So I came across this podcast with Singtel CFO Arthur Lang over the weekend.

And as I went through the podcast, it occurred to me that a lot of the stuff the CFO was saying, especially on using their cash flows from the mature telco business and reinvesting into growth areas of data centres and enterprise tech, really echoed what I’ve been saying about Singtel.

At the same time – share price has been astounding since I started looking at Singtel stock again.

Up almost 65% in the past 12 months.

With that in mind, I wanted to take a closer look at Singtel stock.

At 4.5% dividend yield and a fantastic looking chart – would I buy this stock?

This is an FH Premium post that I am making available to all readers.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Key takeaways from Podcast with Singtel Group CFO Arthur Lang (11 Jun 2025)

The full podcast is here.

A high level summary from me:

- Earnings momentum is real. Underlying profit climbed 9 % and group EBIT jumped 20 % in FY25, powered by a 55 % EBIT surge at Optus and a 39 % jump at NCS, with tighter cost control and a focus on high-return projects driving the gains.

- “Yield + Growth” is the pitch. Management frames Singtel as a hybrid: cash-rich telco core funds a steady 70-90 % payout, while capital-light tech businesses (NCS) and capital-heavy data centres (Nxera) provide structural growth.

- Bigger cash returns are coming. FY25 dividends total S$0.17 per share (≈ 4.5 % yield at current prices) and a fresh S$2 billion share-buyback programme is under way, partially funded by asset-sale proceeds.

- Capital recycling remains a core playbook. About S$1.9 billion was unlocked in FY25 (Airtel selldown, real-estate, etc.). Lang says only “non-core or matured” assets are sold, with plenty of dry powder left for future monetisation.

- Nxera’s next leg is de-risked. KKR will invest up to S$1.5 billion for a 25 % stake, giving Singtel capital to double SEA data-centre capacity (e.g., Tuas, Malaysia, Thailand) without stretching its own balance sheet.

- Balance-sheet firepower is comfortable. Net-debt/EBITDA sits at 1.5× with mostly fixed-rate borrowings and 18× interest cover; active FX hedging protects offshore dividend flows.

- Singapore remains competitive, but differentiated. Singtel avoids price wars via sub-brands (Gomo, Heya) and pushes a premium “5G+” experience for higher-value users, helping local operations stay a key EBIT contributor despite crowded markets.

Bottom line: Singtel is leaning on disciplined capital recycling and partnerships to fund its data-centre and IT-services expansion while still upping shareholder returns. For investors, the stock offers a mix of mid-4 % cash yield today and optionality from growth platforms like Nxera and NCS.

What caught my attention with Singtel stock?

3 points that caught my eye, that I wanted to discuss further:

- Singtel as a “Yield + Growth” stock?

- 4.5% dividend is pretty juicy?

- How solid is the future growth from Nxera and NCS?

Singtel as a “Yield + Growth” stock?

Essentially:

“Yield + Growth” is the pitch. Management frames Singtel as a hybrid: cash-rich telco core funds a steady 70-90 % payout, while capital-light tech businesses (NCS) and capital-heavy data centres (Nxera) provide structural growth.

In plain English.

Singtel used to be a boring ah-gong stock that earns money from its telco business.

Okay Singtel today is still earning the bulk of its revenue / profits from the boring ah-gong telco business.

But the difference is that instead of paying all those profits out as a dividend.

Singtel today is taking some of those profits to reinvest into future growth – namely data centres (Nxera) and enterprise tech (NCS).

I talked about this in my articles on Singtel last year, and shared how I really like what management has been doing on this front.

That remains true today.

How has Singtel been executing on this strategy?

So we have strategy (above), then we have execution.

You can see the numbers below.

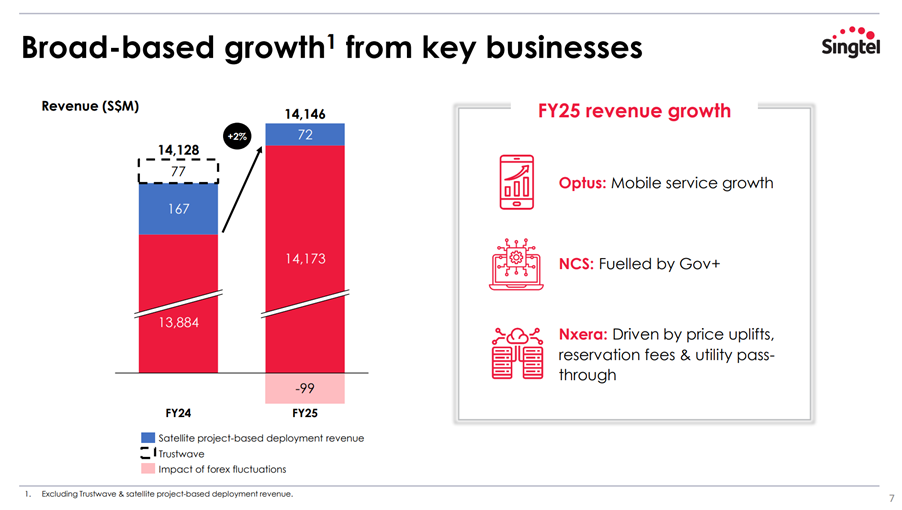

The core Singtel business in Singapore remains stable both on a revenue and EBIT perspective, which is good as it shows the days of declining profits due to intense competition are over (for now).

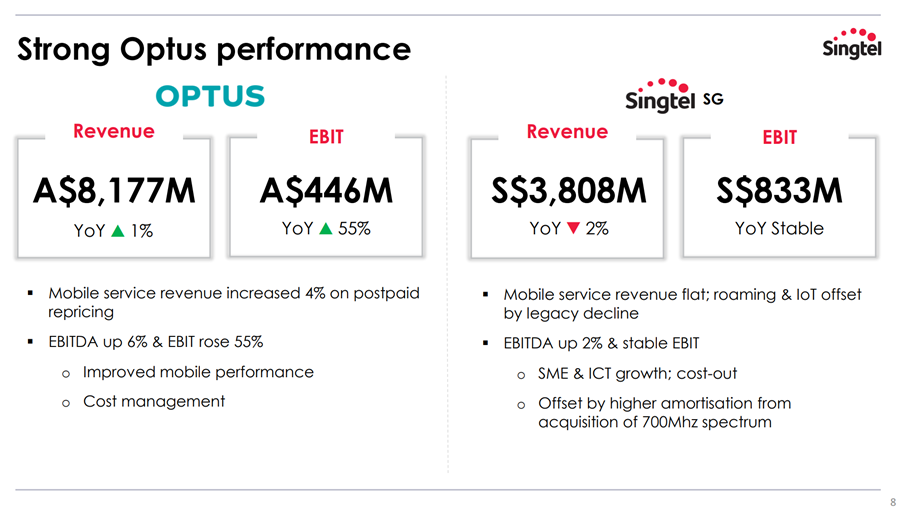

Meanwhile the Australian Optus has flat revenue, but EBIT/EBITDA are both up nicely on what looks to be operational improvements.

This is good, because you want to see the core business remaining stable and generating strong cash flows for reinvestment into new business lines (and sustaining the dividend).

Both Optus and Singtel SG are 100% owned by Singtel.

Then we have the regional associates – the regional telco businesses owned by Singtel that it does not own 100% of.

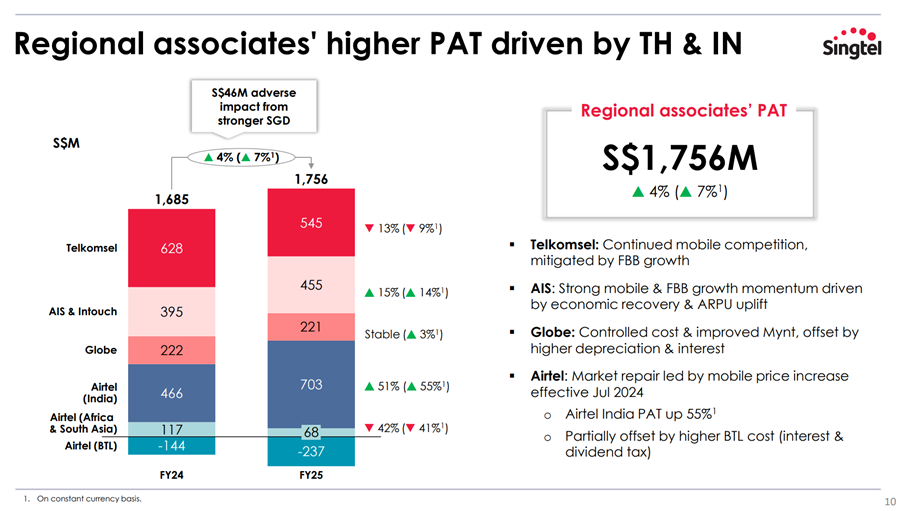

Generally speaking, performance is decent across the board, with a 4% pick up in profit after tax.

You can see the breakdown below, where the Indonesia Telkomsel has not been doing well, but this has been offset by the strong performance in Thailand and India.

Dividend is pretty juicy – 4.3% at the latest share price

Per the podcast summary above:

- Bigger cash returns are coming. FY25 dividends total S$0.17 per share (≈ 4.5 % yield at current prices) and a fresh S$2 billion share-buyback programme is under way, partially funded by asset-sale proceeds.

17 cents dividend.

At latest share price of 3.95, that’s a 4.3% yield.

For what it’s worth, here’s the comparison vs other Temasek Portfolio Companies:

| Rank | Company | Latest indicated yield * | Gap vs Singtel (4.3 %) |

| 1 | DBS Bank | 6.7 % | ▲ +2.4 ppt |

| 2 | Singapore Airlines (SIA) | 5.8 % | ▲ +1.5 |

| 3 | UOB Bank | 5.3 % | ▲ +1.0 |

| 4 | OCBC Bank | 5.1 % | ▲ +0.8 |

| 5 | Sembcorp Industries | 4.9 % | ▲ +0.6 |

| 6 | Keppel Ltd. | 4.7 % | ▲ +0.4 |

| 7 | CapitaLand Investment | 4.7 % | ▲ +0.4 |

| 8 | Singtel | 4.3 % † | — |

| 9 | ST Engineering | 2.1 % | ▼ -2.2 |

| 10 | SATS | 1.6 % | ▼ -2.7 |

* “Latest indicated yield” refers to the forward or trailing-twelve-month ordinary dividends divided by the current share price, rounded to one decimal place.

† Singtel’s 4.3 % is based on its FY-2025 total dividend of S$0.17 and the recent share price of ~S$3.95, matching the figure you quoted.

Here’s the commentary from ChatGPT O3, which is pretty interesting:

- DBS remains the dividend king. Its quarterly cheques and stepped-up base DPS (plus the odd special) keep it comfortably on top at ~6.7 %. Raised ROE guidance and a chunky CET-1 buffer give management room to keep the tap flowing.

- Banks dominate the top tier. UOB’s 90th-anniversary special bump and OCBC’s higher regular payout lift both above 5 %, though still shy of SIA’s refreshed level.

- SIA slots straight into second place. After restoring a 40-cent payout (30 ¢ final + 10 ¢ interim), the flag-carrier now throws off a near-6 % yield—handsome for an industry still climbing out of the pandemic hole.

- Middle of the road: Sembcorp, Keppel, CLI.

- Sembcorp edges up thanks to rising renewables cashflows.

- Keppel’s yield normalises after last year’s one-off O&M windfall rolled off.

- CapitaLand Investment stays resilient at ~4.7 %, underpinned by management fees and dividend income from its listed REITs.

- Singtel is now firmly mid-pack. Its 4 %-plus payout is respectable but no longer top-quartile among its Temasek siblings, especially after the banks’ bumper years.

- Low-yield corner: ST Engineering and SATS continue to reinvest heavily (defence-aviation capex and post-pandemic ramp-up, respectively), leaving income investors with yields south of 2 %.

Bottom line for income hunters

- If you want the fattest cheques, DBS (and now unexpectedly SIA) lead the charge, with UOB and OCBC close behind.

- The infrastructure-to-energy plays (Sembcorp, Keppel) offer middling yields but stronger growth optionality.

- Singtel still provides a decent carry, but the relative gap has narrowed—hardly the standout it once was.

- ST Engineering and SATS remain more of a growth (or recovery) story than a dividend one.

Okay I get that it’s slightly lower than the banks at 5%ish dividend yield.

But Singtel offers a very different risk-reward profile being in the Telco / Tech business, and also you cannot have all your portfolio in bank stocks right?

And the banks profitability looks pretty maxxed out here, and with declining interest rates and uncertainty over economic growth, there may be downward pressure on bank profitability going forward.

Whereas Singtel with the telco business is quite a different play, and the Nxera and NCS plays give growth potential.

So there is some nuance beyond just looking at dividend yields, as the sustainability and growth potential matters as well.

How solid is the future growth for Singtel?

That said.

Much of the future growth potential of Singtel, is conditional on how well they execute on Nxera and NCS.

This is not rocket science.

The entire premise of the strategy is to use cash flow from the maturing boring telco business to invest in sexy growth areas.

So management really needs to deliver here.

Nxera is the data centre business, and NCS is the enterprise tech business.

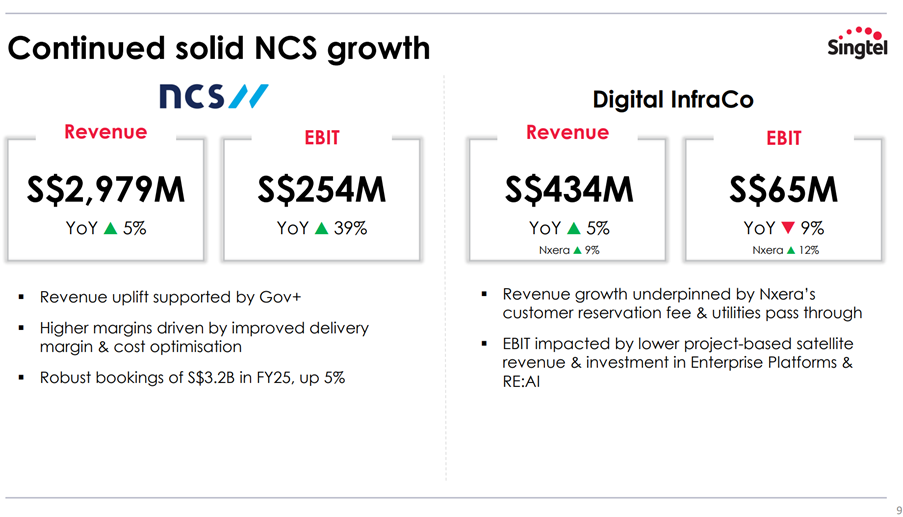

You can see the numbers below.

NCS is doing well, with decent revenue growth, and very strong EBIT growth on operational improvements.

Follow Financial Horse to avoid missing any post!

The data centre Nxera is mixed, but this is understandable as they are still in the data centre build out phase and it will take time for the revenue / profits to show.

From the podcast this was what the CFO shared:

- Nxera’s next leg is de-risked. KKR will invest up to S$1.5 billion for a 25 % stake, giving Singtel capital to double SEA data-centre capacity (e.g., Tuas, Malaysia, Thailand) without stretching its own balance sheet.

My personal take is that NCS is the more proven product at this stage.

For Nxera – a lot of promises have been made, but so far we haven’t seen the concrete execution / numbers yet, and until we do it is hard to comment definitively.

Unlike Keppel where you know for certain that they can run and execute a data centre delivery, I don’t think Singtel has the same track record (for now – but happy to be proven wrong).

That said, big picture wise the numbers look good, which is why you see this rewarded in the share price.

Will I buy Singtel Stock at 4.5% dividend yield?

Bottom line – I like what management is doing with Singtel.

In hindsight I probably should have bought a position at the low 3s range, after my original article in mid 2024, and the price dipped.

But the fact is I didn’t and there’s no point crying over spilt milk.

At today’s share price, and a 4.3% dividend yield, I think the upside is not as attractive as it was at the low – mid 3s.

So personally I don’t see myself buying a position for now.

But that said, Singtel is definitely a stock on my watchlist, and at the right price, or if management continues to execute well, I could well pick up a position.

As always, I share regular updates on FH Premium on what I am buying and selling, as well as my full portfolio.

This is an FH Premium post that I am making available to all readers.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).