So I’ve been seeing a lot of articles recently about OCBC Bank breaking $20, and soaring to all time highs.

Now those with access to my personal portfolio (on FH Premium) will know.

That OCBC Bank is my largest Singapore bank position today.

I largely accumulated this position in the 15ish range in 2025.

With the recent rally, I’m up about 40-50% if you include dividends.

Which is frankly an astounding return for a bank stock in the span of less than 12 months.

When a stock goes on a monster rally like that.

I like to reanalyse the stock to see if there is anything I am missing.

And whether I should take profit, add to the position, or just continue holding.

Valuations of OCBC Bank compared with UOB and DBS Bank

Let’s start big picture with valuations.

I’ve tabulated the valuations of the 3 local banks below (prices as of Thursday, so slightly out of date after the Friday rally).

| Metric | DBS | OCBC | UOB |

| Share Price | S$58.89 | S$20.55 | S$37.62 |

| Price to Book (P/B) | 2.40x | 1.53x | 1.28x |

| ROE (Proj. FY26) | 16.9% | 13.4% | 12.5% |

| Est. Dividend (FY26) | S$3.30 (Total) | S$0.90 (Base) | S$1.75 (Base) |

| Fwd Div. Yield | ~5.6% (including capital return) | ~4.8% (including special dividend) | ~4.6% (assuming no special dividend)* |

*With special dividend, UOB can go to 6% dividend yield.

DBS Bank

You can see how DBS is the most “expensive” at 2.4x book.

But also supported by best in class 16.9% Return on Equity.

DBS because of the aggressive capital return, also pays the highest dividend yield today at 5.6%.

UOB Bank

UOB on the other hand, is the “cheapest” at 1.28x book value.

Largely because of their recent loan loss provisions, and market perception over UOB being the “weakest bank” (as supported by their lowest ROE).

Note that even though UOB is cheap on a Price/Book basis, there is a lot of uncertainty over the dividend yield because we don’t know if management will continue to pay the special dividend.

Yes, and you’re looking at a 6% dividend yield.

No, and it drops to 4.6% – the lowest of the 3 banks.

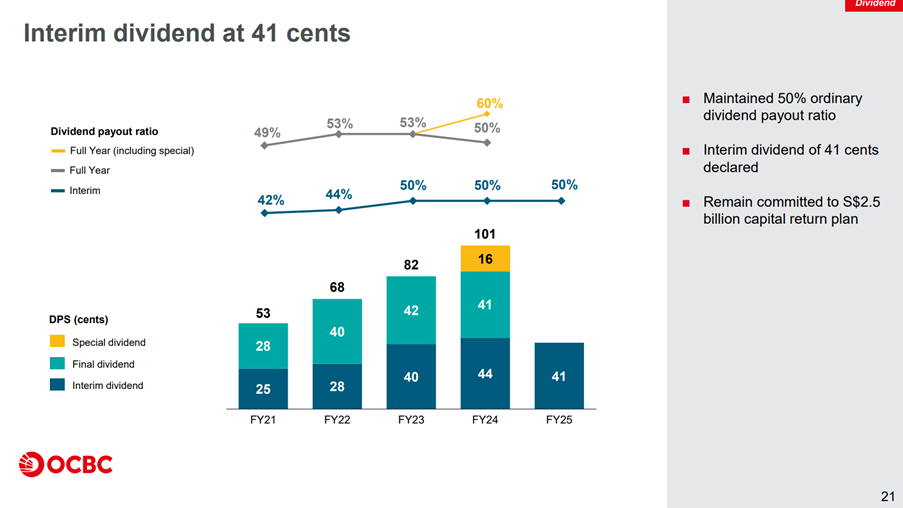

4.8% Dividend yield of OCBC Bank (including special dividend)

OCBC on the other hand, sits in the middle of the pack.

Not quite DBS’s record breaking 17% ROE.

Not quite as bad at UOB with its loan loss provisions.

1.53x Price to Book, in the middle of DBS and UOB.

If you assume the special dividend continues, you’re looking at about a 4.8% dividend yield.

That’s okay, but frankly not amazing because you can get a higher dividend yield with a REIT, or a dividend stock.

So if you buy the stock today, you do need to care about the capital return (or loss) which will determine a good chunk of your total returns.

So… why does the share price of the 3 Singapore banks keep going up?

And on that note.

The price performance of the 3 local banks are unbelievable.

The charts are as beautiful as it gets from a technical analysis point of view.

Both OCBC and DBS are trending up very strongly.

Even UOB the lagged has broken the recent downtrend in a very strong way.

Just look at the 2 day performance for UOB this week.

Why are the Singapore bank stocks doing so well?

For reference, here’s the chart for JP Morgan, the biggest bank in US.

And JP Morgan is actually down 6% year to date – in stark contrast to the Singapore banks.

Why is the price performance for the local banks so strong, especially compared to global banks?

For what it’s worth, I don’t have any easy answers to this question.

What could make sense is that the Singapore banks like UOB and OCBC are still cheap at low 1.x book value.

Whereas DBS and JP Morgan both trade well in excess of 2x book value.

So one theory is that this is not a big macro driven move.

But a more fundamental value driven kind of move, where investors rotate capital into cheaper stocks.

Which is why you see OCBC and UOB catch up so strongly, relative to DBS and JP Morgan.

But hey frankly I’m just stabbing in the dark here.

If you have any better theories, love to hear them below.

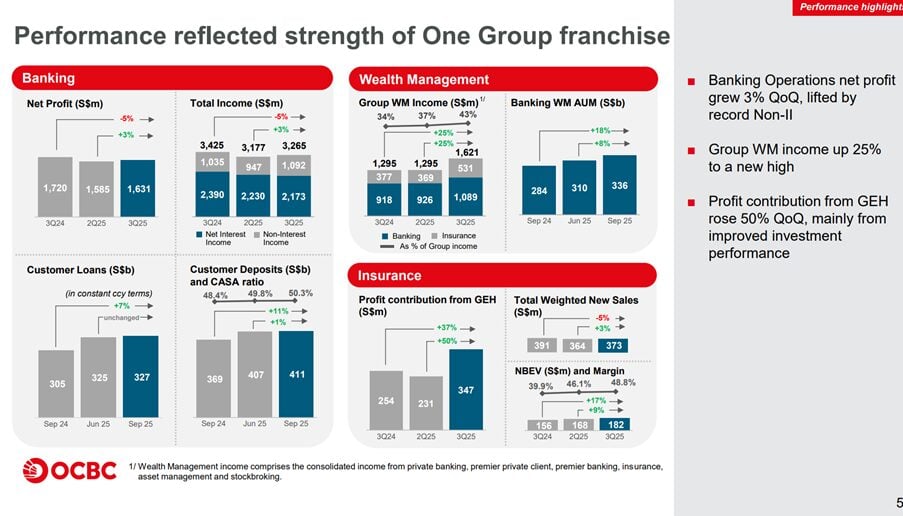

Analysing the business performance of OCBC Bank

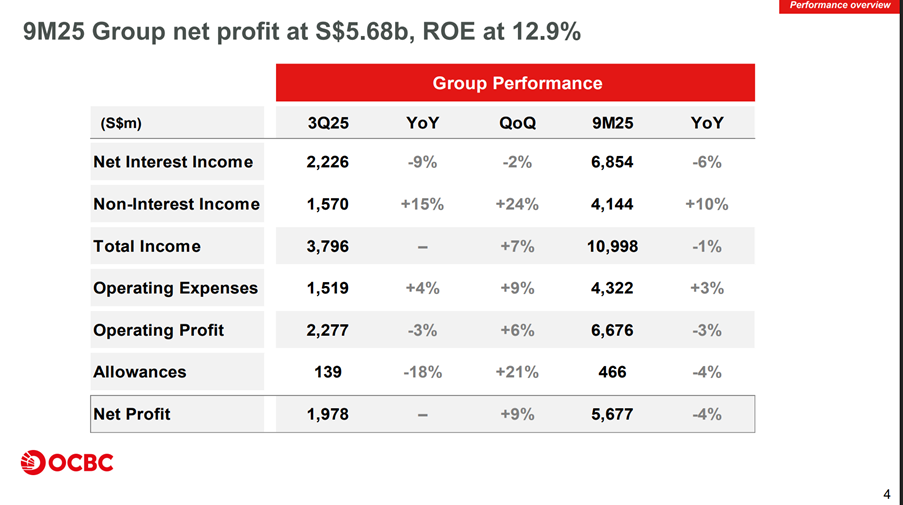

Taking a look at the latest financial results.

Net Interest Income is down as you would expect given we are in a declining interest rate environment.

However that decline is largely offset by the Non-Interest income, which is showing very strong growth.

What is this non-interest income?

Largely Wealth Management and Insurance as it turns out。

Wealth Management looks to be incredibly hot of late – not just for OCBC but for all 3 local banks.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Evaluating risk reward of OCBC Bank assuming a 3 year holding period?

I asked both Gemini 3 Pro and ChatGPT 5.2 Thinking to crunch the scenario analysis on the bull and bear case – assuming a 3 year holding period.

Here’s the analysis from Gemini, indicating:

- Bull Case – 37% upside

- Base Case – 18% upside (largely from dividends)

- Bear Case – 5% downside (cushioned by dividends)

| Scenario | Prob. | Key Drivers | Exit P/B | Price Target | Exp. Total Return* |

| Bull Case | 20% | “Wealth Haven Boom” Soft landing achieved. Wealth inflows accelerate. ROE sustains >13%. Fed rates settle >3.5%. | 1.60x | S$25.00 | +37% (~11% CAGR) |

| Base Case | 50% | “Mean Reversion” Rates normalise. NIM compresses. Growth slows. Valuation fades from peak euphoria to a sustainable premium. | 1.35x | S$21.00 | +18% (~5.8% CAGR) |

| Bear Case | 30% | “Hard Landing” Recessionary cuts (Fed <2.5%). Asset quality issues emerge. Market de-rates banks to historical mean/lows. | 1.05x | S$16.40 | -5% (Negative CAGR) |

GPT on the other hand:

- Bull Case – 36% upside

- Base Case – 17% upside (largely from dividends)

- Bear Case – 23% downside (cushioned by dividends)

| Case | Prob. | Exit P/B | Divs (3yr, S$) | Total Return (3yr) | CAGR |

| Bull | 25% | 1.60x | 3.25 | +36.0% | +10.8% |

| Base | 55% | 1.45x | 2.91 | +17.0% | +5.4% |

| Bear | 20% | 1.00x | 2.40 | -23.3% | -8.5% |

My thoughts? Is this risk-reward for OCBC Bank attractive?

So ChatGPT and Gemini largely agree on the base and bull case.

But ChatGPT projects more downside in the bear case.

I’m inclined to agree with ChatGPT on this one.

In a true bear case recession scenario, you really don’t want to underestimate the downside risk for the banks.

If so, is a return profile like this attractive?

| Case | Prob. | Exit P/B | Divs (3yr, S$) | Total Return (3yr) | CAGR |

| Bull | 25% | 1.60x | 3.25 | +36.0% | +10.8% |

| Base | 55% | 1.45x | 2.91 | +17.0% | +5.4% |

| Bear | 20% | 1.00x | 2.40 | -23.3% | -8.5% |

I suppose you could argue yes, as long as you know that this is not a growth stock with asymmetric risk-reward.

You don’t buy OCBC Bank expecting the stock to triple in the next 2 years, or anything ridiculous like that.

But if you’re looking for a steady compounder kind play, OCBC can fit the bill, as long as you are aware of the downside risk (as with all banks).

Will I buy more OCBC Bank stock at 4.8% dividend yield?

As shared above, OCBC Bank is my largest bank stock today.

With the analysis above, I don’t see an immediate need to sell the stock.

Especially not when the chart is showing such a powerful uptrend.

When a stock has unbelievable momentum like that, best to let it play out until the trend starts to change.

But will I buy more of OCBC bank today?

Now that’s a lot more tricky.

Given this is already my biggest bank stock, and after such a powerful rally.

It makes me somewhat more reluctant to add to my position at these prices.

Is UOB Bank better “value” today?

On the other hand, I shared in a recent article that instead of adding to OCBC Bank, I have been adding to UOB Bank.

For the simple reason that:

- Starting valuations are cheaper

- Technical analysis is showing a potential bottom at $33 (and break above the 200 day moving average)

- The recent loan loss provision *may* indicate a short term bottom for now

| Metric | DBS | OCBC | UOB |

| Share Price | S$58.89 | S$20.55 | S$37.62 |

| Price to Book (P/B) | 2.40x | 1.53x | 1.28x |

| ROE (Proj. FY26) | 16.9% | 13.4% | 12.5% |

| Est. Dividend (FY26) | S$3.30 (Total) | S$0.90 (Base) | S$1.75 (Base) |

| Fwd Div. Yield | ~5.6% (including capital return) | ~4.8% (including special dividend) | ~4.6% (assuming no special dividend)* |

So far at least, that decision has been paying off in spades, because look at that unbelievable price performance from UOB Bank this week.

I suppose the next question is whether I would add to UOB Bank.

I was actually planning to in the 34-36 range, but then we had a monster 2 day rally in the stock that went parabolic.

With this it probably makes sense to watch a bit more of the price action before making any decision on UOB Bank.

And also with the recent rally, the valuation gap between UOB and OCBC Bank has narrowed significantly.

So both UOB and OCBC Bank probably look a lot more equal today.

US Bank stocks have not been doing well in 2026? Foreshadowing for Singapore bank stocks?

It’s also interesting to note that US bank stocks have not been doing well in 2026 at all.

Year to date price performance for the S&P500 below.

You can see how the financial segment is all red.

That being said, yes I get that the US banking sector and Singapore banking sector have different industry dynamics, and it is possible for one to underperform while the other outperforms.

But still – a cautionary note to never forget risk management, and always watch position sizing carefully.

From the chart above you can see how Semiconductors, Industrial, Commodities and Precious Metals have all been doing very well.

And that’s where I’ve been deploying some of my new funds of late – and you can see exact portfolio changes on FH Premium.

Closing Thoughts

I suppose to sum up, I hold positions in OCBC and UOB.

With the recent rally I’m still holding positions, but not making any decision on adding for now.

I’ll let price action play out a bit more before deciding.

In the meantime, my semiconductor, industrial, commodities and precious metals have been doing well, and all show very strong momentum.

And I’ve also been adding to positions in crypto and Biotech, since I see comparative value there for longer term positions.

There’s just a lot of opportunities out there at the moment, and you can see my exact portfolio changes updated on FH Premium.

Love to hear what you think though!

Would you buy more OCBC bank stock at these prices?

If you enjoy articles like this, do support Financial Horse on FH Premium and get access to premium articles like this, including my stock watch and investment portfolio.

Are you able to find out how much of SRS funds are deployed into the banks at the start of the year ? Does it have an impact of their shares prices ?

That’s an interesting question. My gut feel is that with this kind of move, it’s institutional money and not retail money. But interesting point.

Sg bank stocks are the new crypto memes

Crypto meme being the new sg value stocks

Time is a flat circle

And gold is the new Bitcoin, silver is the new Ethereum/Solana. 😉

Hi FH,

https://sgwealthbuilder.com/2025/12/31/ocbc-share-price-to-hit-30/

OCBC’s swashbuckling exploits in Great Eastern proved to be shrewd as it comes at a time when banks are facing pressure from the interest rate cuts. For the 3rd quarter financial result, OCBC’s net interest margin plunged 34 basis points year-on-year, causing net interest income to drop 9% to $2.23 billion. However, the 38% increase in insurance income from Great Eastern helped to cushion the impact. In the end, net profit for 3rd quarter remained unchanged year-on-year at $1.98 billion, supported by higher non-interest income and lower allowances.

https://sgwealthbuilder.com/2025/12/31/ocbc-share-price-to-hit-30/

Good point Gerald – I agree the Great Eastern buy was a great move for OCBC. I liked it a lot when it was announced (mainly because of the price), but the same reasons why I like it as a OCBC shareholders, is why GE shareholders don’t like it.