I said a couple of months back with the CICT purchase of ION, that with lower interest rates and recovering REIT prices, we may see more mega acquisitions come to market.

And this week we saw exactly that.

Keppel DC REIT is buying $1.1 billion worth of everyone’s favourite asset class at the moment – AI Data Centres.

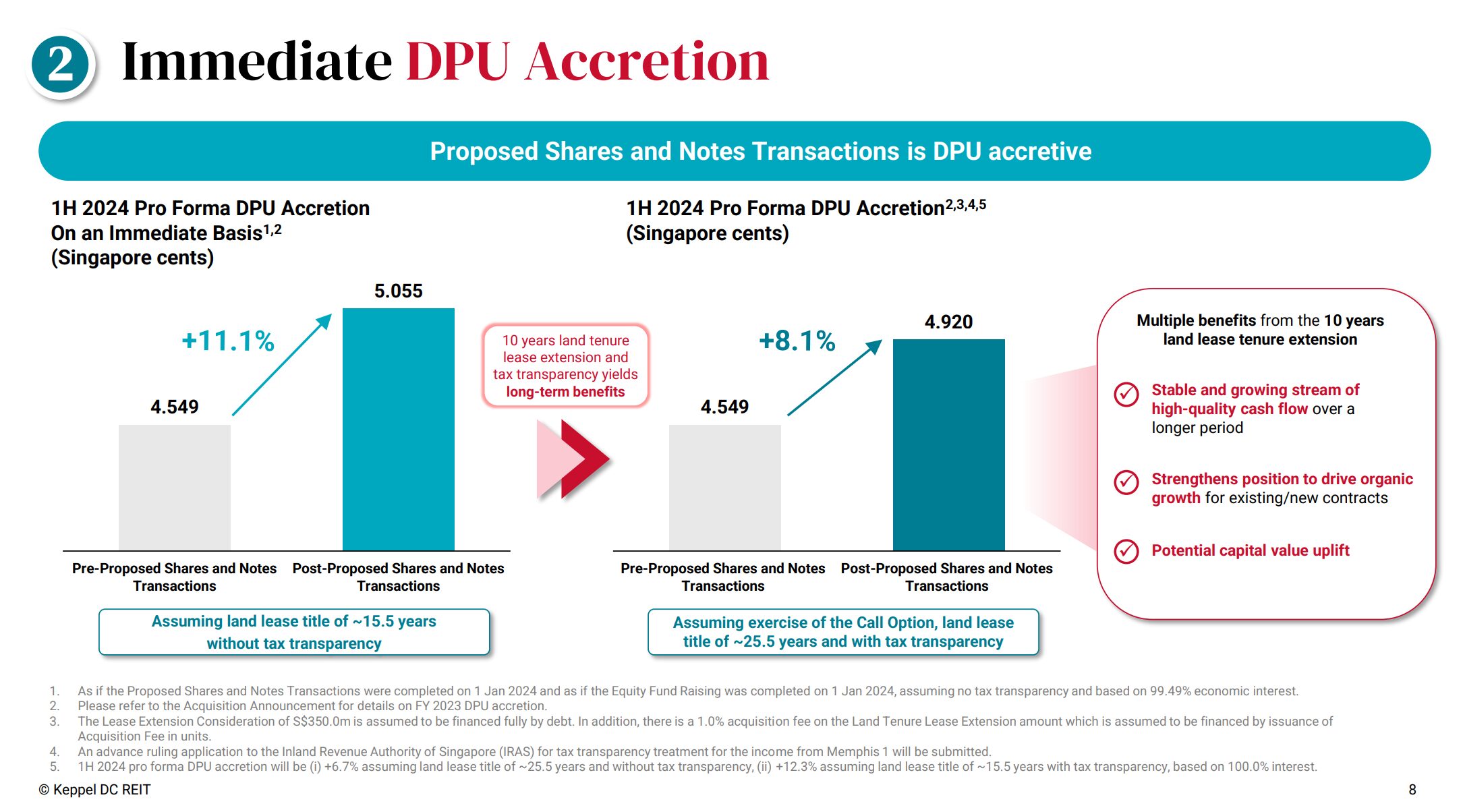

Interestingly the DPU accretion numbers look very strong, and the market reaction to the acquisition was very positive.

So I wanted to take a closer look at Keppel DC REIT – and see whether it is worth buying more of this REIT (Full disclosure that I have a position in Keppel DC REIT).

Keppel DC REIT buys $1.1 billion worth of Artificial Intelligence (AI) Data Centres

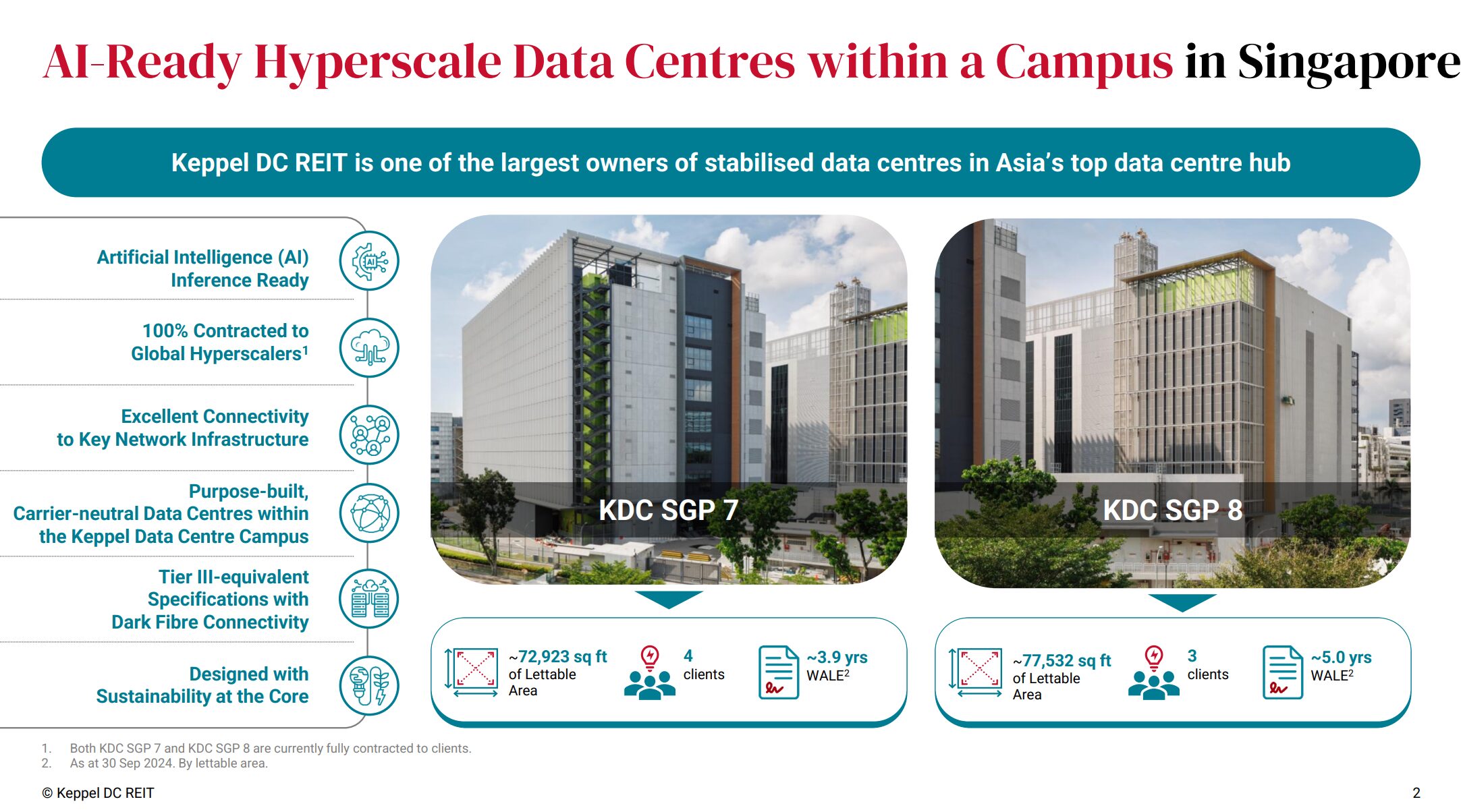

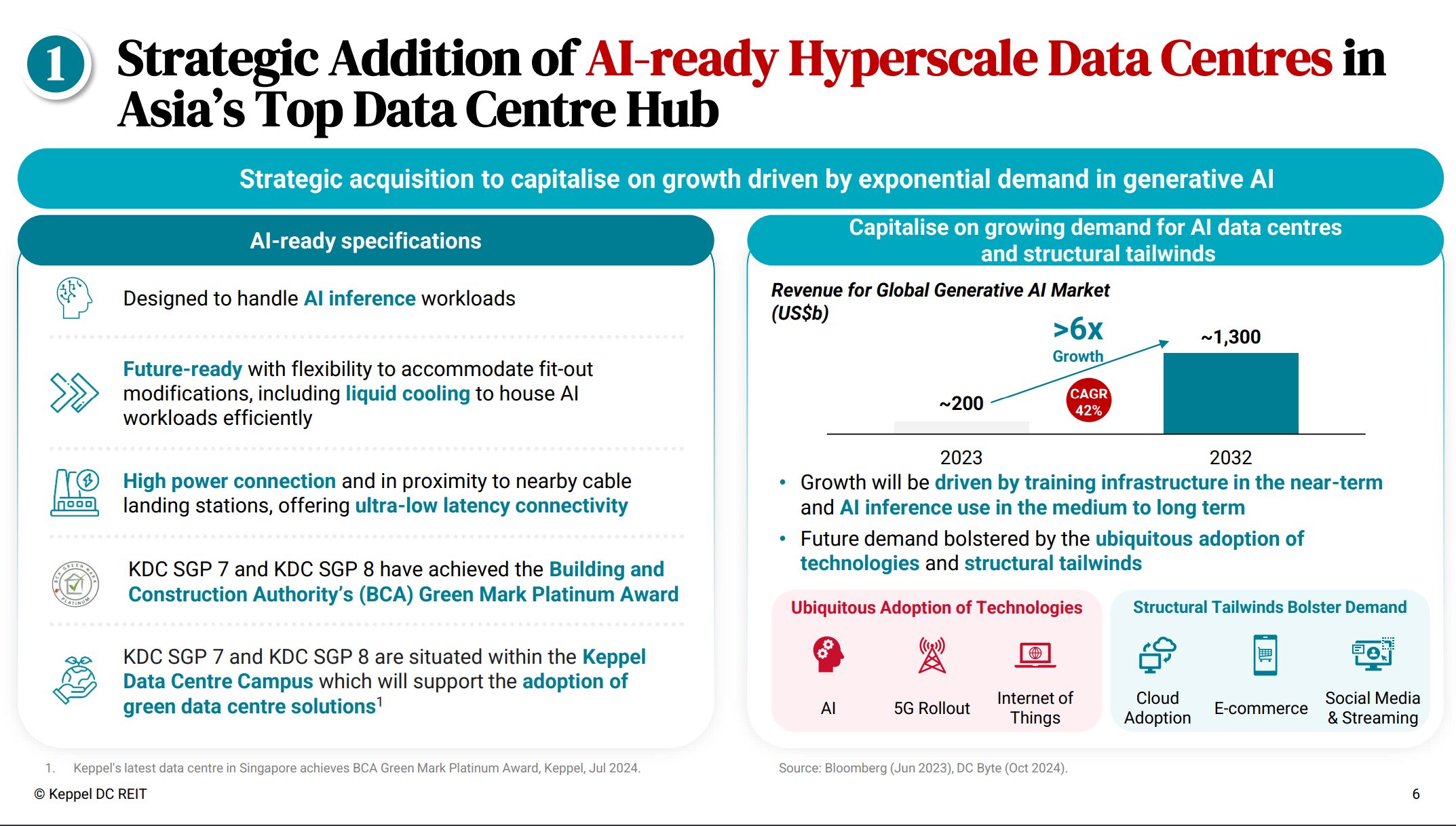

Keppel DC REIT is buying $1.1 billion in Artificial Intelligence ready Hyperscale Data Centres.

AI, Inference Ready, 100% contracted to Global Hyperscalers, located in Singapore.

I mean if you wanted a list of the buzzwords to include in a real estate acquisition today – the above just about hits it on the head.

AI data centres are red hot right now, and being located in Singapore makes them an especially prized asset (as Singapore tightly controls the supply of new data centres due to electricity consumption).

More details on the data centres below.

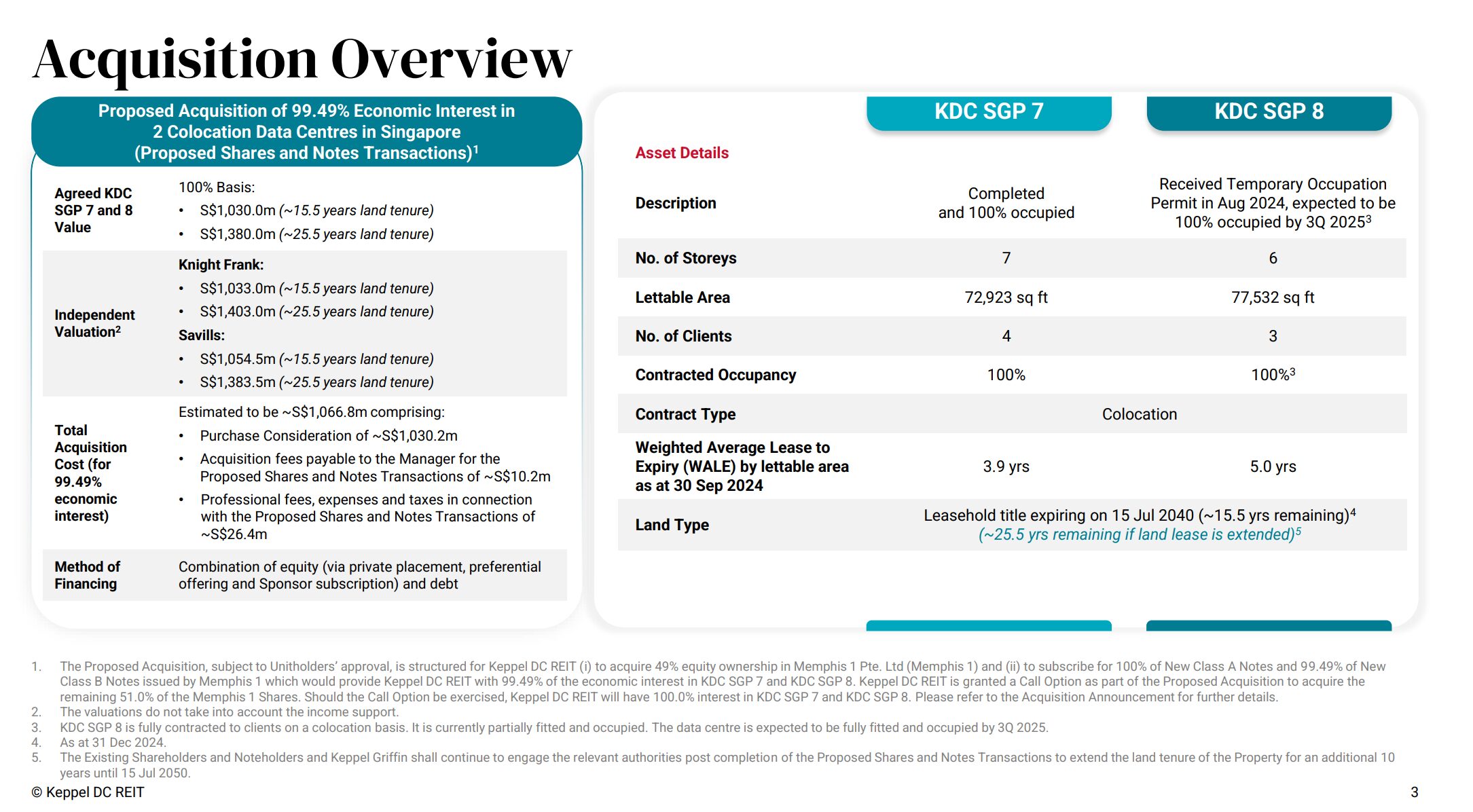

Note that the leasehold title expires on 15 July 2040, so there is only 15.5 years left on the least (25.5 years if the lease is extended).

I know this seems short, but this is pretty much par for the course for these kind of industrial / data centre assets in Singapore.

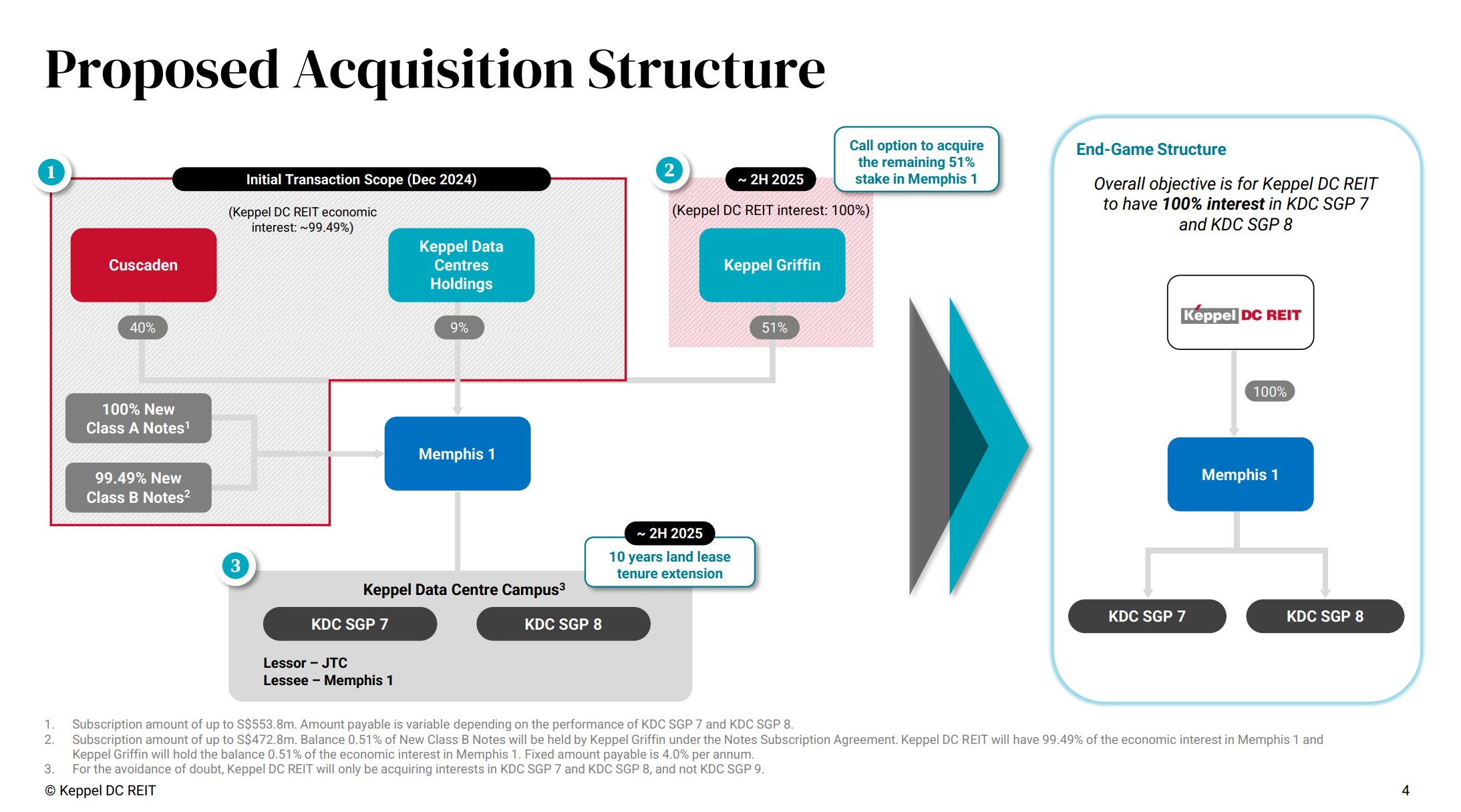

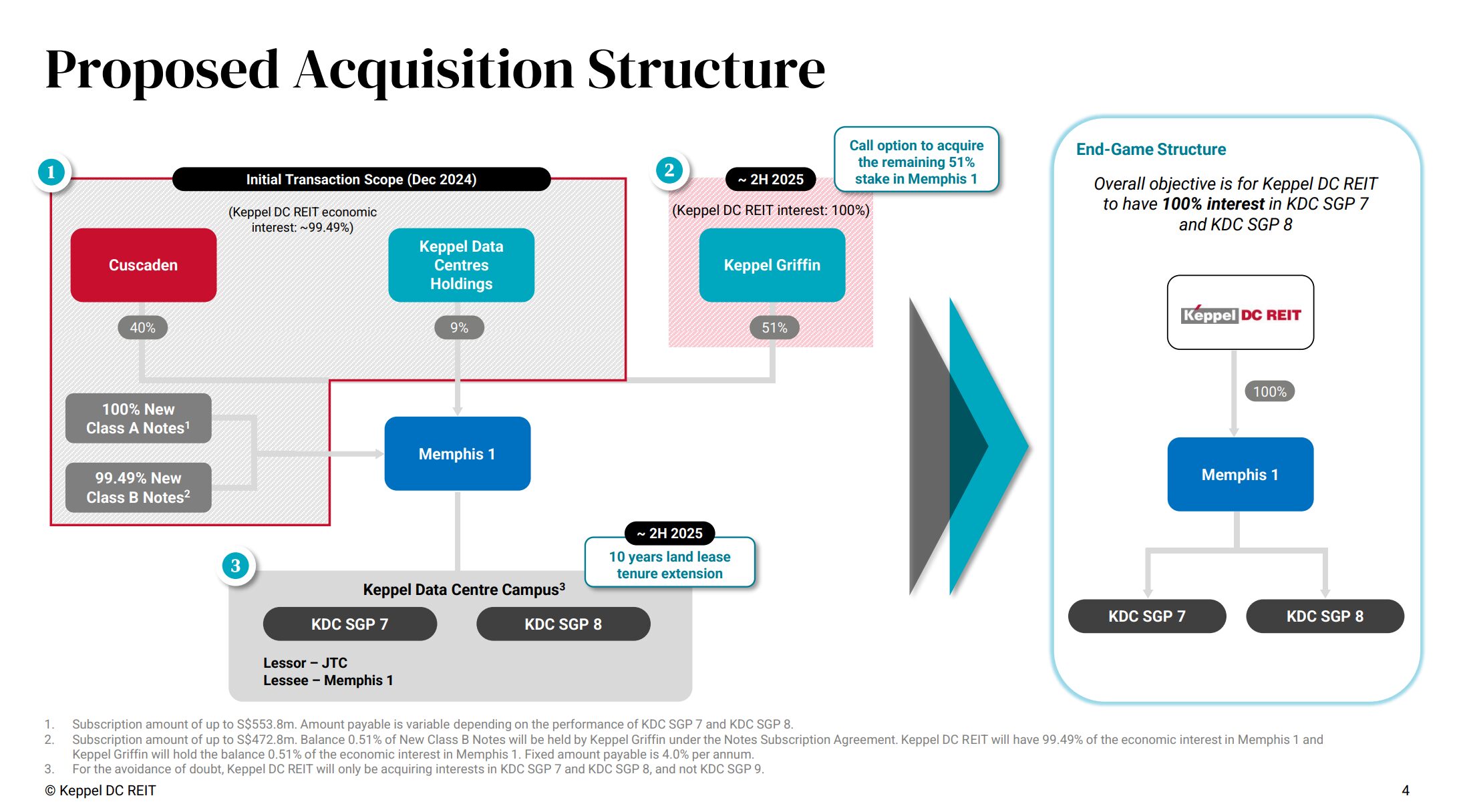

The transaction is split into 2 phases.

First phase is to buy approximately 49% of the data centres, and should be done by end 2024.

The second phase will be to acquire the remaining 51%, and it should complete by 2H 2025:

On paper – the Acquisition looks like a good one for Keppel DC REIT

I’m just going to put it out there that on paper – this looks like a fantastic acquisition for Keppel DC REIT.

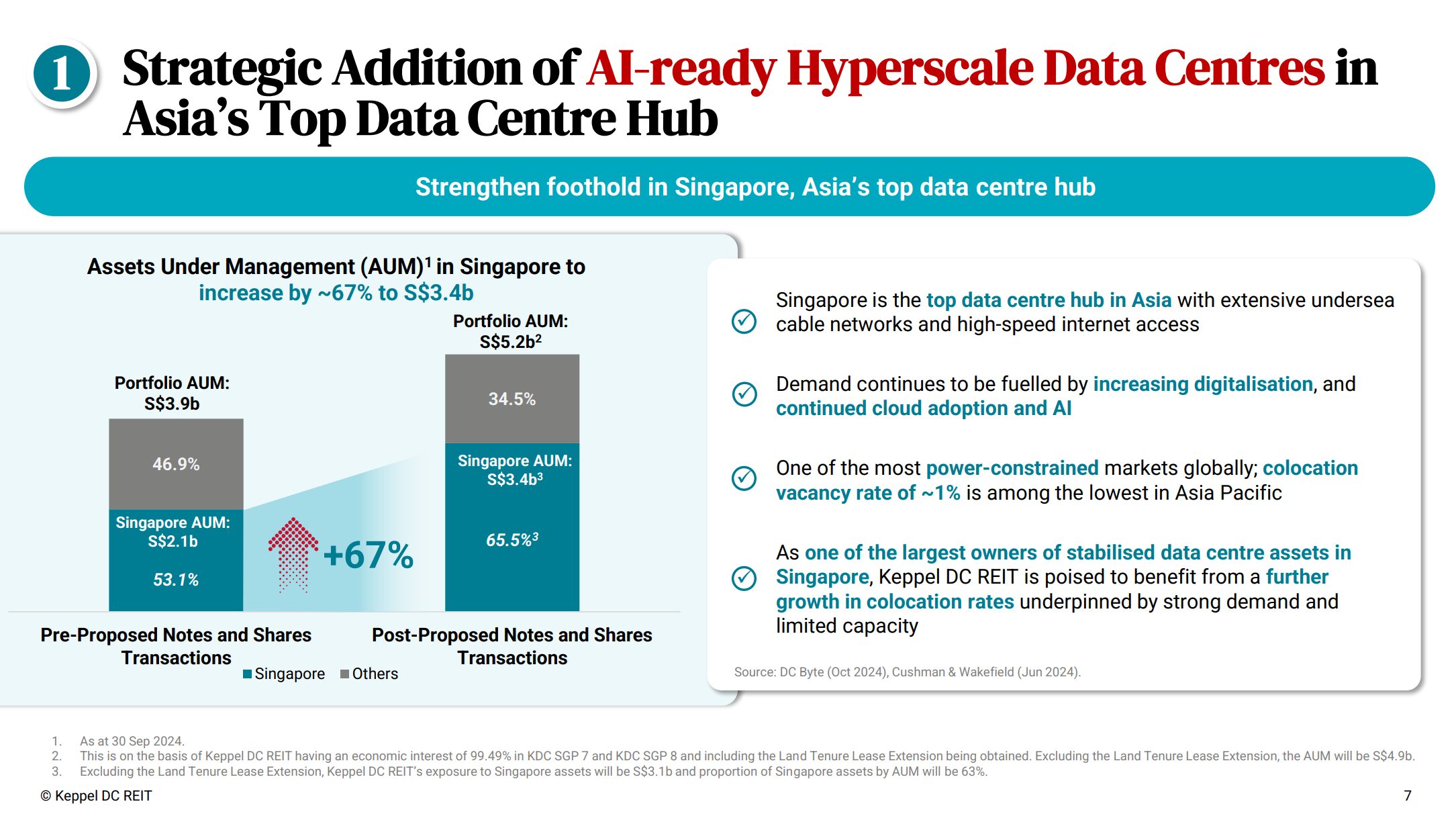

First off – it’s a 67% jump in AUM for Keppel DC REIT.

In this world, you want to either be super big or super small, and Keppel DC REIT increasing it’s AUM massively is a good thing (to be able to compete in the big boy leagues).

And of course – they’re not just driving up AUM for the sake of driving AUM up.

They’re actually buying what is probably the hottest asset class in the market right now – AI data centres, located in Singapore to boot.

But here’s where things start getting really crazy.

The DPU is actually DPU accretive, to the extent of 11.1%?!

Okay depending on the assumptions you use, the DPU accretion may drop to 8.1%.

But still.

Most other deals you see in this market are DPU accretive to the extent of 1%, maybe 2% if you’re lucky.

8.1% is pretty much unheard of.

The icing on the cake.

Is that accordingly to Keppel DC REIT.

The contracted rents for these 2 AI data centres are actually 15% – 20% below market rents.

That’s just crazy talk at this stage.

You get a 8.1% DPU accretion comes from buying AI data centre assets, where market rents can easily go up 20% or more on renewal?

What’s the catch?

If you need any more reason why this is a good deal for Keppel DC REIT.

It turns out after the huge equity fundraise to fund this deal.

The leverage actually drops a whopping 6.4% to a very reasonable 33.3%.

In this era of volatile interest rates, this is worth its weight in gold, and gives the REIT a ton of optionality on how to position going forward.

If it’s too good to be true…

I guess the question is if this is such a good deal for Keppel DC REIT.

Doesn’t that suggest that this is a bad deal for Keppel?

Since they appear to be selling these prized data centre assets as a discount?

For what it’s worth I don’t have any easy answers to this one.

I suppose one reason is that the transaction structure is highly complex and takes place over 3 phases, and it would not be easy to convince any other third party buyer to purchase.

And I suppose that even at this price it’s still a decent deal for Keppel DC REIT as they free up $1.1 billion on their balance sheet.

But hey – if there’s anything I’m missing here on why this acquisition looks so good for Keppel DC REIT, please feel free to point out below.

Follow Financial Horse to avoid missing any post!

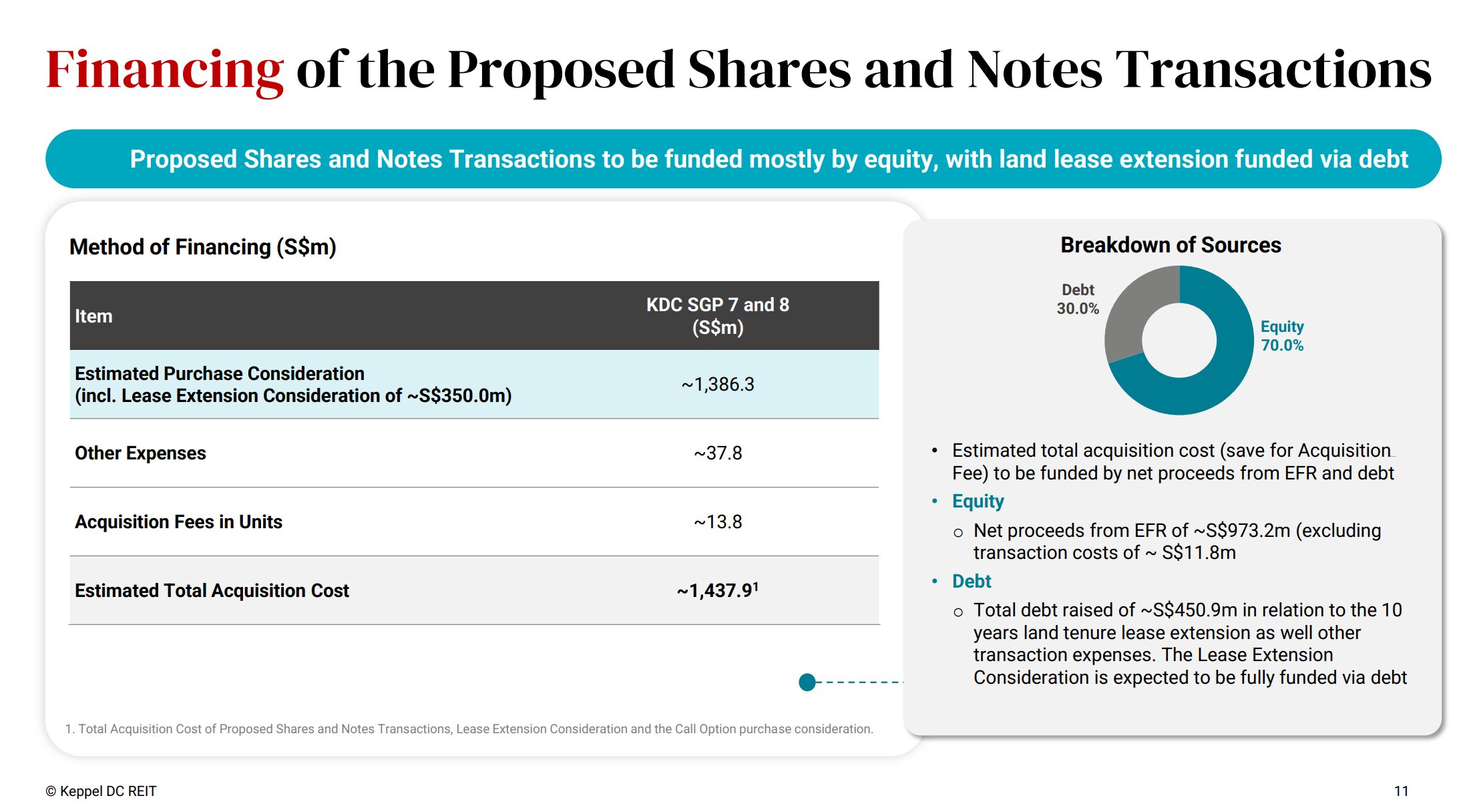

How will the deal be financed by Keppel DC REIT?

The acquisition will be financed via 70% Equity, 30% debt.

Details of the Equity Fundraising by Keppel DC REIT

In total, $1 billion will be raise via the equity fund raising, split broadly as:

$700 million via private placement

$300 million via preferential offering

Private Placement saw very strong demand

The private placement saw very strong demand at 3.4 times cover, and allocation was to primarily long-only investors and real estate investors.

This is not unexpected, since looking at the above this is a very good deal for Keppel DC REIT, and Singapore AI data centres are a very much prized asset:

The Private Placement was 3.4 times covered (including the Upsize Option) and 4.0 times covered (excluding the Upsize Option) with strong demand from new and existing unitholders globally comprising institutional investors and accredited investors. A majority of the Private Placement New Units have been allocated to long-only investors and real estate specialists

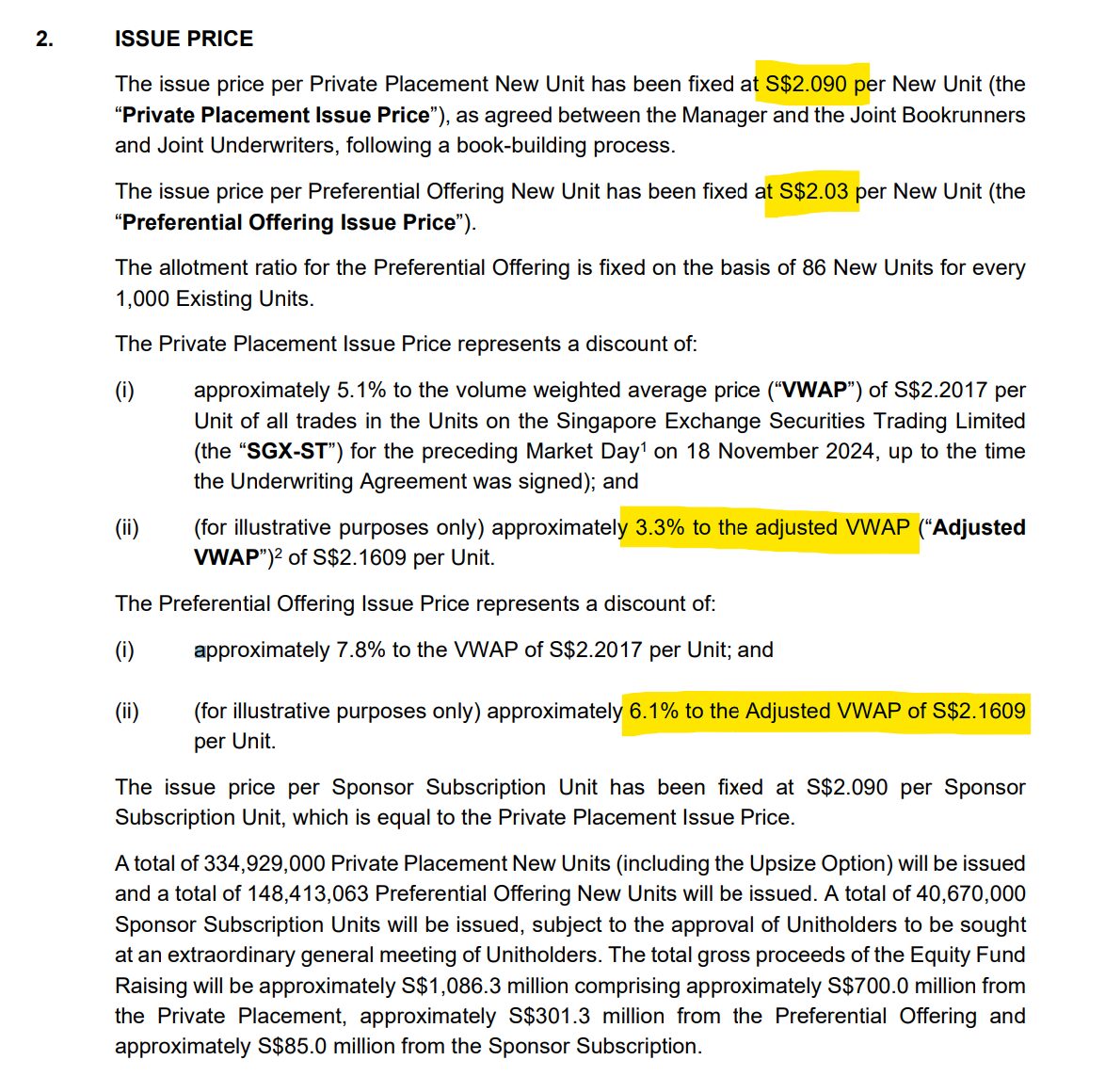

Preferential Offering at $2.03 per unit

The preferential offering will be issued at $2.03 per unit, on the basis of 86 New Units for every 1000 Existing Units.

How did Keppel DC REIT’s share price react?

The immediate share price reaction was actually very positive.

You can see the massive daily candle – on huge volume as well.

And current share price sits above both the 50, 150, and 200 daily moving averages.

Here’s the longer term weekly chart.

Share price is still below the COVID highs.

But it’s up almost 40% from the lows of about 1.6 in late 2023 / early 2024.

Keppel DC REIT pays a 4.3% dividend yield at this price

At this price – even using the higher DPU post acquisition.

You’re only looking at about a 4.3% dividend yield.

Compared to an industrial REIT like Ascendas REIT which pays 5.9% dividend yield, this definitely looks to be on the low side.

But I suppose the benefit is that you are buying into Singapore data centre assets, which are a very prized (and scarce) asset class.

Will I buy more Keppel DC REIT at this price?

Full disclosure that I hold a position in Keppel DC REIT (you can see my full portfolio on FH Premium).

If you recall I wrote a bunch of articles on Keppel DC REIT in late 2023 after the sell-off on the Guangzhou tenant default fears.

And it was around that time that I built my position in Keppel DC REIT, at an average buy in price of about 1.6 – 1.7.

Will I buy more Keppel DC REIT today?

For what it’s worth, I really like this acquisition, and I think it’s a great deal for the REIT.

It’s buying prized data centre assets, at an attractive valuation, and largely funded via equity fundraise when the share price is close to cycle highs.

And on top of that – the acquisition is DPU accretive to the tune of almost double digit percentage.

Valuations of Keppel DC REIT

But I can’t help but shake the feeling that Keppel DC REIT is very richly priced today.

Long time readers know that I like to use an “Effective Cap Rate” concept for REITs.

That’s basically taking the Net Property Income divided by (Market Cap + Outstanding Debt).

If you use the pro-forma NPI for Keppel DC REIT post acquisition.

You get about a 4%ish effective cap rate for the REIT.

4%ish cap rate for Singapore Data Centre assets, in a climate where the Singapore 10 year government bond yields about 2.9%.

I wouldn’t say that’s expensive, but neither would I say it’s dirt cheap.

At best I would say that’s fairly valued.

Will I buy more Keppel DC REIT at this price?

I like the data centre assets, and I like the acquisition.

I just don’t like the price.

Or rather, I don’t like the price enough to add to my position in Keppel DC REIT in a big way.

The preferential offering at $2.03 is still a no brainer because you can literally sell your existing units today and subscribe to them back at $2.03 down the road for a risk free arbitrage.

But at this price, I don’t really see myself adding to Keppel DC REIT in a big way.

I’ll probably still hold onto my existing units for now, but if the share price gets really crazy, or I see other opportunities in the market, I don’t think I’ve above selling and locking in a profit in Keppel DC REIT.

As always – This post is written on 22 Nov 2024 and will not be updated going forward.

I’ll share updates as and when I buy / sell Keppel DC REIT on FH Premium.

I’ll also be updating the FH Stock / REIT Watchlist this weekend to share the stocks / REITs that I am interested to add.

Hi FH,

Why do you include outstanding debt for cap rate?

Net Property Income divided by (Market Cap + Outstanding Debt)

Thanks.

I want to understand the price I am paying for the underlying real estate, without the debt. If you don’t add the debt back it you cant compare across REITs as the leverage will affect the analysis.

It’s like buying a HDB, if you buy a HDB for 200k but the house comes with 400k of debt loaded on it, you’re actually paying 600k for the property.

Thanks FH!

Hi FH, you mention that you bought the reit at pretty low price as compared to now, would you subscribe to the preferential offering at $2.03? Not an easy decision if the offering price is way above the price you bought as I face similar dilemma

Why should you not take it? It will increase your average buy price but you buy them below market value.

Yes I will still subscribe as it is below market price. You can literally sell the units today (and subscribe down the road) if you dont want to increase your exposure to the REIT, and play a risk free arbitrage.

/QUOTE/ First phase is to buy approximately 49% of the data centres, and should be done by end 2025.

/UNQUOTE/

I believe this is a typo, should be end 2024

Thanks you’re absolutely right, have corrected this.