As you all know by now, what would have been considered unthinkable at the start of the year is now a reality.

The US is engaged in a direct war with Iran.

Sure, this is an air campaign, but war is war, and nobody can predict with certainty that things will not spiral out of control.

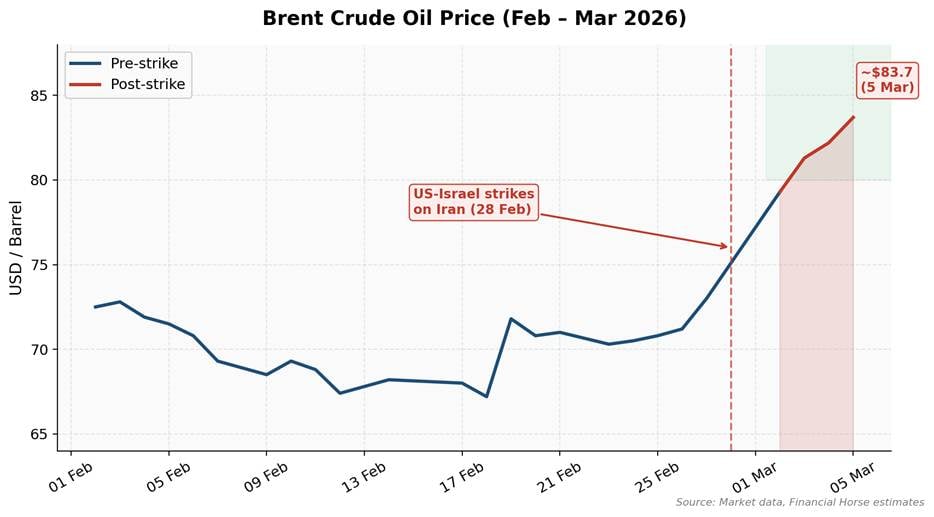

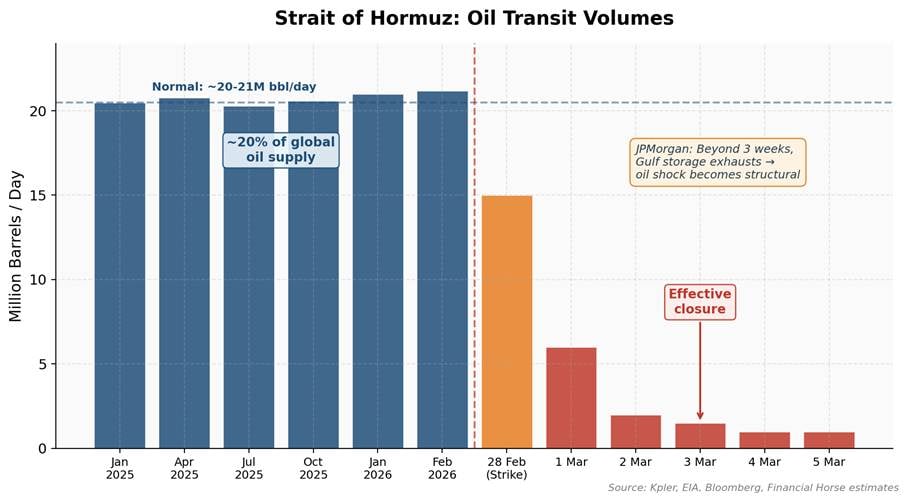

Especially given that Iran sits right next to the Strait of Hormuz which 20% of global oil flows through, and Iran this week has shown that they are willing to take down regional oil infrastructure.

I shared my preliminary thoughts in the earlier articles.

But now that we’ve had a week to watch this play out.

I wanted to share deeper views on how I see this playing out, and how it would drive my investments in 2026.

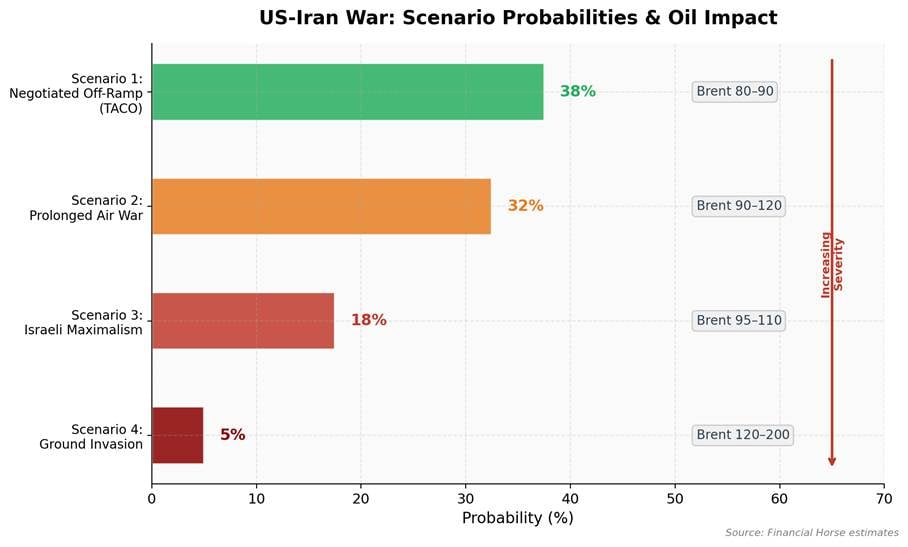

The 4 scenarios – and what each means for markets

Broadly speaking, I see 4 broad scenarios for how this plays out:

| Scenario | Probability | Duration | Brent Range | GDP Hit | Inflation |

| 1. Negotiated Off-Ramp / TACO | 35–40% | 2–4 weeks | $80–90 | Minimal | Minimal |

| 2. Prolonged Air War | 30–35% | 6–12 weeks | $90–120 | Moderate | Mild |

| 3. Israeli Maximalism | 15–20% | Variable | $95–110 spike | Moderate | Moderate |

| 4. Ground Invasion | <5% | Months+ | $120–200 | High | High |

Let me walk through each.

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.

Scenario 1: Negotiated Off-Ramp / TACO (35–40%)

This is basically TACO – Trump Always Chickens Out.

We saw this play out with tariffs in 2025 – Trump escalated dramatically, markets sold off, and then he walked it back and declared victory.

The same playbook could work here.

In this scenario, the US achieves its “core” military objectives (nuclear infrastructure degraded, Khamenei dead, IRGC severely weakened), then Trump pivots to declaring “mission accomplished”.

Iran’s new leadership likewise declares victory without officially giving up their nuclear and ballistic missile campaign.

In this world, Brent settles $80–90 during hostilities, drops to $70–75 post-ceasefire. Equity markets recover within 4–8 weeks.

In this scenario, any dip would be a buying opportunity.

The problem?

As I discussed in Part 2 – I think a clean negotiated exit is harder than it looks.

You need Iran’s Assembly of Experts to select a leader perceived as acceptable for negotiation, who then agrees to a peace deal with the US, while the US-Israel is actively bombing their country.

And that this leader doesn’t immediately get thrown out / assassinated by his own population.

That’s a big ask.

Also now that Israel has finally “convinced” the US to engage in a war with Iran – would Israel allow such an easy offramp?

Scenario 2: Prolonged Air War (30–35%)

In this scenario, neither side finds a face-saving exit quickly.

US continues striking progressively deeper.

Iran’s decentralized command structure means no single entity can surrender. IRGC fragments – some factions fight on, others seek accommodation.

Trump’s own “4–5 week” timeline suggests the administration anticipates sustained operations.

In this scenario, Brent sustains the $85–100+ range.

JPMorgan has warned that a war lasting more than 3 weeks would exhaust Gulf storage capacity, forcing production shutdowns and potentially pushing Brent to $120.

Goldman’s base case of 5 more days of low Hormuz exports puts Brent at $76 average for Q2, but 5 weeks of disruption could push it to $100.

This is the scenario where stagflation risk starts to materialise for the global economy.

In this scenario, there will be higher inflation and slower economic growth, and how much will depend very much on how bad the Strait of Hormuz blockage gets.

Scenario 3: Israeli Maximalism (15–20%)

Israel takes the opportunity to permanently destroy Iran’s nuclear program – not just damage it, but eliminate centrifuge manufacturing capability, kill remaining nuclear scientists, and destroy underground facilities at Fordow.

Recent evidence suggests Israel pulled the strings to bring the US into this war.

Netanyahu has every incentive to make this operation maximally decisive – he may not get another window like this.

Short-term oil spike to $100–120, but medium-term (6–12 months) could be bearish for oil as Iranian production is permanently impaired and a “new Iran” premium emerges.

Scenario 4: Ground Invasion (<5%)

This is the tail risk scenario.

Air campaign fails to produce regime change. No successor emerges. Trump, having committed to regime change, faces the “now what?” problem.

Iran has 4x Iraq’s population and 4x the terrain. The US has zero appetite for another occupation.

But mission creep is a historical constant.

If Iran launches a genuinely devastating asymmetric attack – say sinking a US warship, or a mass casualty event on a Gulf state capital – political dynamics shift rapidly.

If US / Israel launch a ground invasion against Iran to force regime change, then all bets are off.

This scenario would be catastrophic for markets.

Brent $100+ easily.

Deutsche Bank’s worst case of full Hormuz closure via mines and anti-ship missiles pushes Brent toward $200.

Soaring oil prices would be inflationary and recessionary.

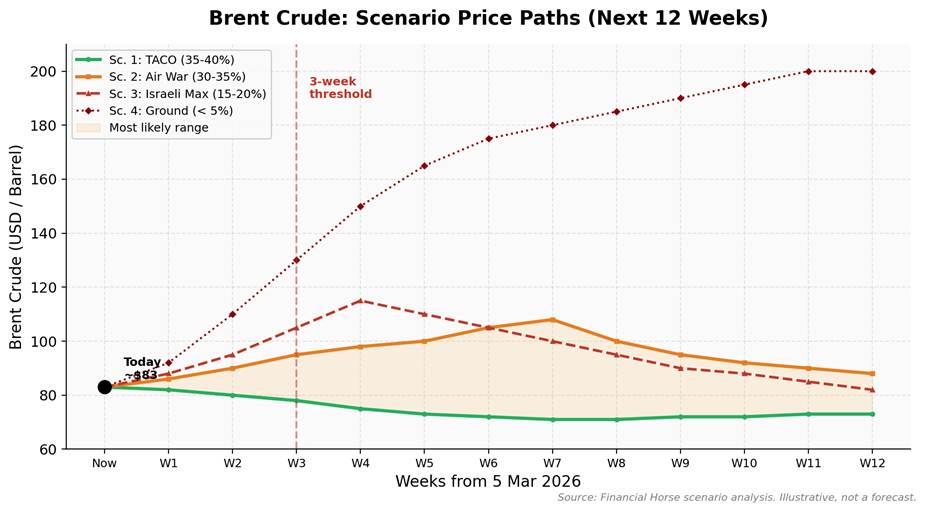

My base case?

The highest probability outcome based on the above is a messy, drawn-out air campaign lasting 3–6 weeks followed by a face-saving negotiated pause.

Not a clean resolution. Not a full-scale invasion.

The base case for oil is Brent in the $80–95 corridor for the next 4–8 weeks with extreme two-way volatility.

If so, this is a buying opportunity for equities.

But note the tail risk.

The market is pricing in a relatively benign outcome – that the Hormuz reopens quickly and oil settles down.

If that’s wrong, and the disruption lasts 3+ weeks, we’re looking at a very different picture.

The key watchpoints

The 3-week mark is the critical threshold – does the Strait of Hormuz open within 3 weeks?

Beyond that, Gulf storage exhausts and the oil shock becomes structural rather than transitory.

To determine that – the Khamenei succession question is the single biggest variable.

Iran literally cannot negotiate coherently until someone is empowered to commit the state.

Every day without a clear successor extends the conflict timeline mechanically, regardless of what either side wants.

Whether a pragmatic, moderate leader can consolidate power.

And convince the population that a peace deal with the US is in their country’s interests.

Big question mark.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

What does this mean for my portfolio?

If my base case is broadly correct – that this is a 3–6 week air campaign followed by a messy negotiated pause.

And the tail risk is for a prolonged closure of the Strait of Hormuz beyond 3 weeks.

Then this is how I’m thinking about asset allocation:

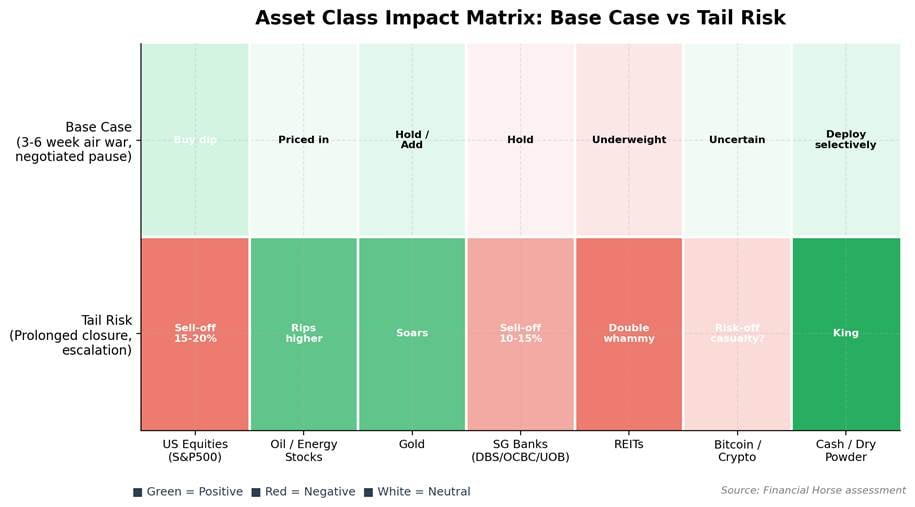

| Asset Class | Base Case View | Tail Risk View |

| US Equities (S&P500) | Buy the dip if sell-off deepens. War impact likely transitory. | Could drop 15–20% if Hormuz stays shut 3+ weeks. |

| Oil / Energy Stocks | Likely already priced in. | $100+ Brent if prolonged. Energy stocks march higher. |

| Gold | Moderate. Classic safe haven play benefitting from geopolitical uncertainty. | Could push significantly higher on geopolitical premium. |

| Singapore Banks (DBS/OCBC/UOB) | Limited direct exposure. Higher oil = mild inflation headwind. | If recession risk materialises, banks could sell off. |

| REITs | Higher oil = higher inflation = higher for longer rates. Mild Headwind. | Double whammy – recession + sticky rates = REIT pain. |

| Bitcoin / Crypto | Outperforming so far this week. BTC above $70k. Interesting but could be a bull trap (Bitcoin has done this in the past). | Unclear – could be safe haven OR risk-off casualty. My money would be on the latter. |

| Cash / Dry Powder | Keep enough to capitalise if sell-off deepens. | Cash is gold as it allows you to buy any sell-off in size. |

How I’m personally positioned

I shared in my 2026 Outlook for FH Premium readers that I wanted to keep enough dry powder to capitalise if we get a sell-off.

Well, coupled with the decline in software stocks – here’s the sell-off.

The way I see it, you can broadly split what happens next into 2 outcomes.

One where both sides find a face saving exit, the war ends in the next 3 – 6 weeks without significant damage to the Strait of Hormuz and global economy.

Then you want to buy the dip.

The other outcome is where both sides play chicken and keep escalating, the Strait of Hormuz stays shut for an extended period, we have global inflation and risk-off.

Then you don’t want to buy the dip, and cash / oil / gold is king.

How to invest in this scenario?

In investing, you always have to think in terms of probabilities.

Because while my base case is for a relatively contained outcome, I genuinely don’t know how this plays out.

So I am buying the dip.

But I’m not going all in here, and saving some dry powder for the tail risk.

This is not tariffs where Trump can just tweet a 90-day pause.

This is a hot war, with real bombs, a dead Supreme Leader, a closed Strait of Hormuz, and multiple countries firing missiles at each other.

Trump can say what he wants, but if Iranians decide they want revenge for their dead Supreme Leader and continue to send drones at any oil tanker in the Strait of Hormuz, what do you do next?

The range of outcomes is unusually wide here, and as investors we need to be alive to those possibilities.

The key insight?

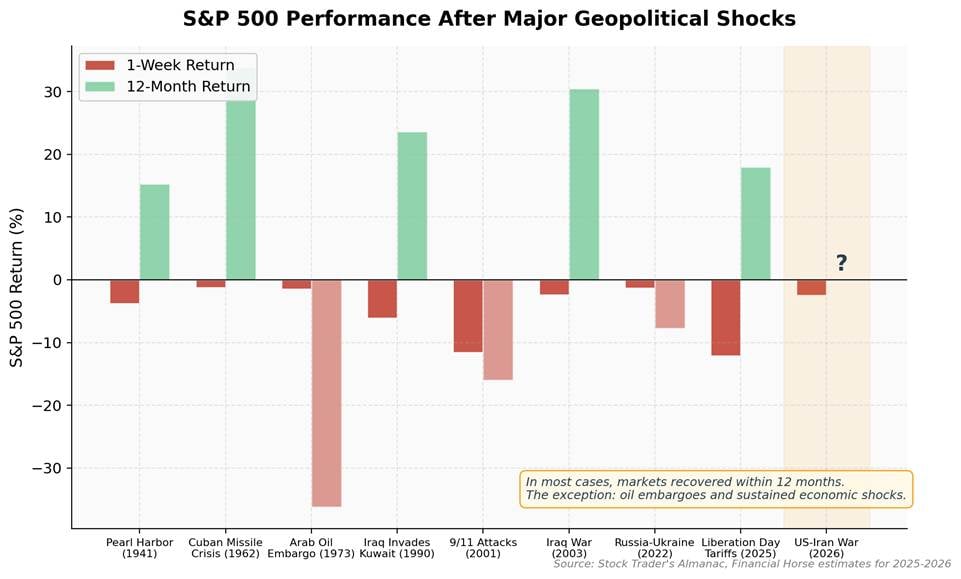

History shows that geopolitical shocks – even severe ones – tend to be transitory for equity markets.

The average one-week drop in the S&P500 after a major geopolitical shock is about 1%. Twelve months later, the average gain is around 3%.

Markets are forward-looking. Once the worst of the uncertainty passes, they tend to recover.

But – and this is a big but – this time the oil supply disruption is real. The Strait of Hormuz is actually closed. This isn’t a theoretical risk anymore. If this persists, the economic impact could be more structural than what the historical averages suggest.

That’s why I’m not blindly buying the dip.

I’m buying the dip, but with caution, and keeping plenty of reserves.

You can see my full portfolio and what I’m buying / selling on FH premium.

What is the impact on Singapore / Asia?

Singapore is an oil refining hub, but not an oil producer.

Higher oil prices are generally a net negative for Singapore – they feed through to transport costs, electricity prices, and eventually consumer inflation.

Likewise for Asia, which is a net importer for oil.

For Singapore banks, they have limited direct exposure to the Middle East.

The bigger risk for Singapore is second-order effects – if this triggers a global recession or a sustained spike in inflation that forces central banks to keep rates higher for longer.

For my Singapore bank positions (OCBC and UOB) – I’m holding for now, but keeping a close eye on what happens next.

For REITs – higher oil means higher inflation means rates stay higher for longer. Not great for REITs. I shared at the start of the year that I don’t plan to overweight REITs in 2026, and I don’t see anything that makes me change my mind.

Full updated views shared on FH Premium.

Closing Thoughts

Look, I’ll be the first to admit – I don’t know how this war ends.

Nobody does.

My base case is a messy 3–6 week air campaign followed by a negotiated pause. Brent in the $80–95 range. Equity markets volatile but ultimately recover.

But the tail risk is real.

If the Strait of Hormuz stays shut beyond 3 weeks, we’re looking at the most severe energy crisis since the 1970s oil embargo.

I’ll continue to share my thinking on FH Premium as the situation develops.

But I would love to hear what you think – how are you positioning your portfolio for this?

This is an FH Premium article that I am releasing to all readers, in the hopes that it helps you in your decision making. It will not be updated going forward.

My latest macro views, as well as my full stock watch and personal portfolio, are shared on FH Premium.