In recent FH Premium articles, I have shared my views that this market is expensive across the board.

The S&P500 sits at a lofty 22.7 times forward P/E.

The last time it was this high – was 2021, and late 2024 – both of which eventually resulted in large declines.

But at the same time you have a Fed that is on a rate cut cycle, and a US president hell bent on depreciating the value of money.

Until either of the above changes, it also makes it dangerous to sit out this market entirely.

In a market like that, I think there is decent value to be had in both China and Singapore markets.

After the recent rally, China looks much closer to fair value today, but that’s a topic for another day.

For today’s article, I wanted to discuss the good ol SGX dividend stock.

Why are dividend stocks good in a climate like that?

The benefit with a dividend stock in this climate is that you are effectively getting paid to wait (via the dividend).

The stock price can literally go nowhere for a year and you’re already ahead vs T-Bills simply because of the dividend.

If the stock price goes up, that’s just icing on the cake.

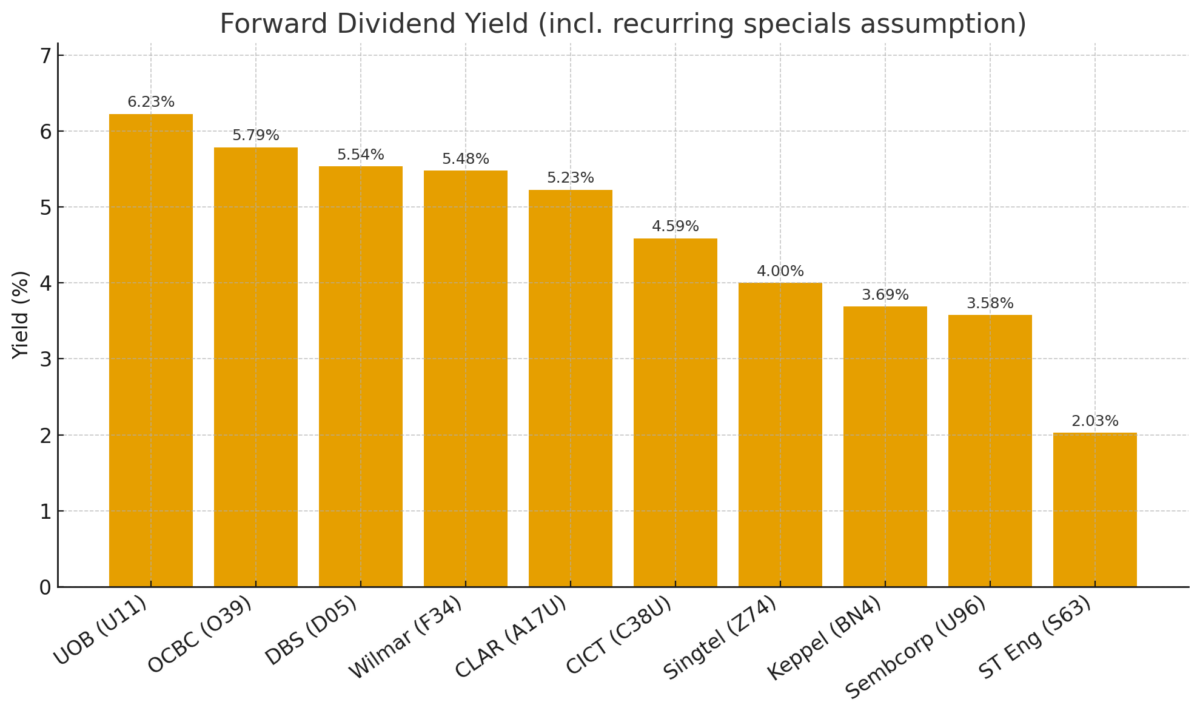

Which are the Top 10 dividend yield stocks on the SGX with attractive risk-reward today?

I’ve compiled a list of the Top 10 blue-chip dividend stocks on the SGX that I think offers decently attractive risk-reward.

Arranging from highest dividend to lowest:

| Name | Ticker | Share Price (S$) | Forward Dividend Yield (estimated) |

| United Overseas Bank | U11 | 35.33 | 6.23% |

| OCBC | O39 | 16.92 | 5.79% |

| DBS | D05 | 54.16 | 5.54% |

| Wilmar | F34 | 2.92 | 5.48% |

| CapitaLand Ascendas REIT (CLAR) | A17U | 2.86 | 5.23% |

| CapitaLand Integrated Commercial Trust (CICT) | C38U | 2.37 | 4.59% |

| Singtel | Z74 | 4.25 | 4.00% |

| Keppel | BN4 | 9.21 | 3.69% |

| Sembcorp Industries | U96 | 6.43 | 3.58% |

| ST Engineering | S63 | 8.87 | 2.03% |

Do note that the forward dividend yield is calculated by annualizing the latest dividend (and assuming that special dividends continue to be paid going forward).

So by its very nature this is an estimate, and can change if the assumptions do not hold.

Top 5 highest yield dividend stocks on SGX I would buy? 5% dividend yield minimum?

Now of the list above – which dividend stocks would I consider buying?

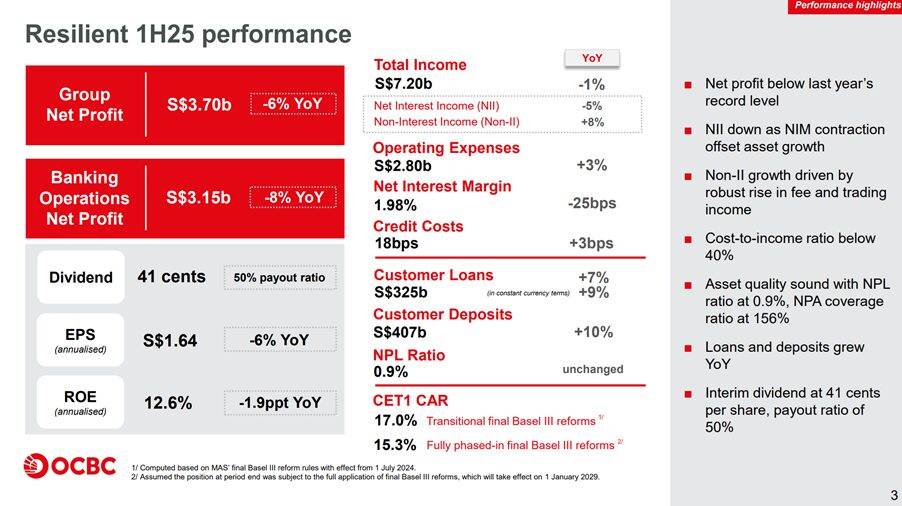

OCBC Bank (O39) – 5.8% dividend yield

It should come as no surprise that OCBC is on the list (full disclosure that I hold a position in OCBC – full portfolio breakdown shared on FH Premium).

I wrote an article comparing the 3 local banks last week, and my conclusion was that I liked the risk-reward for OCBC today:

“You’re getting a 6% dividend yield at a comfortable 60% payout ratio so you get paid to wait.

Price/Book is a reasonable 1.2x which limits downside if things head south (whereas DBS looks scary at 2.09x Price/Book).

And a good chunk of the business is insurance / wealth management, which (hopefully) is less cyclical than the core lending business, and provides earnings resilience even if interest rates continue to fall or we get a recession.”

I suppose the risk with OCBC Bank (or any bank stock today for that matter), is that you’re literally buying banks into a rate cut cycle.

With the market is pricing in another 4 rate cuts to come.

Yes you can argue that the banks will be able to preserve their net interest margins by paying lower interest rates on customer deposits.

But it’s also fairly clear that net interest margins are indeed going down with lower interest rates, and this is hitting bank profitability.

Ultimately though, the question is whether it is priced in, and whether you’re getting decent risk-reward at the price you buy.

At a 1.2x book and about 5.8% dividend yield, I think the answer is a qualified yes.

But of course, as with all stocks, you do need to manage risk, and size the position well.

Sembcorp Industries (U96) – 3.6% dividend yield

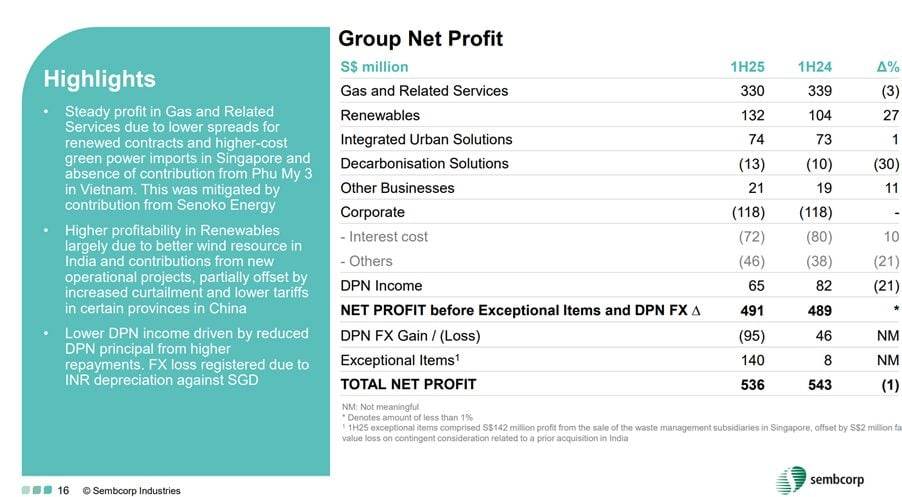

Sembcorp Industries is an interesting one, and I did think long and hard about whether it belonged on this list of dividend stocks.

I looked at Sembcorp Industries a month or two back after the post earnings drop, and this was my conclusion then:

“For what it’s worth, I like the story of using profits from the Singapore power business to reinvest in renewables regionally.

I like that valuations are cheap.

I also like that dividend payout ratio is low, and the strong pipeline and decent balance sheet means we can probably see room for dividend growth years to come.

What makes me slightly more nervous is that huge exposure to China renewables, because it really just is very hard to predict how power prices in China play out (given national goals of keeping power costs low).

I think what holds me back – is that base case, the stock probably still just chops around for 12 months, and the upside is probably in the 10 – 20% range that I set out above.”

Fundamentally, nothing much has changed from that analysis.

Sembcorp today is still a business where the bulk of the profits comes from the Singapore power generation business (which don’t get me wrong is a great business I would want to own).

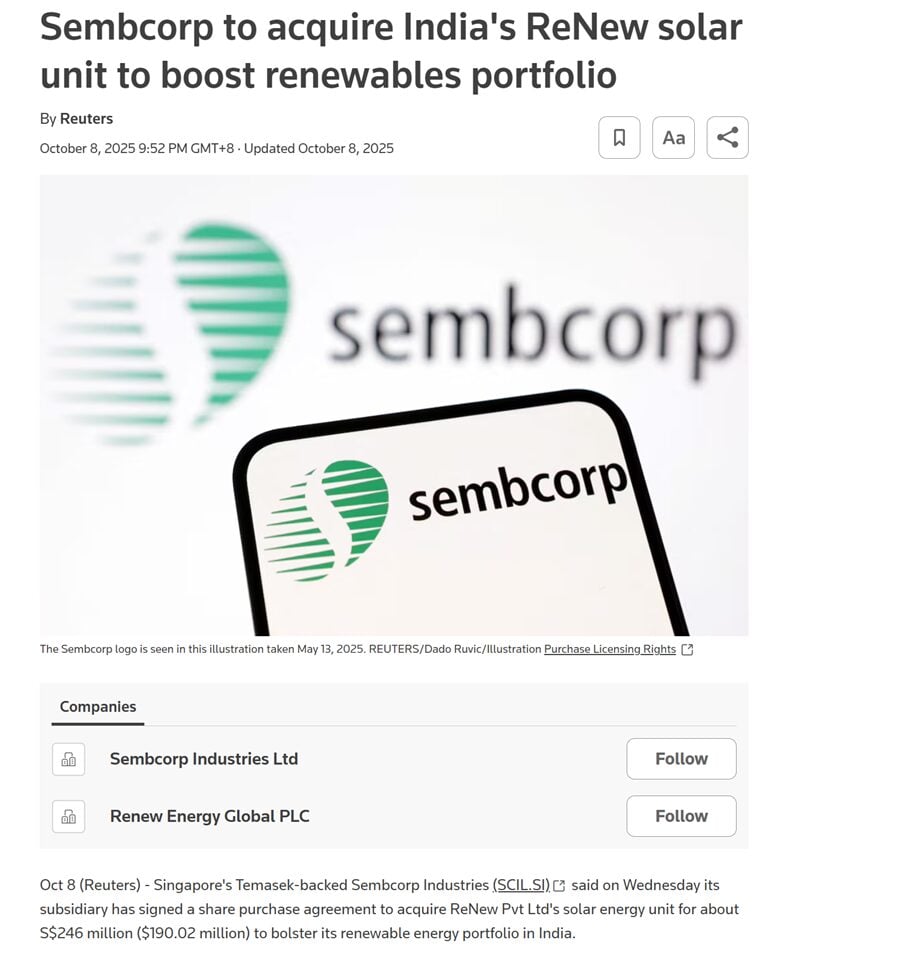

And Sembcorp is taking those profits to invest in renewable energy in India and China, as the growth engine.

See for example their acquisition of ReNew Pvt Ltd’s solar energy unit for S$246 million to bolster its renewable energy portfolio in India.

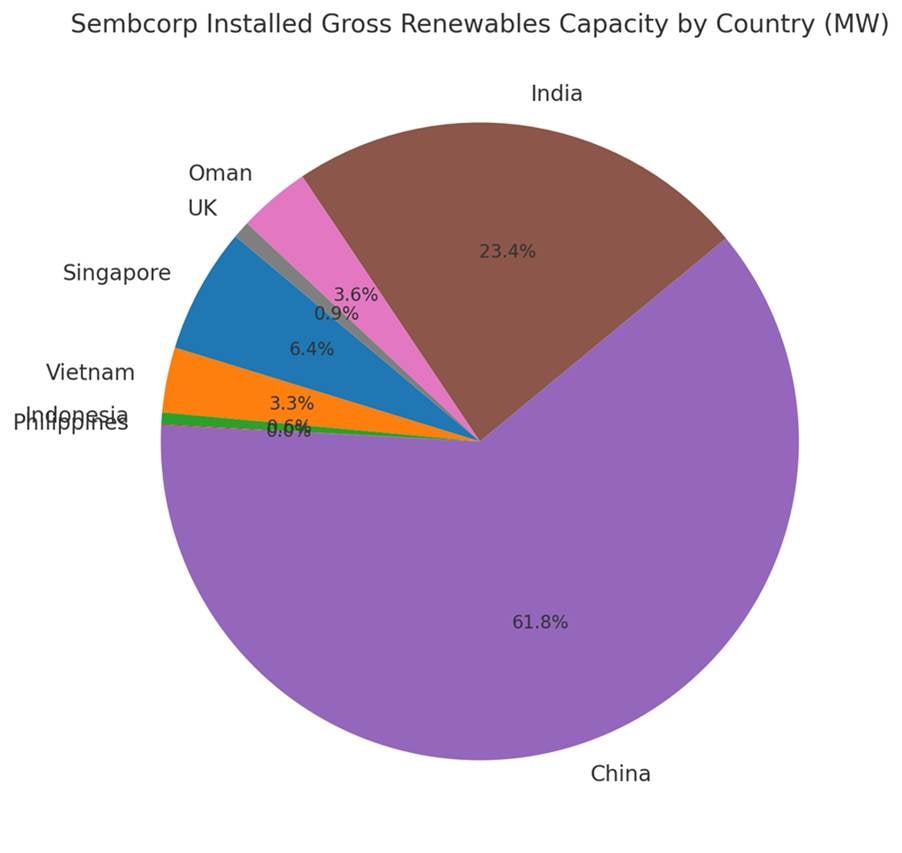

Although that said, for now China is the bulk of the renewables capacity:

So nothing much has changed on the core strategy / fundamental picture.

What has changed I suppose, is that the chart is showing some a potential breakout, rising above the 50 and 200 day moving averages of late:

I still don’t like the huge China exposure from Sembcorp as I think the China electricity generation market will be structurally oversupplied for years to come (policy wise it makes sense for China to run a cheap energy regime).

But I like the core Singapore business, and I like the general direction that Sembcorp is moving towards.

If the chart continues to look healthy, Sembcorp could be an interesting add.

Singtel (Z74) – 4.0% dividend yield

Speaking of boring TLCs that take profits from a core cash cow to invest in new growth areas.

We then have Singtel.

Much like Sembcorp, Singtel’s new strategic direction is to take the profits from its core Telco business (in Singapore, Australia and regionally), and invest in new growth areas of data centers (nxera) and enterprise technology (NCS).

And hence the strategy of Singtel as a “yield + growth” stock.

Much like Sembcorp, I’ve liked Singtel for a while now on this basis.

And it generally looks like the market agrees:

My only reservation is that at current share price Singtel looks quite fairly valued to me, so it’s no longer a bargain.

But in a market where everything else is expensively valued, I guess you could argue comparatively that fair value is the new “cheap”.

CICT (C38U) – 4.6% dividend yield

Ascendas REIT (A17U) – 5.2% dividend yield

Okay, I cheated slightly for number 4.

If you asked me to pick between CICT, Ascendas REIT and Frasers Centrepoint Trust.

I would say why bother picking and why not just buy all 3.

That’s pretty much the logic here.

If you want broad exposure to office, industrial, and retail Singapore properties.

That’s pretty much what you’re getting with these REITs.

The problem is that REITs in general have rallied quite a bit in 2025, so they are no longer cheap.

But this is again relative, because when you consider the fact that you were getting 3%+ on a risk-free T-Bill at the start of the year, and you’re only getting 1.44% now, then actually comparatively REITs still look good value.

The drawback of course, is that eventually when interest rates go back up, REIT prices will probably go down.

So do be aware of that.

UOB Bank (U11) – 6.2% dividend yield

And for the final name on this list.

You know what I thought long and hard (and you can see the honourable mentions below).

But I thought UOB Bank deserved a spot as well.

Yes the chart is indeed ugly and it looks to be in a downtrend, so you do want to be careful.

But including special dividend, UOB Bank pays a 6.2% dividend yield.

And UOB’s higher ASEAN SME exposure means that if the macro turns around, UOB Bank could have greater upside than either OCBC Bank or DBS Bank.

And the acquisition of Citibank’s ASEAN consumer banking business means that if UOB executes well on integration, there could be further upside there (although yes I am always skeptical when it comes to big M&A and “synergy”).

The biggest red flag with UOB Bank today is the chart though, and technical analysis wise it does look scary to buy a position here.

But that said I do think UOB Bank deserves a spot on this list.

| Name | Ticker | Spot (S$) | Forward Dividend Yield (estimated) |

| United Overseas Bank | U11 | 35.33 | 6.23% |

| OCBC | O39 | 16.92 | 5.79% |

| DBS | D05 | 54.16 | 5.54% |

| Wilmar | F34 | 2.92 | 5.48% |

| CapitaLand Ascendas REIT (CLAR) | A17U | 2.86 | 5.23% |

| CapitaLand Integrated Commercial Trust (CICT) | C38U | 2.37 | 4.59% |

| Singtel | Z74 | 4.25 | 4.00% |

| Keppel | BN4 | 9.21 | 3.69% |

| Sembcorp Industries | U96 | 6.43 | 3.58% |

| ST Engineering | S63 | 8.87 | 2.03% |

Honourable Mention – DBS Bank – 5.5% dividend yield

DBS Bank is on a tear recently.

To the point where it seems there’s just structural institutional inflow into DBS Bank at this point.

Yes I know I have been cautious with DBS Bank for a while now, and yet the share price keeps going up, so do take what I say with a pinch of salt.

But at this price DBS Bank trades >2.1x book value.

And the 5.5% dividend yield includes the special dividend which pushes dividend payout ratio into the 75% range.

So yes, DBS Bank can continue to go higher if institutional money continues to flow in.

But at these prices you do need to be careful of downside risk in case something goes wrong.

But no doubt a fantastic dividend stock firing on all cylinders at the moment.

Honourable Mention – Keppel – 3.7% dividend yield

Keppel is an interesting one.

Power generation / infrastructure / data centre is just a great business to be in right now with all the massive data centre demand, and they’ve also done well in the pivot to fund management (just look at the chart above).

Question is whether this can continue going forward.

If you think the answer is yes, then hey Keppel could be an interesting choice too.

Closing Thoughts – Top 5 highest yield dividend stocks on SGX I would buy? 5% dividend yield minimum?

And there you have it!

Top 5 highest yield dividend stocks on SGX I may consider buying?

Love to hear what you think though.

Any other stocks that deserve to be on this list?