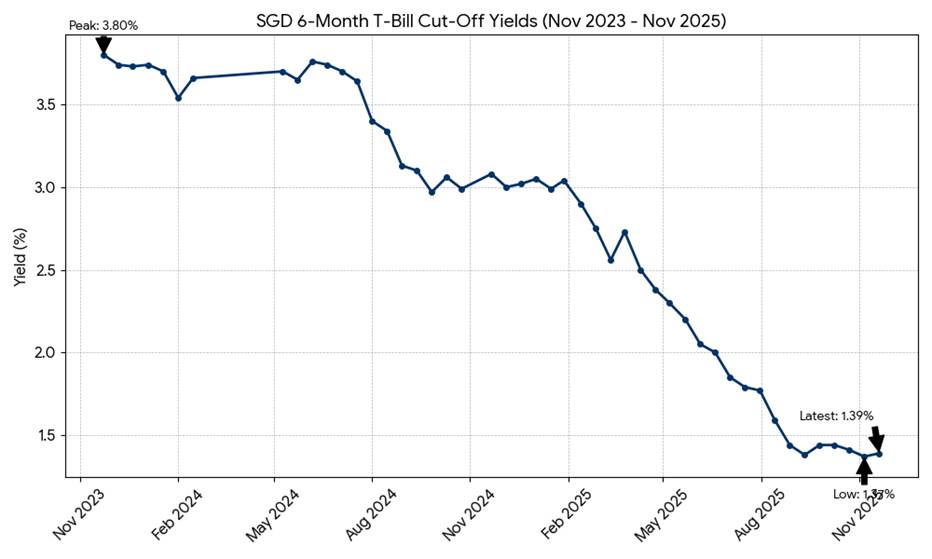

So… the latest T-Bills yield 1.39%.

And the latest Singapore Savings Bonds yield 1.35% first year, and 1.85% over 10 years.

This is a sea change from just 1 – 2 years back when you can get easily 4% yield on risk free cash.

In a climate like that.

I find it a helpful thought exercise to think about how I can invest for yield, as it helps me understand the options on the market, and what is a realistic expectation.

Put simply – let’s say I have $1 million cash, and I want to invest to get 6% dividend yield (works out to $5,000 a month).

Assuming I have a “medium risk” appetite, in that I can accept equity volatility in exchange for yield but still prioritize capital preservation over speculative growth.

How would I invest that money?

How I will invest to get $5000 a month passive dividend income – 6% yield on a $1 million portfolio?

I’ve been using the new Gemini 3 Pro (LLM) for a couple of days.

So I figured hey let’s plug the question in and see what it turns out.

And the answer – completely blew me away:

Executive Answer

Achieving a 6% yield in late 2025 is ambitious because the “risk-free” rate (Singapore Savings Bonds/T-Bills) has dropped to ~1.4% – 1.85%. To hit 6%, you cannot hold significant cash or government bonds; you must allocate heavily to dividend stocks and REITs, which pushes the risk profile from “Medium” to “Medium-High.”

Below is a constructed portfolio that targets ~5.8% – 6.0% yield by anchoring on Singapore banks (currently yielding ~5.6%–6%) and industrial REITs, using Astrea Private Equity Bonds as a lower-volatility substitute for cash.

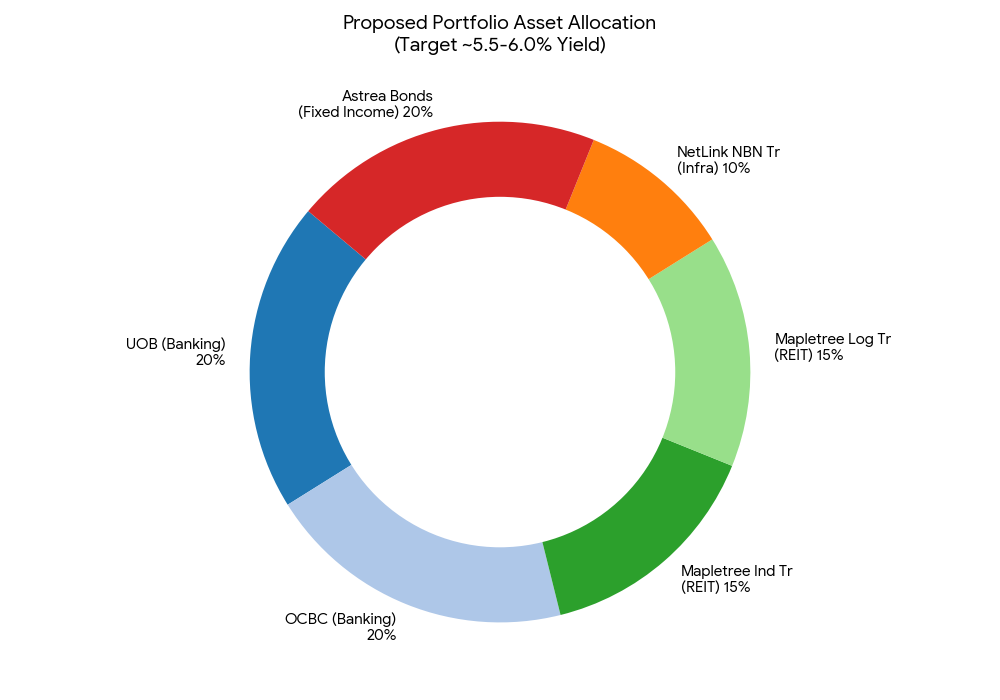

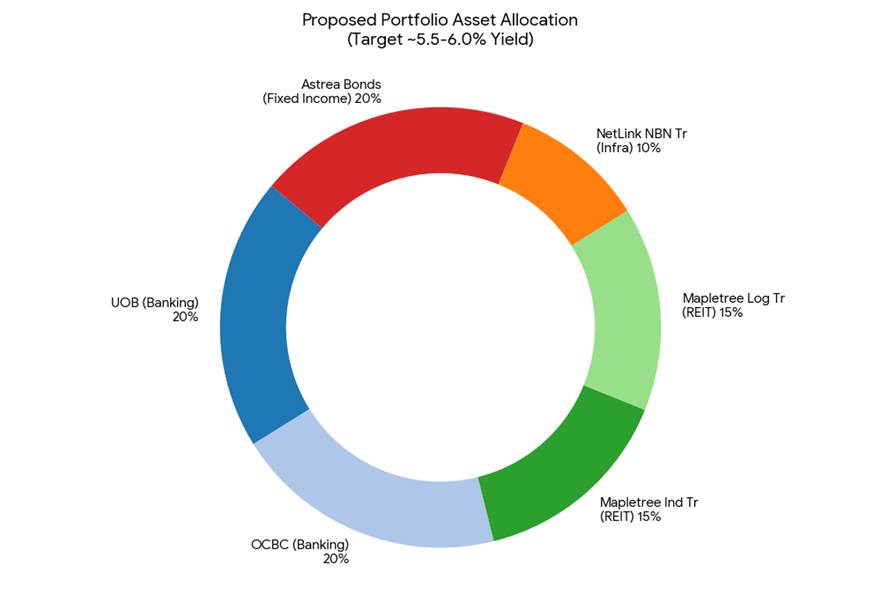

The “Target 6%” Yield Portfolio (SGD 1 Million)

This portfolio is weighted 80% Equities / 20% Fixed Income to achieve the yield target.

| Asset Class | Ticker/Instrument | Allocation | Amount (SGD) | Est. Yield | Est. Annual Income | Role in Portfolio |

| Banking (Core) | UOB (U11) | 20% | $200,000 | ~6.0% | $12,000 | Highest yielding local bank; growth & dividend mix. |

| Banking (Core) | OCBC (O39) | 20% | $200,000 | ~5.7% | $11,400 | Strong capital buffer; consistent 50% payout policy. |

| REIT (Industrial) | Mapletree Ind Tr (ME8U) | 15% | $150,000 | ~5.9% | $8,850 | Data center exposure; resilient industrial assets. |

| REIT (Logistics) | Mapletree Log Tr (M44U) | 15% | $150,000 | ~5.6% | $8,400 | Logistics exposure; slightly higher yield but sensitive to rates. |

| Infrastructure | NetLink NBN Tr (CJLU) | 10% | $100,000 | ~5.4% | $5,400 | “Bond-like” equity; monopolistic fibre network assets. |

| Fixed Income | Astrea 8/9 Class A-1 | 20% | $200,000 | ~4.3% | $8,600 | Crucial Ballast. Safer than equity, yields more than SSBs. |

| TOTAL | 100% | $1,000,000 | ~5.5% | $54,650 | Blended Yield |

Thought Process behind this dividend portfolio asset allocation?

I asked Gemini to flesh out the thought process, and this was what it shared:

“1. The Banking Engine (40% Allocation)

Singapore banks are the best “risk-reward” play for income right now.

- Why UOB/OCBC over DBS? While DBS is excellent, its yield has compressed to ~4.0%–5.6% (depending on entry price) due to share price appreciation. UOB and OCBC currently offer higher yields (~6%) and better valuations for a pure income investor.

- Risk: They are cyclical. If a recession hits, loan growth slows, and dividends could be cut, though they are well-capitalized.

2. The REIT Yield Boosters (30% Allocation)

REITs struggle when interest rates rise, but with rates falling in late 2025, they become attractive again.

- Mapletree Twins (Industrial & Logistics): These are blue-chip REITs. They offer ~5.6–5.9% yields. They are safer than retail/commercial REITs which face structural headwinds.

- Avoid: US Office REITs (too risky) or small-cap REITs (liquidity risk), even if they yield 8%+.

3. The “Ballast” (30% Allocation)

- NetLink NBN Trust: This is technically an equity but acts like a bond. It owns the fibre cables in your home. It creates predictable cash flow (~5.4%) that doesn’t fluctuate much with the economy.

- Astrea Private Equity Bonds (Class A-1): These are bonds backed by cash flows from private equity funds. They are accessible to retail investors on SGX (e.g., Astrea 8 or 9) and yield ~4.3%. They are significantly safer than stocks but yield much more than the 1.85% Singapore Savings Bond.

Important Risks for 2025/2026

- Reinvestment Risk: As interest rates fall globally, banks may lower their net interest margins, potentially reducing dividends in 2026.

- Fixed Income Drag: Because “safe” money (T-bills) pays so little (~1.4%), holding any cash drags your average yield down. You are forced to take risk to get yield.

- Concentration: This portfolio is heavily exposed to the Singapore economy and Property market.”

My thoughts? What I may do differently if I were investing?

For a first cut response with minimal prompting from me, I was really impressed.

Sure this is not a perfect one sized fits all solutions.

But it gets the big picture details right, and it gets you about 80% of the way to the answer.

Layer on the final 20% of thinking for your personal situation, and you might have a pretty good solution.

Looking deeper at the proposed portfolio, I have 2 big comments.

Replace Astrea bonds with a Bond fund

Parking $200,000 in Astrea Bonds – I’m not sure I would be fully comfortable with that.

Yes the Astrea series of bonds are traded on the SGX – but just look at the trading volume below (I pulled this before lunch on a trading day).

0 trading volume for many names, and 30,000 volume for the highest volume Astrea 9A2.

Trying to build a $200,000 portfolio of these Astrea bonds – or worst still trying to exit and get your money back in a hurry.

That’s just not going to be fun.

And sure Astrea Bonds are probably low risk, but that’s still quite a bit of concentration risk there.

I would probably replace this with a diversified bond fund.

Not only do you get diversification, you also get better liquidity in that you can redeem the units early if you need the cash.

Personally I might focus on Investment Grade corporate credit and make sure its SGD hedged.

In this market, something like PIMCO GIS Income Fund probably yields about 4.5-5.5% yield depending on the price you buy it at.

That could be an alternative to consider.

Replace the REITs

Gemini is great and all.

But picking specifically Mapletree Logistics Trust and Mapletree Industrial Trust?

Okay this one just flat out baffles me.

I get the logic behind putting 30% of the portfolio into REITs.

But these 2 REITs at 15% allocation each?

Yeah… nope.

Every time I write an article on REITs I get a ton of questions from readers asking why not buy a REIT ETF.

And this time, I actually agree that instead of picking REITs, just putting the 30% into a REIT ETF might be a pretty good idea.

You get the diversification, and you don’t need to bother with stock picking.

That said I love REITs and I’m familiar with them, so if this were me I’ll probably still stock pick single REITs.

Names like CICT, Frasers Centrepoint Trust, Starhill Global, Netlink Trust, Ascendas REIT are what I might consider.

In any case, you can see my full portfolio on FH Premium, where I allocate a healthy chunk of my portfolio into REITs and Bonds given the lower interest rate climate (I also own growth stocks like US tech and Bitcoin etc).

But… this portfolio only yields 5.5% dividend yield?

Okay let’s deal with the elephant in the room.

This portfolio only yields 5.5% dividend yield.

What if we want to get to 6.0%?

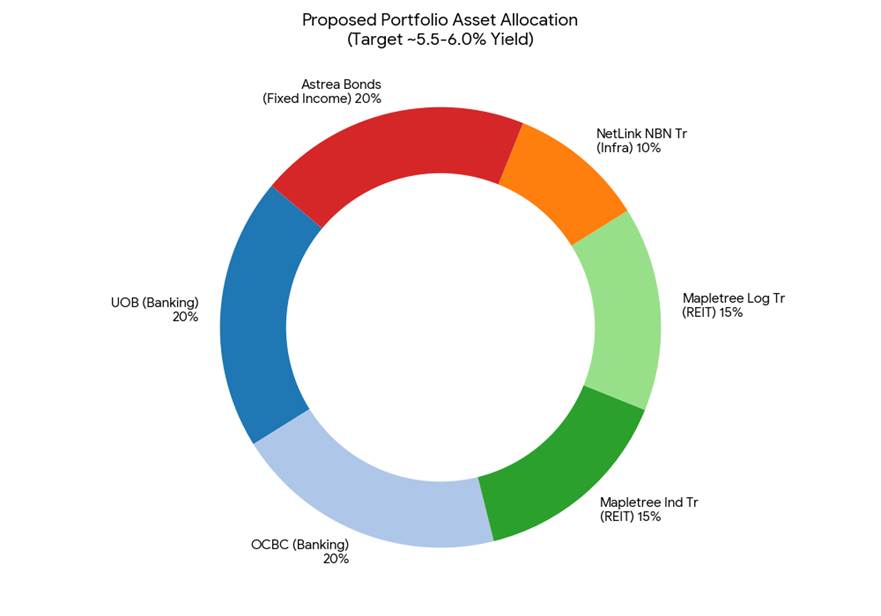

| Asset Class | Ticker/Instrument | Allocation | Amount (SGD) | Est. Yield | Est. Annual Income | Role in Portfolio |

| Banking (Core) | UOB (U11) | 20% | $200,000 | ~6.0% | $12,000 | Highest yielding local bank; growth & dividend mix. |

| Banking (Core) | OCBC (O39) | 20% | $200,000 | ~5.7% | $11,400 | Strong capital buffer; consistent 50% payout policy. |

| REIT (Industrial) | Mapletree Ind Tr (ME8U) | 15% | $150,000 | ~5.9% | $8,850 | Data center exposure; resilient industrial assets. |

| REIT (Logistics) | Mapletree Log Tr (M44U) | 15% | $150,000 | ~5.6% | $8,400 | Logistics exposure; slightly higher yield but sensitive to rates. |

| Infrastructure | NetLink NBN Tr (CJLU) | 10% | $100,000 | ~5.4% | $5,400 | “Bond-like” equity; monopolistic fibre network assets. |

| Fixed Income | Astrea 8/9 Class A-1 | 20% | $200,000 | ~4.3% | $8,600 | Crucial Ballast. Safer than equity, yields more than SSBs. |

| TOTAL | 100% | $1,000,000 | ~5.5% | $54,650 | Blended Yield |

2 ways to get to 6% yield – take more risk, or get active

There are 2 ways to do it.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Take on more risk (or wait for a market pullback)

This portfolio yields approximately 5.5%. To bridge the gap to 6.0% ($60k/year) without adding speculative REITs or stocks, you would need to:

- Reduce Fixed Income: Swap the Astrea Bonds for more UOB or REITs, raising the risk.

- Tactical Entry: Buy during market dips. Yields rise as prices fall. If UOB drops 5%, its yield pushes past 6%.

1 means taking on more risk which really depends on risk appetite.

2 requires opportunistic buying, market timing, and just getting lucky.

Both are frankly not great options in my view.

What if you use leverage?

There is another way to do it.

And that is via leverage.

On a 1 million portfolio, IBKR will lend SGD at 3.47% interest rate.

If you borrow at 3.47% and invest in 5.5% yielding stocks, the yield spread may just be enough to push the portfolio yield to 6.0%.

So I got Gemini to run the numbers for me:

The “Leveraged 6%” Plan (20% Leverage)

Here is how the numbers work if you take a SGD 200,000 margin loan (conservative 20% leverage) to buy more shares of UOB and Mapletree Industrial Trust.

| Unleveraged (Base) | Leveraged (Proposed) | |

| Your Capital | $1,000,000 | $1,000,000 |

| Margin Loan | $0 | + $200,000 |

| Total Assets | $1,000,000 | $1,200,000 |

| Asset Yield | ~5.5% | ~5.5% |

| Gross Income | $55,000 | $66,000 |

| Loan Interest | $0 | ($7,000) (at ~3.5%) |

| Net Income | $55,000 | $59,000 |

| Net Yield | 5.5% | 5.9% |

Result: You generate an extra $4,000/year of passive income. If you pick specifically higher-yielding assets (like UOB at 6%) with the borrowed funds, your net yield comfortably crosses 6.0%.

1. The Opportunity: “Arbitraging” the Rate Cut

- The Spread: In late 2025, the Singapore Overnight Rate Average (SORA) has stabilized.

- Cost of Debt: ~3.5% – 4.5% (depending on your broker).

- Yield of Asset: ~5.8% – 6.0% (Banks/REITs).

- Profit: You pocket the difference (~2.0%).

- Broker Choice is Critical:

- Local Bank Brokerages (e.g., DBS Vickers, OCBC Sec): Often charge 4.5% – 5.25%. The spread is too thin; the risk is not worth it.

- Discount Brokers (e.g., IBKR, Moomoo, Tiger): Typically charge Benchmark + 1.5% (approx. 3.5% total). This is where the math works best.

2. The Risks (Must Read)

Leverage is a double-edged sword. It amplifies gains but also amplifies losses.

A. The “Margin Call” Risk

- Scenario: If the market crashes, the value of your $1.2M portfolio drops, but your $200k loan stays fixed.

- Trigger: If your portfolio drops by ~30–40%, the broker will demand you deposit cash immediately or they will sell your stocks at the bottom to cover the loan.

- Mitigation: Your Loan-to-Value (LTV) with a $200k loan on $1.2M assets is only 16.6%. Banks typically lend up to 70% on blue chips. You have a massive safety buffer. The market would need to fall >50% (a Depression-level event) to trigger a forced sell.

B. Interest Rate Risk

- Margin loans are floating rate. If the Fed/MAS raises rates back to 2024 highs, your borrowing cost could jump to 5%+, erasing your profit spread. You must be prepared to pay off the loan if rates spike.

C. Psychology Risk

- Can you sleep at night knowing you owe $200,000? If seeing your portfolio drop $50k in a bad month causes you panic, do not use leverage.

My personal thoughts?

My simple view is that for 80% of retail investors out there, I’m just going to say you should not touch leverage.

In which case you either accept a lower 5.5% yield and accept this is all you get for a medium risk appetite in this market.

Or you go into more active market timing strategies, where you try to buy opportunistically on dips, you stock pick etc.

Or you increase risk exposure.

But for the remaining 20% of investors who are comfortable to use leverage?

To be fair I would say 20% leverage on a $1 million portfolio that is primarily invested in blue chip stocks is probably manageable.

Even if you get a market crash, with a 20% LTV you need a fairly big market correction before you would be at risk of margin call.

But to be absolutely clear – once you start using leverage you go into a whole new area of risk management, because in a market crash you can no longer just hold and wait for the market to recover.

My personal view – touching leverage just to bring the portfolio yield from 5.5% up to 6.0%, I think that’s a step too far for me.

Closing thoughts

Couple of key takeaways for me.

First is that in this climate, you can probably build a 5 – 5.5% dividend yield portfolio for moderate risk, that should be fairly achievable.

But 6.0% requires either taking on more risk, or some active portfolio management.

Whatever the case, I like to barbell my portfolio these days.

On one end build dividend yield with REITs, bonds, cash instruments etc.

And on the other end build growth with US tech, stocks, Bitcoin etc.

And adjust the allocation to each end of the barbell based on risk appetite.

You can see my full personal portfolio and what I am investing in on FH Premium.

I actually took the opportunity with the recent market sell-off to add to my stock positions, which I will update on FH Premium.

This post is written on 27 Nov and will not be updated going forward.

For the latest macro views and other premium commentary on the markets, check out FH Premium.

You will also get access to FH stock / REIT watchlist.