Okay first off – my apologies.

Quite a few of you have asked for my views on Keppel Infrastructure Trust back when they were doing a rights issue (a few weeks ago).

I had promised to do an article on Keppel Infrastructure Trust then – but unfortunately it took me longer than I expected to finish up the research on this REIT (okay technically business trust, but let’s just view it as an infrastructure REIT for now).

In any case, I’ve finally wrapped my head around what this infrastructure REIT is, and I must say I really liked what I saw.

So let me share full views in this article, and why I may buy a position in Keppel Infrastructure Trust going forward.

What I like about Keppel Infrastructure Trust

Let’s start with what I like about Keppel Infrastructure Trust.

Prices of Keppel Infrastructure Trust are down after the Rights Issue

Keppel Infrastructure Trust did an equity fund raising recently, where they issued:

- Placement Units at 47.7 cents

- Rights Issue Units at 46.7 cents

Current price of $0.49 is only a 2.7% premium to the placement price, and 4.9% premium to the rights issue price.

And also down from the all time highs of $0.55.

At a nominal level (not rights adjusted), this is the lows hit in November 2022, and back to where it was in Jan 2022 before the Ukraine war.

Keppel Infrastructure Trust is an Infrastructure Play

And what do you get for that price?

Here’s Keppel Infrastructure Trust’s investment strategy, in their own words (emphasis mine):

“KIT’s investment strategy is to build a well-diversified portfolio of businesses and assets that exhibits linkage to economic growth and domestic inflation. This will support the long-term growth of KIT’s distributions and contribute to a sustainable future.

…

With a focus on evergreen, yield-accretive businesses and assets that will benefit from long-term growth trends, KIT’s key target sectors include traditional infrastructure with long-term utility-like contracted cash flows, infrastructure that will benefit from the low-carbon economy and support the digital economy, as well as infrastructure that will enhance economic growth and social wellbeing.”

So… an infrastructure REIT with exposure to utilities, green energy transition, and economic growth infrastructure.

That does well if there is economic growth or domestic inflation?

Man… where do I sign up.

How exactly does Keppel Infrastructure Trust try to achieve this?

Of course, the devil is in the details.

How does Keppel Infrastructure Trust plan to achieve this?

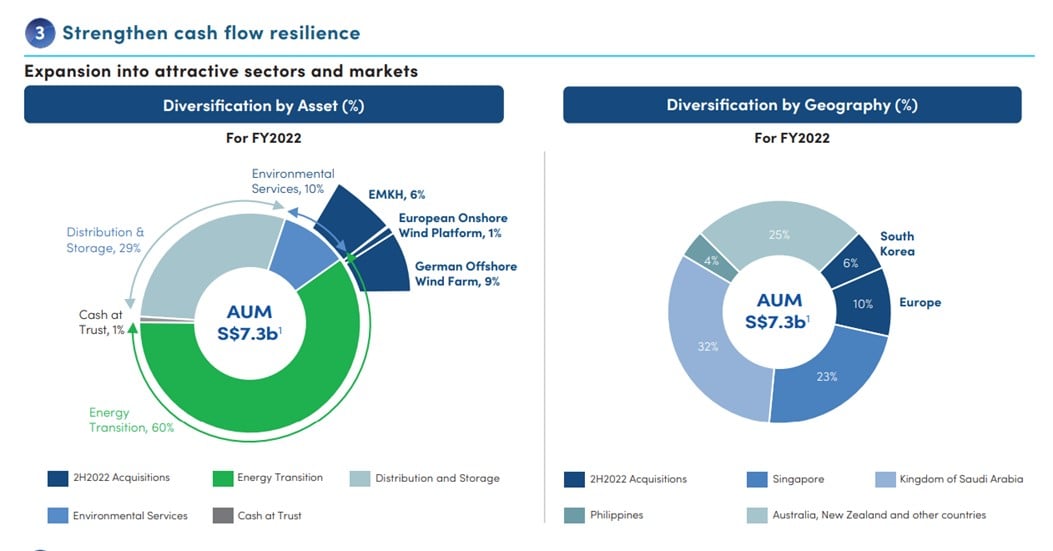

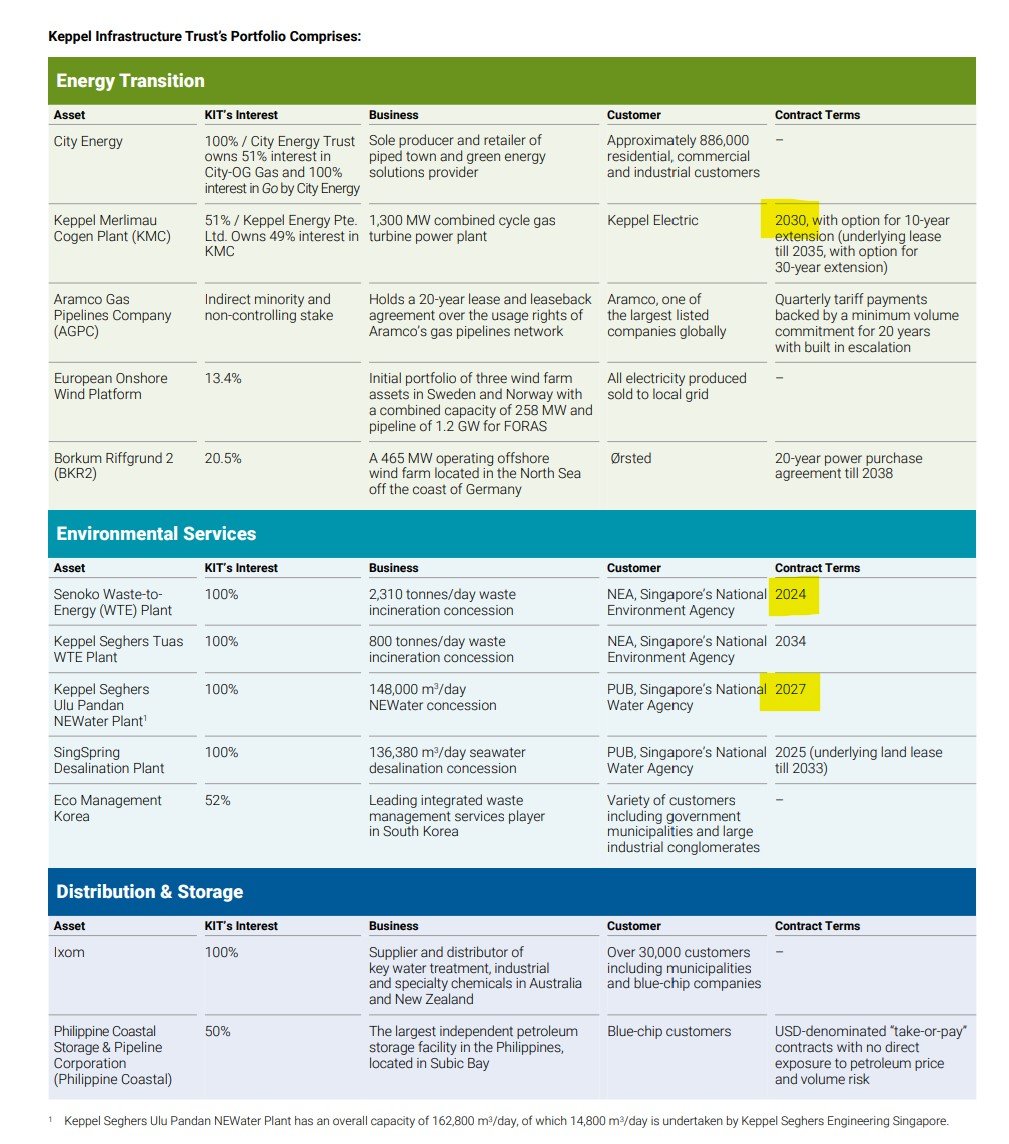

I’ve set out their high level asset break down below.

Broadly speaking, their exposure is:

- 23% Singapore

- 32% Saudi Arabia

- 25% Australia

- The rest scattered across Europe, Korea and Philippines.

Keppel Infrastructure Trust’s Singapore Portfolio

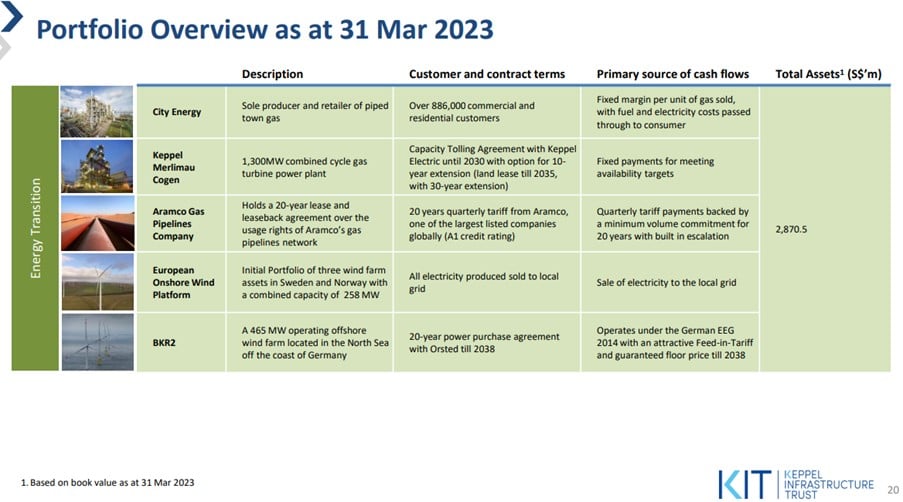

Their Singapore portfolio is a mix of energy and waste assets:

- City Energy which produces piped gas for Singapore

- Keppel Merlimau Cogen which is a gas turbine power plant that generates electricity for Singapore

- Senoko and Tuas waste incineration plants

- Ulu Pandan NEWater plant

- Singspring Desalination plant

So this is a very interesting mix of utilities, and you would expect very stable underlying cash flow from the Singapore assets.

Kind of like the infrastructure version of Netlink Trust, if you like.

Sure, you won’t see much growth, but on the flip side you won’t see much downside given that prices are locked in long term.

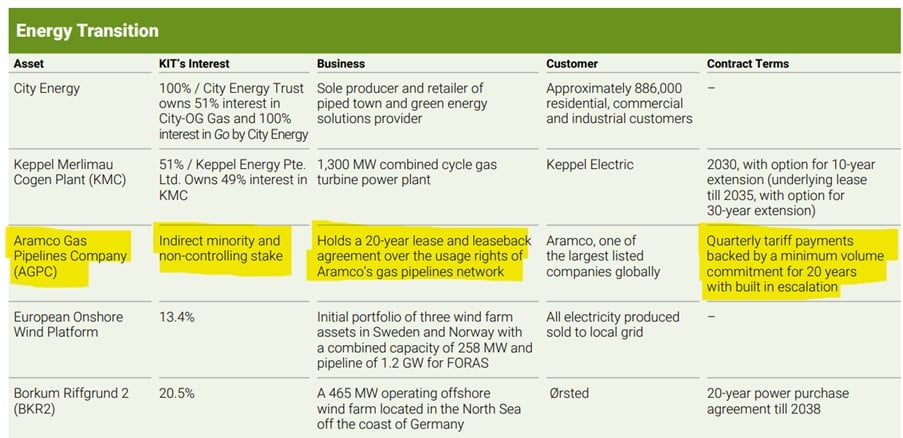

Keppel Infrastructure Trust’s Saudi Arabia Portfolio

The Saudi Arabian portfolio on the other hand, consists of a 20 year lease over the usage rights of Aramco’s gas pipeline network (Aramco is the Saudi Arabian Oil Group, one of the largest oil producers in the world).

This is only a minority equity ownership, so the operational control still rests with Saudi’s Aramco.

Given that this asset is 32% of Keppel Infrastructure Trust’s asset base, it does raise some questions on how stable this is going forward.

Especially with Keppel Infrastructure Trust as a Singapore company buying a minority and non-controlling stake in a Saudi pipeline – how much visibility, and how stable will this be going forward?

How extensive was the due diligence, and how much do we really know about this Saudi asset?

Payments are a “Quarterly tariff payments backed by a minimum volume commitment for 20 years with built in escalation”.

That’s not bad, because you have a minimum guarantee with built in escalation.

But it also means upside is capped because prices are locked in for 20 years.

Keppel Infrastructure Trust’s Australian Portfolio

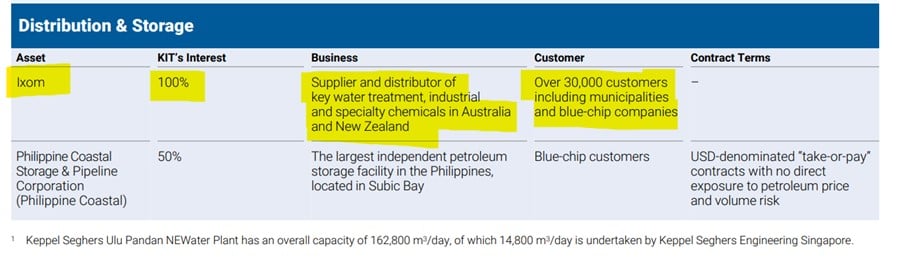

The Australian asset on the other hand, is Ixom, which is one of the key supplier and distributor of water treatment chemicals in Australia.

From the Annual Report:

In Australia, Ixom is the sole manufacturer of liquefied chlorine, as well as the leading provider of manufactured caustic soda. The group also operates one of the largest bulk and packaged chemical distribution businesses in Australia and New Zealand. The chemicals manufactured and distributed by Ixom are fundamental components used in a range of industries including the water treatment, dairy, agriculture, mining and construction sectors.

Unlike the other assets which are mostly locked into long term pricing, Ixom likely to be exposed to market pricing.

If the costs of these chemicals goes up (like it did the past year), Ixom will do very well.

If the costs of these chemicals goes down, then Ixom might not do so well.

On the bright side, they do look to have a close to monopoly status in Australia, which is good.

In fact management even conducted a strategic review and considered selling Ixom after receiving unsolicited offers.

You can see the response from management below, but the deal was eventually dropped when they couldn’t get the price they wanted for Ixom.

“Ixom is the crown jewel of KIT. It has performed well and generated strong returns for KIT. Why the strategic review of the business?

▪ Ixom is a creditable investment for KIT, which has been delivering attractive returns since 2019. Ixom’s EBITDA has grown from approximately $130 million in FY 2019 to approximately $199 million in FY 2022, demonstrating our ability to grow the company organically and inorganically.

▪ Through the pandemic, there has been a better appreciation of industrial assets. As a business that handles hazardous chemicals in Australia, Ixom continued to thrive during the pandemic, and we received unsolicited offers for the business, which triggered the strategic review.

▪ A strategic review of Ixom will allow us to optimise the KIT portfolio through crystalising Ixom’s intrinsic value, to redeploy capital for asset recycling and rotation. This is an active asset management approach to increase our capital to achieve further growth for KIT.”

Rest of Keppel Infrastructure Trust’s Assets

The rest of the assets are basically a Philippines coastal storage & pipeline, a European wind platform, and a waste management player in South Korea

Pretty much in line with the whole infrastructure play.

What worries me about Keppel Infrastructure Trust?

Now let’s talk a bit about what is not so great about Keppel Infrastructure Trust.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Some of the Concession Agreements for the Singapore Assets will end soon

The big one – is that the concession agreements for a few of the Singapore assets will end in 2024, 2027 and 2030 respectively.

These are:

- Senoko Waste to Energy Plant (2024)

- Ulu Pandan NEWater Plant (2027)

- Keppel Merlimau Cogen Plant (2030)

I know many investors out there who only buy REITs with freehold property, and if you’re one of those, this is going to worry you.

For what it’s worth, Keppel Infrastructure Trust’s management is well aware of the problem and is taking steps to solve it.

Here’s their response when queried on it (emphasis mine)

“Can you share more about the three acquisitions, and how they have helped to replace the cash flows from the concession assets that are expiring in the years to come?

▪ With the acquisitions last year, we have elongated the cashflow profile of the Trust through:

- a 20-year contract with Saudi Aramco,

- approximately 27 years of useful life from the renewable energy assets, and

- an evergreen business in South Korea

▪ In the Aramco Gas Pipelines Company investment, we received approximately $26.5 million in FY 2022 for two quarters of contributions. With an annual contribution of approximately $30-40 million on a conservative basis, this investment would add to the income stream of the Trust.

▪ The acquisitions of the European Onshore Wind Platform, the German Offshore Wind Farm, as well as EMKH are also DIPU-accretive on a standalone basis and will contribute to mitigating the concession shortfalls, such as the Senoko WTE plant that is expiring in 2024.

▪ Beyond replenishing cash flows, we are also actively working with regulators to extend the concessions and look to provide an update on the extension of the Senoko WTE plant sometime this year.”

So basically – their solution is to buy new assets to replace those cash flows, while concurrently negotiating with regulators to extend the concession agreements.

Given that their Sponsor is Keppel, I do think they have a good chance at a renewal, but of course there are no done deals until it is announced.

And even if an extension is granted, you won’t know the terms of the renewal ahead of time.

So this is a pretty big uncertainty to take note of with Keppel Infrastructure Trust.

There is exposure to market prices for chemicals and electricity

While the bulk of the portfolio (Singapore and Saudi) is locked into long term fixed price contracts.

The Australian Ixom and European Windfarms are subject to market pricing.

Ixom will be subject to market pricing on chemicals.

While the European Windfarms are subject to market pricing on wholesale electricity prices.

Here’s the disclosure from Keppel Infrastructure Trust on the risk:

“Volatility in wholesale electricity prices could have an adverse impact on the KIT Group’s profitability

Wholesale electricity prices in the countries where the acquired businesses operate may be volatile. Wholesale electricity prices are generally influenced by many factors that are difficult to predict, including weather and climate patterns, operating constraints of power stations, transmission and distribution infrastructure, generator competitive behaviour, power station and gas plant reliability, the type and amount of new build power stations, changes to the regulation of energy markets and actions of the market operator. Wholesale electricity prices can reach and have reached very high levels for short periods at times of peak demand or as a result of constraints on transmission or generation capacity. Unexpected movements and extreme short-term fluctuations in wholesale electricity prices which are not effectively mitigated through hedging arrangements could result in adverse impacts on the relevant acquired business’ financial performance, and in turn could have a material adverse effect on the KIT Group’s business, cash flows, financial condition, results of operations and cash flow.”

Last 12 months have been very inflationary – what about the next 12?

This matters because the past 12 months post-Ukraine war have been a very inflationary period.

So the price of chemicals and wholesale European electricity prices went up significantly.

Can this continue going forward?

Especially with the Feds on a crusade to stamp out inflation?

Big question mark.

We’re also going into a period of economic slowdown, which may hit the price of chemicals and electricity, affecting Keppel Infrastructure Trust’s revenue.

So there is a risk that a lot of these assets may look good because of higher prices the past 12 months, and you really don’t know where prices are going the next 12 months.

So there is cause for concern in the short term, if we get a deep recession.

What is the dividend yield of Keppel Infrastructure Trust?

I suppose the question then is whether this has been priced in.

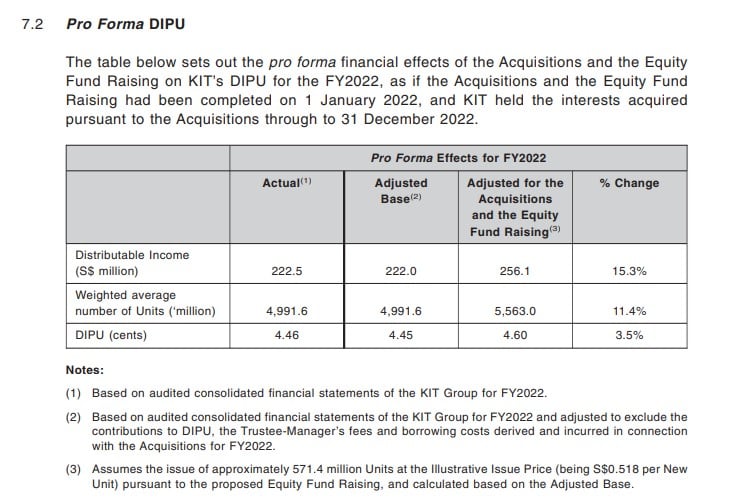

Their pro forma DIPU in the circular assumes the equity fund raise was done at 50.9 cents.

Whereas in reality the placement was done at 47.7 cents, and the rights issue at 46.7 cents.

So we need to adjust the DIPU numbers down quite a bit.

Let’s say conservatively we slash 20% from the pro-forma DIPU.

In that case you’ll be looking at about a 7.5% dividend yield at current price of $0.49.

These are very rough numbers of course, so I would say you are looking at about 7% – 8% dividend yields at this price.

If you assume a long term SGS 10 year yield of 3%, that’s about a 4%+ yield spread, which is decent.

So… Will I buy Keppel Infrastructure Trust?

Full disclosure that I do not have a position in Keppel Infrastructure Trust today.

I actually like the REIT enough that I queued a buy order all week, but unfortunately I got slightly too greedy with my price and it hasn’t filled yet.

Generally speaking I like Keppel Infrastructure Trust.

I think this decade has the potential to be a very inflationary one, and I like how Keppel Infrastructure Trust is positioned.

They have a good mix of assets with fixed income (Singapore + Saudi Arabia), with assets that have the potential for upside in an inflationary world (Ixom + Europe).

With Keppel as the Sponsor (18% stake), and Keppel making significant moves to go into the whole energy transition / green energy space, that also bodes well for Keppel Infrastructure Trust in the mid term.

The concession agreements expiring soon are definitely a problem, but it’s hard to say that it’s a black swan.

I mean the numbers are fully disclosed in the annual report, so you can’t really argue that you’re going to be blindsided by this.

What about Recession… and poor macro climate?

What does worry me is the macro climate.

At this point in the cycle, I think a US recession in the next 12 months is pretty much a done deal.

The only question now is how deep the recession is going to be.

Are we going to see a mild recession (negative real growth but positive nominal growth), or are we going to see a deep recession to stamp out inflation?

That will depend very much on policy makers reactions the next 9 months, and not so straightforward to predict.

If we do get a deep recession, the non-fixed prices portion of Keppel Infrastructure Trust like Ixom and the Electricity exposure will get hit.

It’s also possible we get a hard landing and all assets sell off, so that’s a risk to note.

But… Recession means interest rate cuts? Which is good for REITs?

I know there’s a school of thought out there that says a recession is the best thing that could happen for REITs.

It says that we are at peak interest rates today, and with interest rates going to be cut going forward.

This makes fixed income proxies like REITs a screaming buy at this point in the cycle.

My personal views – screaming buy is probably a bit extreme considering you don’t know the depth of the recession to come.

But I don’t deny that we are likely at peak interest rates here, to the point where I would be buying high quality fixed income and REITs, as long as I can get them at an attractive enough price.

As shared with Patreons, I myself picked up some REITs this week, as I see certain REITs trading at attractive enough valuations to warrant a buy (full list shared on Patreon).

It all goes back to asset allocation and risk-reward

Some of you have interpreted my previous macro articles as a call to sell everything and go to 100% cash, but that’s absolutely not what I’m saying.

All I’m saying is to be aware of the elevated risks in this climate, and to ensure you are running an asset allocation you are comfortable with for that uncertainty.

Some of you may be comfortable with 20% cash levels, while some others may want the peace of mind that comes with 50% cash levels.

There’s no right or wrong here – to each his own.

A 60 year old about to retire, and a 25 year old just starting their career – the cash levels you run will be completely different.

As long as you’re running an asset allocation you’re comfortable with, it’s perfectly fine to be buying stocks / REITs with attractive risk reward.

As shared with Patreons, I myself picked up some REITs this week, as I see certain REITs trading at attractive enough valuations to warrant a buy (full list shared on Patreon).

Closing Thoughts: When I like a position, I usually buy a small position first

Just to share a bit more about how I usually invest.

When I do the initial research on a new counter and I like what I see, I usually just go out there and buy a small position first.

The market moves very fast these days, so I don’t want to spend too much time thinking and miss the opportunity.

So I might just do that with Keppel Infrastructure Trust.

And over the next few weeks / months, I have more time to finish up my research and mull over what I bought.

If I like it I will add to the position.

Or if I discover that I am wrong (or there’s something I missed), I will sell the position.

So that’s how I tend to invest with new counters, and just because I may buy a small position in Keppel Infrastructure Trust doesn’t mean I won’t change my mind and sell it all 2 months later.

So do bear that in mind, and as always – Patreon members will get regular updates on my latest thinking, and if / when I decide to add or exit Keppel Infrastructure Trust.

This article was written on 25 May 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi boss, unless I’m mistaken, KIT is technically a Business Trust and not a REIT, so it is not compulsory to pay out 90% of its profit to enjoy tax benefit like a REIT, among other differences. Thought the headline needs to be correct.

Haha yup you’re exactly right. I wrote on this in the introductory paragraph as well – that it’s a BT not a REIT.

Might see if I can update the title or add another liner to make this absolutely clear to readers.

Great article & analysis Horse. Thanks! I might start a small position in KIT myself.

Haha just to add that I could change my mind any time! We do look to be heading into a recession after all, there is going to be a lot of uncertainty over the next 12 months.

Understand & agree. Hell, anyone who comes around boasting that they can accurately predict how the markets are gonna go in 2023 must either be a charlatan and/or insane. I like what I see in your analysis of KIT & will allocate accordingly to my risk appetite after I track & analyse KIT for myself in the next few months. 🙂

Dear FH

Nice summary

I have held KIT for a few years now

Had been a steady dividend payer with the unit price steady as well between 54-58c for several years

All was well until this recent expansion spree and rights issue

Although I subscribed for excess units and got allocated a few, courtesy the significant oversubscription, I am now ambivalent regarding KIT

As expected, this dilution has resulted in a significant price drop

It will need two years of preserved distributions for the “price” to March the pre rights issue

Am in no hurry to add and aerate down despite the high yield on paper!

As I have mentioned here several times, these ambitious expansion plans of SG TEITS and BT, end up causing more pain . Averaging down is just not a great strategy as it locks up your hard earned capital just like that

No easy solution but this “yield chasing” mindset causes suboptimal returns

My 2 cents

Regards

Garudadri

Yeah I get what you mean. If I were an existing unitholder I would not have liked what they did the past year.

That said, I can see why management did what they did though.

A business trust with no acquisitions, while good for the unitholders, is not so great for the sponsor / manager!