Malaysian stocks have had a very strong performance in 2024.

The Bursa Malaysia (the Malaysia stock index) is up 12% in 2024 alone.

Meanwhile the Malaysian Ringgit (MYR) has strengthened about 4% against SGD this year

Throw in the dividend of about 3%+.

And actually the Bursa Malaysia has had a total return of 17% in 2024 (and that’s in SGD terms).

Meanwhile the STI is up only about 4% year to date.

With dividends that’s about 7% returns – less than half of the Bursa Malaysia.

I know a lot of FH readers also invest in Malaysia stocks (or are keen to understand more).

So I wanted to spend some time looking at Malaysia stocks today, but I would really appreciate any feedback from you guys.

If you want more content on Malaysia stocks, or on alternative topics – please let me know in the comments below!

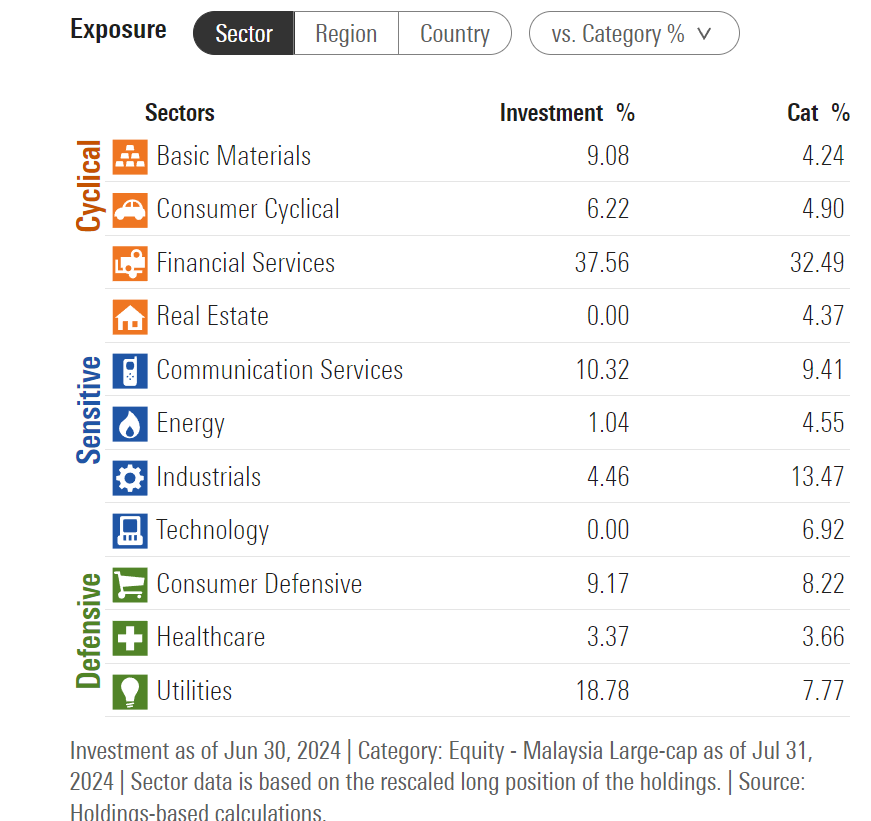

Malaysia Stocks offer a very different exposure to Singapore stocks – Diversification benefits

The broad sector exposure of the Bursa Malaysia below.

Like the Singapore STI Index – it is very heavy on banks.

But unlike the STI, which is very heavy on real estate.

The Bursa Malaysia has very different exposure to a mix of cyclicals (materials, energy, industrial) and defensives (healthcare, utilities).

So pure returns aside, there are interesting diversification benefits in adding Malaysian stocks to your normal portfolio (that would be heavy on US/Singapore stocks).

But what about FX Risk?

But I know many investors will point out that when investing in Malaysia (or Emerging Markets generally).

FX risk is a huge risk that needs to be watched out for.

I’ve charted the Bursa Malaysia (candles) against the MYR/USD pair below (red).

You can see that while the stock index has gone up since 2009.

The currency has been continually depreciating against the SGD (or USD).

In fact from 2009 to today, the Ringgit has depreciated 36% against the SGD.

This would have eroded a big chunk of any stock returns.

So… are Malaysia stocks still a good investment?

That is where I think some nuance comes into play.

With Emerging Markets like Malaysia.

Actually the biggest returns come from tactically playing the cycles.

If you buy at the right time when the economy is on a cyclical upswing, when foreign investors are pouring capital into the country, you benefit from both stock price appreciation + FX appreciation.

This can really supercharge returns.

This is actually playing out right now, as expectations over US rate cuts has weakened the USD pair, and driving an outflow of money from US into Emerging Markets.

This is partly why you see Malaysian stocks performing well in 2024, and if rate cuts play out aggressively there could be more room to run.

The challenge of course, is that you want to exit the positions before the cycle reverses.

And for that you will need some understanding of where we are in the cycle.

Long story short though, is that you can definitely make money on Malaysian stocks if you know what you are doing.

Top 5 Malaysia Stocks I may buy in 2024 – for capital gains and dividend yield?

YTL Power International Berhad

2024 Year to Date (YTD) Performance: +59%

Dividend Yield: 2.33%

Dividend Payout Ratio: 14%

Let’s start with the standout performer in Malaysia in 2024 – YTL Power International Berhad.

This power generation company is up 59% in 2024, and it was up 110% at one point.

By comparison, Singapore’s Keppel (which also generates electricity) is down 13% in 2024.

The reason why power generation is in Malaysia is doing so well, but not in Singapore?

Because of AI of course.

AI data centres consume much more electricity than traditional data centres.

So for investors who want to bet on the AI trend, they have been crowding into the electricity trade.

The reason why Singapore electricity stocks like Keppel have not benefitted similarly is because Singapore has been “stingy” with approval for new data centres.

There was even a moratorium on building new data centres at one point, out of fears that data centres would place unnecessary strain on the city’s power grid.

Out of necessity, this forced data centres into neighbouring countries like Malaysia and Indonesia – where electricity supply is plentiful.

Just like in the US – local electricity producers have had a huge boost in share price as a result.

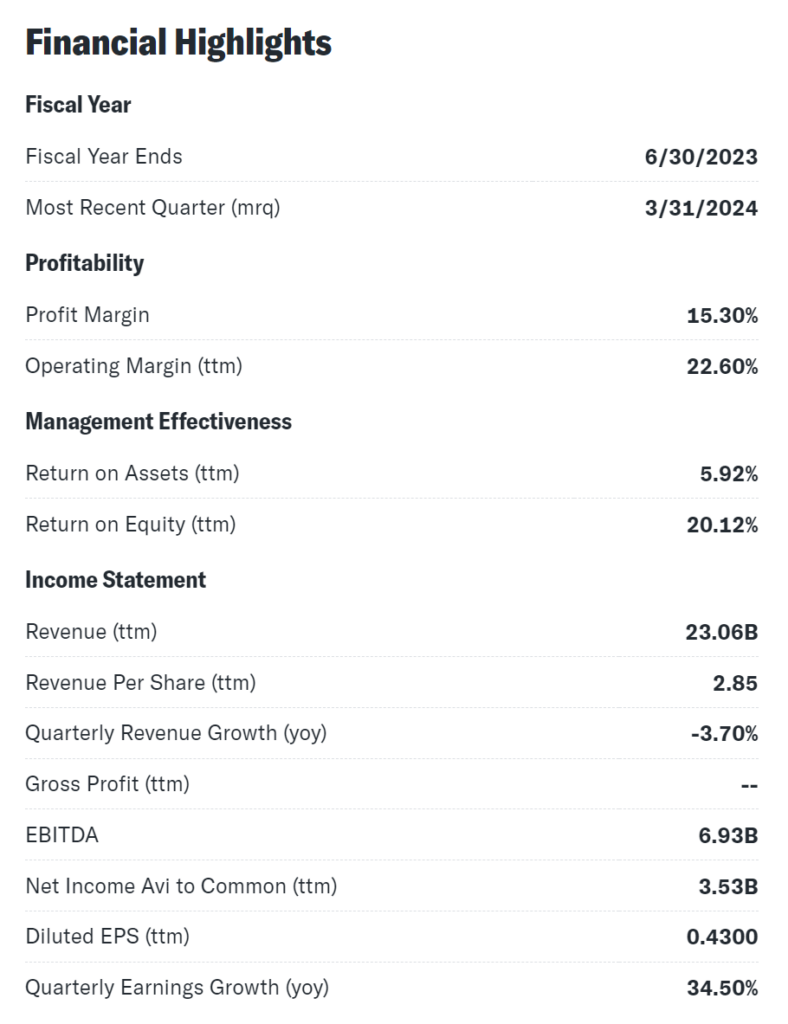

Even after the 59% rally in 2024 (was up 110% at one point), trailing P/E is only 8.8x.

For a company that is growing earnings 34% on a year on year basis, and has a 20% ROE (that’s higher than DBS Bank).

Tenaga Nasional Berhad

2024 Year to Date (YTD) Performance: +39%

Dividend Yield: 3.3%

Dividend Payout Ratio: 107%

In the electricity generation space in Malaysia.

Tenaga Nasional Berhad is the larger, state-linked national utility focused primarily on Malaysia.

While YTL Power is a more diversified, international player with a broader range of utility-related businesses.

That said, AI is a massive tailwind for this space, which has become a rising tide lifts all boats scenario.

This stock is up 39% in 2024 alone.

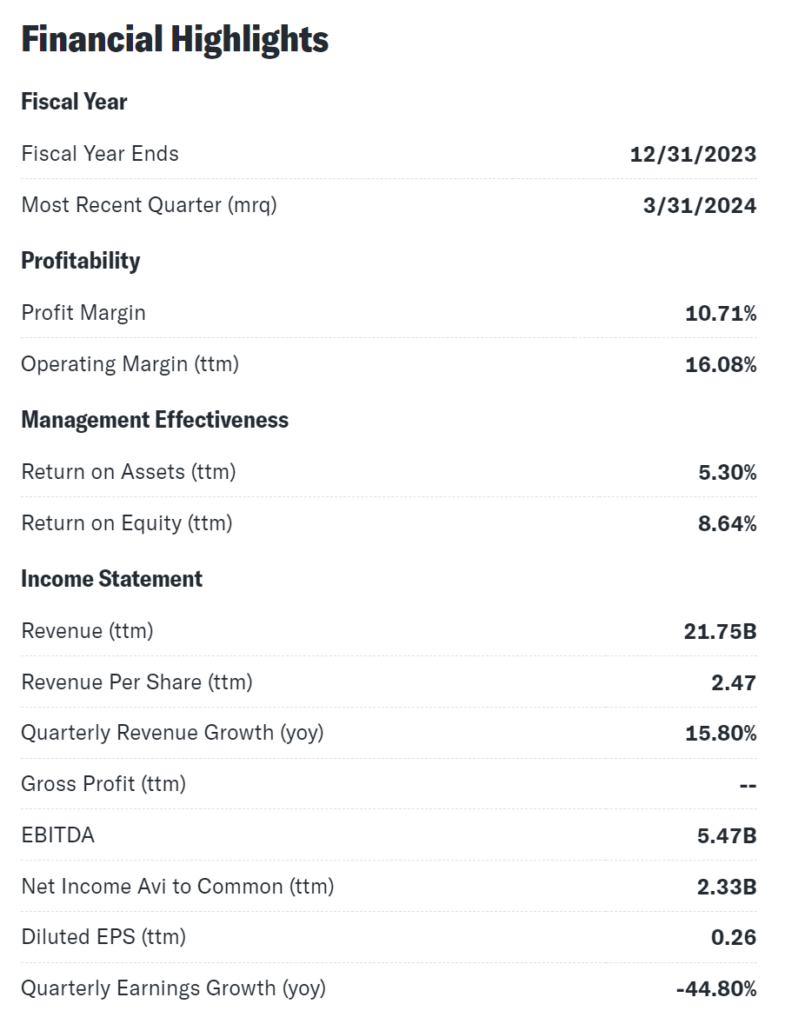

Generally speaking the numbers don’t look as good as YTL Power.

Trailing P/E is 32x, and Forward P/E is 20x.

Operating Margin is 12.7% (vs 22% for YTL), and ROE is a measly 3.9%.

But sometimes you just need to be in the right place at the right time, as the stock price has demonstrated.

Malayan Banking Berhad

2024 Year to Date (YTD) Performance: +18%

Dividend Yield: 5.7%

Dividend Payout Ratio: 75%

With the “sexy” AI power generators out of the way.

Let’s go back to basics.

Malayan Banking Berhad (Maybank) is the largest bank in Malaysia.

If you love bank stocks, I suppose you would love Maybank.

This bank stock is up 18% in 2024 alone – exactly the same performance as DBS Bank.

On top of that you’re getting a 5.7% dividend yield, which is pretty similar to what the Singapore bank stocks are paying today.

Do note that the dividend payout ratio for Maybank is 75%, which is higher than the Singapore Bank stocks which average around 50%.

P/E ratio is 13.3x, and Price/Book is 1.3x.

For a bank with a 10.6% ROE, with 9.8% year on year revenue growth.

Is that cheap?

I think it really goes back to the discussion above on where we are in the cycle for Malaysia generally.

If you think that the US rate cut cycle is going to drive a lot of capital out of developed markets into emerging markets, and that the Ringgit is going to strengthen against the USD, then hey I would say these valuations are cheap and I could see further upside.

But if you think the US may enter a recession, and the subsequent risk-off may drive the USD sharply higher.

Then we might be much later in the cycle for Malaysia stocks, and I would be more cautious.

Time will tell.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

CIMB Group Holdings Berhad

2024 Year to Date (YTD) Performance: +32%

Dividend Yield: 4.6%

Dividend Payout Ratio: 52%

If you want an alternative to Maybank.

CIMB Group is the third largest bank in Malaysia (behind Maybank and Public Bank).

The stock is up 32% in 2024, and you’re getting a 4.6% dividend yield.

Valuations wise CIMB Bank is slightly cheaper than Maybank, but I suppose this is fair as they are slightly smaller and less dominant.

Price/Book is 1.24x, trailing P/E is 11.55.

ROE is similar at 11.0%.

Earnings growth is slightly better at 17.7% year on year.

Fundamentally though, with Malaysian banks it’s not that different with Singapore banks.

In that yes you can spend a lot of time analysing differences between the various banks, but at the end of the day they are “same same but different”.

Each of them will give you broad exposure to the country’s economy.

Just buy 2 or 3 of the biggest banks (to diversify away the single stock risk) and ride the broad exposure to the country’s economic cycle / GDP growth.

IHH Healthcare Berhad

2024 Year to Date (YTD) Performance: +5%

Dividend Yield: 5.7%

Dividend Payout Ratio: 75%

IHH Healthcare is, as the name suggests, a Healthcare company.

Key brands include names that would be familiar to most Singapore investors:

- Mount Elizabeth – A well-known hospital brand in Singapore.

- Gleneagles – An international hospital brand with presence in Singapore, Malaysia, India, and Hong Kong.

- Parkway – Another prominent healthcare brand in the group’s portfolio.

- Acibadem – A leading healthcare provider in Turkey and the surrounding region.

- Prince Court – A healthcare facility brand.

- Fortis – A healthcare brand primarily operating in India.

- Pantai – A hospital brand in Malaysia.

- IMU (International Medical University) – Focused on medical education services

Healthcare services are provided across Singapore, Malaysia, India and Greater China.

List of shareholders is equally interesting, with Mitsui as the largest strategic investor (Mitsui themselves being the Japan trading house that is invested in by Warren Buffett)

Second largest shareholder meanwhile is Khazanah, the Malaysia Sovereign Wealth Fund (Temasek equivalent):

- Mitsui & Co., Ltd.: The largest shareholder, holding 32.80% of shares.

- Khazanah Nasional Bhd.: The Malaysian government’s sovereign wealth fund, owning 25.94% of shares.

- Employees Provident Fund: Holds 11.25% of shares.

- Mehmet Aydinlar: Owns 5.877% of shares.

- Aydinlar Family: Holds 3.486% of shares.

Generally speaking though, the share price has been pretty disappointing.

Up 5% year on year.

And share price has been somewhat flat since 2018 (although there is a juicy 5.7% dividend yield).

Trailing P/E is 23x which looks cheap, but falling profits means that forward P/E is a pricey 36x.

ROE is a measly 8.6%.

And year on year profits is down a staggering 45% (but revenue is up 15.8%).

So generally speaking the short term numbers are not good, which explains the disappointing stock performance.

That said healthcare is as recession proof as it gets, and the brands owned by IHH Healthcare (Gleneagles, Mount Elizabeth, Parkway) are pretty sound.

Closing Thoughts: Would I buy commodities stocks in Malaysia?

Some of you may have realised that commodities stocks are a notable exception from this list.

The Bursa Malaysia is heavy on commodities stocks, and the Top 10 largest names include stocks like:

- Press Metal Aluminium Holdings Berhad

- Petronas Chemicals Group Berhad

- Petronas Gas Berhad

So why did I leave commodities out of this list of stocks?

The short answer is that because with latest macro events (US data weakening, China economic growth staying weak).

I think the outlook for commodities has become less bullish than it was just 6 – 12 months ago.

Between inflation and economic slowdown, I think the greater fear in the short term is the latter.

You can see how stocks like Petronas Chemical peaked in early 2022 with the Russia/Ukraine war, and have been trending down ever since.

I still like commodities in the mid term, but in the short term, I can definitely see the risks piling up – and I have been dialling back exposure in my own portfolio (see my full portfolio on FH Premium).

So there you have it!

Top 5 Malaysia Stocks I may buy in 2024 – for capital gains and dividend yield.

Note that this is just a snapshot of my views, and for obvious reasons my views will change and evolve going forward (as facts change).

For my latest updated views, and the full list of stocks I am keen to add (across US, Singapore and China), do sign up for FH Premium.

This post is written on 23 Aug 2024 and will not be updated going forwards. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

Dear FH,

Thank you for sharing about Malaysia shares with us. Much appreciated.

Can you share about the tax on Dividend payout by the company (if any)? i.e. witholding tax etc.

Thanks for the kind words.

No, there are no withholding tax on Malaysia dividends. The key risk though is FX, as the Ringgit is quite a volatile currency.

Dear FH,

Thanks for sharing that Malaysia Dividends do not have witholding tax. On a side note, I think IHH is also listed in SGX too. If a SG person want to buy IHH stock, what is the key consideration for him/she to buy IHH at Malaysia stock exchange instead of buying this stock at SGX?

Thanks

Because there is no withholding tax, and the underlying assets are the same, there is no big difference to be honest.

The bigger consideration would be (1) liquidity and (2) personal investor preference.

If one were truly neutral about both exchanges – I might just go for Malaysia exchange for the better liquidity.

Hi FH, my take is that for KLSE, the growth and risk/reward lies in the mid cap section of the market instead of the big caps mentioned above. Names like Sunway, Sunway Construction, Gamuda, IJM, Mah Sing have seen YTD returns in excess of 60%. Would really love it if you could review some of the potential growth stocks especially in sectors like Data Center, Semicon and renewal energy. tq

Thanks Leon, that’s a great comment. I do agree there is better opportunity in the mid caps, the challenge is always stock picking and being able to identify the right names.

I will definitely have a closer look though, especially the names you mentioned.

Sunway in particular I have heard a lot of good things.

Hi FH, thanks for doing a great favour to prospective investors like me who wish to invest in Bursa listed stocks. Hope you can run more commentaries on Bursa listed stocks in the coming months ahead.

Thanks for the feedback. Appreciate it very much – will do my best!