As most of you would know.

There are only four 1-year T-Bills each year – one every quarter.

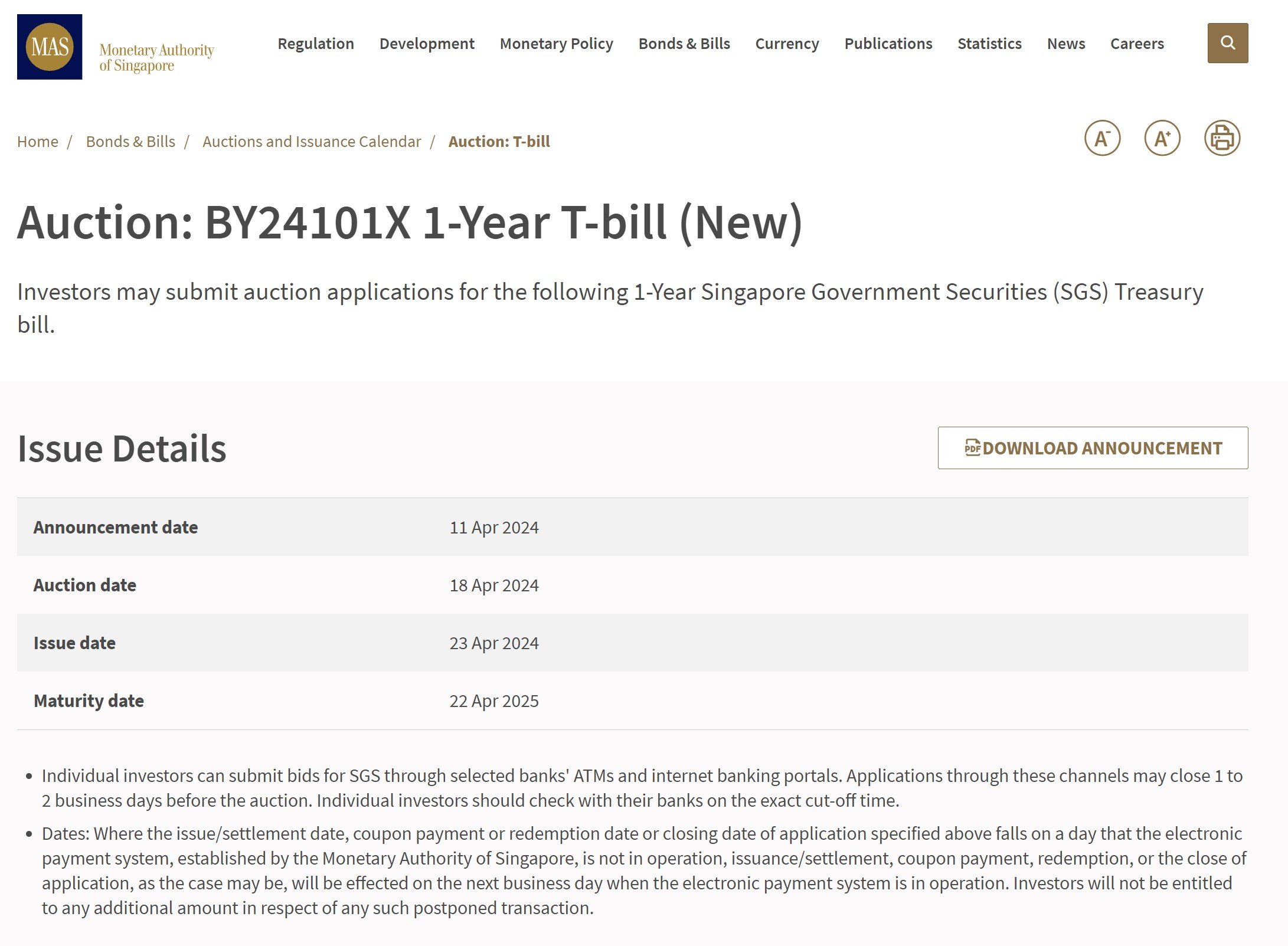

And the next one is coming up on 18 April – so if you want 1-year T-Bills you really should apply as the next one wouldn’t be for another 3 months.

Given expectations over interest rate cuts in 2024/2025.

1-year T-Bills might be a good way to lock in interest rates going forward, if you don’t need the liquidity.

Especially for CPF-OA buyers, as you minimise the lost interest from rolling over 6-month T-Bills.

The problem of course, is that if everyone thinks this way, then you’ll see a lot of demand for the 1-year T-Bills, sending yields down.

Couple of questions I wanted to discuss today:

- What is the estimated yield on the next 1-year T-Bills?

- Should you buy 6-month or 1-year T-Bills? What about for CPF-OA buyers?

- Where to park cash – 1 year T-Bills vs 6-month T-Bills vs Fixed Deposits or Money Market Funds?

Next 1-year T-Bills auction is on 18 April (Thursday) – (BY24101X 1-Year T-bill)

First off – the next 1-year T-Bills auction is on 18 April (Thurs).

Deadline for CPF-OA applications is same as cash applications?

I’ve noticed recently that with DBS, the deadline for CPF-OA applications (via ibanking) is the same as cash applications, so there is no need to submit 1 day earlier if you’re applying with CPF.

If so, the deadline for applications would be 9pm on 17 April (Wed) – whether you’re buying with Cash, SRS or CPF-OA.

Can’t confirm for UOB/OCBC though, so let me know if you guys have personal experience on this.

What is the estimated yield on the next 1-year T-Bills auction? (BY24101X 1-Year T-bill)

I’ll split the analysis up into 2 parts:

- Fundamentals perspective (economic growth, inflation, global interest rates etc)

- Technical perspective (supply-demand)

(1) Fundamentals perspective:

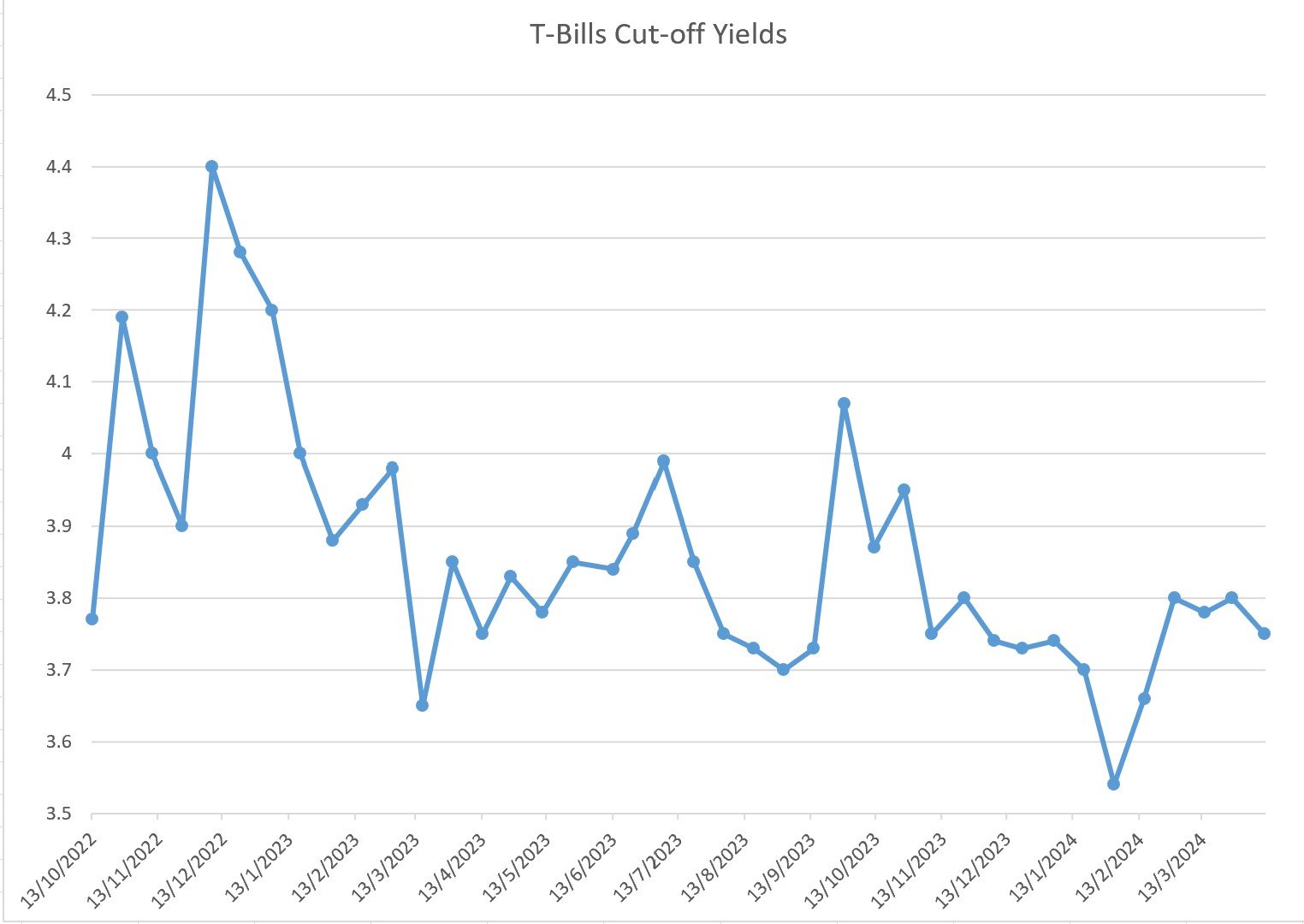

1-year T-Bills trade at 3.60% on the open market

1-year T-Bills are trading at 3.60% on the open market.

But… T-Bill trading liquidity is incredibly thin

But we’ve seen the past few auctions that trading liquidity on the T-Bills is so thin (just look at trading liquidity in the chart above) – that actually the market pricing is not that indicative.

You’ll find that the market pricing actually takes its cue from the T-Bills auction, and not the other way round.

So I would caution against placing too much reliance on market pricing on T-Bills – there just isn’t sufficient trading liquidity for true price discovery.

What about interest rate cuts? What is the market pricing in?

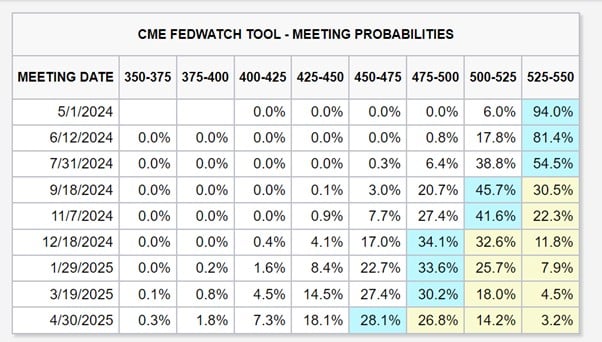

After this week’s inflation data (which shows US inflation is reaccelerating and no longer coming down – which creates a big problem for the Feds looking to cut interest rates in the second half of 2024).

The market is now only pricing in 2 interest rate cuts – starting in Sep 2024:

I suppose this is bullish for the 1-year T-Bills, because less rate cuts would imply higher yields on the 1-year T-Bills.

But… is the market correct on less rate cuts?

Spin in whatever way you like.

But the US economy remains very resilient.

I said in late 2023 that the early pivot from the Treasury/Feds creates the risk of allowing inflation to return.

3 – 4 months on, that looks to be exactly what’s happened.

Had Janet Yellen and Jerome Powell stuck to their guns a few more months and allowed the pain in markets to play out in Q4 2023, we might be looking at a very different inflation environment today.

But they chose to take the foot off the pedal at that crucial juncture, allowing stock markets to inflation, and significantly easing financial conditions – allowing inflation to return.

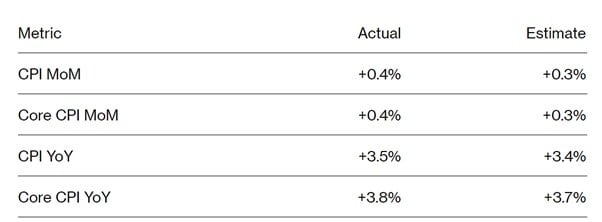

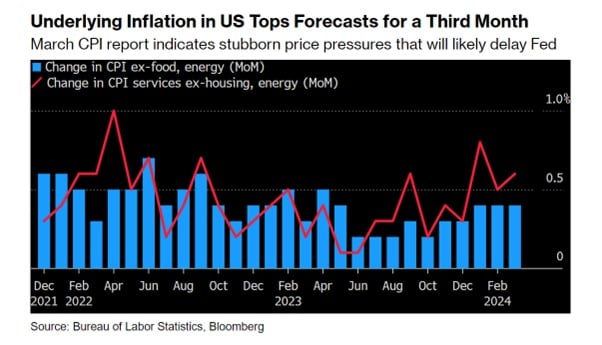

You can see how latest March US CPI numbers came in hotter than expected on all fronts.

0.4% month on month increase in both CPI and core CPI.

Core CPI up 3.8% year on year.

If the Feds cut interest rates with this kind of inflation numbers, I would be really worried about a second wave of inflation.

The complexity of course, is that 2024 is a US election year, and Biden would want rate cuts in 2H 2024 heading into the elections.

Does Powell oblige him, even if inflation data stops coming down?

I really don’t know.

From a Technicals, supply-demand perspective

From a more micro perspective, what matters is the supply-demand dynamics.

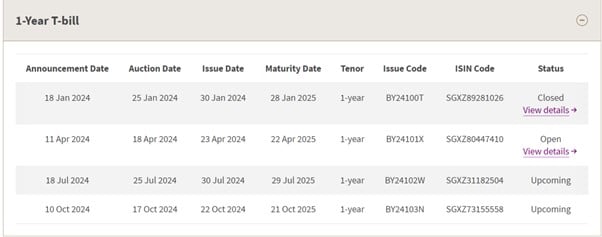

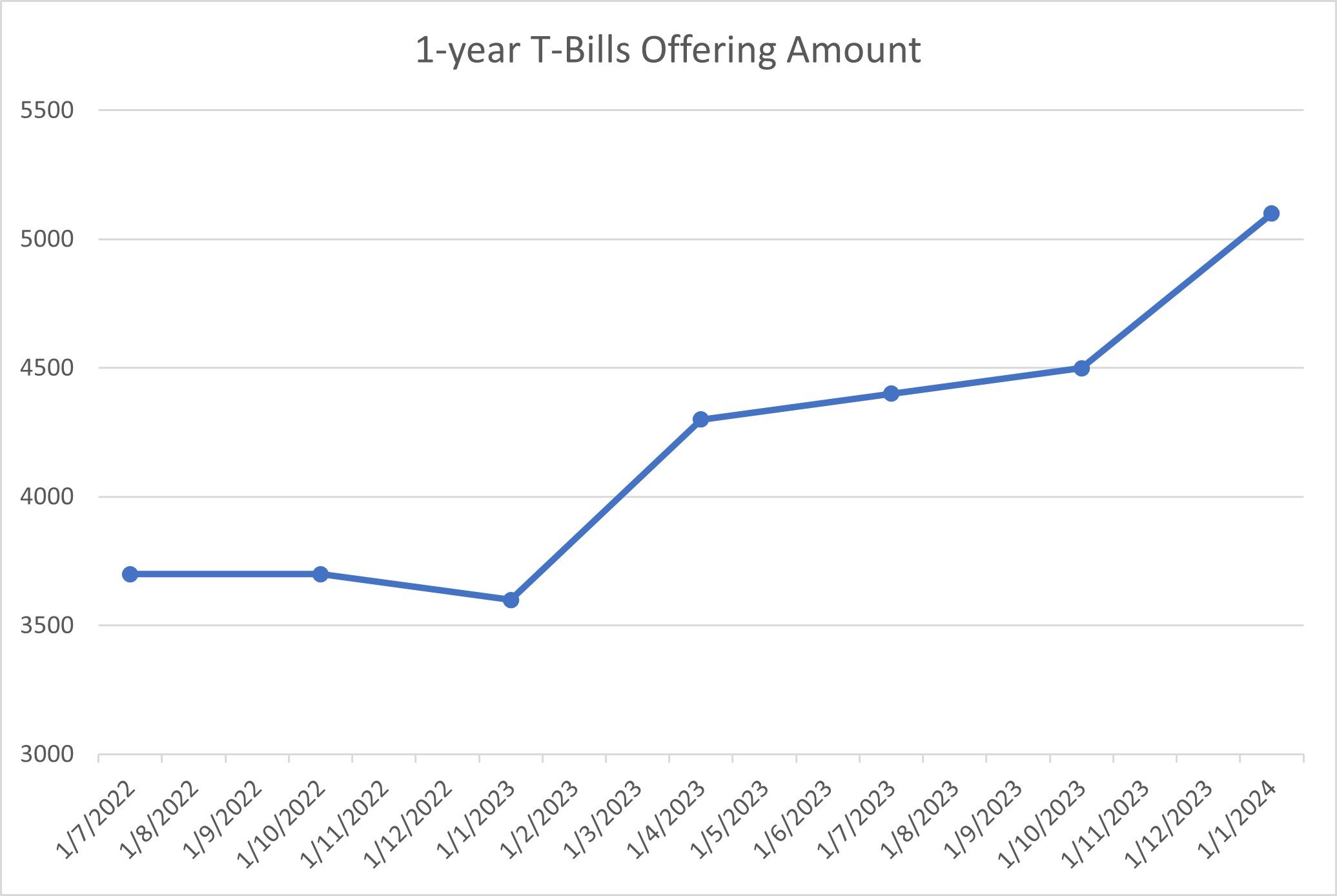

T-Bills Supply is up to $5.1 billion (vs $4.5 billion in the Jan 2024 auction)

The amount of 1-year T-Bills on offer is $5.1 billion, a 13% increase vs the previous 1-year T-Bills auction.

This is good, as higher supply usually translates into higher yields.

Do note that this $5.1 billion is substantially lower than the amount on offer for 6-month T-Bills auctions though ($6.3 billion at the most recent auction).

Demand for 1-year T-Bills might be very high – may skew yields down below market yields

Demand for 1-year T-Bills typically tends to be very high, given that there are only 4 such auctions each year.

1-year T-Bills are also very attractive for CPF-OA buyers, as you minimise the lost interest when you roll over the 6-month T-Bills.

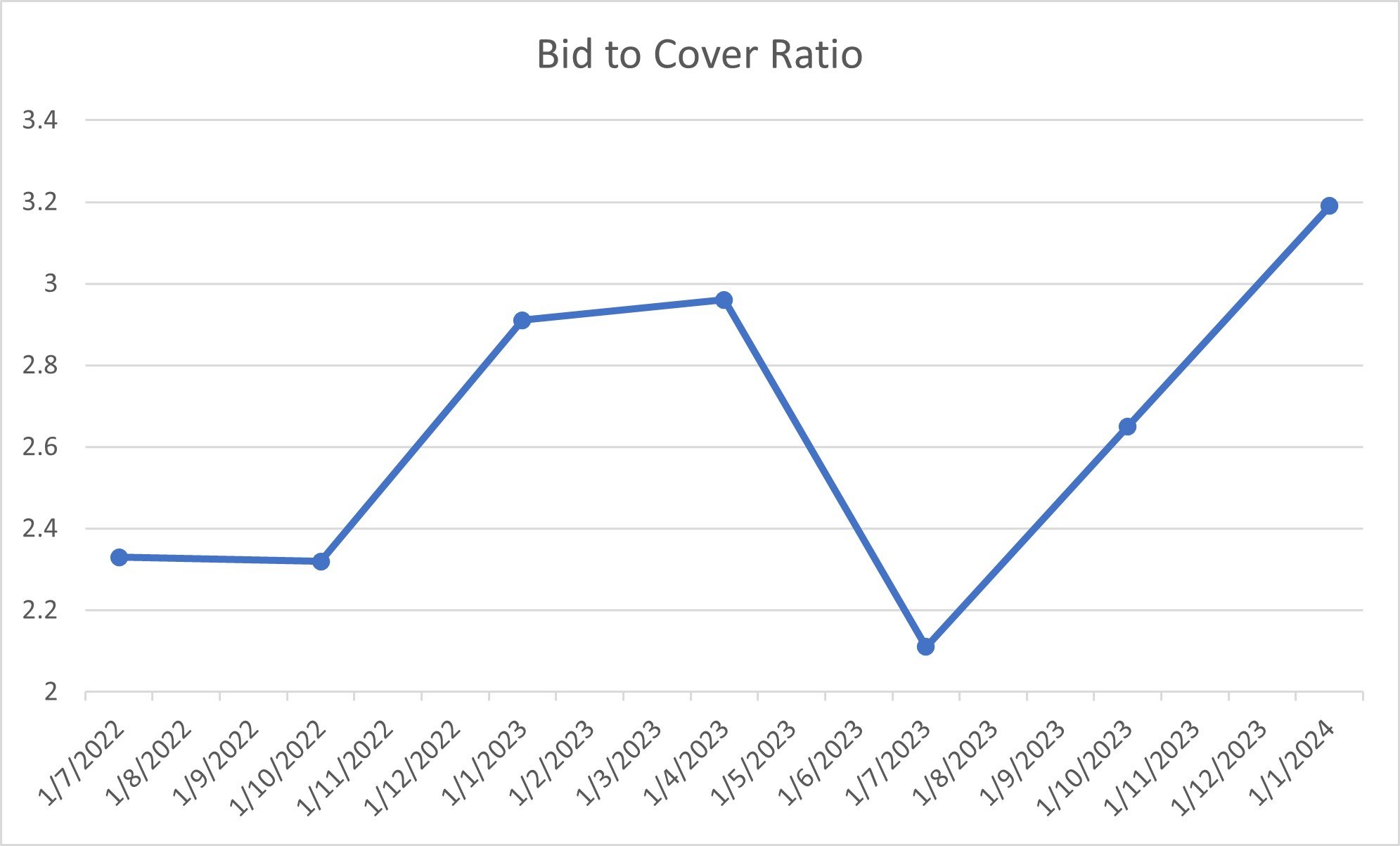

Here is the bid-cover ratio for the past 6 auctions.

You’re looking at easily more than double the demand vs the amount on offer – and in the most recent auction it went up to 3.2 times:

Because of this, most of the previous 1-year T-Bills auctions have cut-off yields that come in below market yields.

In the Jan 24 1-year T-Bills auction – market yields were 3.75%, while the final cut-off yield was 3.45% – a whole 0.3% lower than the market yield

It looks like we may see the same here.

Which means 3.60% might be the upper limits of the cut-off yields for this auction.

Demand for 6-month T-Bills is at record highs, pressuring yields

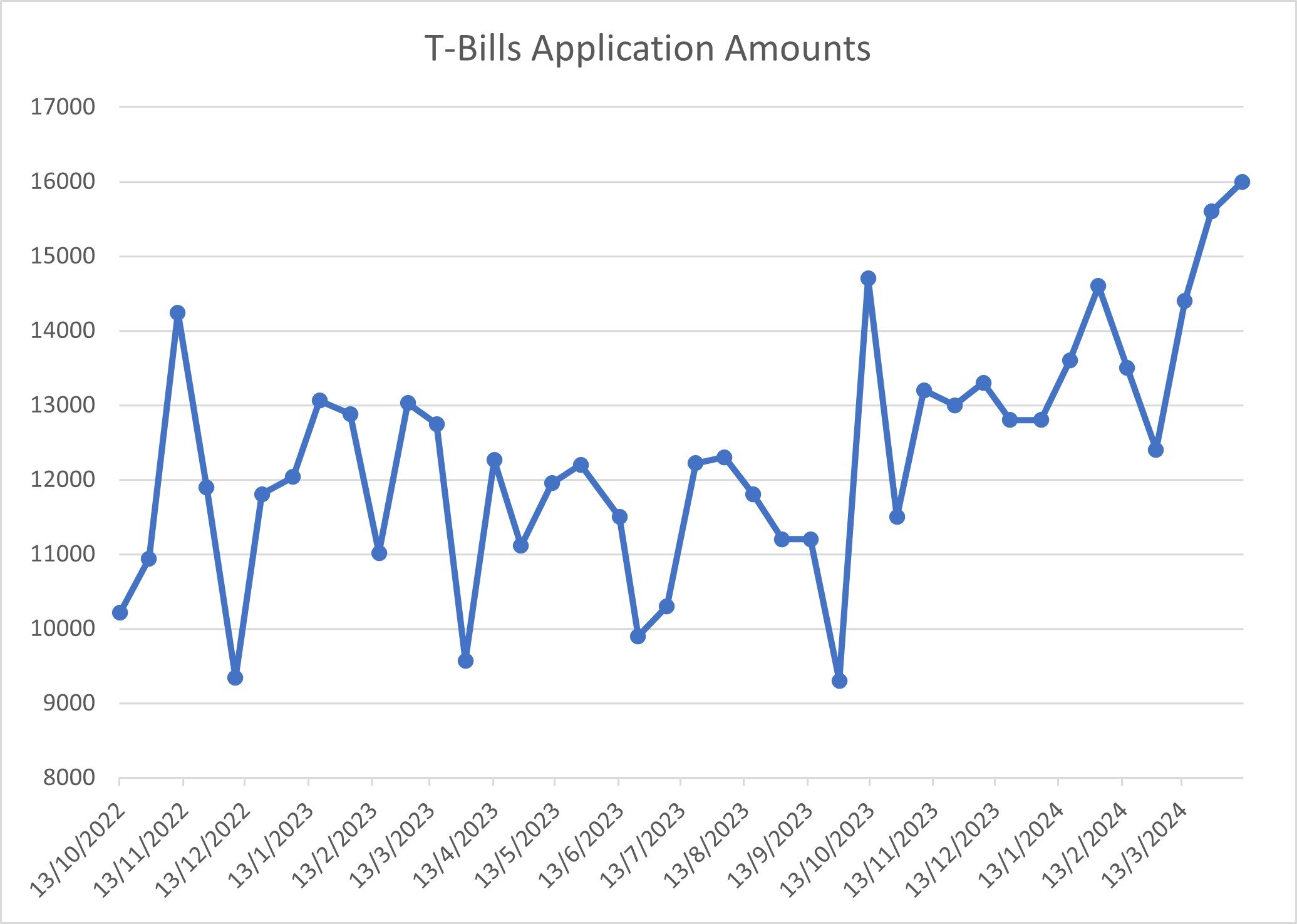

Given that there are only 4 1-year T-Bills each year, let’s take a look at the 6-month T-Bills to give us an idea of market demand.

In the latest 6-month T-Bills auction, demand remains very strong.

At $16.0 billion, it’s the highest in the past 18 months since interest rates started going up.

This is not a good sign, as it shows very strong demand for T-Bills, which is likely to spill over into this 1-year T-Bills.

This led to T-Bills yields dropping to 3.75% (vs 3.80% the previous auction):

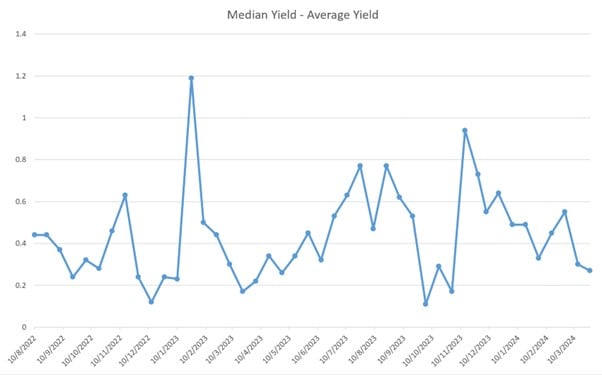

However, the spread between median and average yields remains low, which suggests rational bidding from investors (although it could be due to the recent stabilisation in yields).

Estimated yield of 3.30% – 3.60% on the 6-month T-Bills auction? (BY24101X 1-Year T-bill)

So the good news is that the amount of 1-year T-Bills on offer is up this auction, at $5.1 billion.

The other good news, is that the market is now pricing in less rate cuts in 2024, which should be good for 1-year yields.

The bad news though, is that demand for T-Bills sits at record highs for this cycle.

With a record $16 billion in demand for the 6-month T-Bills, you’re likely to see some of that demand spill over into the 1-year T-Bills.

1-year T-Bills tend to be especially popular among CPF-OA investors too, as they allow you to minimise lost CPF-OA interest, and lock in interest rates for a whole 12 months.

Because of this, I think the market yield of 3.60% is likely to be the upper end of the range.

I’m going to go with a conservative 3.30% – 3.60% anticipated yield for the 1-year T-Bills.

I know it’s a large range, but the 1-year T-Bills are notoriously volatile and hard to predict because there are only 4 a year.

This means very little market data, as well as investors who submit lowball bids to ensure an allocation.

Gun on my head if you forced me to narrow the range, I would say maybe 3.30% – 3.50% indicative.

Are 6-month T-Bills a better buy than 1-year T-Bills?

I think it really goes back to the yields you get on the 1-year T-Bills.

Let’s say worst case the 1-year T-Bills come in at 3.4% yield.

That means that if you buy the latest 6-month T-Bills at 3.75% yield, as long as you can roll over the cash into 3.10% or more yields in 6 months time, you’re probably ahead (technically it’s 3.05% but I buffered in a margin of safety for the time in between T-Bills).

Can you roll over into T-Bills at 3.10% or higher in 6 months time?

Who knows, frankly.

What would I do? Stick with 6-month T-Bills?

Personally I will not be applying for the 1-year T-Bills.

I’m a huge sucker for liquidity, and I don’t like having cash tied up for a whole 12 months that I cannot get back before maturity.

If the yields were higher vs 6-month T-Bills maybe I would be open to it.

But by all indications it doesn’t look like the yields would be higher, and best case they would match the 6-month T-Bills.

In which case I would just stick with the 6-month T-Bills.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What about for CPF-OA buyers? Buy 6-month T-Bills or 12-month T-Bills?

For CPF-OA buyers though, the 1-year T-Bills are pretty attractive because:

- You lock in interest rates for the next 1-year (in fact you get the interest upfront)

- You minimise the lost interest from when you roll over 6-month T-Bills

So I can see a lot of CPF-OA buyers going for this 1-year T-Bills.

Which perversely, has the potential to skew yields down.

So you might want to consider putting in a competitive bid, just in case there is a freak result.

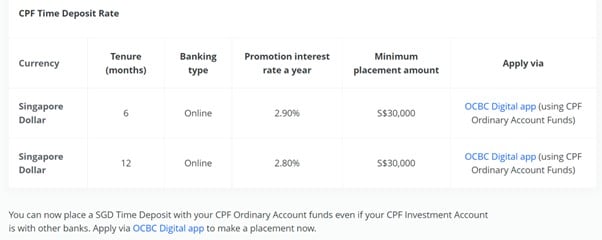

OCBC has a CPF Fixed Deposit – 2.8% for 1 year

Do note that OCBC has a CPF Fixed Deposit.

However the interest rate at 2.8% for 12 months is not attractive at all, so you’re still better off using buying T-Bills.

Even if demand is very high, I doubt of the 1-year T-Bills would come in below 2.80%.

Where to park cash – 1 year T-Bills vs 6-month T-Bills vs Fixed Deposits or Money Market Funds?

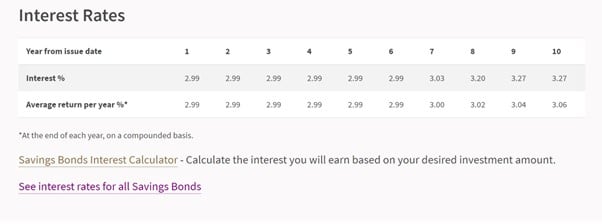

Singapore Savings Bonds are actually a decent buy – 2.99% for 1-year

I just want to put it out there that the yields on the latest Singapore Savings Bonds are pretty decent.

- 2.99% for the first 6 years

- 3.06% for 10 years

If you look at the latest Singapore 10 year yields, you’ll see they shot up quite a bit this month.

If this holds up, we might see even higher yields on the next SSB – perhaps up to 3.2%.

Given that this allows you to lock in yields for up to 10 years, yet redeem any time with no risk of capital loss, it’s a pretty decent alternative to the 1-year T-Bills.

Money Market Funds pay about 3.5% – 3.8% yield – but not risk free, and yields can change any time

Money Market Fund yields have been dropping of late though (MariInvest, Fullerton SGD Cash Fund etc).

We’re looking at about 3.5% – 3.8% yields.

Money Market Funds are technically not risk free though – so this is a big point to note.

And Money Market Funds invest in short term instruments, so the interest rates will fluctuate from time to time.

This is unlike a 1-year T-Bill where you are “locking in” interest rates for the full 1-year.

The benefit though, is that you can get your money back with T+1 liquidity, which is a big plus vs T-Bills

Best Fixed Deposit option? 3.20% for 1-year with DBS/POSB Bank

As shared in yesterday’s article, the best fixed deposit option for 12-months is 3.20% with DBS / POSB Bank.

If you’re comfortable using Syfe Cash+ Guaranteed (where you deposit with Syfe who parks the funds in an institutional fixed deposit account for higher yields).

Then the yields go as high as 3.5%, but do note that this is NOT SDIC insured (and therefore not risk free).

So basically 3.20% – 3.50% for fixed deposit options, and I would think the final cut-off yields for the 1-year T-Bills come in around that range too.

Picking between 1-year T-Bills vs Money Market Funds vs Singapore Savings Bonds vs Fixed Deposit vs Savings Accounts?

I would say if you want the highest yield for a locked in 1-year period, T-Bills are probably your best bet.

The other options like Singapore Savings Bonds and Fixed Deposit are unlikely to match the yields on T-Bills.

If you’re okay with Syfe Cash+ Guaranteed you can get 3.5%, but do note that is not SDIC insured and not risk free.

That said based on the rise in 10 year interest rates, next month’s Singapore Savings Bonds might be pretty attractive.

So if you’re looking to lock in some yields for the longer term, that could be an alternative to consider as well.

This article was written on 12 April 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

WeBull Account – Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.