pain. SORA spiked above 3.6%, fixed rates breached 4%, and monthly instalments jumped hundreds of dollars almost overnight.

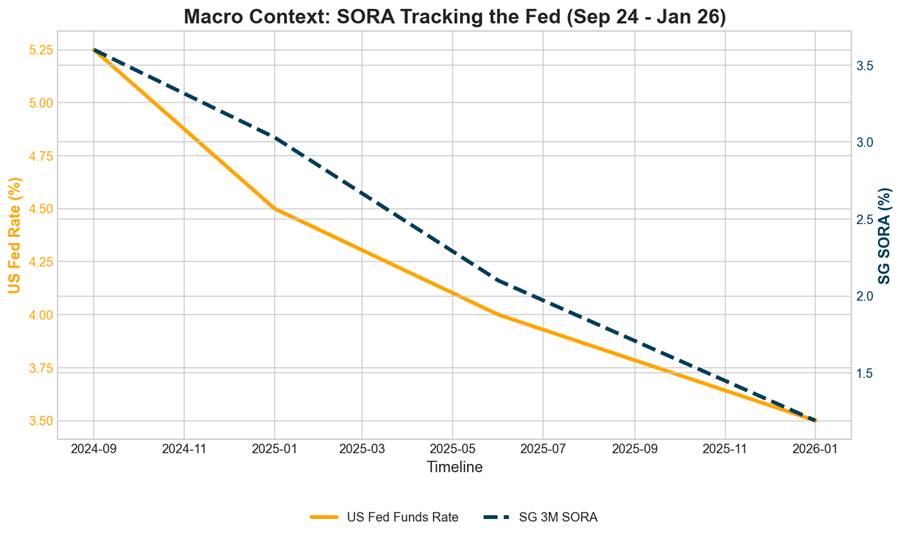

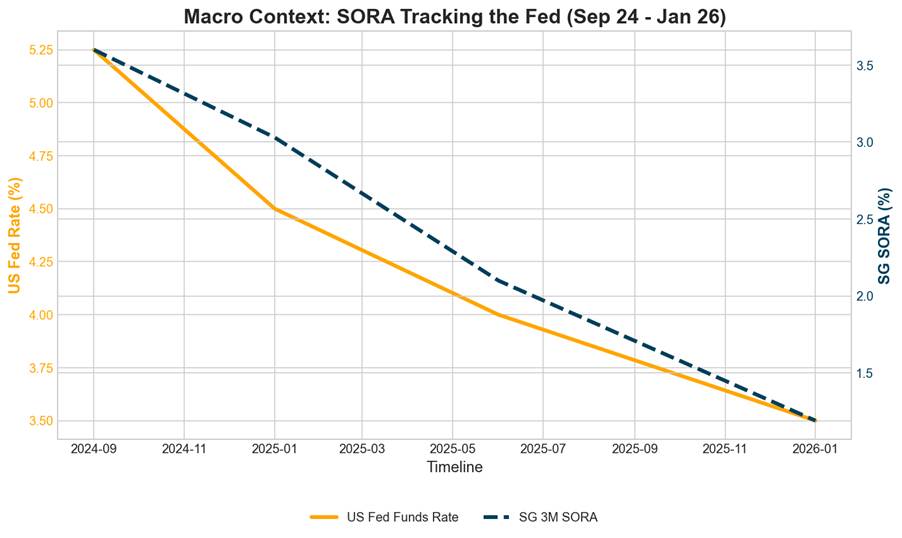

Fast forward to January 2026, and the landscape looks completely different. The 3-month compounded SORA has fallen from 3.03% in January 2025 to approximately 1.19% today. Fixed-rate packages have followed suit, with promotional rates starting from 1.30% for well-qualified borrowers.

The old playbook was simple: choose floating in a downtrend to capture savings, lock in fixed when rates bottom out. But that logic assumes a meaningful gap between fixed and floating rates. Today, that gap has compressed to just 20–50 basis points.

This changes the calculus.

Current Rate Snapshot

Here’s what the market looks like as at late January 2026:

Fixed Rates:

- 2-year fixed: 1.30%–1.55%

- 3-year fixed: 1.45%–1.75%

Floating Rates (SORA-pegged):

- 1M SORA + 0.25%–0.40% ≈ 1.35%–1.55%

- 3M SORA + 0.25%–0.40% ≈ 1.45%–1.60%

HDB Concessionary Loan: 2.60% (unchanged, pegged to CPF OA + 0.1%)

The key observation: fixed and floating are trading at near-parity. The premium you pay for payment certainty has shrunk to almost nothing.

What’s Driving Rates—and What’s Priced In

Singapore mortgage rates don’t exist in isolation. They track the US Federal Reserve and are filtered through MAS policy. Understanding where rates are headed requires understanding the macro picture.

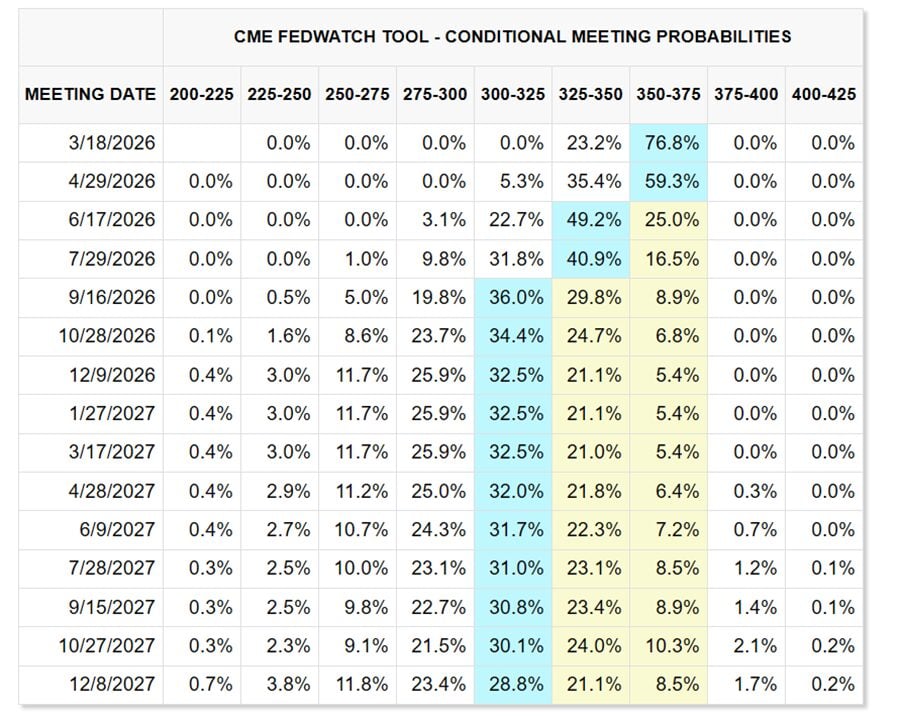

The Fed’s Path: The Fed has cut rates by 175 basis points since September 2024, bringing the federal funds rate to 3.50%–3.75%. At its January 2026 meeting, the Fed held rates steady and signalled no urgency to cut further. Market expectations point to just 1–2 cuts through 2026, with rates potentially settling around 3.0%–3.25% by year-end.

MAS Policy: The Monetary Authority of Singapore eased policy twice in 2025—its first adjustments in four years. At its January 2026 meeting, MAS held steady but raised its 2026 inflation outlook to 1%–2%, citing resilient growth and potential imported cost pressures. The message: further easing isn’t guaranteed.

SORA Trajectory: Having fallen from 3.03% to 1.19% over twelve months, SORA has likely found a near-term floor. Consensus forecasts cluster around 1.0%–1.2% through 2026, absent a major economic shock.

The bottom line: most of the rate decline is already behind us. Floating rate borrowers hoping for another 100 bps of savings may be disappointed.

The Case for Fixed Rate Mortgages

Fixed-rate mortgages lock your interest rate for a defined period—typically 2 to 3 years in Singapore. After the lock-in expires, rates revert to the bank’s prevailing floating rate.

Why Fixed Makes Sense Now:

- Near-historical lows. At 1.30%–1.55% for 2-year packages, you’re locking in rates not seen since pre-2022. Even if SORA falls further, you’re giving up perhaps 20–30 bps of upside—a rounding error over a 2-year horizon.

- Asymmetric risk protection. If SORA stays flat at 1.2%, floating saves you roughly 20 bps. If SORA rises to 2.5% (a scenario that isn’t far-fetched given sticky global inflation), fixed saves you 135 bps. The downside protection is larger than the upside sacrifice.

- Payment certainty. For owner-occupiers on single incomes or tight budgets, knowing exactly what your monthly payment will be for the next 24 months has real value. That $200–$300 swing in monthly instalments might not matter to high-income borrowers, but it matters to most households.

The Trade-offs:

- Lock-in penalties (typically 1.5% of outstanding principal) if you sell or refinance early

- Rates revert to floating after lock-in—you’ll need to actively reprice or refinance

- Opportunity cost if SORA falls materially below 1%

Best Suited For: Risk-averse borrowers, first-time buyers, owner-occupiers, households with tight cashflow, and anyone who doesn’t want to actively manage their mortgage.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

The Case for Floating Rate Mortgages

Floating-rate mortgages in Singapore are pegged to SORA plus a bank spread (typically 0.25%–0.40%). Your rate adjusts monthly or quarterly as SORA moves.

Why Floating Makes Sense:

- Marginally cheaper today. At current levels, floating rates run about 20–50 bps below comparable fixed packages. On a $500,000 loan, that’s $80–$170 per month—not trivial, but not transformative either.

- Optionality on further cuts. If the Fed accelerates its cutting cycle (say, due to a US recession), SORA could drift toward 0.8%–1.0%, and floating borrowers would capture that benefit automatically.

- Greater flexibility. Many floating packages offer shorter lock-in periods or easier conversion options. If you’re planning to sell within 2–3 years, the flexibility can outweigh the rate consideration.

The Trade-offs:

- Payment unpredictability—your instalment can change quarterly

- Limited upside remaining if SORA is already at its floor

- Risk of reversal if inflation re-accelerates

Best Suited For: Investors with rental income as a buffer, borrowers with substantial cash reserves, those planning to sell within 2–3 years, and active managers who monitor and reprice regularly.

Scenario Analysis: Stress-Test Your Decision

Let’s put numbers to the decision. Assume a $500,000 loan over 25 years.

| Scenario | SORA Path | Fixed (1.50%) | Floating (SORA + 0.35%) |

| Base case | SORA stays ~1.2% | 1.50% | 1.55% |

| Bull case | SORA falls to 0.8% | 1.50% | 1.15% |

| Bear case | SORA rises to 2.5% | 1.50% | 2.85% |

Monthly payment impact (approximate):

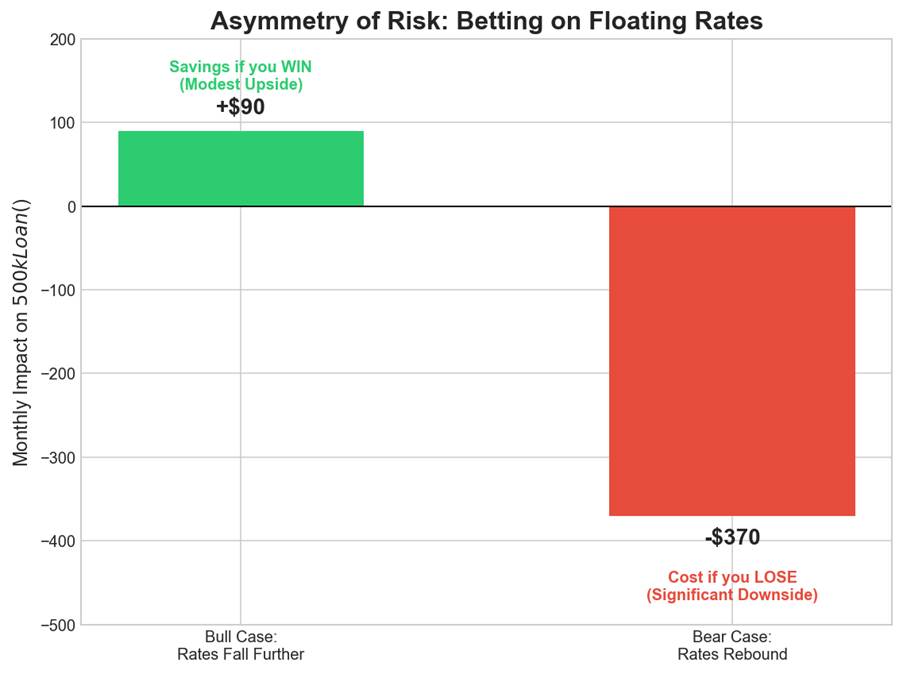

- Base case: Fixed costs ~$20/month more

- Bull case: Floating saves ~$90/month

- Bear case: Fixed saves ~$370/month

The asymmetry is clear.

You’re sacrificing modest upside (bull case savings of $90/month) to protect against meaningful downside (bear case cost of $370/month).

For most borrowers, that’s a trade worth making.

What would I do? Fixed or Floating rate mortgage?

If you ask me?

I think I would go with a fixed rate mortgage today.

Either 2 or 3 years, but leaning towards the latter for me.

The way I see it, it’s just how much you make when you’re right, vs how much you lose if you’re wrong.

If you pick floating rate mortgage today, and you’re right that interest rates go down – the amount you make is minimal.

If you pick floating rates and you’re wrong and interest rates go up, – you could lose a lot.

For me personally, this doesn’t make sense.

But hey there’s no right or wrong here.

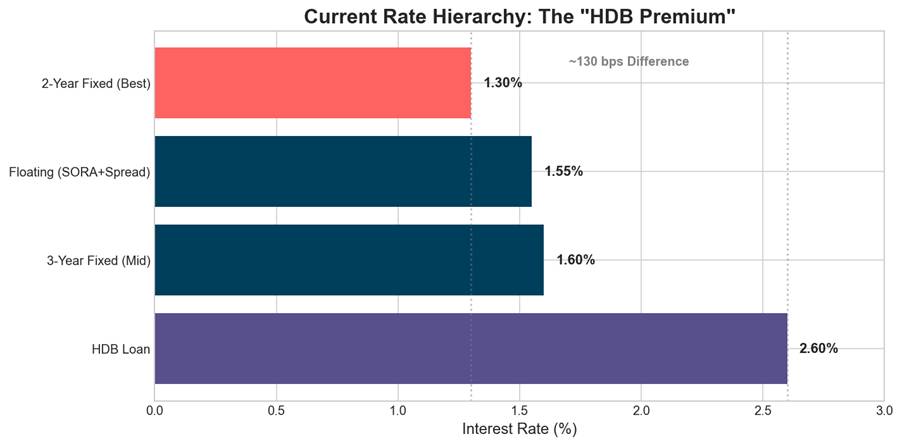

The HDB Loan Question

HDB owners face an additional decision: stick with the HDB concessionary loan at 2.60%, or refinance to a bank loan at ~1.5%?

The savings are substantial—roughly $460 per month on a $500,000 loan. That’s over $5,500 per year.

But there’s a critical catch: once you refinance from HDB to a bank loan, you cannot switch back. Ever. If rates spike in the future, you can’t return to the stable 2.60% HDB rate.

Refinancing makes sense if you’re confident in your ability to manage rate volatility over the long term, have adequate financial buffers, and understand this is a one-way door. For conservative borrowers who value the HDB loan’s stability and flexibility (lower downpayment, ability to use CPF fully), the 110 bps premium may be worth paying.

The Bottom Line

At current rate convergence, the fixed vs floating debate matters less than it did in 2022–2024. The spread is tight, the upside is limited, and the downside risk hasn’t disappeared.

For most borrowers, the rational default is straightforward:

- Lock in a 2-year fixed rate at 1.3%–1.5%. You’re securing near-historical lows with manageable lock-in risk.

- Calendar your lock-in expiry. Set a reminder to review and reprice or refinance when the lock-in ends.

- Don’t over-optimise. The difference between 1.40% and 1.50% on a $500,000 loan is $42 per month. It’s not worth losing sleep over.

For sophisticated borrowers with liquidity and active management appetite, floating still offers modest upside if SORA drifts toward 0.8%–1.0%. But the asymmetry favours fixed: you sacrifice 20–50 bps of potential upside to avoid 100+ bps of potential downside.

In a narrow-spread environment, don’t overthink it. Pick the structure that lets you sleep at night.

Or at least, that’s what I would do…

But to be absolutely clear – there’s no right or wrong here.

Pick the one that you can live with.

Use Cashew to compare latest mortgage rates

Financial Horse readers can use Cashew to compare packages across banks and check if repricing/refinancing meaningfully lowers monthly payments — fast, online, with clear side-by-side comparisons.

Cashew lets you compare bank packages and see if refinancing/repricing saves you real money – for both private & HDB properties, find out more here.