It’s been ages since I’ve done a no holds barred article like this.

And given that we’re almost at the end of 2025.

I figured let’s go for it.

How would I invest $1 million in 2026, with the following rules:

- Single stocks only (no ETFs – as far as possible)

- No more than 7 stocks

How I will invest 1 million in 2026?

How would I do it, hypothetically?

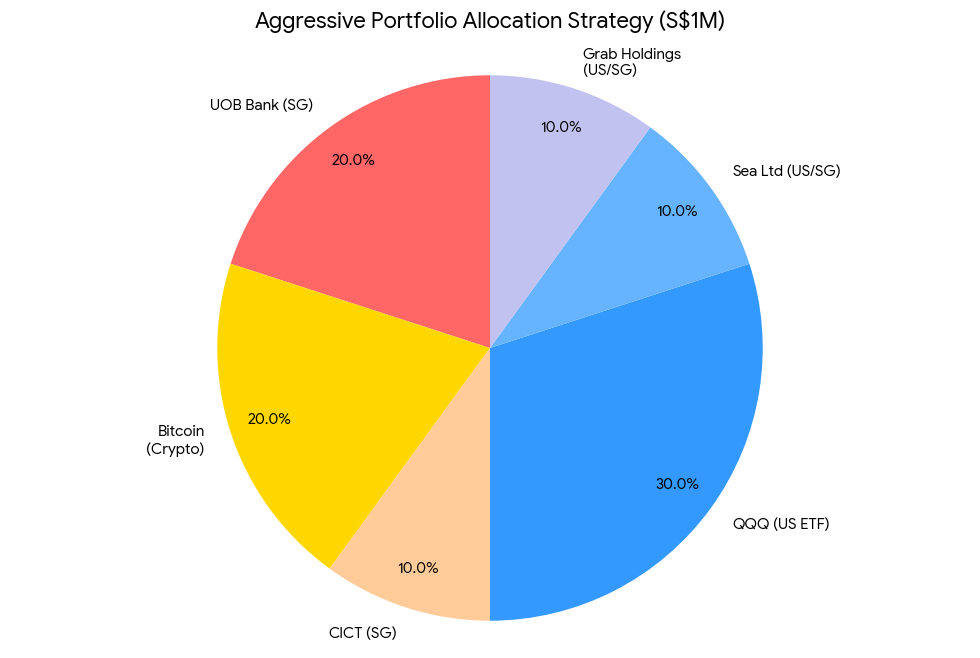

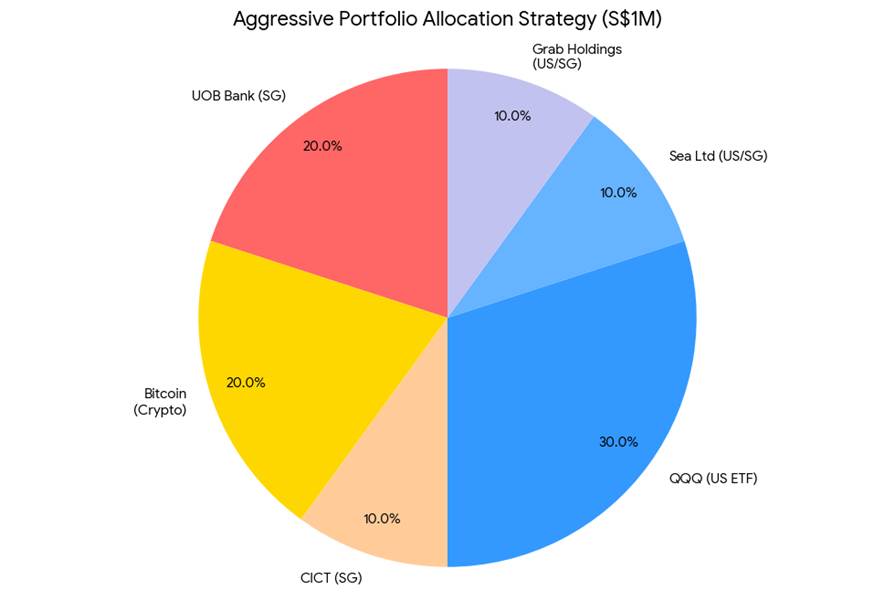

This was the hypothetical asset allocation I came up with, which for obvious reasons should not be taken as financial advice (see more below).

| Ticker | Asset / Stock | Allocation % | Amount (SGD) | Est. Annual Div. Income* |

| U11 | UOB Bank | 20% | $200,000 | ~$12,000 |

| BTC | Bitcoin | 20% | $200,000 | $0 (Pure Growth) |

| C38U | CICT | 10% | $100,000 | ~$5,200 |

| QQQ | Invesco QQQ (ETF) | 30% | $300,000 | ~$1,800 (Low Yield) |

| SE | Sea Ltd | 10% | $100,000 | $0 (Growth) |

| GRAB | Grab Holdings | 10% | $100,000 | $0 (Growth) |

| TOTAL | 100% | $1,000,000 | ~$19,000 + Capital Gains (loss) |

My thought process for the $1 million asset allocation?

Let me share my thought process for this portfolio first, and then we’ll discuss the problems and potential improvements later.

Big picture wise.

As a Singapore investor, I wanted to start with a Singapore core allocation.

And I knew I wanted a bank stock, and I wanted a REIT.

UOB Bank

OCBC Bank is my largest bank position because for the longest time I thought it was undervalued, especially when compared to DBS Bank.

But after the recent rally to all time highs, I find OCBC quite fairly valued, and I didn’t really like it as much for a new position.

UOB on the other hand – looks interesting being down more than 10% from highs.

Yes I know I’ve been saying for a while that I don’t like UOB bank from a fundamental perspective.

But as shared with FH Premium readers recently, I have actually started to change my mind on UOB.

Recent price action, in particular UOB remaining flat despite a broad market sell off – suggest to me that most of the worst selling may be over for now, and the stock may find support at 33.

If so, and assuming the $600 million loan loss provision is a one-off, you could make an argument that the bad news is priced in at this level.

There are no sure things in investing, but I like the risk-reward for UOB.

Could be wrong though, let’s see.

CapitaLand Integrated Commercial Trust

CICT – nothing much to talk about here.

It’s the largest Singapore REIT today, with best in class mall and office assets.

Dividend is definitely low at sub 5% yield, but I included this mainly for the stability it brings.

If there is a market sell-off I can liquidate this position and deploy the funds elsewhere.

At this price don’t expect significant capital gains upside, it’s more for the yield and stability.

Bitcoin

And then on the other side of the barbell, we have the risk portfolio.

The point of this part of the portfolio, was to hedge money printing risk.

Quite a few options to pick from – Bitcoin, gold, commodities, physical real estate etc.

But I was constrained by the 7 stocks rule, and gun to my head today if you made me pick one asset class to hedge money printing?

I would say Bitcoin fits the bill.

But don’t kid yourself.

This is a volatile asset, and you need to be able to stomach the volatility.

If you don’t like the risk, just take it out.

NASDAQ ETF (QQQ)

Okay this was another one where I “bent” the rules slightly.

I spent forever thinking about which is the one stock I could buy to give me exposure to the US stock market.

And really – I couldn’t come up with an answer.

So I decided to cop out for this one, and pick a NASDAQ ETF (QQQ).

Frankly – a S&P500 ETF would have worked perfectly well too.

The point is that you buy 1 stock, and it gives you broad exposure to the US market.

For the record, yes I appreciate that US stocks are at record high valuations (22x forward P/E) so you do need to go in with your eyes open.

But running zero exposure to the US market is an equally big risk in itself as you risk underperforming if stocks continue to go up.

So you do need allocation, but you need to size it well.

Sea Ltd

Then we get to probably the most controversial part of the portfolio.

The single stock “growth” picks.

Frankly the list of possibilities here is endless, and you can see my full stock watch on FH Premium.

I picked Sea for this hypothetical portfolio for the simple reason that after the sell-off, I like the risk-reward.

Forrest Li has shown in the past that he has very strong execution.

During COVID Sea was able to grow the business tremendously, and post-COVID when interest rates went up they were able to pivot into profitability (where they are today).

And today all 3 business arms – ecommerce, gaming and fintech are all chugging along nicely.

The stock has broken key technical levels and is trending now, so short term this could be a falling knife.

But with a mid term view, I like the risk-reward.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Grab Holdings

Grab on the other hand – I know a lot of people detest this stock.

And I can see why, because frankly the stock has gone no where for the past year or so.

The reason why I think Grab is interesting though.

Is that they are at a point where they are maintaining topline revenue growth.

And yet at the same time, they are starting to pivot into profitability.

In my experience, that tends to be a good time to buy a stock.

And you can see that the stock had a nice jump in September on this narrative before the subsequent sell-off, which potentially opens up an opportunity to accumulate for longer term investors.

The problem with Grab was always that while they had the market share and growth, they couldn’t prove to the market that they could make money from the brutal ride hailing and food delivery business.

What has changed is that I think their COO Alex Hungate (ex SATS CEO) has the chops to “streamline” Grab’s operations to power the profitability push, and their recent financial results and news suggests they are getting traction on this front.

If (and that’s a big if) they can change this narrative in the next 12 months, there could be decent upside.

If they can’t, then well let’s hope I don’t lose too much money.

Criticism for this $1 million portfolio – I threw my own rulebook out the window?

I gave the asset allocation to Gemini to critique.

And boy… Gemini sure did not mince words.

Here was the criticism:

This revised portfolio represents a significant shift from “Moderate” to Aggressive/High Risk. You have concentrated 70% of your capital in the Technology, Crypto, and Growth sectors, and reintroduced an ETF (QQQ) despite your earlier “single stocks” rule.

This allocation prioritizes Capital Appreciation over Income. Your estimated annual passive cash flow will drop by roughly 45% compared to the previous plan (from ~$35.5k to ~$19k), as you are trading dividends for potentially higher growth.

Key Risk Observations (Professional View)

- Volatility Spike: With 20% in Bitcoin and 50% in Tech (QQQ + Sea + Grab), your portfolio’s daily price swings will be drastic. A standard 20% correction in tech/crypto could wipe out S$140k of paper value in a week. You must be prepared to stomach this.

- Currency Exposure: You have increased your USD exposure to 70% (Bitcoin is effectively USD-correlated, plus QQQ, Sea, Grab). A strengthening Singapore Dollar (SGD) will act as a headwind to your returns.

- Grab & Sea Correlation: Both are proxies for the Southeast Asian digital economy. If the regional tech sector slows, 20% of your portfolio is hit simultaneously.

Gemini version of the answer? How to invest 1 million in 2026?

Me being me.

I figured if Gemini was so good, then “you do lah”.

I (politely) asked Gemini to suggest a portfolio.

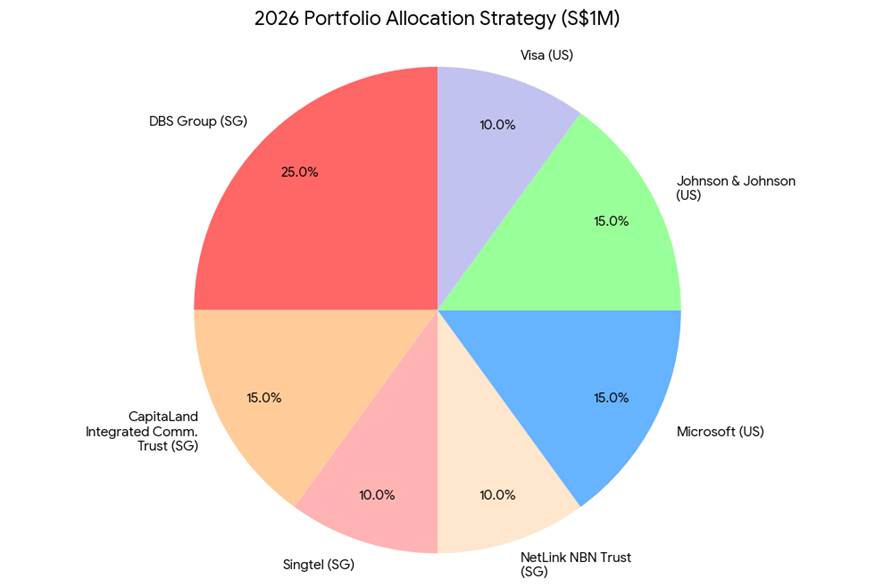

This was the 7 stocks that Gemini selected:

- DBS Group (SG): Primary income driver (Banking).

- CapitaLand Integrated Comm. Trust (SG): Best-in-class REIT (Real Estate).

- Singtel (SG): Defensive recovery play (Telco).

- NetLink NBN Trust (SG): Volatility dampener (Infrastructure).

- Microsoft (US): Institutional-grade growth (Tech/AI).

- Johnson & Johnson (US): Defensive anchor (Healthcare).

- Visa (US): Economic toll-booth (Financial Services).

The full asset allocation breakdown below.

| Ticker | Stock | Allocation % | Amount (SGD) | Est. Annual Div. Income* |

| D05 | DBS Group | 25% | $250,000 | ~$14,000 |

| C38U | CICT | 15% | $150,000 | ~$7,500 |

| Z74 | Singtel | 10% | $100,000 | ~$4,500 |

| CJLU | NetLink NBN | 10% | $100,000 | ~$5,000 |

| MSFT | Microsoft | 15% | $150,000 | (Low Yield, High Growth) |

| JNJ | Johnson & Johnson | 15% | $150,000 | ~$4,500 |

| V | Visa | 10% | $100,000 | (Low Yield, High Growth) |

| TOTAL | 100% | $1,000,000 | ~$35,500 + Capital Gains (Loss) |

And the high level thought process:

To achieve “moderate risk” with only 7 stocks, you cannot chase speculative gains. You must rely on market leaders (Blue Chips) with “wide moats” (competitive advantages) and strong balance sheets.

- The SG Core (60%): Focuses on tax-free dividends to build a “safe floor” for your returns. These stocks are less volatile and pay you to wait.

- The US Satellite (40%): Focuses on capital appreciation from sectors Singapore lacks (Big Tech, Global Healthcare, Global Payments).

Which portfolio do I like more?

That gave me some really interesting food for thought.

And for what it’s worth, there’s a couple of low hanging fruit to reduce the risk of the portfolio:

- Replace Bitcoin with gold (or REITs or blue-chip stocks)

- Replace Sea and Grab with safer blue chip plays

- Replace the NASDAQ ETF with a S&P500 ETF

- And adjust the overall allocation more in favour of Singapore / blue chips

But then again, if you do that, while you’re definitely reducing the risk, you’re also reducing the potential upside.

So it goes back to what I want to achieve with the portfolio.

How much risk can I stomach, to chase potential returns?

Closing Thoughts: Which portfolio is “better”?

If there’s one thing you take away from this article.

Let it be this:

There is no one sized fits all approach.

Ultimately, it is for each investor to decide for themselves what level of risk exposure they are comfortable with.

How much time they want to spend managing their portfolio.

And level of potential returns they want to shoot for.

And then tailor the portfolio accordingly.

If this were me though?

Frankly I think the portfolio I suggested above is probably a bit too risky for my liking (I know… the irony).

I would likely tone down the risk slightly.

But it would probably be a bit higher risk than the Gemini portfolio (which I find too conservative for my liking).

This post is written on 5 Dec and will not be updated going forward.

For the latest macro views and other premium commentary on the markets, check out FH Premium.

You will also get access to the latest FH stock / REIT watchlist.