So I received this question from a reader recently.

“Dear FH,

I am subscriber of Dividend Investing Masterclass. I like your style of analysis and investing decision making process.

I am in my mid 50s and have retired from corporate world at 50. I have recently sold my condo and expected to receive a proceed of S$3.0m in September. I do not own any property after this sale. Therefore I need to buy a house in the near future.

I can consider:

(a) buying a HDB and keep the rest of the money for investment or

(b) buy a condo for flipping over next 3 years as I might not have enough fund for retirement if I keep the condo.

With the current tariff war, I am concern about able to sell the condo with a profit in 3 years time while incurring rental cost.

My plan will probably go with the first option. That is to buy a HDB and keep the balance of the money for dividend investing.

My wife and myself have RA that will be paying about 2.1k per month for each of us upon reaching 65 years. In addition, we have a annuity which will be paying out 1.4k per month upon reaching 65 as well.

Assuming we buy a HDB that will cost about 1m inclusive of renovation, we will have a balance of 2.0m for yield investing.

I would prefer to be conservative in this investment.

How should we allocate the fund between share/ REITS and bond?

I am targeting to get a yield of about 4% without incurring too much risk.”

This is an FH Premium post written earlier this week.

I am making this available to all readers in hopes that the thought process may be helpful for others out there.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

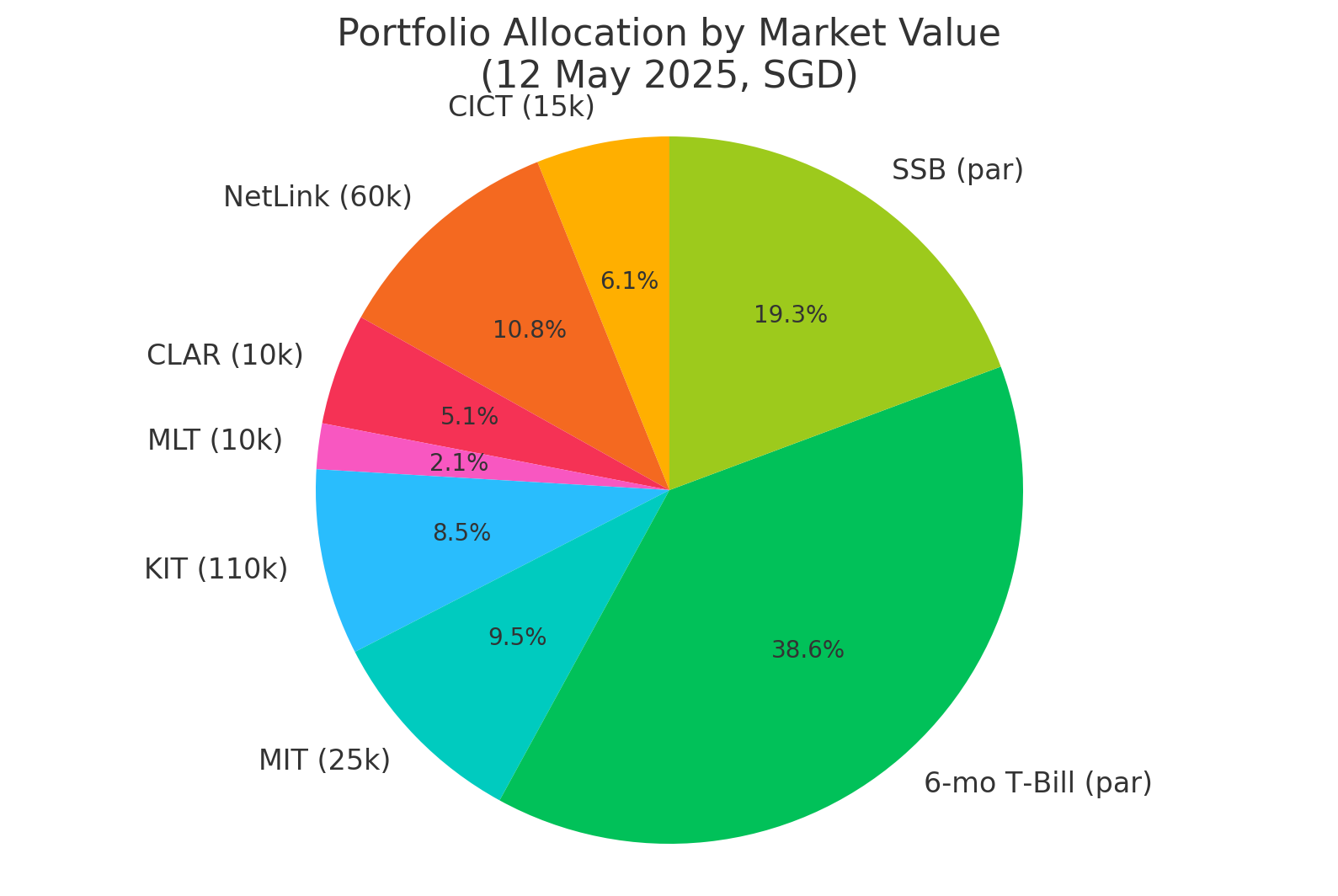

What is the current dividend portfolio the investor has?

The investment portfolio of the reader is largely broken down as follows (amended to protect privacy)

| Holding | Units | Last price (S$) | Market value (S$) |

| CapitaLand Integrated Commercial Trust (CICT) | 15 000 | 2.07 | 31 050 |

| NetLink NBN Trust | 60 000 | 0.895 | 53 700 |

| CapitaLand Ascendas REIT (CLAR) | 10 000 | 2.64 | 26 400 |

| Mapletree Logistics Trust (MLT) | 10 000 | 1.08 | 10 800 |

| Keppel Infrastructure Trust (KIT) | 110 000 | 0.395 | 43 450 |

| Mapletree Industrial Trust (MIT) | 25 000 | 1.96 | 49 000 |

| 6-month T-Bill (maturing end-Jul, held in CPF-OA) | — | — | 200 000* |

| Singapore Savings Bonds (principal) | — | — | 100 000* |

| Total portfolio | — | — | 514 400 |

What is the current yield on the dividend portfolio? How much dividend income per month?

Crunching the numbers on the current dividend yield – gives us a blended portfolio yield of about 4.26% yield on the current portfolio.

On S$500,000, that’s about $20,000+ a year in dividend income.

Or $1830 a month in dividend income.

The actual yield is probably higher because the T-Bills and Singapore Savings Bonds likely were bought some time back and have higher yields than the latest ones, but let’s stay big picture here.

| Holding | Mkt value* | Est. yield | Est. yearly income (S$) |

| CapitaLand Integrated Commercial Trust (CICT) | 31 050 | 5.17 % | 1 605 |

| NetLink NBN Trust | 55 800 | 5.81 % | 3 242 |

| CapitaLand Ascendas REIT (CLAR) | 26 400 | 5.78 % | 1 526 |

| Mapletree Logistics Trust (MLT) | 10 800 | 7.46 % | 806 |

| Keppel Infrastructure Trust (KIT) | 44 000 | 9.87 % | 4 343 |

| Mapletree Industrial Trust (MIT) | 49 000 | 6.92 % | 3 391 |

| 6-month T-Bill (CPF-OA, mat. Jul-25) | 200 000 | 2.30 % | 4 600 |

| Singapore Savings Bonds (SSB) | 100 000 | 2.49 %† | 2 490 |

| Total estimated income | — | — | 22 002 |

| Portfolio-level yield | — | ≈ 4.26 % | — |

* Market values use the last-close prices from 9-10 May 2025.

† First-year coupon of the May-2025 SSB issue; later years step up slightly.

What is the dividend income on the new S$2.5 million portfolio?

Assuming the investor sells the condo and buys a HDB, that will leave about S$2 million to be invested.

Together with the existing S$500,000, that’s a total combined portfolio of about $2.5 million.

At 4% yield that is about $100,000 a year dividend income.

Or $8300 a month.

But remember the investor also said that:

“My wife and myself have RA that will be paying about 2.1k per month for each of us upon reaching 65 years. In addition, we have a annuity which will be paying out 1.4k per month upon reaching 65 as well.”

That works out to almost another $5,600 at 65.

Adding that up is a total of $13,900 a month for the household.

Based on today’s prices that’s definitely pretty comfortable (unless you have a really high standard of living).

But given the investor has about 10 years to go until 65, you do need to factor in inflation.

If the cost of living continues to go up as quickly as it did the past 5 years, this could spell trouble for a dividend portfolio that does not have growth potential.

How I would invest to get a 4% yield without a lot of risk?

With that in mind – how would I invest, assuming this were me?

Broadly, the big asset classes I would consider buying are

- Dividend stocks

- REITs

- Bonds

- Cash

- Stocks for capital gains (or Gold/Bitcoin)

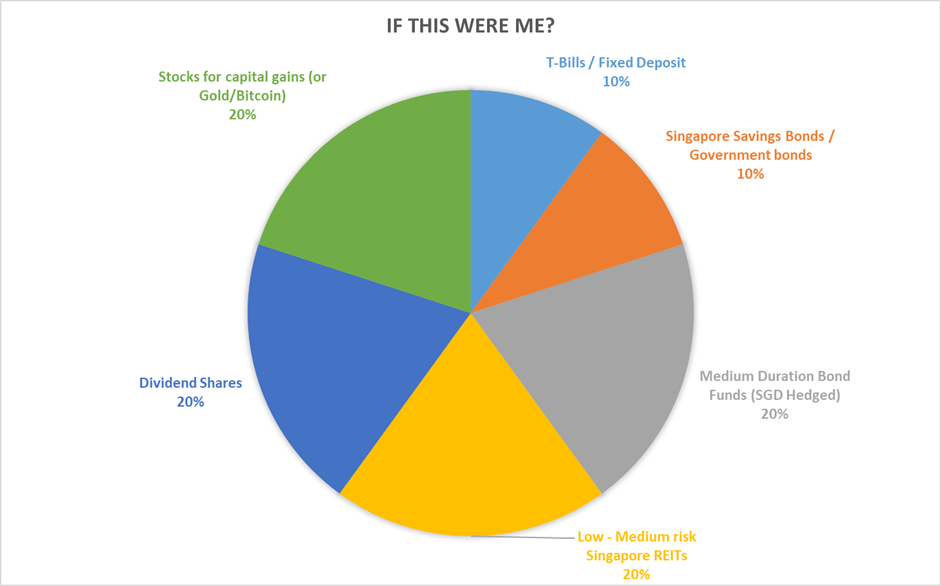

If this were me? How would I allocate the dividend portfolio?

If this were me?

I think I might use an asset allocation like the below.

| Asset Class | Instrument | Amount | Dividend Yield | Dividend per year |

| Cash | T-Bills / Fixed Deposit | 250,000.00 | 2.30% | 5,750.00 |

| Bonds | Singapore Savings Bonds / Government bonds | 250,000.00 | 2.50% | 6,250.00 |

| Bonds | Medium Duration Bond Funds (SGD Hedged) | 500,000.00 | 5.00% | 25,000.00 |

| REITs | Low – Medium risk Singapore REITs | 500,000.00 | 5.00% | 25,000.00 |

| Shares | Dividend Shares | 500,000.00 | 5.00% | 25,000.00 |

| Shares | Stocks for capital gains (or Gold/Bitcoin) | 500,000.00 | 0.00% | – |

| Portfolio Level | 2,500,000.00 | 3.48% | 87,000.00 |

My thought process for portfolio construction? Inflation is one of my biggest fears?

And yes – for the record, I know that this blended yield of 3.5% falls below the 4.0% target set by the reader.

The reason why is largely due to the $500,000 allocation to capital gains stocks / bitcoin / gold.

Personally, I felt this was important because for someone in their mid-50s.

Assuming live expectancy of mid 80s, that’s about another 30 years to go.

Another 30 years to go in one of the higher cost of living countries in the world (Singapore).

You absolutely need to factor in the possibility of inflation.

My concern was that a pure dividend yield focussed portfolio may not keep pace with inflation sufficiently.

Whereas with an allocation to capital gains stocks / Bitcoin / Gold could provide a potential hedge against inflation.

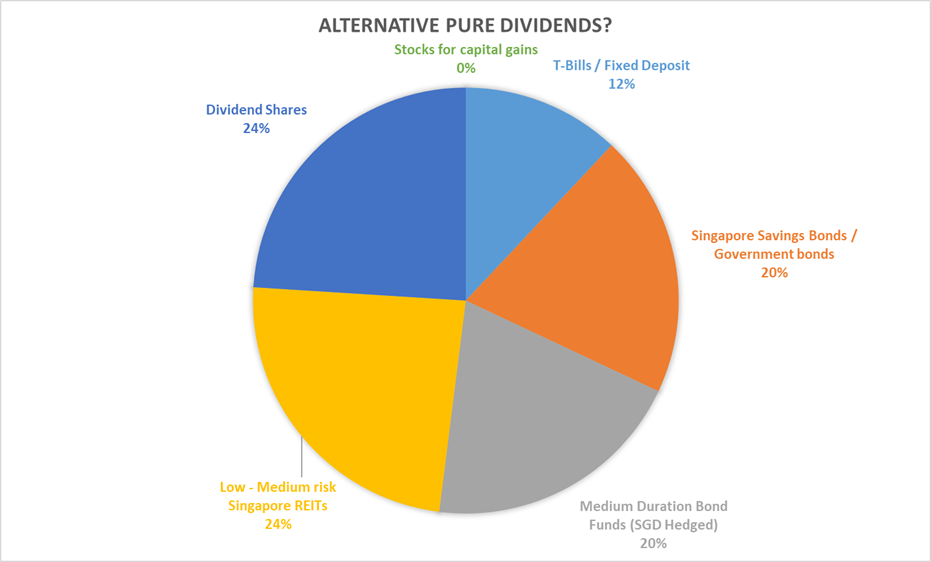

What if I wanted to invest in a pure dividend portfolio?

But since I was at it.

I also decided to think about how I would allocate if I were investing in a pure dividend focused portfolio.

And I came up with the below:

| Asset Class | Instrument | Amount | Dividend Yield | Dividend per year |

| Cash | T-Bills / Fixed Deposit | 300,000.00 | 2.30% | 6,900.00 |

| Bonds | Singapore Savings Bonds / Government bonds | 500,000.00 | 2.50% | 12,500.00 |

| Bonds | Medium Duration Bond Funds (SGD Hedged) | 500,000.00 | 5.00% | 25,000.00 |

| REITs | Low – Medium risk Singapore REITs | 600,000.00 | 5.00% | 30,000.00 |

| Shares | Dividend Shares | 600,000.00 | 5.00% | 30,000.00 |

| Shares | Stocks for capital gains | – | 0.00% | – |

| Portfolio Level | 2,500,000.00 | 4.18% | 104,400.00 |

My thought process for portfolio construction?

This would hit the 4% target set by the reader, and then some.

But like I said, my concern with this portfolio is that the dividends lulls you into a false sense of security.

You think you are safe and comfortable with $13,900 a month in dividend income at 65.

Only to find that because of increase in cost of living, the $13,900 no longer buys you as much as it did 10 years ago.

Even less so at 75.

This portfolio will hedge inflation in some ways from the dividend shares.

For example a stock like DBS Bank has the potential to raise dividends over time, acting as an inflation hedge.

But by and large, I don’t think this portfolio would hedge inflation as well as the one above with meaningful allocation to stocks / gold / bitcoin with capital gains potential.

What would I consider buying for bonds, REITs and stocks?

I don’t want this article to turn into financial advice, so I am going to keep the discussion high level and talk mostly about broad asset classes.

But I figured some level of discussion into what I would look at when choosing what Bonds / REITs / Stocks to buy would be helpful.

REITs

The problem with REITs in this new paradigm, is that this is a climate of much higher interest rate volatility.

I don’t think we are ever going back to zero interest rates (at least not for an extended period of time).

And this has huge implications for REIT prices.

That being said, as a Singapore investor, who wants to build a dividend portfolio, I don’t think you can get away without including at least some REITs.

A blue-chip REIT like CapitaLand Integrated Commercial Trust or CapitaLand Ascendas REIT pays about 5%+ dividend yield today.

That’s actually pretty decent being almost a 3.0% yield spread vs the latest Singapore 10 year government bond:

This being a conservative portfolio I would stick to blue chip REITs with a strong sponsor and balance sheet, and focus primarily on high quality Singapore real estate.

You can see the list of REITs I am looking at on FH Premium.

Dividend Stocks

For Singapore dividend stocks you have of course the obligatory DBS Bank, UOB Bank, OCBC Bank.

All pay about 5% dividend yields today.

And just like REITs, Banks are probably the other bedrock of a Singapore dividend portfolio, so you can’t really get away from this.

But what about other dividend stocks?

Here I actually think there is good opportunity for stock picking.

For example – Singtel pays about a 5% dividend yield and the chart has just broken out:

ST Engineering meanwhile has a monster of a chart, but at 1.7% yield I find it hard to call this a dividend stock anymore.

Point here, is that in this new paradigm of US-China conflict, and investors shifting marginal capital away from US markets, if you pick the right stocks on the SGX the share price performance can actually be really strong.

Again, you can see the stocks I am monitoring on FH Premium.

Capital Gains Stocks (or Gold/Bitcoin)

I suppose the easiest play here is just to buy a low cost S&P500 ETF and be done with it.

Yes, maybe US stocks no longer outperform the next decade.

But it would take a very brave investor to not be allocated to US markets, given the US remains the largest and most dynamic economy in the world today.

I think you do need some allocation, but the question is always how much.

I also see a strong case for allocation to Bitcoin and gold in a modern portfolio.

Gold’s performance has been absolutely stunning the past 2 years – almost a straight line up with limited drawdowns.

I’m a lot more nervous about gold after such a huge runup though.

That said, there’s real structural inflows into gold for investors (and countries / central banks) who are nervous about holding too much USD denominated assets.

With Trump at the helm, you never really know what’s going to happen next.

Bitcoin is touted as the digital gold.

But compare the charts of gold vs Bitcoin and it’s fairly clear these 2 asset classes are very different.

Bitcoin responds much more to liquidity conditions in my view, making it more of a “risk-on” asset, that will sell off together with stocks.

But I personally own both in my portfolio, and I think that’s the best way to play it.

Follow Financial Horse to avoid missing any post!

Bonds are a decent alternative in this new interest rate environment

In a climate where the US 10 year yields close to 4.5%.

It would be foolish to rule bonds out of your portfolio.

You can buy a portfolio of investment grade bonds at 5-6% yield, SGD hedged, for low to moderate risk.

That’s kind of a game changer for yield investors.

There are a lot of bond funds out there such as PIMCO GIS Income fund and so on, but each have their own pros and cons, so you do need to understand what you’re buying into.

Closing Thoughts – Diversification the name of the game?

After reflecting on the issue somewhat, I think it’s fairly safe to say that we are going into a period of heightened geopolitical volatility, with the conflict between US and China playing out, and a US that is no longer willing to bankroll the rest of the world’s security and trade.

I don’t see that going away any time soon.

The problem with a pure dividend focused portfolio, is that I have my concerns on how well it will hedge the volatility, and keep up with inflation in such a climate.

Sure maybe it works out well.

But what if it doesn’t?

When it’s your retirement money you’re playing around with, best not to fool around.

The age old adage is that “diversification is the only free lunch in investing”.

And I think that’s just gold.

As I always say on Financial Horse.

Concentrate to get rich, diversify to stay rich.

If you’re investing for retirement, but its very definition you already think you have enough, and the goal is to stay rich (wealth preservation).

To me, diversification would be the name of the game here.

This is an FH Premium post written earlier this week.

I am making this available to all readers in hopes that the thought process may be helpful for others out there.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

How would you do things differently, if I don’t mind drawing down the capital over time? So like target to leave $1m by 80 (estimated life expectancy).

If you can draw on capital, that increases the margin of safety (because of optionality). In which case I would probably add on more exposure to equities / capital gains play. My main concern with a dividend portfolio like that is that if I am right and the next few decades are inflationary, a pure dividend portfolio may not cut it.