As you’ve probably heard by now.

6-month T-Bills yields fell to 2.56% at the most recent auction.

Which needless to say, is a very sharp drop from the 3% we were seeing just earlier this year.

I’ve been getting a lot of questions on alternative places to park cash, for higher yield.

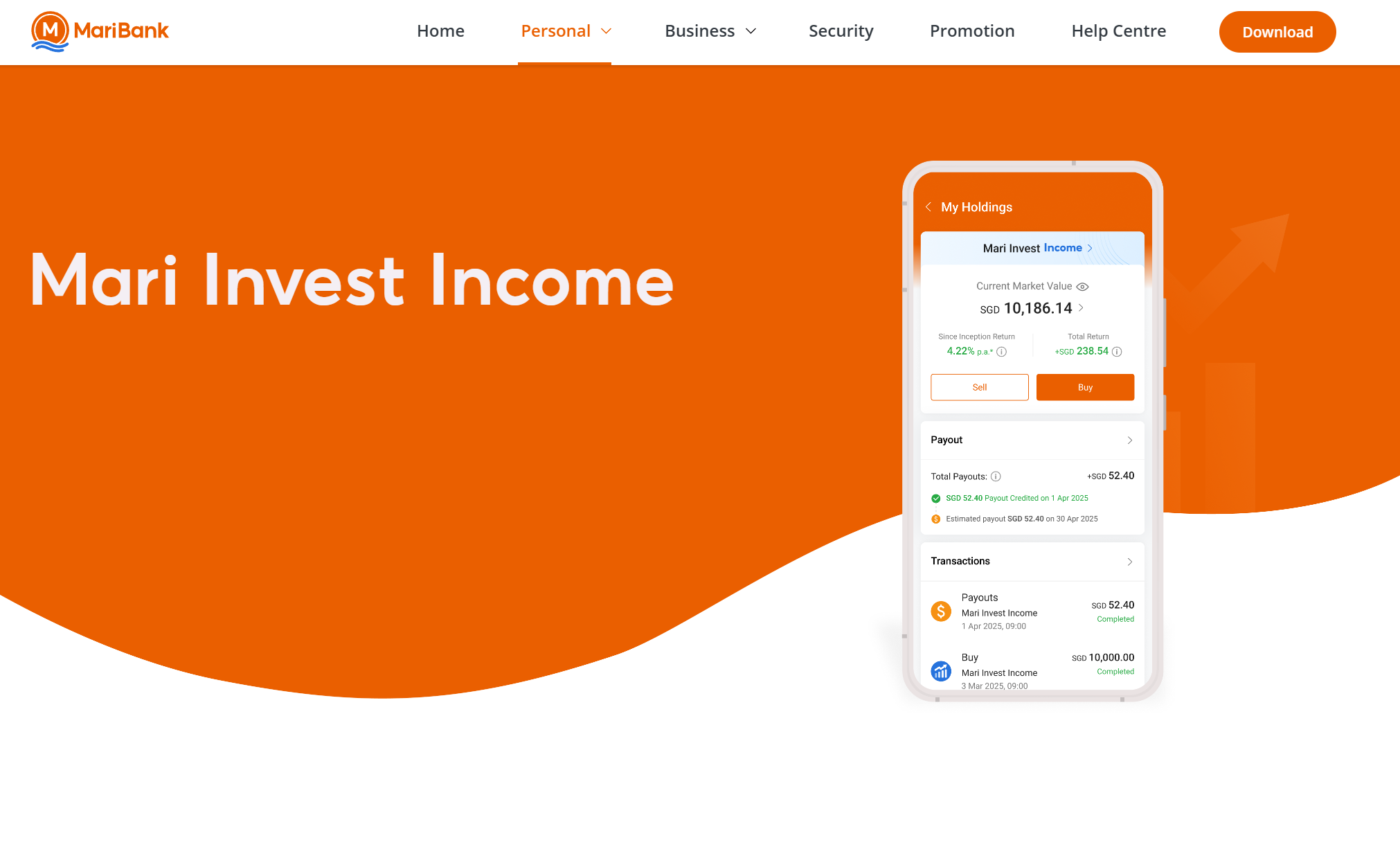

Mari Invest Income is a new product from Mari Bank (same group as Sea / Shopee), that basically invests in PIMCO GIS Income Fund.

The underlying fund pays about 5 – 6% yield, which compared to T-Bills, looks pretty attractive.

Quite a few of you have asked for an in depth review of Mari Invest Income and PIMCO GIS Income fund – so here goes!

What is Mari Invest Income?

Per the website:

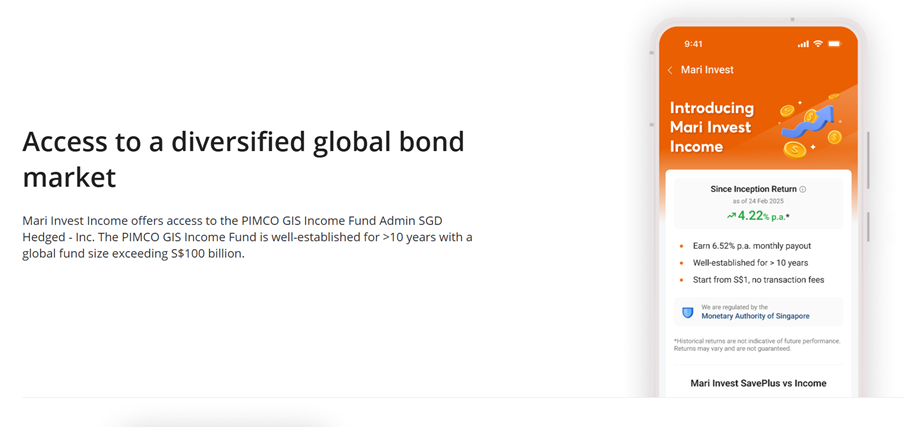

Mari Invest Income offers access to the PIMCO GIS Income Fund Admin SGD Hedged – Inc. The PIMCO GIS Income Fund is well-established for >10 years with a global fund size exceeding S$100 billion.

Basically, it allows you to buy PIMCO GIS Income Fund, via Maribank.

Some other key features or Mari Invest Income below:

- You manage it with a MariBank app

- Minimum investment amount of S$1

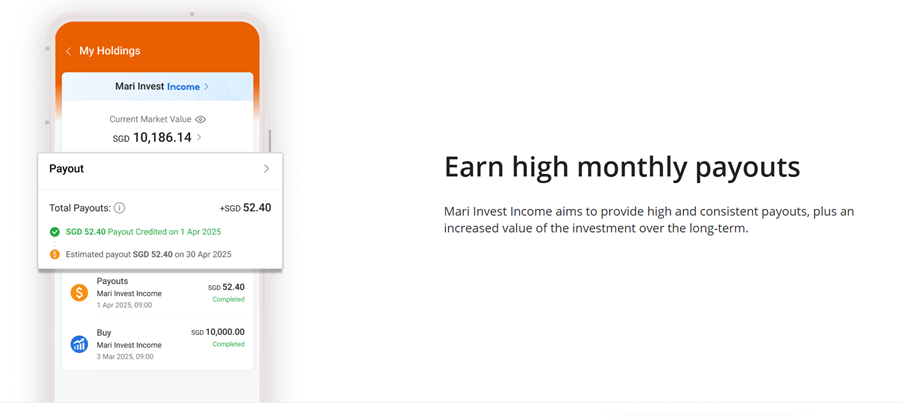

- Since the underlying bond fund has a regular payout, you can review your payouts on Mari Invest Income

- No transaction, upfront, sales fees charged by Maribank

- No ongoing fees charged by Maribank

Mari Invest Income Review – What is PIMCO GIS Income Fund Admin SGD Hedged?

Because Mari Invest Income invests in PIMGO GIS Income Fund.

We need to understand what exactly is PIMCO GIS Income Fund.

This is one of the largest bond funds with the world with US$90 billion+ AUM, and is actively managed by PIMCO which is a renowned bond fund manager.

From the fact sheet (emphasis mine):

The primary investment objective of the Fund is to seek high current income, consistent with prudent investment management. Long-term capital appreciation is a secondary objective.

The Income Fund is a portfolio that is actively managed and utilizes a broad range of fixed income securities that seek to produce an attractive level of income with a secondary goal of capital appreciation.

This fund seeks to meet the needs of investors who are targeting a competitive and consistent level of income without compromising total return. The fund aims to achieve this by employing PIMCO’s best income-generating ideas across global fixed income sectors with an explicit mandate on riskfactor diversification. The fund offers daily liquidity.

The Fund may use or invest in financial derivatives.

The fund taps into multiple areas of the global bond market, and employs PIMCO’s vast analytical capabilities and sector expertise to help temper the risks of high income investing. This approach seeks to provide consistent income over the long term.

Benchmark that PIMCO GIS Income Fund Admin SGD Hedged tracks

The underlying benchmark index that PIMCO GIS Income Fund tries to outperform is basically a US investment grade bond index:

Bloomberg U.S. Aggregate (SGD Hedged) Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis. It is not possible to invest directly in an unmanaged index.

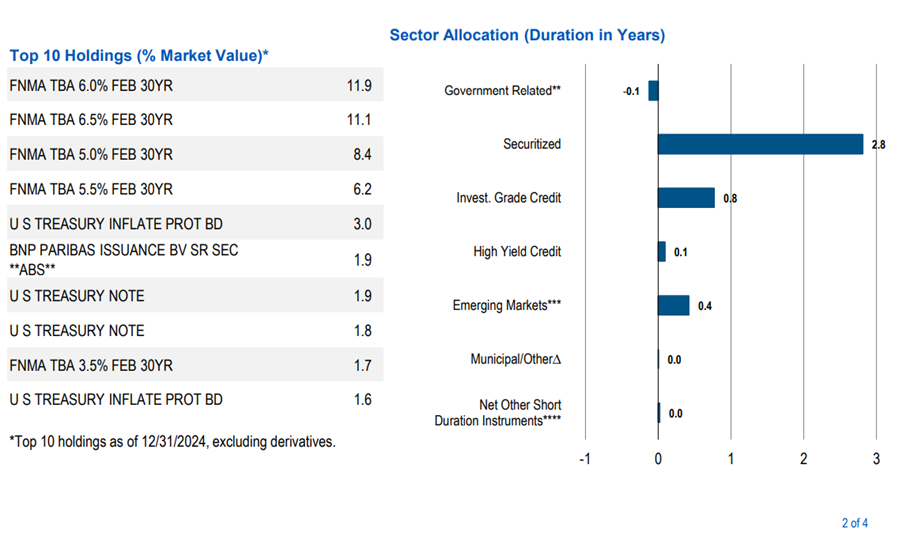

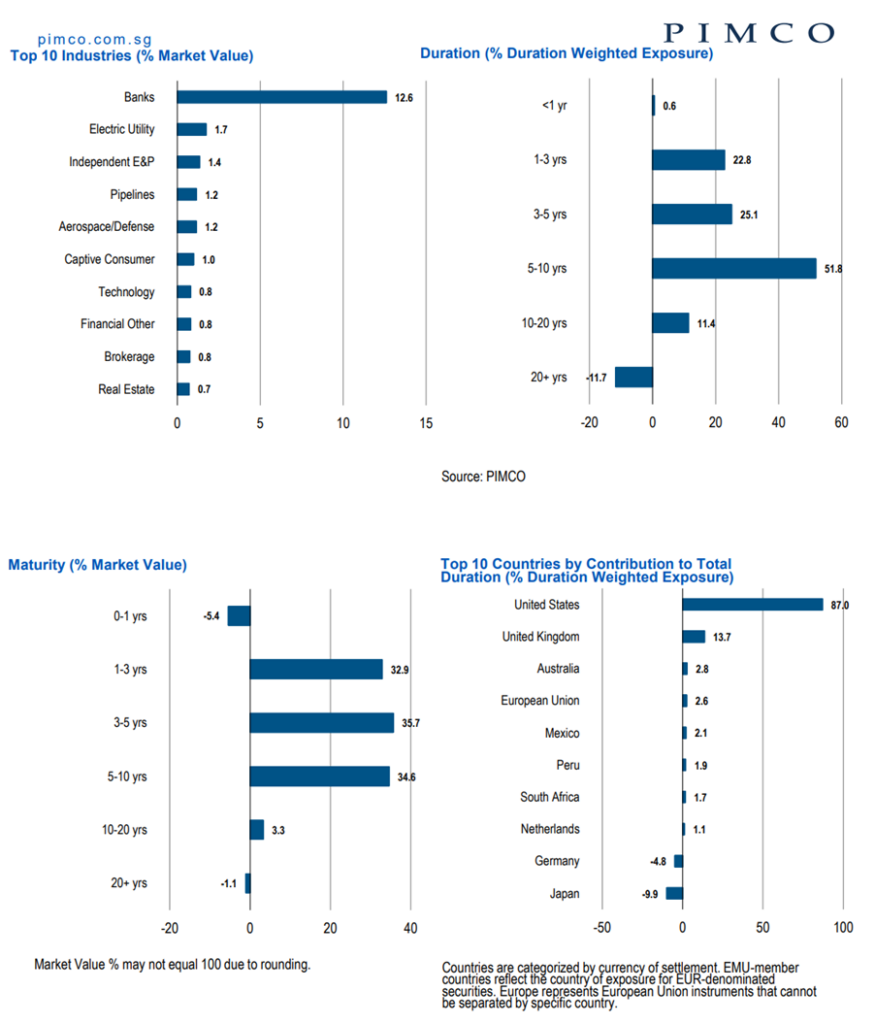

What are the underlying assets held by PIMCO GIS Income Fund Admin SGD Hedged / Mari Invest Income

The charts below give you a bit more colour as to what is held by PIMCO GIS Income Fund.

You can see how a big chunk of the fund is invested in Federal National Mortgage Association (FNMA), or mortgage backed securities.

The rest is a mix of US government bonds, bank bonds, corporate investment grade credit and so on.

How safe is PIMCO GIS Income Fund Admin SGD Hedged / Mari Invest Income

FNMA is also known as Fannie Mae, and I’m sure at this point many of you will recall how mortgage backed securities performed in 2008 (hint – not well).

So I get a lot of questions on how safe is PIMCO GIS Income Fund – especially given that 36% of the fund is parked in Fannie Mae mortgage backed securities.

Here’s a summary from AI on MBS in 2025:

Fannie Mae mortgage-backed securities (MBS) are considered relatively safe investments due to their government-sponsored enterprise (GSE) status, which includes an institutional guarantee of timely principal and interest payments. While not explicitly backed by the U.S. government, Fannie Mae benefits from implied federal support, evidenced by its 2008 bailout and access to Treasury credit lines. These securities carry an implied AAA rating, supported by strict underwriting standards and oversight from the Federal Housing Finance Agency (FHFA). Key risks include prepayment uncertainty (if borrowers refinance) and minimal credit risk tied to Fannie Mae’s financial stability. Though slightly riskier than fully government-backed Ginnie Mae MBS, they are safer than private-label MBS and comparable to Freddie Mac’s offerings. Investors seeking stable, low-risk fixed-income assets often favor Fannie Mae MBS, but those prioritizing maximum safety may prefer Ginnie Mae. Overall, they remain a cornerstone of conservative portfolios with manageable risks.

But I know… the more sceptical would say analysts were saying the same of MBS in 2007…

My personal views? How safe is PIMCO GIS Income Fund Admin SGD Hedged / Mari Invest Income?

What I would add, is that this isn’t 2008 anymore.

After 2008, the US did clean up the household debt situation, so the credit strength of these mortgage backed securities is a world of a difference from 2008.

So my personal view is that this is a low – medium risk bond fund.

But if your question is whether this is risk free, then it’s fairly clear the answer is no.

If you want risk free, a 5 year Singapore government bond pays 2.5% today.

That’s your risk free yield right there for a SGD bond fund with medium duration.

Anything higher and you do need to take on some risk.

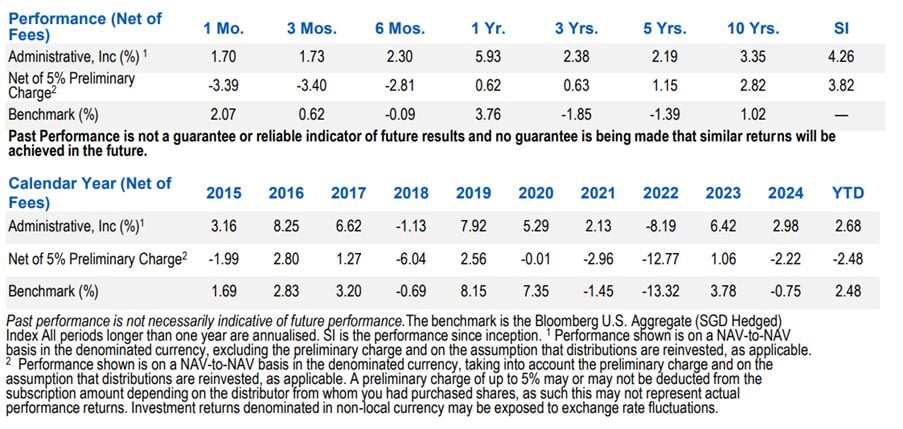

What is the historical performance of PIMCO GIS Income Fund Admin SGD Hedged

Historical performance is set out below.

Anything before 2023 doesn’t really make sense because that was a much lower interest rate regime.

2023 returns were about 6%ish, and 2024 returns about 3%ish.

So you can see the returns does bounce around quite a fair bit – mainly because of mark to market pricing.

Why are “returns” from Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged so volatile?

Why are the total returns for a bond fund so volatile?

I always get a lot of questions about this, so let’s spend some time discussing it.

When you buy a bond fund, you’re basically buying into a portfolio of bonds.

And value of these bonds fluctuate on a daily basis, inversely correlated with interest rates.

So when interest rates go up, the value of the bonds go down, and vice versa.

In plain English, this means that when you buy a bond fund like Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged, your “returns” come in 2 forms:

- The daily price of the bonds (which can go up or down)

- The coupon from the bonds (ie. Dividend yield)

What does this mean… in practice?

To give a simple example.

Let’s say interest rates drop, and the bond price goes up by 3%.

Throw in the 6% bond yield, and you make a 9% return that year.

Very nice.

What if interest rates go up?

Let’s say the bond price drops by 5%.

Throw in the 6% bond yield, and you are up 1% that year.

Get it?

The logic is pretty similar to REITs, because of the daily mark to market.

Follow Financial Horse to avoid missing any post!

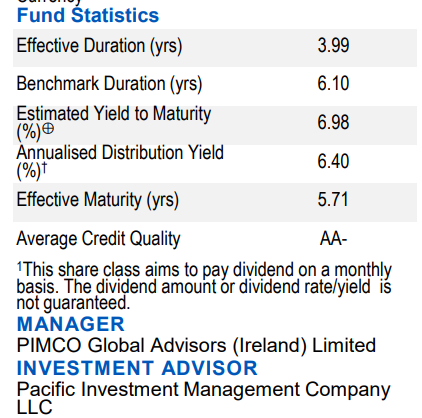

What is the approximate distribution yield of Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged?

On that note – the underlying bonds have about a 6.4% annualised distribution yield.

So net off fees, and the distribution yield is about 5%ish.

The big question mark of course, is the mark to market price, as that depends on where interest rates go.

Fees for Mari Invest Income

Per Maribank:

Good news! There are no transaction fees or ongoing fees charged by MariBank to investors for Mari Invest. This means no account fees, upfront fees, sales charge or withdrawal fees, so 100% of your money gets invested.

The annual management fee for the PIMCO GIS Income Fund Admin SGD Hedged – Inc fund charged by the fund manager, PIMCO, is 1.05% p.a.

The management fee of a fund is a fee charged by the respective fund manager for its ongoing management of the fund, of which a portion is paid to MariBank as a distributor. It is factored into each day’s Unit Price shown, and no further deductions are made when fund units are bought or sold. Read here to find out how it works.

Long story short:

- No charges by Maribank to buy/sell, or on an ongoing basis

- However the all-in fee from fund manager is 1.05%

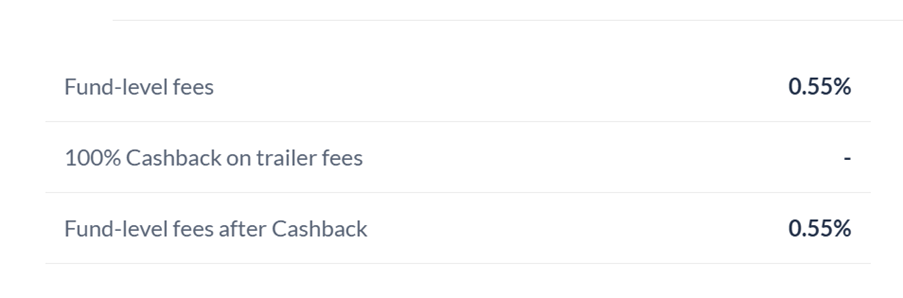

You can buy PIMCO GIS Income Fund for 0.85% all-in fees via Endowus

Note that actually if you buy the PIMCO GIS Income Fund via Endowus.

You’ll actually end up paying 0.55% at the fund level after trailer fee rebate.

And 0.30% Endowus fee.

For an all-in fee of 0.85%.

Which is lower than the 1.05% if you buy via Mari Invest Income.

Now I’m not saying that this is a no brainer, as many investors may prefer buying Maribank.

But just to put it out there that you can save 0.20% on fees just by using an alternative platform.

Do with that what you will!

Endowus promo code below if you need:

Endowus Promo Code

Join me to get S$20 off your Endowus Fee. Use my unique promo code XX9YZ at https://endowus.com/invite?code=XX9YZ

What are the risks with Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged

To sum up.

Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged is a much more complex instrument than simply T-Bills or Mari Invest.

There’s broadly 2 risks to note:

- Risk of default of underlying bonds

- Mark to market losses if interest rates go up

Risk of default of underlying bonds

I think it’s fairly clear that Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged is not risk free.

The better question is whether you are adequately compensated for the risk that you are taking on.

With a 5-6% coupon yield, for investment grade US corporate credit style risk, I think that’s probably fair.

Mark to market losses if interest rates go up

Boy this one is really hard to call.

Trying to call the path for US interest rates is a whole profession in itself.

Because of recession fears, there’s been a lot of downward pressure on US interest rates of late (note that because effective duration is 4 years, you need to look at the medium term duration part of the curve to understand the impact on these bonds).

And if recession fears continue to materialise, we could see further downward pressure on interest rates – which would be good for Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged.

But if those recession fears go away, and inflation fears returns, and interest rates creep up – you could well be sitting on mark to market losses.

My views on Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged?

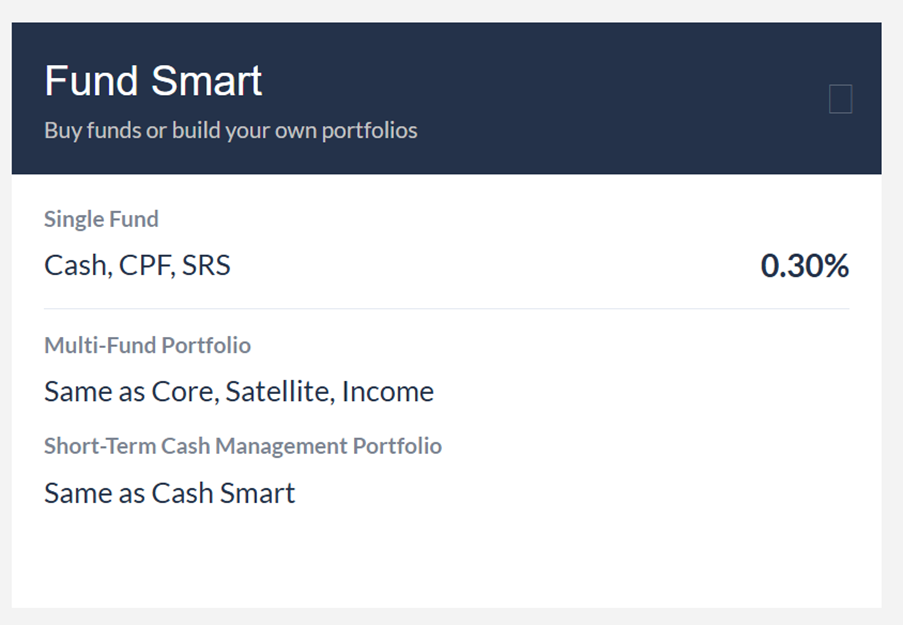

Full disclosure that I hold a position in PIMCO GIS Income Fund (bought via Endowus Fund Smart).

I bought a position late last year, and returns are decent for me.

Generally speaking on default risk – I think short of a bad recession, I *don’t think* we will see massive corporate defaults.

But yes I know that is a big if.

In my view – the biggest thing investors need to note about Mari Invest Income s is that when interest rates go up, you will see mark to market capital losses.

So you need to think this more as a REIT equivalent, rather than a T-Bills or Mari Invest kind of product where the returns are highly stable, and risk of capital loss is close to zero.

Will I buy Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged today?

The bigger risk to me today might actually be mark to market losses when interest rates go up.

If you buy in when US 5 year yields are at 4%, it’s not impossible to imagine US 5 year yields going back up to 5% and beyond down the road when the US economy picks up, or if inflation makes a return.

In that scenario you could be sitting on capital losses.

But that said – where we are today, I think it’s probably a decent buy if you want something with higher yields, and you don’t mind taking on some risk.

Your holding period matters too.

The longer you hold a product like Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged, the more time you have for the distribution yield to offset any capital losses.

So some thought process around your cash management is required.

Put some into risk free stuff like T-Bills, some into short term money market funds like Mari Invest, some into high yield savings account like UOB One, and some into Mari Invest Income for a higher yield.

This gives you a lot of optionality into which to draw on in the event you need liquidity.

But hey that’s just my views – I would love to hear what you think!

Would you buy into Mari Invest Income / PIMCO GIS Income Fund Admin SGD Hedged?

This post is written on 14 March 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Thanks, Financial Horse, for writing such articles to help us keep abreast of various investment options. Two things:

1. If I’m not mistaken, Endowus fee is 0.3% if only single fund. If multiple funds, then it’s 0.6% (for less than $200K). So if use Endowus for multiple funds, then the fees would be 0.55%+0.6%=1.15%. Which would be higher than the 1.05% with Mari Invest Income, correct?

2. It seems POEMS (Phillip Securities) also offers this PIMCO fund (https://www.poems.com.sg/fund-finder/pimco-gis-inc-admin-sgd-hedged-income-ie00b91rq825-556842/). It also does not charge any sales fee or platform fee. So, would buying this PIMCO fund using Mari Invest Income and POEMS be the same?

Thank you.

Hi my replies below:

1. Yes you’re right. But just create a portfolio under fund smart with 1 fund, and you will get the 0.3% fee. No need to put more than 1 fund into the portfolio unless you want the rebalancing function.

2. If I recall the POEMS one is a different share class (without trailer fee rebate), so it will be more similar to Mari Invest than Endowus.

For now, I can see one difference: minimum investment amount is $1 for Mari Invest, whereas it is $1,000 (and subsequent investment amount is $500) for POEMS. Can you see any other differences that I didn’t notice?

Confirm the share class before you buy as well. Endowus will have trailer fee rebate, but POEMS wont – but this is offset by the Endowus fee to a certain extent.

Hi FH,

Thanks for thi great article. It seemed that I can save 0.20% on fees just by using Endowus. But is the PIMCO GIS Income Fund from Endowus SGD hedged???

Hi FH,

Thanks for interesting article. So I save 0.20% on fees just by buying from Endowus instead of Mari Bank.

But if I buy from Endowus, is PIMCO GIS Income Fund SGD hedged?

Yes pretty much. Yes Endowus also has a SGD hedged version of the PIMCO GIS Income Fund – make sure to select the right one.

Hi,

I noticed the ISIN for Endowus is IE00BSTL7535 while Mari one is IE00B91RQ825; are they essentially the same fund?

Thanks for pointing this out. If the ISIN is different then actually they might be using a different share class.

Been starting to invest in Mari Income fund and see my capital lost to $700. Not sure if worth to continue to stay with the fund from the current trade wars.

Well you need to see how PIMCO GIS Income Fund fits into your broader cash management strategy. It should be used in conjuction with other products like money market funds and T-Bills, and in such case if you have a longer holding period for the income fund it will allow the higher yield to make up for the volatility.

Thanks for the advice..Guess you are right to have a long term holding period with the higher interest rate to offset the capital losses.

Thanks for the advice..Guess you are right to have a long term holding period with the higher interest rate to offset the capital losses.

Yes that’s right.