In our recent article on How to Buy Gold in Singapore, we covered the main ways Singapore investors can get gold exposure — from physical bars to ETFs to bank savings accounts.

And in that article, we said there was only one gold ETF listed on the SGX — the SPDR Gold Shares.

Well, that’s about to change.

On 26 March 2026, Singapore will get its second gold ETF on the SGX — the LionGlobal Singapore Physical Gold ETF.

And this one has some features that are genuinely different from the SPDR product.

The gold is vaulted right here in Singapore. It’s fully insured. And the entry price is just USD 5.00 per unit.

So the question for investors is — how does this new ETF fit alongside all the other gold buying options we covered in Part 1?

Let’s break it down.

But first — the big picture on gold as an investment

Before we get into the product comparison, I want to step back and share some big picture thoughts on gold as an asset class.

Because the question isn’t just which gold product to buy.

The question is — should you be buying gold at all, at these prices?

What’s driving the gold rally?

Gold is up 75% in the past year. That’s an extraordinary move for what’s supposed to be a boring, defensive asset.

So what’s behind it?

I see 3 big structural drivers:

1. Central bank buying has gone parabolic. This is the single most important driver. Central banks bought roughly 800–900 tonnes of gold in 2025 — and consensus forecasts project another 800+ tonnes in 2026. That’s equivalent to about 26% of annual mine supply being soaked up by central banks alone. China, India, Poland, Turkey — they’re all diversifying reserves away from the US dollar. For the first time since 1996, gold now accounts for a larger share of central bank reserves than US Treasuries.

2. Money printing and fiscal deficits. We’ve been saying this for a while now — gold is a hedge against money printing. The US is running massive fiscal deficits under Trump, the Federal Reserve is keeping monetary policy easy, and there’s no sign of fiscal discipline on the horizon. Gold thrives in this environment because it’s nobody’s liability. You can’t print more of it.

3. Geopolitical risk premium. The US-Iran conflict, US-China tensions, tariff wars, the weaponization of the financial system — all of this is driving demand for gold as the ultimate neutral, sanction-proof asset. When Russia’s foreign reserves were frozen in 2022, every central bank in the world took notice. Gold can’t be frozen or sanctioned.

What are the investment banks saying?

For what it’s worth, the sell-side is overwhelmingly bullish on gold:

- JP Morgan: US$6,300 per ounce by end 2026

- Wells Fargo: US$6,100–6,300 by end 2026

- UBS: US$6,200 by September 2026 (upside scenario to US$7,200)

- Goldman Sachs: US$5,400 end-2026 target

- BNP Paribas: US$6,000 per ounce by year end

Now, I would take these forecasts with a pinch of salt. Investment banks are frequently criticized for inaccurately predicting commodity prices.

But the point is that the consensus view is bullish, and the structural drivers (central bank buying, fiscal deficits, geopolitical risk) are not going away anytime soon.

The bear case — what could go wrong?

I always think it’s important to think about what could go wrong. Especially when consensus is so overwhelmingly bullish.

1. Gold pays no income. Unlike stocks (dividends) or bonds (coupons), gold gives you exactly zero yield. At 5%+ risk-free rates, you’re giving up meaningful income to hold gold. If rates stay higher for longer, or go even higher, that’s a real opportunity cost.

2. The price has already moved a lot. Gold at US$5,200 is priced for a world of perpetual fiscal deficits, geopolitical instability, and central bank buying. If any of those drivers slow down — say Trump negotiates a deal with Iran, or central banks pull back on buying — you could easily see a 10–20% correction from these levels.

3. The US dollar could strengthen. A stronger dollar is generally bad for gold. If the US economy outperforms, or the Fed turns hawkish, that could create headwinds.

4. Demand destruction from high prices. Gold jewellery demand — which accounts for about 40% of gold consumption — is already showing signs of weakness. At some point, high prices choke off demand.

My macro view on gold today?

My simple view.

I think the structural case for gold is strong. Central bank buying is a secular trend, not a cyclical one. Fiscal deficits aren’t going away. And geopolitical risk is, if anything, increasing.

But at US$5,200, I would not go all-in.

The easy money has been made. Gold is no longer cheap by any measure.

The risk-reward at these prices is not the same as buying gold at US$1,800 or US$2,400. You’re buying after a 75% run-up.

So what’s the smart play?

1. Don’t try to time the top. Nobody knows if gold goes to US$6,000 or corrects to US$4,000 first. If you have conviction on the long-term thesis, start building a position. But do it gradually.

2. Dollar-cost average. This is not the time for a lump sum buy. Spread your purchases over 6–12 months. If gold corrects 10–20%, you’ll be glad you didn’t go all-in at the top. If gold keeps rallying, you’re still building exposure.

3. Size it appropriately. Most advisors recommend 5–10% of a diversified portfolio in gold. I think that’s sensible. Gold is insurance — it’s not meant to be your entire portfolio. Don’t let FOMO after a 75% rally lead you to over-allocate.

4. Think of gold as insurance, not a trade. Gold is the asset you own that you hope you never need. It’s insurance against tail risks — hyperinflation, currency crises, geopolitical shocks, financial system breakdowns. If none of those happen, your stocks and REITs will do fine. But if they do happen, you’ll be very glad you own some gold.

That’s how I’m thinking about gold in the current environment.

Now with that macro context in mind — let’s talk about the new LionGlobal ETF and how it fits into the picture.

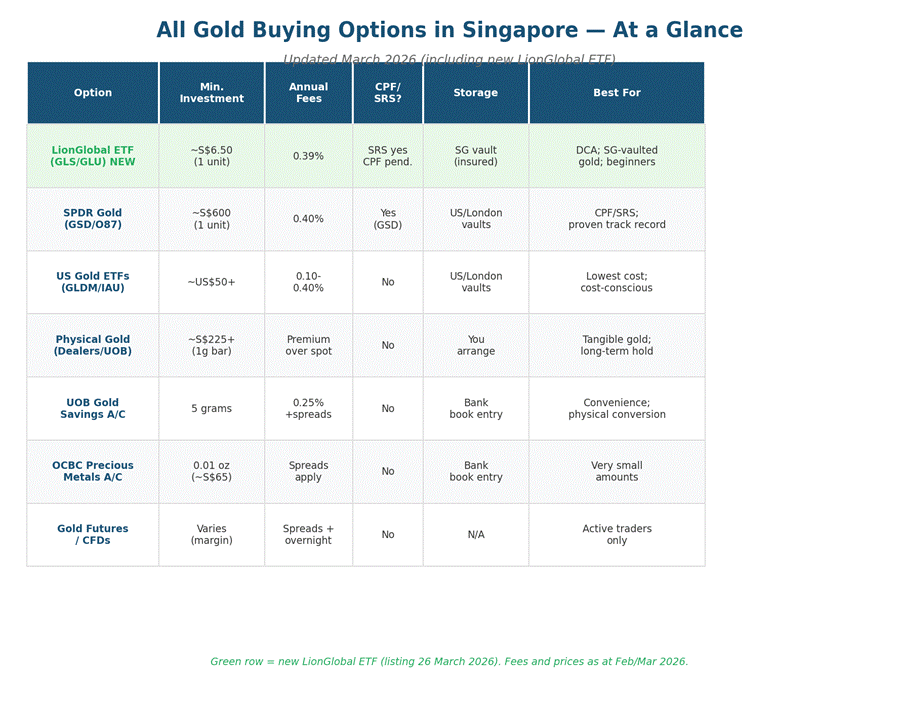

Quick recap: All the ways to buy gold in Singapore

If you haven’t read Part 1 of this guide, here’s a quick recap of all the gold buying options available to Singapore investors — now updated to include the new LionGlobal ETF.

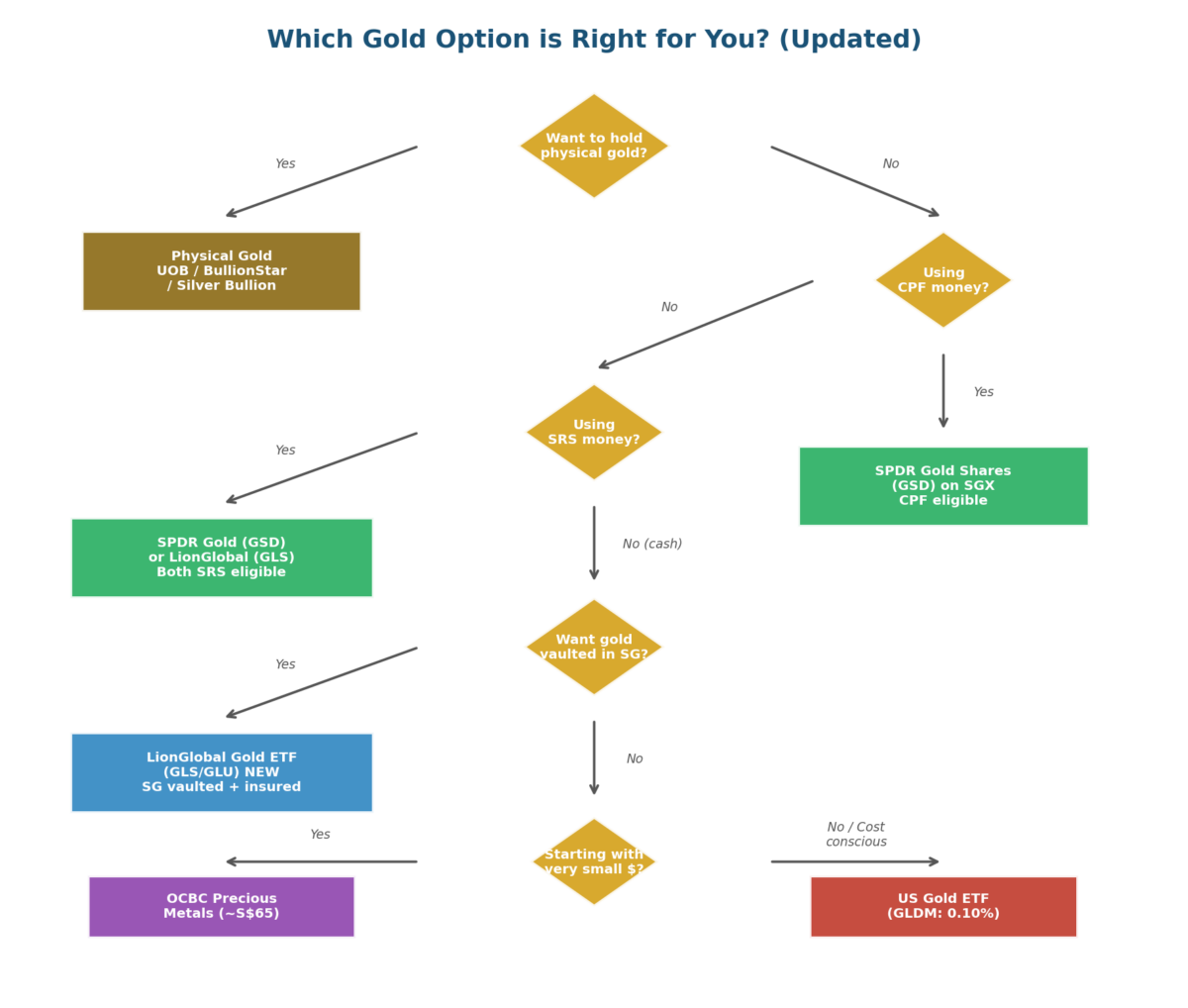

And if you’re not sure which option suits you, this updated decision flow might help:

We covered physical gold, SPDR Gold Shares, gold savings accounts, gold certificates, and futures/CFDs in detail in Part 1. So in this article let’s focus on the new kid on the block — the LionGlobal Physical Gold ETF.

Let’s get into it.

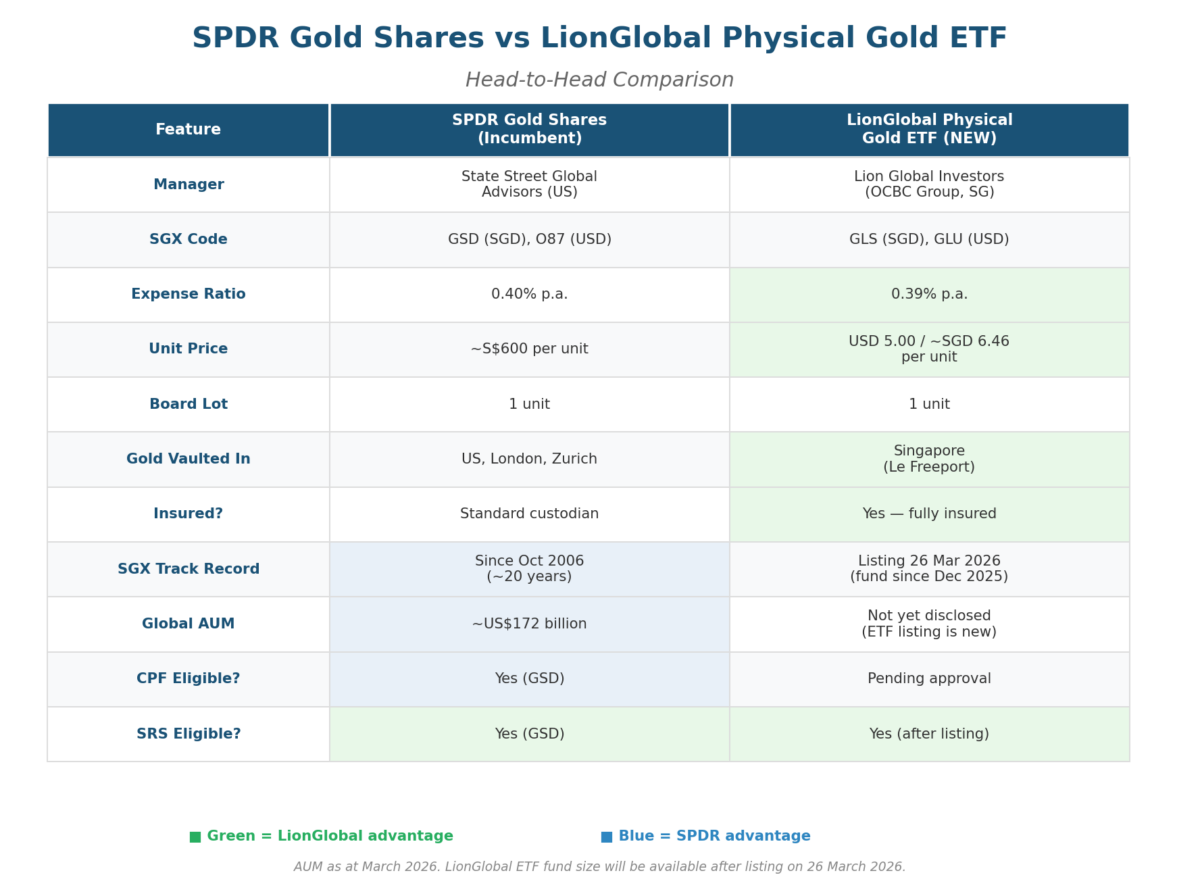

LionGlobal Singapore Physical Gold ETF — Fund Facts

The LionGlobal Singapore Physical Gold ETF is managed by Lion Global Investors, which is part of the OCBC Group.

The ETF is a listed share class of the LionGlobal Singapore Physical Gold Fund, which was incepted on 1 December 2025. So the underlying gold portfolio is not brand new — it has been managed since late 2025.

Here are the key details:

| Feature | Details |

| ETF Name | LionGlobal Singapore Physical Gold ETF |

| Reference Benchmark | LBMA Gold Price AM |

| Issue Price | USD 5.00 per unit |

| Initial Offer Period | 6 March 2026 to 20 March 2026 |

| Target Listing Date | 26 March 2026 |

| Base Currency | USD |

| Trading Currency | SGD and USD (dual currency on SGX) |

| SGX Code | GLS (SGD), GLU (USD) |

| Bloomberg Ticker | GLS SP (SGD), GLU SP (USD) |

| Board Lot Size | 1 unit |

| Management Fee | 0.39% per annum (capped at 2% of NAV) |

| Gold Storage | Le Freeport, Singapore — 24/7 security, CCTV, armed guards |

| Insurance | Allocated gold insured to full value against loss, theft and damage in custody and transit (applies to allocated gold, 95%+ of fund) |

| Classification | Excluded Investment Product (EIP) |

| CPF/SRS Eligible? | SRS: Yes (after listing). CPF (CPFIS): Not yet — pending approval |

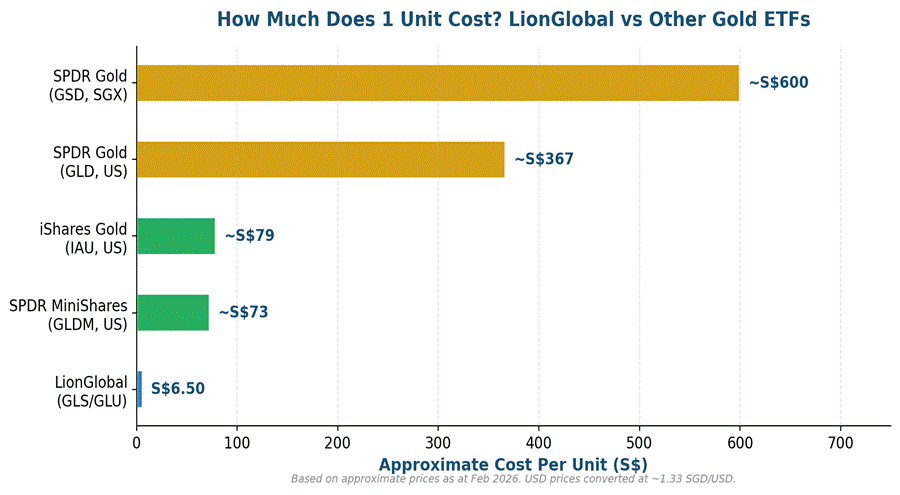

The thing that jumps out immediately — the USD 5.00 issue price. That’s SGD 6.46 per unit at the IOP exchange rate.

Compare that with SPDR Gold Shares at roughly S$600 per unit today.

With LionGlobal, you can start buying gold on the SGX for less than the price of a bubble tea.

SPDR Gold Shares vs LionGlobal

How does the new LionGlobal ETF stack up against SPDR Gold Shares?

Let me walk through each key difference.

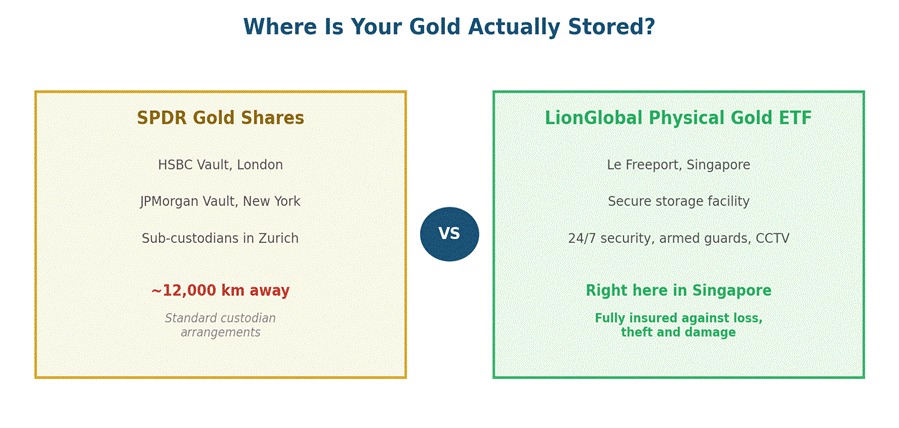

1. Where is the gold stored?

This is the headline differentiator.

SPDR stores its gold in HSBC’s vault in London and JPMorgan’s vault in New York, with sub-custodians in Zurich. Roughly 12,000 km away.

LionGlobal stores its gold at Le Freeport in Singapore — a secure storage facility with 24/7 security, electronic personnel monitoring, CCTV surveillance, and armed guards.

Does it matter where the gold is physically stored?

For most investors in normal times — probably not.

But we don’t live in normal times.

If the past few years have taught us anything — from Russia getting its foreign reserves frozen, to escalating US-China tensions, to the weaponization of the global financial system — it’s that where your assets are physically located matters.

As LionGlobal highlights — Singapore is globally recognised for its strong rule of law, stable foreign relations, safety from natural disasters, and has no history of gold confiscation since its founding in 1965.

Having gold stored in a politically stable, neutral jurisdiction like Singapore is a genuine differentiator for some investors.

2. Insurance

LionGlobal is the first gold ETF backed by physical gold, insured and securely vaulted in Singapore.

The allocated gold is insured to its full value against loss, theft and damage whilst in custody and in transit. (Note: insurance applies to allocated gold, which makes up 95% or more of the fund. Up to 5% may be held in an unallocated account to facilitate dealing.)

SPDR has standard custodian arrangements but doesn’t explicitly market itself as an “insured” gold fund.

In practice, both products have institutional-grade custody. The risk of gold being stolen from an HSBC vault in London is not exactly high.

But the explicit insurance does add a layer of protection that’s nice to have.

3. Fees

LionGlobal: 0.39% p.a. SPDR: 0.40% p.a.

A 1 basis point difference. On a S$10,000 investment, that’s S$1 per year.

For context — both SGX-listed options are significantly more expensive than the US-listed GLDM at 0.10% p.a. But you generally avoid US estate tax risk with the SGX options, so it’s a trade-off.

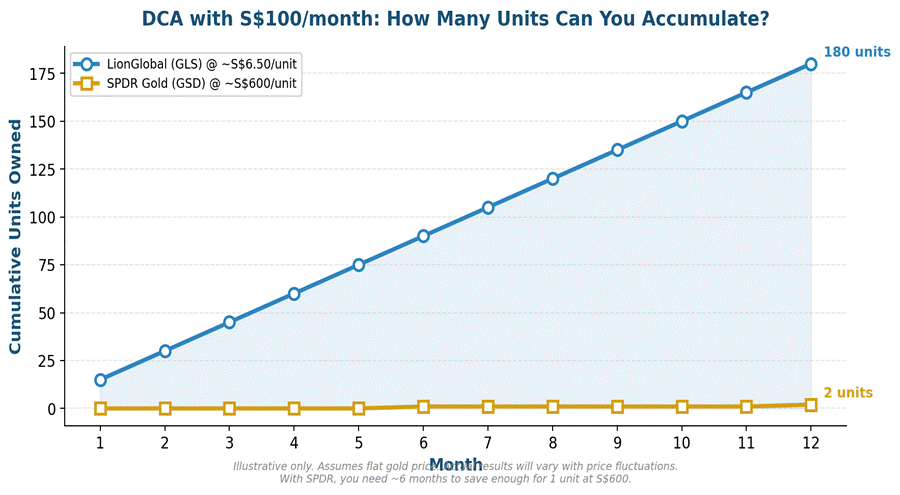

4. Entry Price — and what it means for DCA

This is where things get really interesting.

At ~SGD 6.46 per unit vs SPDR at ~S$600.

The unit price doesn’t affect total return — whether you buy 1 unit of SPDR or 91 units of LionGlobal, you have roughly the same gold exposure.

But the low unit price makes a massive difference for dollar-cost averaging.

If you’re DCA-ing S$100 per month, with SPDR you need ~6 months to buy your first unit. With LionGlobal, you buy ~15 units every single month.

The ability to deploy capital immediately rather than letting it sit as cash is a real advantage.

How does this compare to the other options from Part 1?

The OCBC Precious Metals Account also has a very low minimum (~S$65 for 0.01 oz), but that’s a bank book entry — not a listed ETF you can trade on the SGX.

And the UOB Gold Savings Account requires a 5g minimum (~S$1,125 at current prices) and charges 0.25% p.a. plus spreads.

So LionGlobal at SGD 6.46 per unit with 0.39% fee and SGX liquidity is actually very competitive as a low-entry option.

5. Track Record and Liquidity

SPDR has been on SGX since October 2006 — almost 20 years. Globally, ~US$172 billion in AUM. On SGX alone, >S$4.2 billion.

Larger AUM generally means tighter bid-ask spreads and deeper liquidity.

LionGlobal is brand new as an ETF — although the underlying existing gold fund has been managed since December 2025. Fund size will only be disclosed after listing on 26 March 2026.

That said, LionGlobal has appointed three Designated Market Makers — Phillip Securities, Flow Traders Asia, and North Point Global — which should help provide liquidity and tighter spreads from day one.

For a retail investor buying S$5,000–10,000, this is probably negligible. But for large trades it may matter.

For what it’s worth — physical gold from dealers like BullionStar or UOB is even less liquid than either ETF. Selling physical gold means going back to the dealer or bank, with wider spreads and more hassle.

6. CPF and SRS Eligibility

This is an important one for Singapore investors.

SPDR Gold Shares (GSD) is eligible for both CPF-OA and SRS funds.

LionGlobal is SRS eligible after listing — but not yet CPF (CPFIS) eligible. CPF inclusion is being worked on, but this typically takes time for new funds.

So if you want gold using your CPF money, SPDR is your only option currently.

But if you’re using SRS funds, LionGlobal will be available after its 26 March listing — giving you a second option alongside SPDR.

Overall thoughts

Neither product is objectively “better” across the board. They have different strengths for different investors.

LionGlobal Singapore Physical Gold ETF looks more attractive for investors who care about location peace of mind and DCA strategy: its gold is stored in Singapore, allocated holdings are insured, the fee is marginally lower, and the entry ticket is much smaller.

By contrast, SPDR Gold Shares stands out for investors who value scale, liquidity, and a long operating history. It is a much larger and more seasoned vehicle, which generally means better trading efficiency and tighter execution.

How to subscribe during the IOP?

The Initial Offer Period runs from 6 March 2026 to 20 March 2026. During this window you subscribe at the issue price of USD 5.00 per unit.

Strategic Partner: OCBC Securities

ATM, Mobile and Online Banking Subscription: OCBC — subscribe by 19 March 2026, 12pm, with an application fee of SGD 2. The USD-SGD exchange rate is predetermined at 1.2915, so you subscribe at SGD 6.4575 per unit.

Participating Dealers:

- Phillip Securities (POEMS)

- Moomoo

- Tiger Brokers

- FSMOne

- DBS Vickers

- Maybank Securities

- Lim & Tan Securities

(Note: each dealer has slightly different subscription deadlines. Check with your broker for exact deadlines.)

Full allotment is confirmed — you get exactly what you subscribe for, no balloting.

There are also IOP promotions — FSMOne is offering SGD 10 cashback per SGD 10,000 invested (capped at SGD 100, first 200 subscribers), POEMS is offering SGD 12 cash credit per USD 5,000 invested (capped at SGD 600, first 400 subscribers), and Tiger Brokers is offering cash coupons of SGD 5 to SGD 20 depending on investment size (first 300 subscribers).

After listing on 26 March 2026, buy and sell on SGX. Search for GLS (SGD) or GLU (USD).

Note on MariBank gold: Some of you asked about MariBank’s gold investments in the comments of Part 1. MariBank’s gold product is actually the unlisted version of this same LionGlobal fund. The ETF is just the listed (SGX-traded) wrapper. If you’ve been buying gold through MariBank, you’re already in the same underlying gold — the ETF just gives you the convenience of trading on the SGX.

The underlying fund was incepted on 1 December 2025, so MariBank gold investors have been in this fund since late last year.

Putting it all together — All gold options compared

Let’s put all the options side by side so you can make your own comparison.

| Option | Min. Investment | Annual Fee | CPF/ SRS? | Gold Location | Insured? | Liquid? | Best For |

| LionGlobal ETF (GLS/GLU) | ~SGD 6.46 | 0.39% | SRS yes; CPF pending | Singapore | Yes | Yes | DCA; SG-vaulted gold; new investors |

| SPDR Gold (GSD/O87) | ~S$600 | 0.40% | Yes (GSD) | US/London/Zurich | Std. | Very | CPF/SRS investors; proven track record |

| US ETFs (GLDM/IAU) | ~US$50+ | 0.10-0.40% | No | US/London | Std. | Very | Lowest cost (but US estate tax risk) |

| Physical Gold | ~S$225+ | Premium | No | Your safe/vault | You arrange | Low | Tangible gold; long-term hold; gifting |

| UOB Gold Savings | 5g (~S$1,125) | 0.25%+ | No | Bank (book entry) | N/A | Med. | Convenience; physical conversion option |

| OCBC Precious Metals | 0.01 oz (~S$65) | Spreads | No | Bank (book entry) | N/A | Med. | Very small amounts; multi-currency |

| Futures / CFDs | Varies | Spreads+ | No | N/A | N/A | Very | Active traders only |

My view — Should you subscribe to the LionGlobal Physical Gold ETF?

So after all of the above — what do I think?

My simple view.

I think this is a genuinely good product that fills a real gap in the Singapore market.

Three things I really like:

1. Gold vaulted in Singapore. In a world where geopolitics increasingly determines where your assets are safe, having gold stored locally is a meaningful differentiator.

2. Very low entry price. SGD 6.46 per unit makes this incredibly accessible for DCA. The ability to buy gold on the SGX for less than the price of a chicken rice is powerful.

3. Managed by OCBC Group. Institutional credibility.

So who is the LionGlobal ETF best for?

- DCA investors who want to buy gold monthly with small amounts on the SGX

- Investors who value Singapore vaulting and want their gold stored locally

- New investors who want to start a gold position with very little capital

- Cash or SRS investors who don’t need CPF eligibility

Who should stick with SPDR Gold Shares?

- CPF investors — SPDR (GSD) is the only CPF eligible gold ETF currently

- Institutional or large investors who need deep liquidity

- Conservative investors who prefer a 20-year track record

Who should consider physical gold or bank savings accounts instead?

- Investors who want zero counterparty risk — physical gold from BullionStar or UOB

- Investors who want physical conversion — UOB Gold Savings Account (convert to 100g bars)

- Very small, casual purchases — OCBC Precious Metals Account from S$65

What about owning both or all of the above?

Here’s a thought.

You could own both ETFs.

Use SPDR Gold Shares (GSD) for your CPF gold allocation. And use LionGlobal (GLS) for your cash or SRS gold allocation and DCA.

That way you get CPF eligibility from SPDR, plus Singapore vaulting and low entry price from LionGlobal.

And if you also want some physical gold you can hold, add an appropriate allocation via BullionStar or UOB.

Net net — more options and more competition is good for Singapore investors.

Singapore’s ambition to become a major gold hub in Asia just got a lot more real.

Singapore getting a locally-vaulted, insured, low-cost gold ETF? That’s good for all of us.

Love to hear what you think! Will you subscribe to the LionGlobal Physical Gold ETF during the IOP? Or stick with SPDR? Or go physical?

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi, nice write-up. Can you confirm that GSD/O87 actually avoids US estate taxes? I’ve been debating this at length with different AI tools and have uploaded the SG prospectus into the AI which responded with the following: “The prospectus is quite explicit about the risk. The US Prospectus section on estate tax (which forms part of this Singapore Prospectus) states directly that shares “may well be considered to be situated in the U.S.” for estate tax purposes, and if so, would be includible in the US gross estate of a non-resident alien shareholder at rates up to 40%. The reason this matters regardless of which exchange you buy on comes down to the custody chain. The prospectus describes how CDP maintains Account No. 5700 with DTC (a US depository), and all shares globally are evidenced by global certificates deposited with DTC and registered in the name of Cede & Co., DTC’s nominee. So when you buy GSD on SGX, your beneficial ownership flows through CDP → DTC → Cede & Co. The underlying instrument remains a New York grantor trust.” So if this is the case, the LionGlobal ETF should be a better instrument for avoiding US estate tax risk?

Let me see if this is something Lion Global can comment on.

Great article! My question is the opposite: sell not buy. Should I sell gold bought during 1980-2000? I missed the peak earlier this year. But you mentioned that gold is already up 75% compared to last year. So, should I sell? The greedy me is tempted to wait for it to peak again. But in this very uncertain time and considering that I’m getting old and don’t have another 20 years to wait for recovery if gold price goes south. Should I just sell instead of waiting for another peak? And what about silver? I have some silver coins bought from Singapore Mint. Should I sell them also? Instead of waiting for another peak?