A couple of you guys have asked me for my views on IREIT Global and their recent rights issue.

I own a tiny bit of IREIT Global as well, so I figured I would share some thoughts. Hopefully, it will help you in your decision making on whether to subscribe for the upcoming rights issue.

Note: This article is a premium article that first appeared on Patron. If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Basics: What is the IREIT Rights Issue?

REITs Week has a good summary:

IREIT Global (IREIT), a Europe-focused real estate investment trust, announced that it will be launching a Rights Issue to raise gross proceeds of approximately S$142.8 million (approximately €88.7 million).

This will be mainly used to finance the acquisition of the remaining 60% interest (Acquisition) in a portfolio of four freehold multi-tenanted office buildings located in Madrid and Barcelona, Spain (Spain Properties) from Tikehau Capital and repayment of the CDL Loan.

The Rights Issue comprises an offer of 291,405,597 Rights Units on a renounceable non- underwritten basis to eligible unitholders based on the Rights Ratio of 454 Rights Units for every 1,000 existing units in IREIT at an issue price of S$0.490 per Rights Unit (Issue Price).

This represents a discount of approximately 32.9% to the closing price of SGD0.730 as of 18 September 2020.

It is also a discount of approximately 25.2% to the theoretical ex-rights price (TERP) of SGD0.655 per unit.

For every 1000 units in IREIT you get 454 Rights Units as a price of $0.49.

Theoretical ex rights price is about $0.65.

Price today is about $0.605.

What is IREIT acquiring?

IREIT will be using the money to acquire a bunch of Spanish Offices, in Madrid and Barcelona.

IREIT already owns a 40% stake in these properties, and they will now be acquiring the remaining 60%.

3 Thoughts from me

3 thoughts from me on the deal:

- Price of the Spanish offices looks steep

- Acquisition is DPU dilutive

- Decent alignment of interests with Sponsor

1. Price of the Spanish offices looks steep

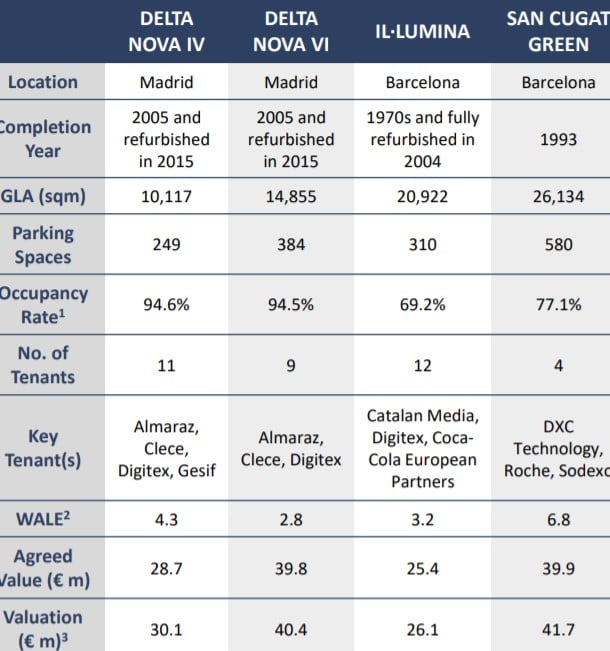

Here are the prices that IREIT paid for the Spanish offices in 2019, when they acquired the 40% stake.

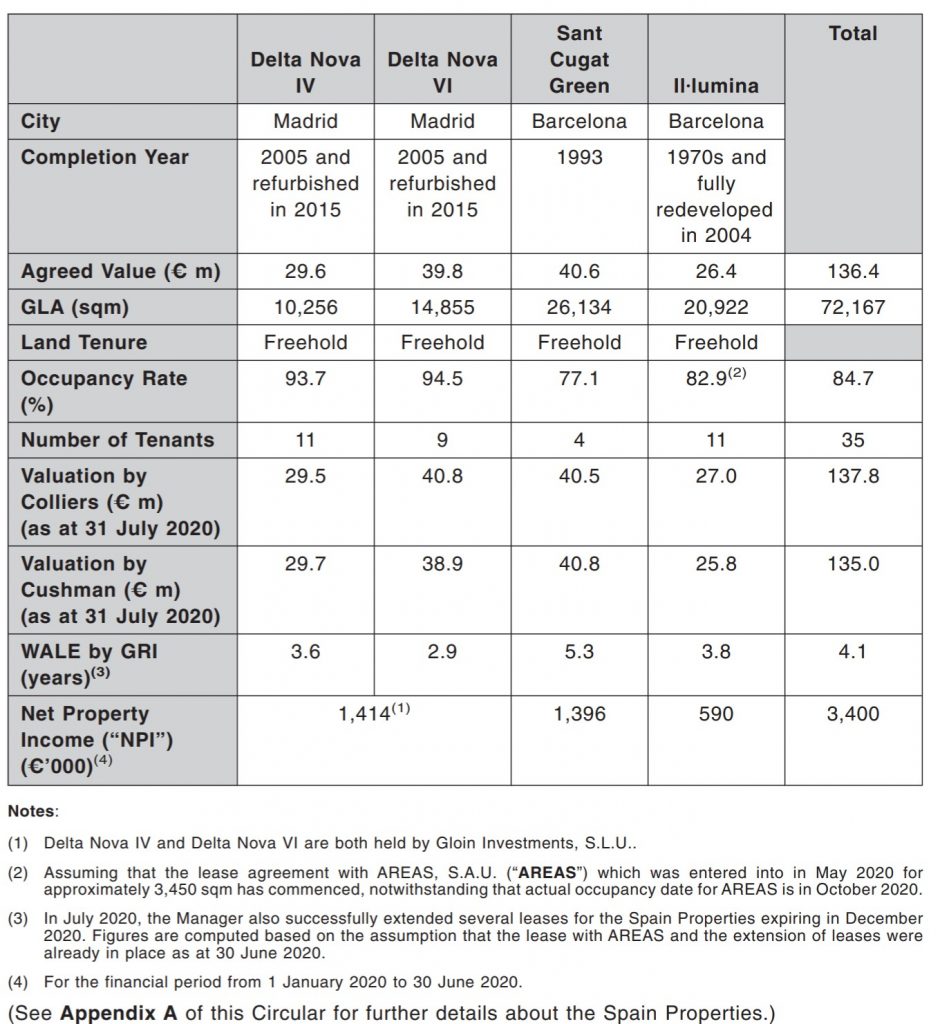

And these are the prices they’re paying for the same properties today.

Long story short, 1 year on, in the midst of a global pandemic and the worst recession since WWII, the prices of these Spanish offices has actually gone up.

I mean I’m not an expert on Spanish offices so I can’t comment on the valuations the REIT is using.

But really?

A global pandemic, work from home trend, high possibility of a second wave heading into winter for Europe, and the price of office buildings are going up?

If it were me, I probably would have wanted a 10% – 20% discount from 2019 prices, minimum.

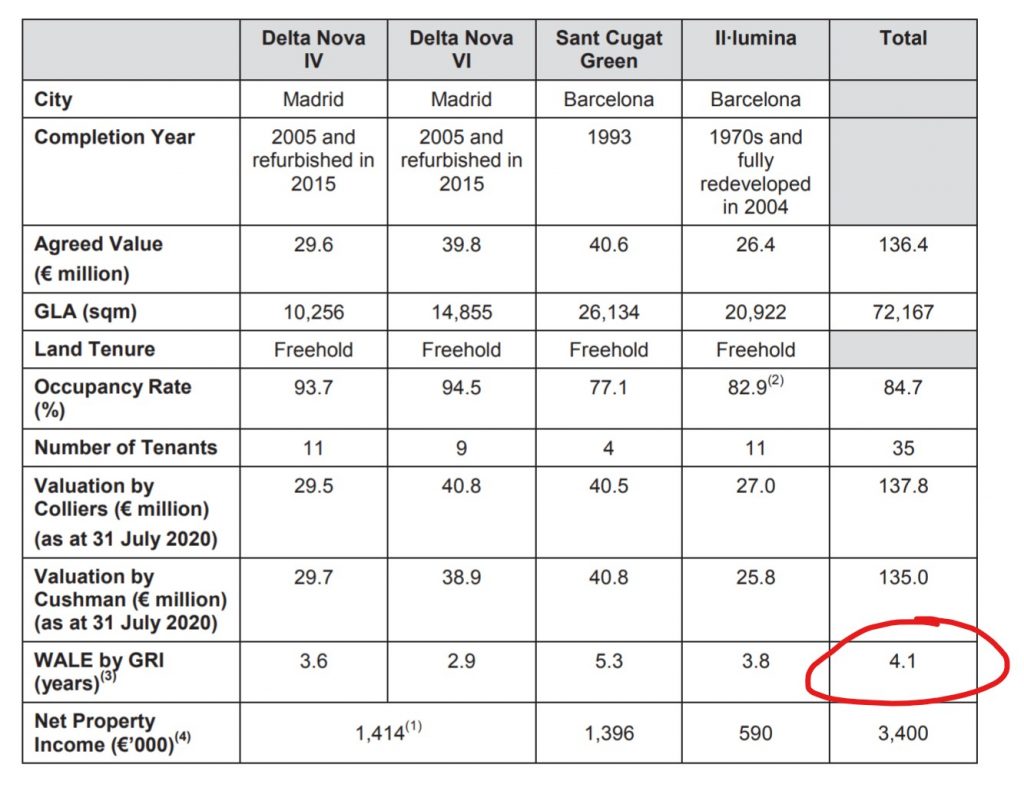

At current purchase price, it works out to about a 4% cap rate for the newer, Madrid and Barcelona buildings (Delta Nova IV and VI, and II Ilumina), and about 6% for the older Barcelona one (Sant Cugat Green).

By contrast, the German properties in CCT’s portfolio go at a 3.9 – 4.2% cap rate.

One could argue that this acquisition of the remaining 60% was already contemplated since 2019 when the deal was first done.

I don’t disagree with that, but the option granted to IRET was a call option, not a put and call option. So the REIT could have had the opportunity to not exercise the call option, or at least renegotiate the purchase price.

Pursuant to the Shareholders’ Agreement, Tikehau Capital granted the Trustee a call option to acquire its interest in 60.0% of the shares in the JVCo for the period of 18 months following completion of the Initial Acquisition upon written notice from the Trustee to Tikehau Capital (“Call Option”) at 60.0% of the call option price calculated based on the consolidated net asset value of the JVCo and its subsidiaries, as adjusted based on the average of the market values of the Spain Properties in aggregate as determined by two independent property valuers, with one to be appointed by each of the Trustee and the Manager, respectively (the “Call Option Price”).

Paying off the bridging loan and reducing gearing

IREIT funded the 2019 purchase via debt, and a bridging loan from CDL. The bridging loan has a tenure of 18 months and an interest rate of 3.875% above EURIBOR per annum, which works out to be about 3.4%.

That’s a bit pricey in this era of low interest rates, but well that’s how bridging loans work.

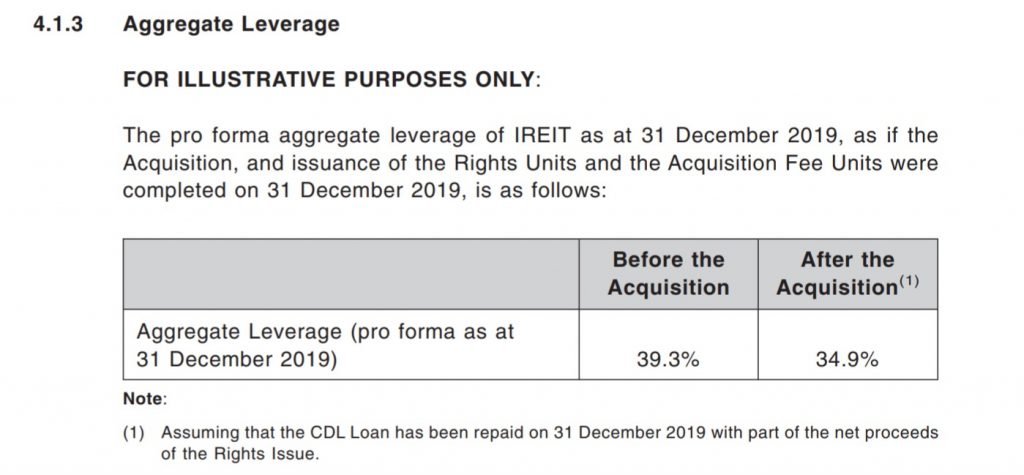

After this equity fundraising, IREIT will pay off this expensive bridge loan, and pay off some debt to reduce overall gearing ratio from 39% to 34%:

The problem though, is that the cost of equity is even more expensive than the cost of debt, which will mean the acquisition is DPU dilutive.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

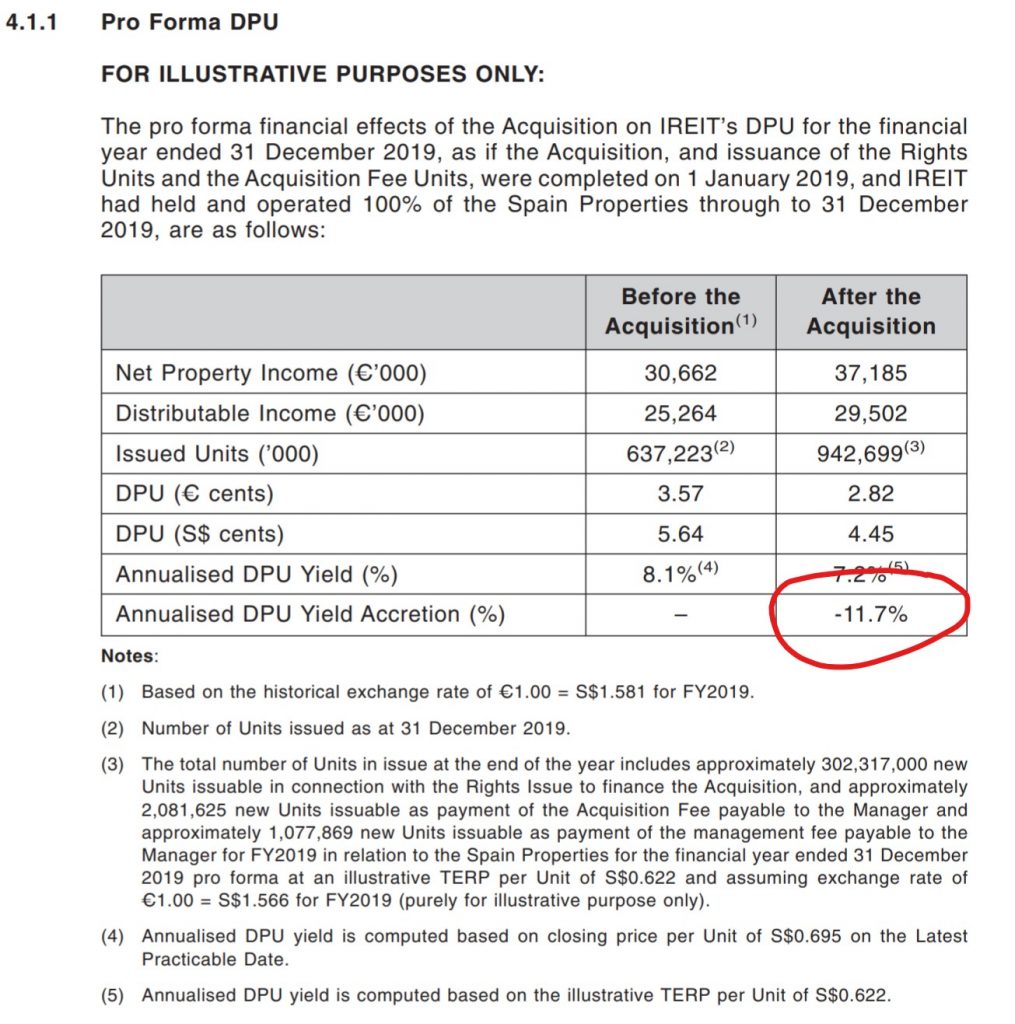

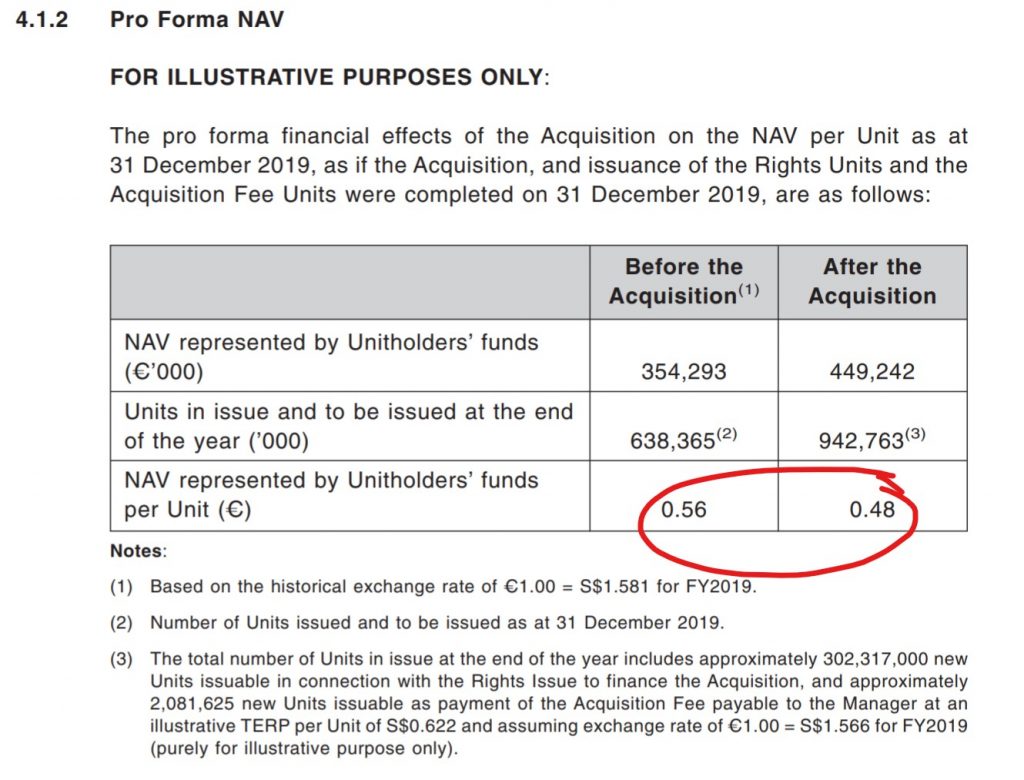

2. Acquisition is DPU dilutive

So the problem with raising equity to pay down debt in this climate, is that debt is dirt cheap, while equity is so expensive (unless you’re Tesla).

So if you do so, the transaction will be DPU dilutive, which is exactly what we see below:

DPU and NAV drop by more than 10% as a result of this deal.

That’s what happens when you raise equity to pay down debt, and use it to buy expensive buildings in this climate.

3. Decent alignment of interests with Sponsor

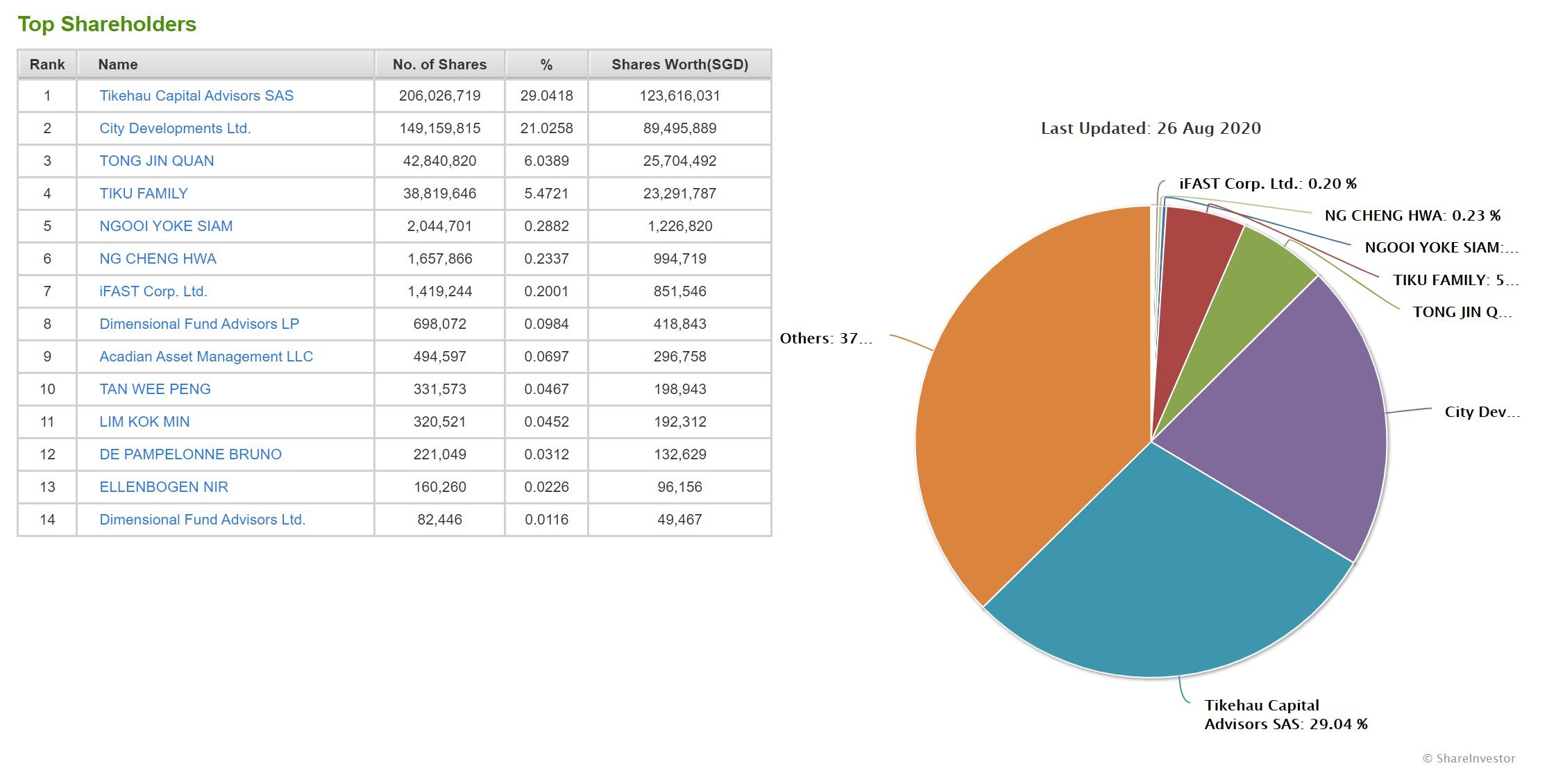

The 2 main shareholders for IREIT are Tikehau Capital and City Dev (CDL).

CDL needs no introduction, it’s the Singapore property developer run by Kwek Leng Beng.

Tikehau capital on the other hand, is a French investment company. They’re no slouch to be fair, with about €25.7 billion AUM:

Tikehau Capital SCA is a France-based asset management and investment company. The Company invests in various asset classes, including Private Debt, which comprises debt financing transactions, such as senior debt, unitranche and mezzanine, as well as collateralized loan obligations; Real Estate, which focuses on commercial property and seeks sale and lease-back transactions in which the Company’s vehicles act as purchaser; Private Equity, which encompasses investments in the equity capital of listed and non-listed companies, and Liquid Strategies, which encompasses investments in bonds, investment grade securities and the management of open-ended funds. The Company operates either through direct equity investments or through its asset management subsidiary, Tikehau IM, on behalf of institutional and private investors. The Company has offices in Paris, London, Brussels, New York and Singapore, among others.

Tikehau holds 29% while CDL holds 21% of IREIT. Collectively, they hold almost 50% of the REIT, which is a really strong alignment of interests from the controlling shareholders / “Sponsors”.

This is a really strong plus point in favour of IREIT Global.

I like this part.

Will I subscribe for the rights issue?

I think I have no choice really.

If I don’t take up the rights, I get diluted out, especially when they’re priced at 0.49 which is almost a 20% discount to its current price of $0.60.

I think there’s no way around it. If I wanted to sell, I should have sold before it went ex-rights, or I should sell a couple of months after this transaction.

Not subscribing and getting diluted out just makes very little sense to me.

Is IREIT a good long term investment?

Here’s where it gets tricky.

I liked IREIT Global a lot more when it was a sleepy REIT with German offices.

I don’t like it so much when they start going down the path of acquiring buildings at steep valuations, in the midst of a pandemic, with a dilutive equity offering.

Now I get the long-term rationale for this acquisition. Longer term, high quality commercial real estate located in major population centers like Madrid and Barcelona are still going to do well. Especially when we kick into the inflationary phase down the road.

I also get that this transaction was already contemplated since IREIT acquired the 40% stake last year.

But things change. COVID was a big gamechanger.

And with all that is going down now, I frankly think purchase price looks pricey here. 2% to 3% cap rates for office buildings are on the high side.

Weighted Average Leave Expiry (WALE) for the acquisition portfolio is 4.1 years, so there could also be leasing pressure in time to come. This isn’t one of those 10 + 10 year master leases locked in for a long time.

Closing Thoughts

That said, I think IREIT is probably still a decent REIT. It’s been a sleepy REIT since IPO, which I like because that meant stable distributions and very low price volatility.

I don’t quite like this new direction for the REIT, but I think the strong alignment of interests from the controlling shareholders still means that this REIT shouldn’t be treated too badly. It’s not like some of the other smaller cap REITs out there (not naming names).

That said, I’ve been doing some portfolio pruning recently, trying to cut down on bloat and rebalance my portfolio.

And frankly speaking, I don’t think IREIT has a strong place in my revamped portfolio.

It’s such a small position for me that the trouble of keeping up to date with the REIT is more effort than it’s worth, and this acquisition in particular is troubling.

So down the road, after the dust settles, I’ll might just sell off my stake if I can get a good price for it on the open market.

Love to hear what you think though. Share your thoughts below!

Note: This article is a premium article that first appeared on Patron. If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

hi FH, actually instead of subscribing, why don’t you sell the rights and liquify the position instead? I’m in the same boat as you (small position) and considering my options as well. Personally i don’t like this massive dilution

The problem is that I may not be able to get a good price for the rights, because everyone is selling at the same time. Usually if one holds on until after the dust settles, one can get a better price then.

But yes, if the rights are at an attractive price, this is worth a shot.

Hi FH,

Good analysis. It really makes one wonder why they would do such a hugely dilutive rights issue and overpay for the Spanish properties.

I think the reason they are willing to do it is because the sponsors upped their stake massively at 40+ cents during the Mar crash so they are not hurt by this.

Then it makes one wonder if they have the interests of other investors at heart or not.

Yes that’s a good point. I would have suspected they did this to offload the property from their books and raise cash (that can be deployed elsewhere given that COVID is going on), but that really brings us into speculation territory, and only the sponsor themselves will know for certain.

That said, I do agree that this raises some questions about the long term alignment of interests, hence my inclination to close off the position down the road if I get a chance.

The NPI given is only for 6 month period, so the cap rate is double what you calculated before. Nonetheless this is a NAV and DPU yield destroying deal…

Thanks, you are right, my bad on the cap rates. I have updated them accordingly.

Properties make a lot more sense at this price, but with COVID I would still have preferred to see them cheaper. Otherwise, current deal is NAV/DPU dilutive.