If you’ve been following the news recently.

You may have seen the headlines about a 68% fall in Singapore Airlines’ half-year profits:

That said, all I hear about from fellow Singaporeans is about how expensive SQ tickets are, and how they must be making a ton of profit.

If so, this must be a pretty good business no?

At current prices, Singapore Airlines stock pays a 6.2% trailing dividend yield.

Is Singapore Airlines stock a good buy?

Charts for Singapore Airlines stock

Let’s start with the charts.

Here is the weekly chart for Singapore Airlines.

You can see how the stock had a huge recovery coming out of COVID.

After bottoming at $3.5 in October 2020.

The stock soared 138% over the next 1.5 years.

Peaking at $8 in mid 2023.

Since then however, the stock has just traded sideways.

This is better illustrated on the daily chart.

The stock has basically gone nowhere for the past 2.5 years:

Singapore Airlines half-year profit falls 68%

And on to the headline: Singapore Airlines’ half-year profit falls 68%

Here’s the reporting from CNA:

Singapore Airlines posted a nearly 68 per cent drop in half-year net profit on Thursday (Nov 13), hurt by intensifying competition, lower interest income and losses from associate airline Air India.

…

The company’s interest income was also dented by S$103 million due to smaller cash balances and interest rate cuts, while share of results from associated companies plunged S$417 million, largely because of Air India’s losses.

Air India’s results were not part of the group’s earnings a year earlier. Singapore Airlines began accounting for the Indian carrier’s performance from December 2024, after completing the integration of its joint venture Vistara into Air India.

Singapore Airlines holds a 25.1 per cent stake in the Indian carrier, in what it called a part of its “long-term multi-hub strategy” to have a stake in “one of the world’s largest and fastest-growing aviation markets”.

“Despite the ongoing challenges, the SIA Group remains committed to working with its partner Tata Sons to support Air India’s comprehensive multi-year transformation programme.”

Singapore Airlines earnings are okay-ish

For what it’s worth.

Singapore Airlines’ core business – being flying people around under the SQ / Scoot name.

Is actually doing okay.

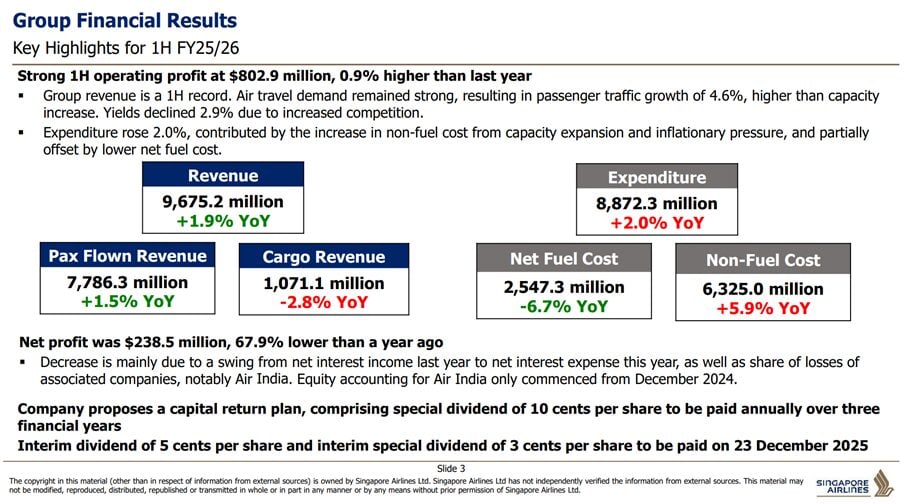

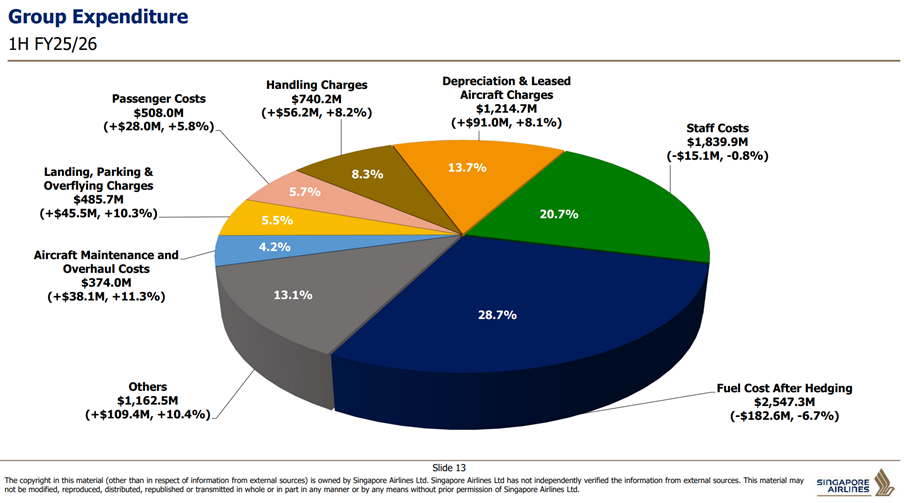

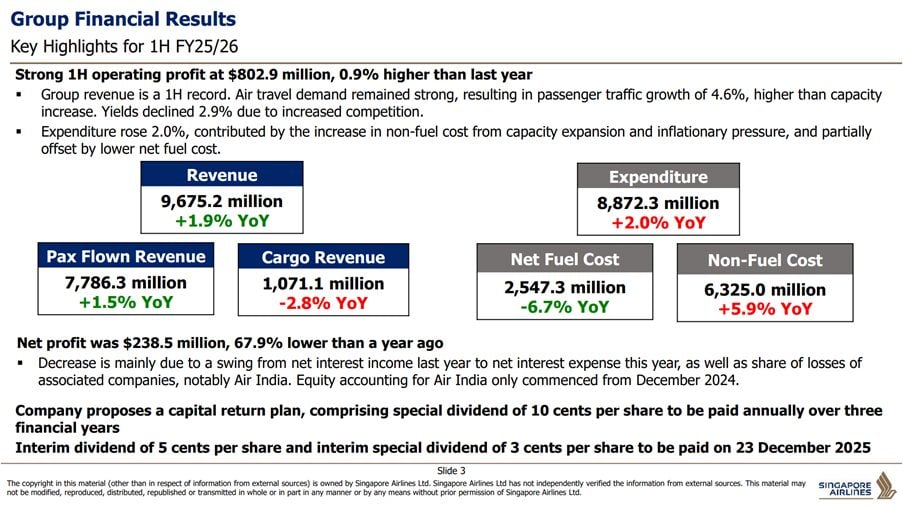

Revenue is up 1.9%.

And yes if you want to nitpick you will say that costs being up 2.0% despite a 6.7% drop in fuel costs doesn’t look good.

But look through at what’s driving the underlying costs, and it’s basically just inflation in general hitting ground handling charges, aircraft costs, maintenance costs etc:

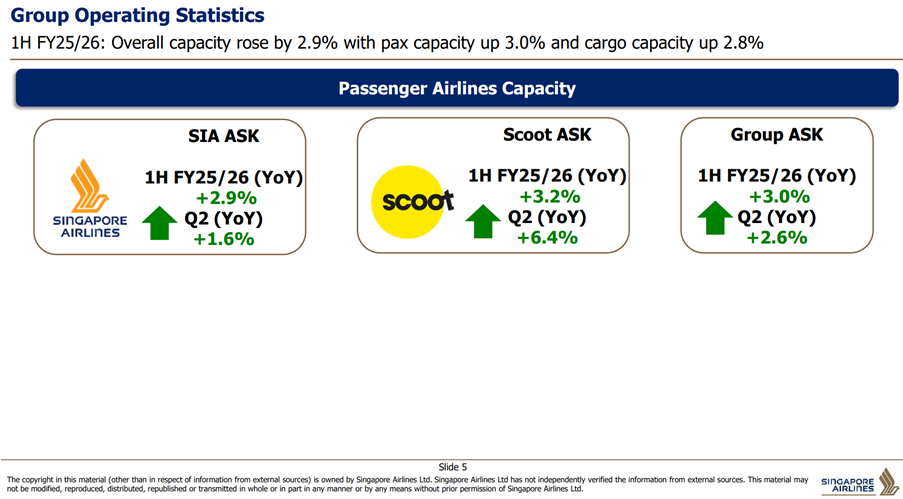

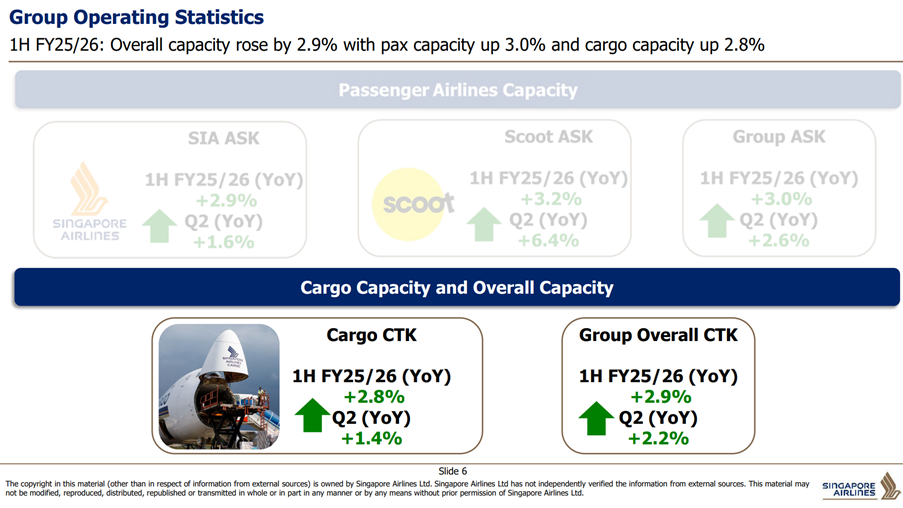

And the operating statistics are okay too.

Not fantastic, but improving year on year:

It’s the Air India that’s dragging profits down

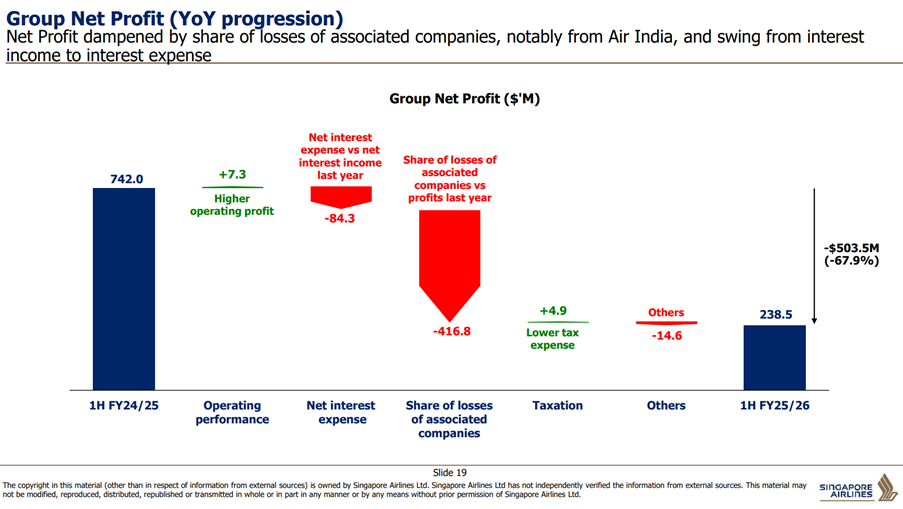

The real problem that resulted in the huge drop in profits – is SQ’s 25.1% stake in Air India.

This was what Singapore Airlines had to say in the recent earnings:

Visualised below, you can see how the big chunk of losses vs last year came from the Air India losses:

Singapore Airlines holds 25.1% of Air India – Summary of the whole saga

Let me summarise the whole Air India saga as simply as I can.

A long time ago, SIA held 49% in the Indian airline Vistara, with the other 51% held by Indian conglomerate Tata.

Air travel in India is a brutal business dominated by price cutting.

So in Nov 2022, Tata and SIA agreed to merge Vistara into Air India (also controlled by Tata), creating a single full-service carrier under the Air India brand.

Under the deal, SIA would:

- Roll its 49% Vistara stake into the merged entity; and

- Inject ₹20.585bn (approx. S$322m) in cash.

- In exchange, SIA would own 25.1% of the enlarged Air India.

- Tata would be 74.9% owner and controlling shareholder of the enlarged Air India.

Accounting treatment wise, Singapore airlines would treat Air India as an equity-accounted associate, recognising its share of Air India’s profits/losses in SIA’s P&L.

In other words, it would recognize its share of Air India’s losses, and boy those losses were big.

Hence the 68% drop in net profits.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Why is Air India struggling so badly?

Okay I know what you’re going to ask.

Why is Air India struggling so badly.

The short answer is that Air India was not a fantastic airline and has a lot of legacy, structural issues that needed to be solved.

Throw in a brutally competitive aviation market with price cuts, and it makes it incredibly tough to turn a profit.

The slightly longer answer, is per below:

Air India is struggling because it’s trying to fix decades of structural problems at the same time as it’s funding an extremely ambitious turnaround in a brutal market.

For years under state ownership, Air India piled up huge losses and debt. The merger with Indian Airlines never really delivered synergies, the airline stayed overstaffed and bureaucratic, and it under-invested in product, maintenance, and systems. Service quality, on-time performance, and brand perception deteriorated, so the airline lost pricing power just as costs stayed high (fuel, airport charges, interest).

When Tata took over, they didn’t get a clean, profitable carrier – they got a heavily indebted, under-invested airline that needed almost everything rebuilt. The Vihaan.AI transformation plan involves massive capex: very large aircraft orders, cabin refurbishments, new lounges, IT overhauls, and restructuring of staff and processes. On top of that, Air India is integrating multiple entities (full-service Vistara, low-cost Air India Express and AIX Connect), which brings one-off integration and restructuring costs, plus operational disruption.

All this is happening in one of the toughest aviation markets in the world. India’s domestic space is dominated by low-cost competitors, especially IndiGo, which keeps fares extremely competitive. Taxes on fuel and airport charges are high, and infrastructure constraints add operational complexity. That makes it hard for Air India to raise fares enough to cover its elevated cost base while it is mid-turnaround.

Then 2025’s major crash added a safety and reputational crisis on top of the financial and operational challenges. A serious accident means regulatory scrutiny, higher safety and insurance costs, and potential damage to consumer confidence right when Air India is trying to rebuild trust.

The result: revenue is growing, but losses are still large and funded by repeated shareholder injections from Tata and Singapore Airlines, with profitability pushed further into the future.

Strategic rationale (from SIA’s perspective)

And now you will ask.

If Indian air travel is so bad.

Why invest?

This is the strategic rationale per Singapore Airlines:

Broadly, SIA has framed the Air India stake as part of a long-term “multi-hub” strategy:

- Access to India growth: Air India is being positioned (large widebody orders, rebrand, network expansion) as a major global carrier in a structurally high-growth market; SIA gets a direct equity stake in that upside without needing majority control.

- Network and product: A stronger Air India group (full-service + low-cost subsidiaries) complements SIA’s Changi hub with more feed, connectivity and co-operation on India-linked traffic.

- Financial trade-off:

- Short term: SIA’s stake has dragged group profit lower because Air India is still loss-making and undergoing heavy capex + restructuring.

- Long term: SIA management has repeatedly said they remain committed to Air India’s turnaround and see value in the recap plan and future profitability.

Or in plain English.

Short term pain during the turnaround, but long term gain via exposure to a huge Indian domestic market.

Assuming Air India will eventually turn around of course, which is itself a big if.

In the meantime, Air India is bleeding cash and will require huge financing

Short term though, Air India is bleeding cash.

And will require a ton of capital from its shareholders:

Singapore Airlines (SIA) has contributed nearly S$1 billion to Air India, with approximately S$322.1 million in equity investment and over S$666.8 million in additional capital injections as of March 2025.

SIA has committed to providing up to S$880 million in additional funding, a total investment of up to approximately $1.24 billion.

Air India recently requested another S$1.5 billion in funding, with SIA’s 25.1% share being around S$376.5 million, which would increase SIA’s total investment to nearly S$1.4 billion if they agree to the request.

Management has stated they are committed to Air India, and that means a lot of shareholder financing in the short term.

Sure it may pay off long term, but that won’t be pretty in the short term.

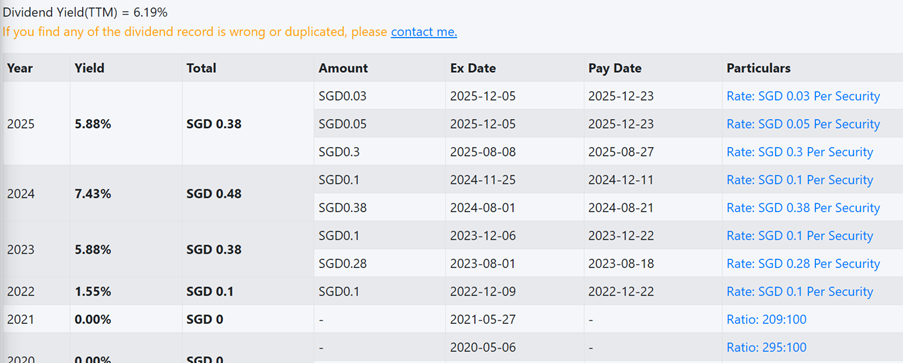

Dividend Yield of Singapore Airlines stock

The trailing dividend yield of Singapore Airlines is 6.19%

However that’s trailing dividend yield.

With the drop in profits, what does the forward dividend yield look like?

Management has committed to a 10 cents special dividend per year for the next 3 years.

Working out some rough numbers:

1H:

- Ordinary: S$0.05 (already declared)

- Special: S$0.03 (already declared)

2H:

- Ordinary: ~S$0.20

- Special: S$0.07 (subject to AGM approval)

Gets us approximately a 35 cents dividend.

On $6.46, that is a forward dividend yield of 5.4%.

It’s okay, but nothing to shout about.

Valuations of Singapore Airlines

Is Singapore Airlines cheap on a valuations basis?

I summarized the valuations of Singapore Airlines against other big airlines below:

| Airline | Region | P/E (ttm) | EV/EBITDA (ttm) | P/B | Dividend yield |

| Singapore Airlines | Asia (SG) | ~9x | ~5.5–6x | ~1.2 – 1.3x | ~5.5–6.0% |

| Cathay Pacific | Asia (HK) | ~9x | ~5–5.5x | ~1.4x | ~5.5–6% |

| Qantas | Asia-Pacific (AU) | ~9x | ~4.5x | ~0.7x | ~5.4% |

| ANA Holdings | Asia (JP) | ~11x | ~4.5x | ~1.3x | ~2.0% |

| Delta Air Lines | US | ~8x | ~7–8x | ~2.0x | ~1.2–1.3% |

| American Airlines | US | ~13–14x | n/a | ~2.5x | 0% |

| United Airlines | US | ~9x | ~6x | ~2.5–2.6x | 0% |

Generally speaking, Singapore Airlines trades at:

- P/E: ~8–9x

- EV/EBITDA: ~6x

- P/B: ~1.2–1.3x

- Dividend yield: ~5–6% (forward ~5.4%)

- FCF yield: high single / low double digits (volatile)

Compared to the other airlines, I would say SQ is reasonably valued:

- Not priced like a “growth stock” – multiples are mid-single-digit on cashflow and high-single-digit on earnings.

- Trading only modestly above book value despite a stronger-than-average franchise and national-carrier status.

- Offering a decent cash return today, but with clear cyclicality risk (competition, yields, fuel) and Air India drag

That said, it offers one of the highest dividend yields in the group, matched only by Cathay and Qantas.

And relative to both, I would say Singapore Airlines is probably a much stronger brand name and company.

So valuations wise, I think Singapore Airlines is reasonably valued.

Will I buy Singapore Airlines stock?

Coming back to the million dollar question.

Will I buy Singapore Airlines stock?

Valuations are reasonable, and arguably on the cheap side compared to other airlines.

That said the chart is terrible – as the stock is clearly rangebound.

And it’s hard to see any catalysts on the horizon that would spark a jump in the share price.

Meanwhile Air India is bleeding cash, and will require a lot of cash infusions in the near term.

Maybe that pays off long term, maybe it doesn’t.

Who knows.

What we do know, is that short term it’s going to be a huge drag on Singapore Airlines profits and cashflow.

Putting all of the above together.

I find it hard to see why I would want to take a position in Singapore airlines.

At least until I see a change in the Air India situation, a breakout in the chart, or another catalyst on the horizon.

Meanwhile with the sell-off in Bitcoin and US tech, I’m seeing a lot of great places elsewhere that I don’t mind deploying capital (see my full portfolio and stock watch on FH Premium).

And that’s probably where I will deploy capital instead.

Love to hear what you think though!

This post is written on 21 Nov and will not be updated going forward.

For the latest market commentary, check out FH Premium.

SQ need to focus on their core business. Just like SingTel, their foreign adventures don’t seem to work out too well. Their ticket prices currently tend to be a bit higher than Emirates, and some aspects of their service are not up to the same level. I’m still flying SQ regularly, but on some routes (to Europe) I’m no longer sure the premium for a direct flight is still worth it.