I’ve been getting quite a few questions on investing for the next generation recently.

Here’s one:

Hi FH,

I have recently come into a pool of cash due to an inheritance.

I have 2 young kids – one three years old, and another that will be born very soon.

I want to invest the cash for the long term, to safeguard my children’s future when they grow up.

I plan to give them this money when they are big.

I am okay to make occasional changes to the portfolio, but I don’t want to have to babysit the investments too much as I have a full time job (not to mention raising 2 kids)!

Any thoughts on how I should allocate the cash, or if you can point me in a general direction.

That would be most helpful.

How I will invest $1 million for the next 20 years? (as a Singapore Investor in 2023)

The more I thought about it, the more I intrigued I got.

Most of the content we write on Financial Horse is targeted at short to mid term investing.

The 12 months to 5 years kind of timeframe.

Where you focus obsessively on what Powell is going to do next, and how the business cycle is going to play out over the next 2 – 3 years.

But here was a reader thinking about investing for a 20 year timeframe.

Over a 20 year timeframe, almost everything that happens in the short term is just noise.

Over a 20 year timeframe, your overwhelming consideration is asset allocation.

It’s not about whether you buy DBS Bank or OCBC Bank, it’s about how much money you put into stocks vs REITs vs cash.

What will the next 20 years look like?

First off – what is the next 20 years going to look like?

If I have to venture a guess, I think it’s going to look completely different from the past 20 years.

I think the next 20 years will be characterised by one word – War.

I don’t mean it on the conventional sense of a hot war with troops on the ground (although that’s already happening in Ukraine).

I mean it more in the form of an economic, trade and technological war between great powers jostling for power, that will define the world in this century.

You can already see the early stages of this “war” starting to take shape.

You have the US and its closest allies (Europe and Japan) on the one hand.

And you have China, Russia, Iran on the other hand.

And increasingly, everyone in between is being forced to choose sides (look at the Middle East, India, Korea for shifting alliances). Check out this headline for one:

The path we are currently on will take a decade or more to play out.

And the path that we are on, will lead to more protectionism, more nationalism, more government spending in the name of “national security”.

It is a path of higher structural inflation, and higher structural interest rates.

If I am right, the days of 0% interest rates, and sub 2% inflation, are over.

With massive implications for long term investing.

The second biggest question to ask – Should you buy Property, or Not?

The next big question – is whether to buy property or not.

I don’t know exactly how much cash the reader has, so I’ll just make some assumptions here.

Assuming you start out with $1 million cash.

You can set aside 40% of it, which is $400,000, to pay the upfront payment on a $1.5 million property (including stamp duty).

That’s more than enough budget to get you a decent 2 bedroom condo which you can lease out (2 bedroom tends to be the sweet spot for rental and capital gains).

Over the next 20 years, it can do pretty well.

Should you do it?

There are a number of issues to consider of course, namely:

- ABSD – will you incur ABSD by buying another property? (although you can put it in your kid’s name if you’re really desperate to avoid ABSD)

- May need to top up cash flow every month if rental < mortgage – this depends very much on your buy price, but you do need to have some cash set aside in case the rental is not enough to pay the mortgage

- Will need to manage the property – Yes, you can get an agent to manage it, but there is still a minimum amount of effort required from you as the owner. Not everybody likes this

Ultimately, this has to be a personal decision.

To get around this, I decided to create 2 sample portfolio – one with a Singapore property allocation, and one without.

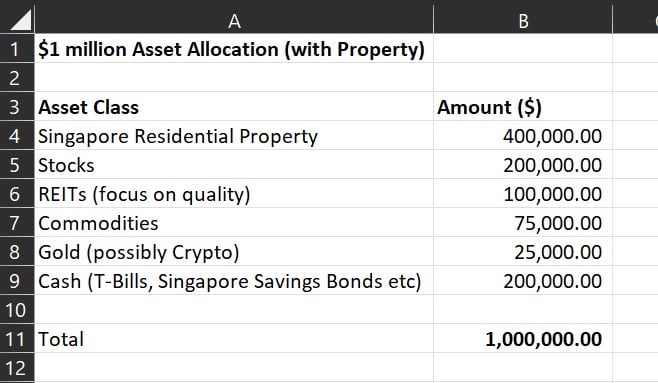

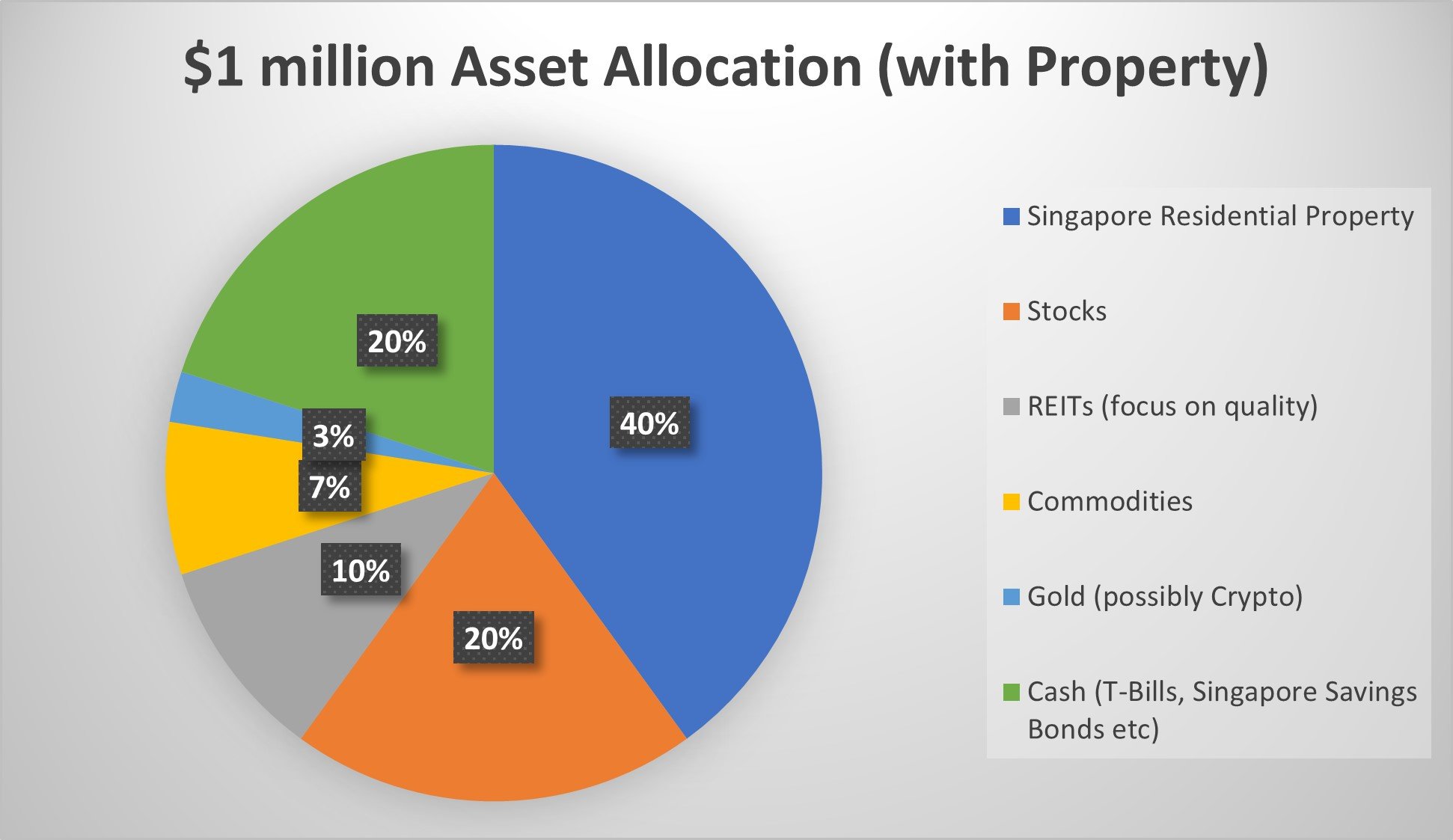

How I will invest $1 million for the next 20 years? (with Property)

For ease of reading, I will share both portfolios first.

Then I’ll share the thought process, and the key risks I see.

Here’s how I would invest a hypothetical $1 million if I bought Singapore property:

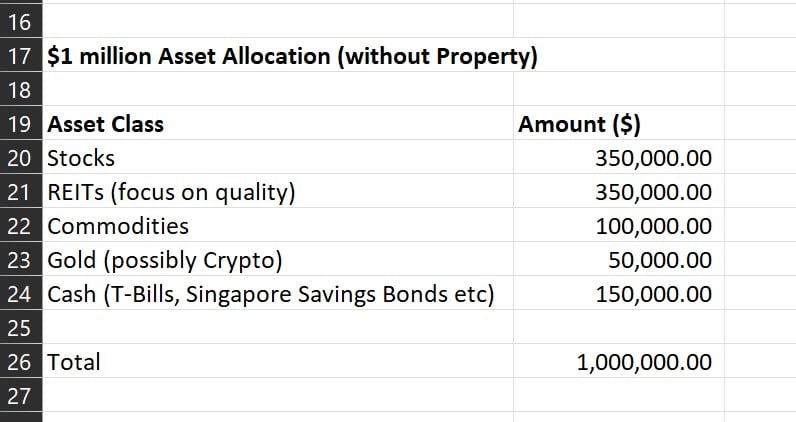

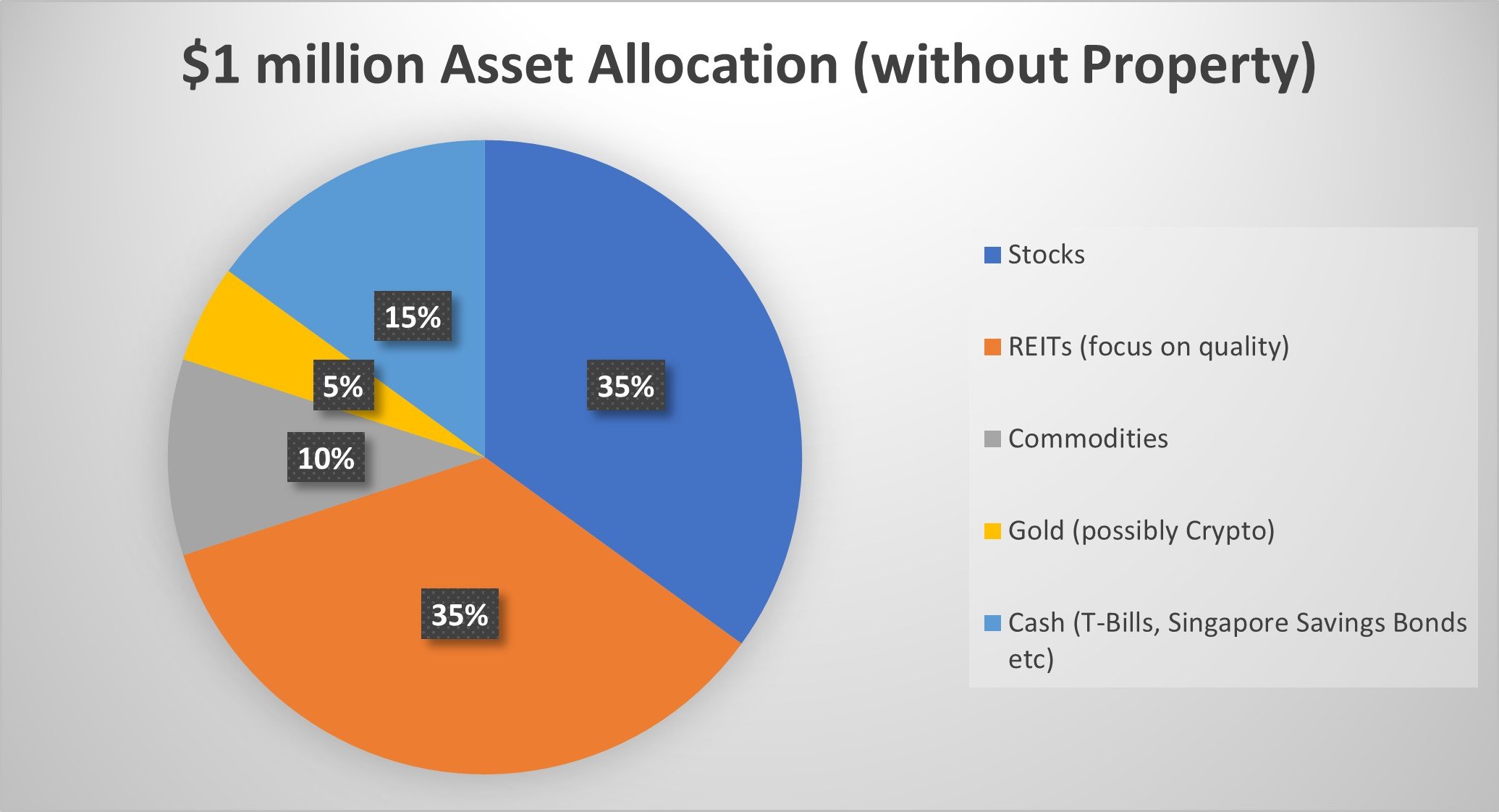

How I will invest $1 million for the next 20 years? (without Property)

And here’s how I would invest a hypothetical $1 million if I did not buy Singapore property:

How do you invest for the next 20 years? (as a Singapore Investor)

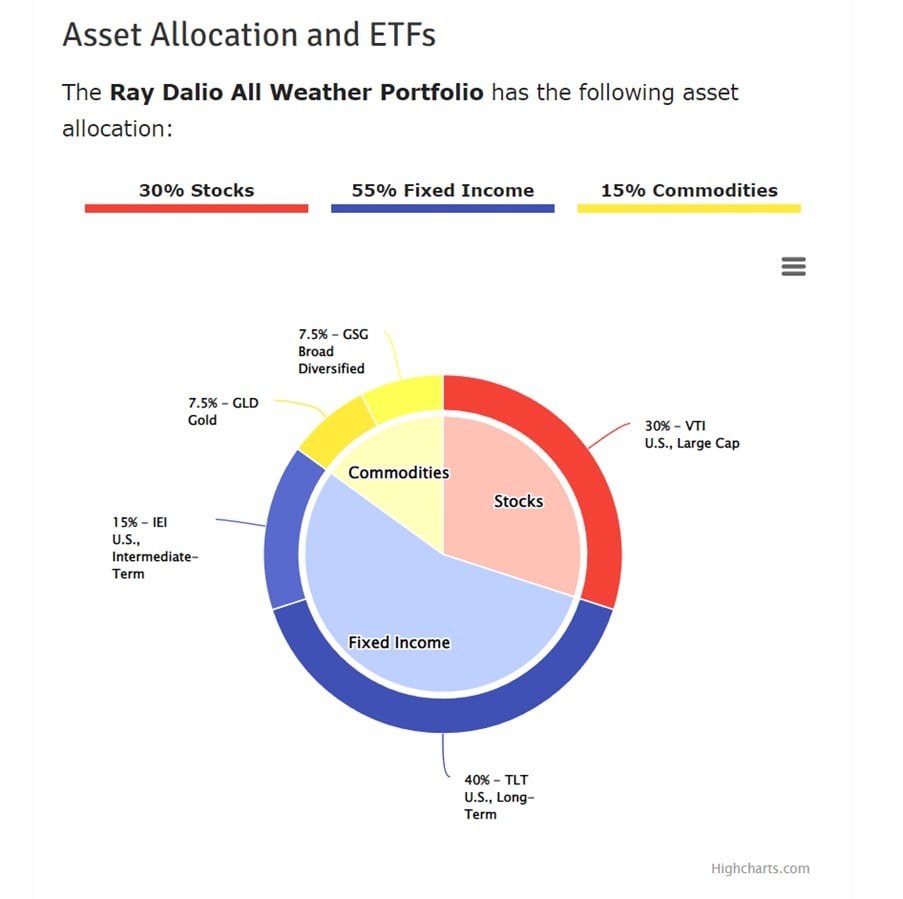

When you’ve investing for the ultra long term, the all-weather portfolio is your holy grail starting ground.

Designed by Bridgewater, it is designed to perform well in all economic situations, whether it is stagflation, or depression.

The problem with the all weather of course, is that because it is designed to do well in all economic situations.

It doesn’t do particularly well in any economic situation.

Long Term Governments Bonds is tricky this decade

And based off my view on how the next decade might play out, the long term government bonds component of the all weather worries me.

A 40% allocation to US long term treasuries makes a lot of sense when you have a 40 year period of declining interest rates where inflation is not a problem.

Moving into a period of higher geopolitical tensions, where the only way for interest rates to go is up, where inflation is a real concern.

Do you necessarily want to put 40% of your portfolio into US long term treasuries?

Not only do you take on USD FX risk over a 20 year period.

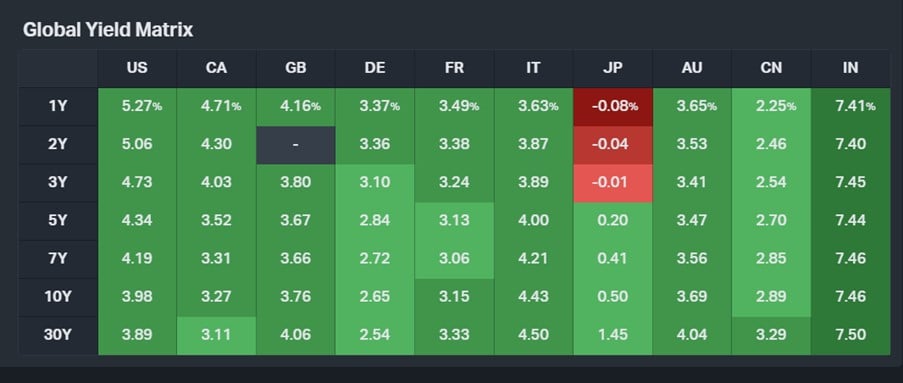

But the US 30 Year Treasury today only yields a 3.89% return if held to maturity.

If you adjust for inflation, you’re almost guaranteed to lose money if you hold a 30 Year Treasury to maturity.

I don’t know, I just think this isn’t 1990.

I don’t feel comfortable putting my 40% of my portfolio into long term US Treasuries at this stage in the debt cycle.

What about Singapore Government Bonds?

Even if you swap it out to Singapore Government Bonds – the 20 year SGS yields a pathetic 3.14%.

In a world of higher structural inflation and interest rates, long term government bonds really worry me.

The way I see it – I want to hold cash for the optionality (to buy dips) and high short term interest rates.

Or I want to hold hard assets like real estate or stocks to hedge inflation.

Not long term government bonds.

What to replace the long term government bonds with?

Ideally it would be investment grade corporate credit.

You can get pretty decent 4 – 6% yields on high quality corporate credit these days. If you stick with the blue chip issuers with a low risk of default, that’s very decent risk-reward.

The problem is that it’s not easy to buy for a Singapore retail investor.

Most of these are for accredited investors only, and go for $250,000 a pop (meaning you can’t diversify easily).

You do get the occasional retail bonds, but it’s not enough to build a diversified portfolio around.

Sure, you could ETF it via one of the bond funds.

But bond funds carry their own risks too (you can’t hold the bonds to maturity to get your principal back), and many of them don’t invest purely in SGD bonds which means FX risk.

Using REITs instead of Bonds is a risky move for the portfolio

Because of that, what I did was to switch the long term government bonds component.

Into high quality REITs / fixed income products instead.

You buy whatever high quality corporate retail bonds you can get your hands on.

And the rest can go into ultra high quality REITs from a rock solid sponsor.

Think names like Netlink Trust, Parkway Life REIT (although yield is on the low side), CICT, Mapletree Industrial etc.

You’re basically using this as a pseudo fixed income product.

You ignore the short term fluctuations in price, and just focus on the dividend yield that you collect (locked in at your buy in price).

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What are the main risks I see with both $1 million portfolios?

Because of this though – I do need to flag a big risk with both portfolios above (vs the all weather).

Because I significantly reduced the long term government bonds component.

There is no effective hedge against a big economic depression.

In a deep recession, the REITs, Stocks and commodities positions would get crushed.

Only the gold and cash component would hold its own, but that’s only 20% of the portfolio.

So you need to decide if this is a risk you can live with.

What are the potential solutions to hedge against a recession?

There are 3 potential solutions I can think of to protect against this.

Market Time

If you are savvy on market timing, one solution is to be a bit more active in your asset allocation.

As we approach the later stages of the business cycle (like now), you might dial back on the stocks / REITs and increase cash allocations.

Personally, that’s how I would run the portfolio above.

Buy and Hold

You could also just opt to just buy and hold through the volatility.

Since you’re investing for a 20 year period, you can just hold, and maybe average in with your cash.

This requires nerves of steel though.

Many people think they can do it, until they see their $1 million portfolio drop $300,000.

Back to the All Weather?

If you don’t want to market time, and you are not comfortable seeing the portfolio value crash in a recession, then I suppose you just have to go back to the all weather:

- 30% stocks

- 40% Treasuries (can throw in some SGS Bonds)

- 15% cash or T-Bills or short term bonds

- 5% gold

- 5% commodities

The 40% long term government bonds will hedge against a recession, but like I said, I do have serious concerns if you hold them for the next 20 years.

What are the main risks I see with the Property portfolio?

The other risk I see, is that the property portfolio is too heavily exposed to Singapore.

Over a 20 year period, there is a real possibility that Singapore loses its relevance.

Singapore the next 20 years, may not perform as well as Singapore the past 20 years.

I suppose if you and your kid plan to live in Singapore long term, this isn’t a problem.

If Singapore doesn’t do well, then the cost of living goes down too.

But when you’re looking at multi-decade periods like that, it does pay to think whether you want to tie your fates to Singapore like that.

I know many readers who see themselves retiring in Australia or Hong Kong.

In which case you may want to increase allocations to those countries (or even buy a property there instead).

You never know sometimes, even a senior member of our ruling party’s family decided to uproot to go to Hong Kong ????.

How geographically diverse should the Stocks / REITs component be?

Which brings us to the next question.

How much money should you allocate to Singapore.

VS to the US, or China, or Europe.

Again, only you can answer this for yourself.

Personally, I would probably overweight Singapore.

I’m cautiously optimistic about Singapore’s future, and it’s where I see myself based long term.

I’m happy to tie my fates to Singapore.

So the stock component for example, might see a 40% allocation to Singapore, 20% to China, 40% to US/Europe.

And the REITs might focus predominantly on Singapore real estate.

But hey, this is just me.

You do need to decided this for yourself.

Where do you see yourself based in the long term?

Which $1 million portfolio do I like more – with property, or without?

And finally – the million dollar question.

Of the two portfolios above, which do I like more?

The property version:

Or the no property version:

The more I think about it, the more I think I like the property version.

BUT – this is on the assumption that you won’t incur ABSD on the property purchase.

If you do, you’re paying $255,000 ABSD on a $1.5 million purchase, which is a quarter of your million dollar portfolio down the drain immediately.

Doesn’t make sense to me.

But if you don’t incur ABSD, and you have the cash flow to support the mortgage if required, and you don’t mind taking some time out to manage the property?

I know that in last week’s article I said I was not a buyer of Singapore real estate at current prices, but that’s more from a 3 – 5 year kind of perspective.

Over a 20 year period, if you plan on living in Singapore long term?

I think Singapore property is a good store of wealth over a 20 year period.

Worst case even if it doesn’t appreciate much, you leave a property to your children, to do as they please.

Do also note that in the property version I increased the cash allocation to 20% because of how illiquid property is.

You can’t cash out a property so easily like you can for stocks / REITs, so it pays to hold more cash on hand.

Closing Thoughts: How to deploy the $1 million as a Singapore Investor for 20 years?

A final note on timing.

Nobody is saying to go out tomorrow and invest $1 million in property / stocks / REITs at one go.

I think at the very least, you have to recognise that with the Feds on a crusade to crush inflation, the risks are elevated at the moment.

Powell all but called for a 0.5% rate hike at the next FOMC (up from 0.25%), showing you that the threat of inflation (and a recession to combat inflation) are very real.

At the very least, I think you would want to buy in over a period of time, to manage your risk.

But hey – exact discussions on market timing and risk-reward, that’s what the rest of Financial Horse is about.

I just penned a lengthy note for Patrons this week on how I see the short term playing out, and implications for risk assets.

Do sign up if you are keen.

As always, this article is written on 10 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

If one is looking at very long timeframe of 15-20 years, a simple, hands-off strategy is to opt for 60/40 or 80/20 portfolio at the robo-advisor that will rebalance regularly.

I think that’s exactly the point here. The 60/40 did very well the past 40 years because it was a period of secular declining interest rates and low inflation – does that hold true for the next 20 years?

You can’t answer the question without more information on the guys financial position. For example if he has debt and what his housing position is.

In his shoes I would pay down debt and upgrade the family home and look to pass it on.

Fair enough! This ultimately needs to be a personal decision, absolutely do not deny that. 🙂

Plenty to mull over. Cheers.