One of the most common questions I get from readers is — “What is a good net worth in Singapore?”

And it’s a fair question.

Because Singapore is one of the wealthiest countries in the world on paper.

But if you live here, you know it doesn’t always feel that way.

When the person next to you at the hawker centre is driving a Porsche Cayenne, and million-dollar HDB resale flats are now the norm, it’s natural to wonder — where do I actually stand?

So I figured it was time to crunch the numbers.

In this article, I’ll break down the actual data on net worth in Singapore — from the average, to the median, to what you need to be in the top 10%, top 1%, and how to think about all of this at different life stages.

I shared my views on the US-Iran war over multiple articles this week, so I thought for the Sunday piece we’ll do something lighter.

Let’s dive in.

Important caveat: There is no official table of net worth percentiles in Singapore broken down by age. SingStat publishes income deciles, but not wealth deciles. So these are ultimately estimates based on the best available data, and should be taken as rough guides rather than gospel.

What is the average net worth in Singapore?

Let’s start with the big picture.

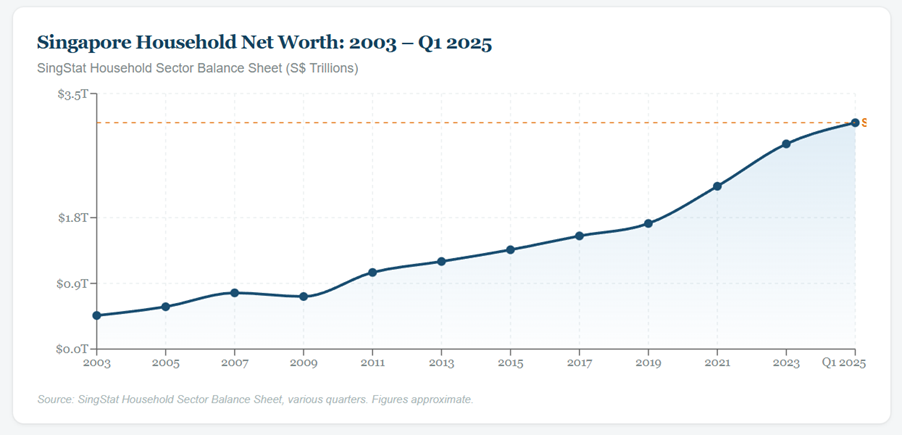

According to SingStat’s Household Sector Balance Sheet, total Singapore household net worth reached S$3.1 trillion as at Q1 2025.

Yes, you read that right. S$3.1 trillion.

You can see in the chart below how Singapore household net worth has grown from S$0.46 trillion in 2003 to S$3.1 trillion today — a roughly 6.7x increase over 22 years.

With approximately 1.43 million resident households in Singapore, that works out to an average household net worth of approximately S$2.17 million.

Now before you freak out at that number — hold on.

The average is massively skewed by the ultra-wealthy.

Singapore is home to an estimated 333,000+ USD millionaires (as per the UBS Global Wealth Report 2024), and that number has been growing rapidly.

Over 3,400 high-net-worth individuals moved to Singapore in 2023 alone.

So the average is pulled up by a relatively small number of very wealthy individuals and families.

Which is why we need to look at the median.

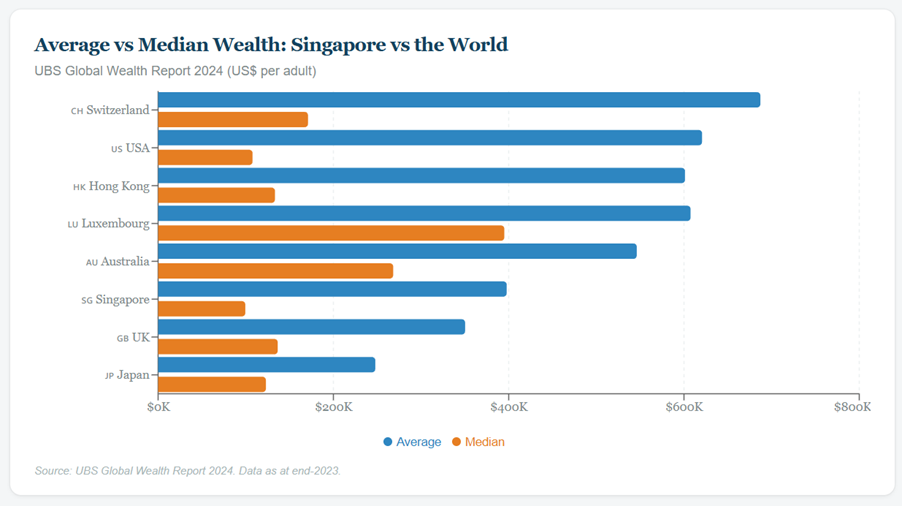

What is the median net worth in Singapore?

The median is a much better indicator of where the “typical” Singaporean stands.

According to the UBS Global Wealth Report 2024, the median wealth per adult in Singapore was approximately US$99,500 (roughly S$134,000) as at end-2022.

That’s a significant gap from the average of US$397,708 (S$537,000) per adult in the same report.

The chart below visualises this gap — average wealth is nearly 4x the median.

Assuming an average household size of 3 – 4 members.

That means a household net worth somewhere around S$400,000 to S$600,000, is probably around the median.

That’s roughly what the typical Singaporean household is worth.

What makes up a typical Singaporean’s net worth?

This is where it gets interesting.

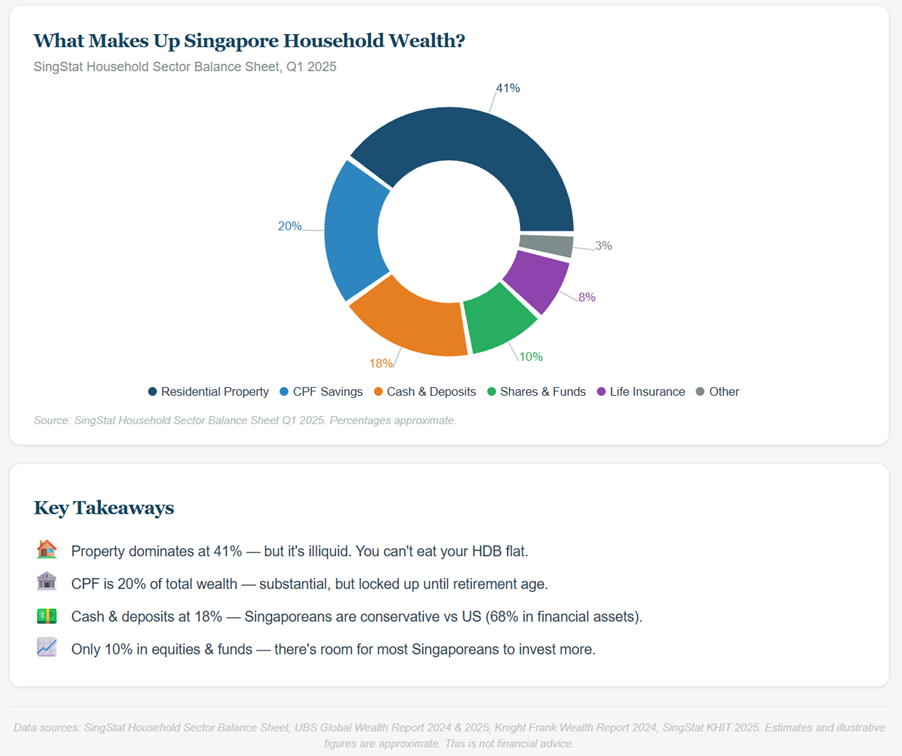

Based on SingStat’s household balance sheet (Q1 2025), here’s the rough breakdown of what makes up household wealth in Singapore:

- Residential Property: ~41% of total net worth

- CPF Savings: ~20%

- Cash and Deposits: ~18%

- Shares, Securities, Unit Trusts and Investment Funds: ~10%

- Life Insurance: ~8%

- Other: ~3%

A couple of observations here.

Property dominates. This is hardly surprising given Singapore’s obsession with real estate, and the fact that home ownership rates exceed 87%.

But it also means that a huge chunk of Singaporean household wealth is illiquid. You can’t eat your HDB flat.

CPF is a significant chunk. At 20% of total wealth, CPF savings are a real contributor.

For 2026, the CPF Full Retirement Sum (FRS) is S$220,400 for members turning 55, while the Enhanced Retirement Sum (ERS) is S$440,800.

That’s a meaningful sum that counts towards your net worth — but again, it’s largely illiquid until retirement age.

Singaporeans are conservative investors. Cash and deposits make up 18% of wealth, versus only about 10% in equities and funds.

Compare this to the US where 68% of household assets are in financial assets. Singaporeans clearly prefer the safety of cash and property over stocks and bonds.

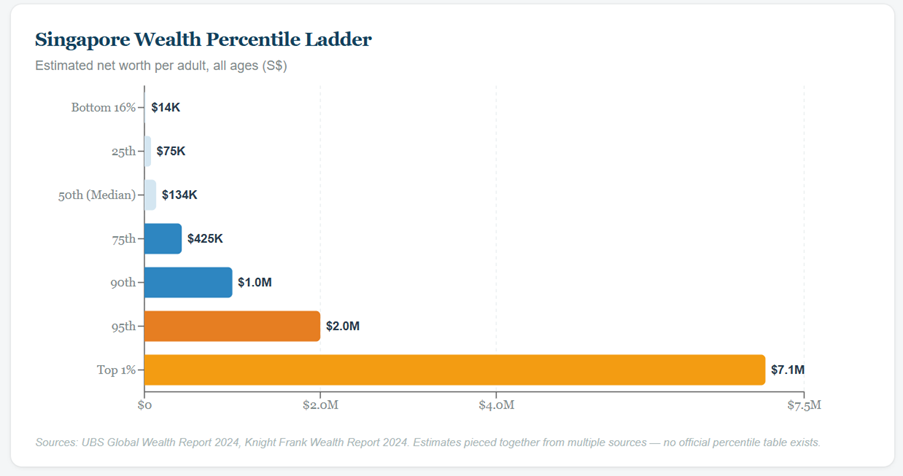

Net worth benchmarks — Where do you stand?

Alright, so let’s get to the question everyone really wants answered.

Here’s my best estimate of net worth benchmarks in Singapore, pieced together from UBS, Knight Frank, SingStat data, and various analyses.

Important caveat: There is no official table of net worth percentiles in Singapore broken down by age. SingStat publishes income deciles, but not wealth deciles. So these are estimates based on the best available data, and should be taken as rough guides rather than gospel.

Wealth distribution per adult (all ages, approximate):

| Percentile | Estimated Net Worth (S$) | What this means |

| Bottom 16% | Below ~S$13,500 | Based on UBS data showing 16% of adults have less than US$10,000 |

| 25th percentile | ~S$50,000 – S$80,000 | Modest savings, possibly young adults or retirees |

| 50th percentile (Median) | ~S$134,000 per adult | The “typical” adult in Singapore |

| 75th percentile | ~S$350,000 – S$500,000 | Comfortable, but not wealthy by Singapore standards |

| 90th percentile | ~S$800,000 – S$1.2 million | Upper middle class, likely own private property |

| 95th percentile | ~S$1.5 – S$2.5 million | High-net-worth territory |

| 99th percentile (Top 1%) | ~S$7 million+ | Knight Frank 2024: US$5.23m (~S$7.06m) to be top 1% across all ages |

For context, Singapore has the highest top 1% net worth threshold in Asia, and ranks fifth globally behind Monaco, Luxembourg, Switzerland, and the US.

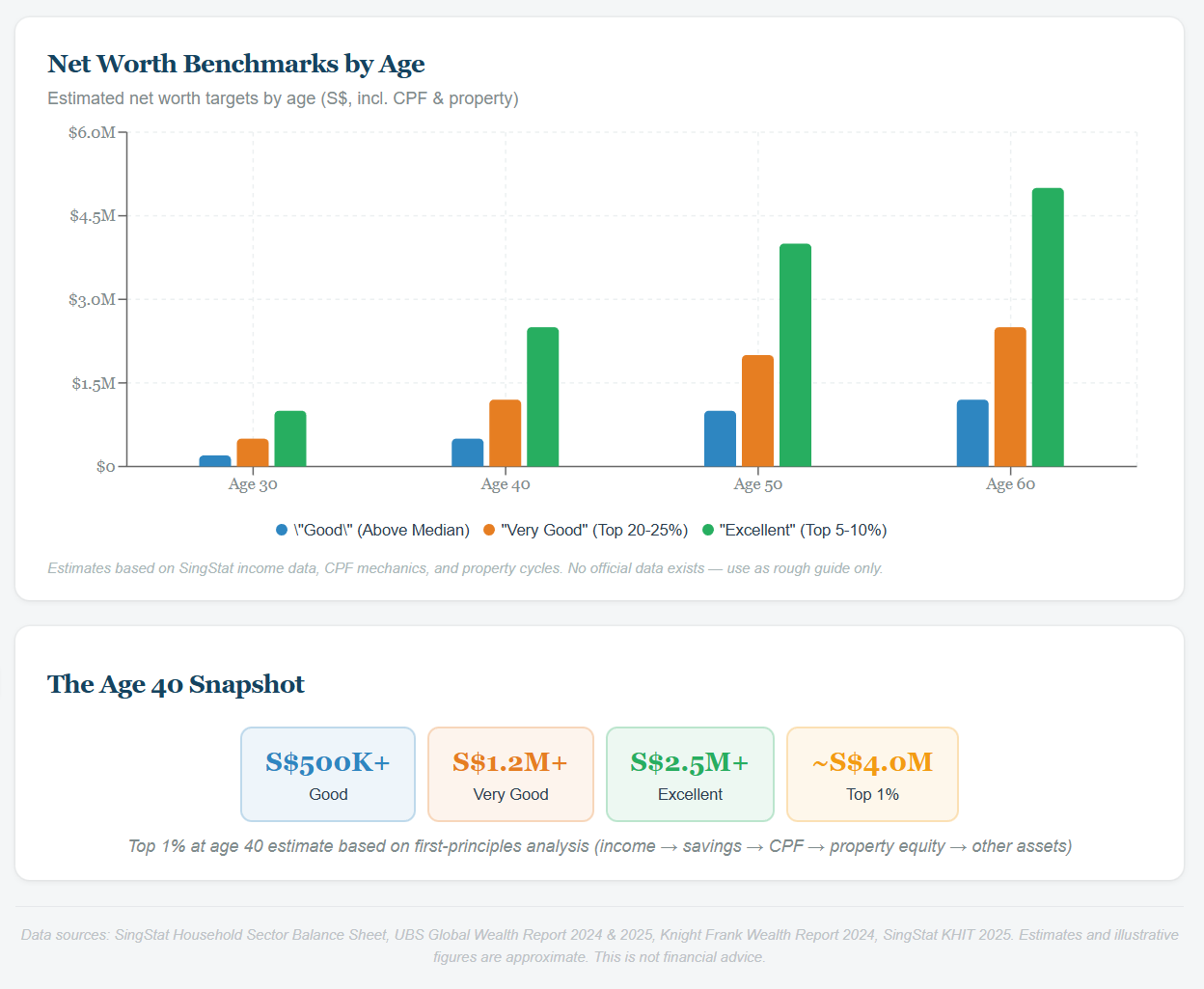

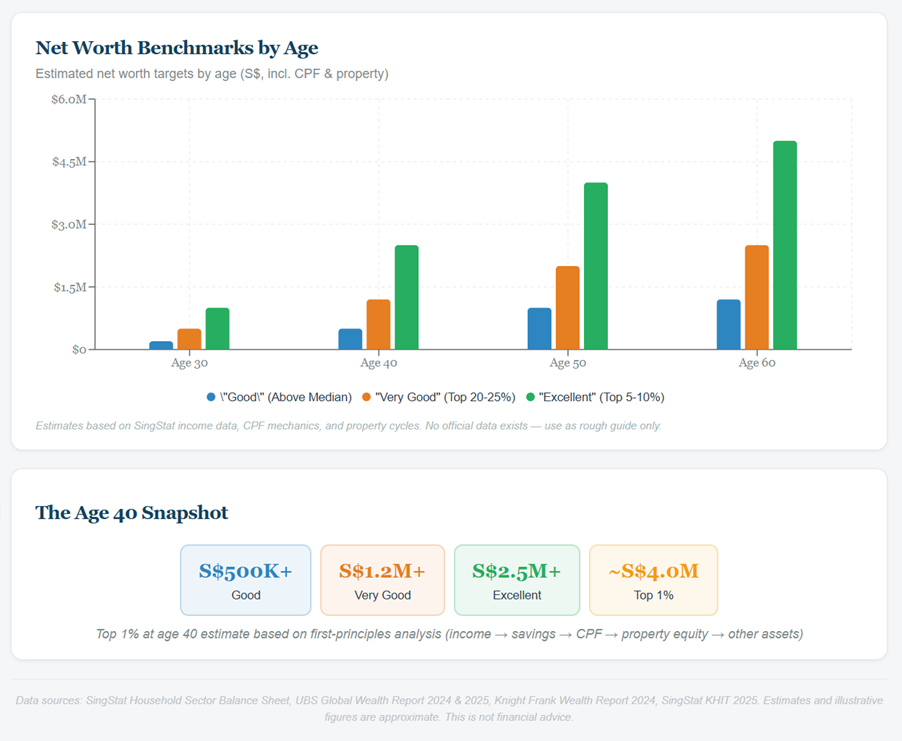

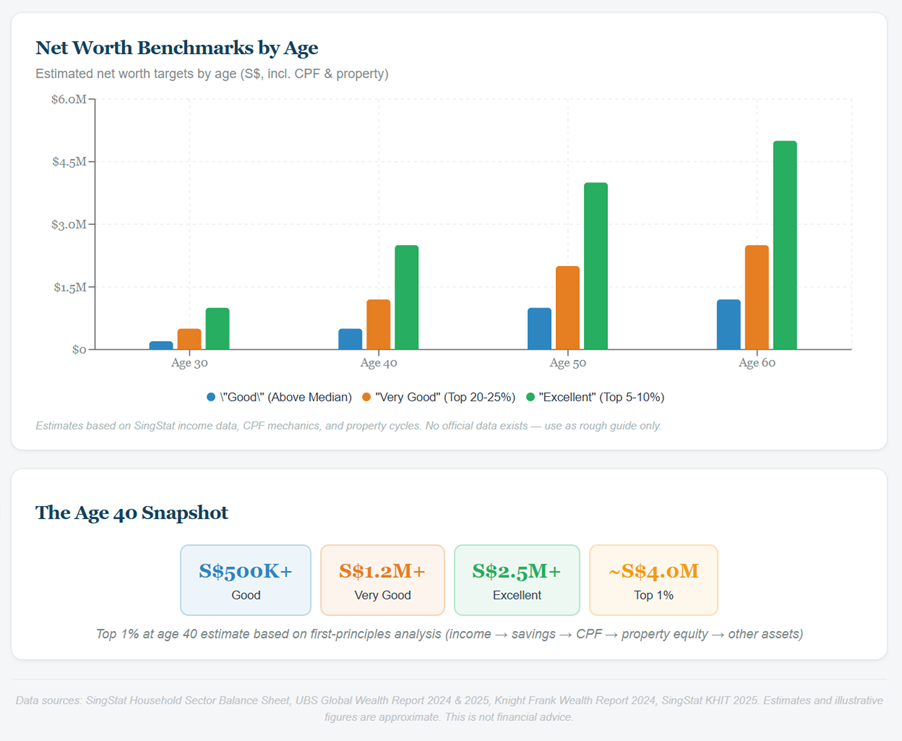

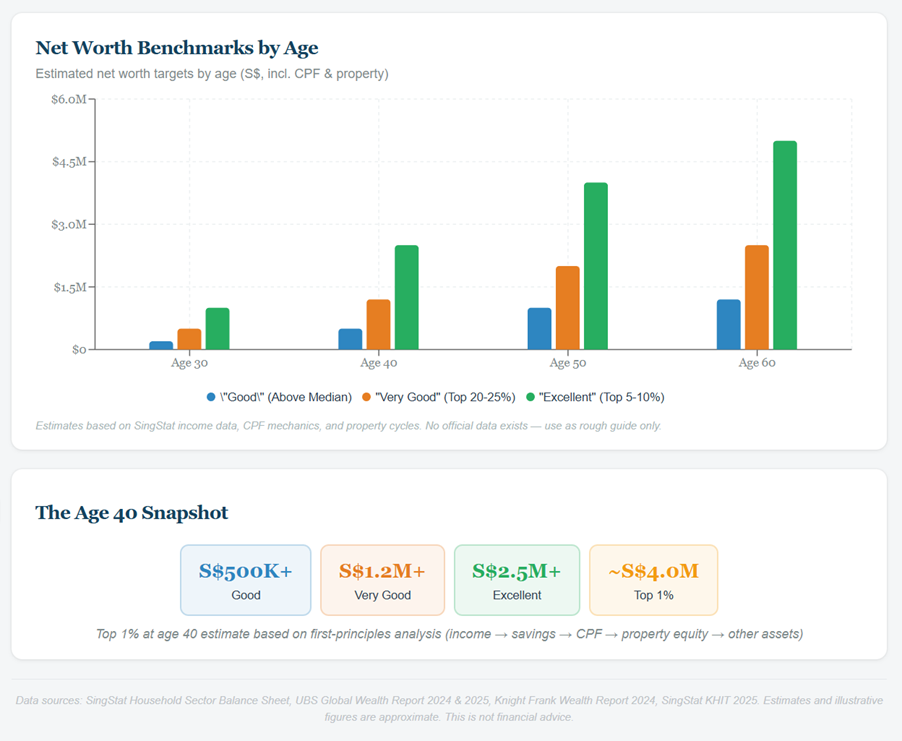

Net worth by age — what’s realistic?

Age matters a lot when thinking about net worth.

A 25-year-old fresh out of university will obviously have a very different net worth from a 55-year-old at their peak earning years.

While there’s no official breakdown, here’s a rough framework for where you “should” be, based on Singapore’s income data, CPF mechanics, and property cycles.

These are estimates for a single working adult, and I would stress these are very rough guides.

| Age | “Good” (above median) | “Very Good” (top 20-25%) | “Excellent” (top 5-10%) |

| 30 | S$200,000+ | S$500,000+ | S$1,000,000+ |

| 40 | S$500,000+ | S$1,200,000+ | S$2,500,000+ |

| 50 | S$1,000,000+ | S$2,000,000+ | S$4,000,000+ |

| 60 | S$1,200,000+ | S$2,500,000+ | S$5,000,000+ |

In your 20s (25-29):

At this stage you’re just starting out. If you’re earning the median salary of about S$4,160 per month (age 25-29 bracket), your net worth is probably dominated by CPF balances and whatever cash savings you have.

A “good” (and by good I mean above the median, not the top 1%) net worth at this stage is probably S$50,000 – S$100,000 including CPF.

Don’t stress if you’re below this. The compounding machine hasn’t kicked in yet.

In your 30s (30-39):

This is where things start to move. You’ve likely bought a home (HDB or condo), which adds property equity to the mix. CPF balances are building up.

A “good” net worth at this stage is probably S$300,000 – S$600,000 including CPF and property equity.

If you’re a dual income couple, then perhaps a combined household net worth of S$500,000 – S$1 million.

In your 40s (40-49):

Peak earning years for most. Property has appreciated, CPF is substantial, investments have had time to compound.

A “good” net worth at this stage is probably S$600,000 – S$1.5 million including CPF and property equity.

In your 50s and beyond (50-65):

By this stage, your net worth should be at or near its peak. Your property is likely fully or largely paid off, CPF balances are at their highest, and investments have had decades to compound.

A “good” net worth at this stage is probably S$1 million – S$2.5 million including CPF and property equity.

At this point, the focus shifts from accumulation to preservation and income generation.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

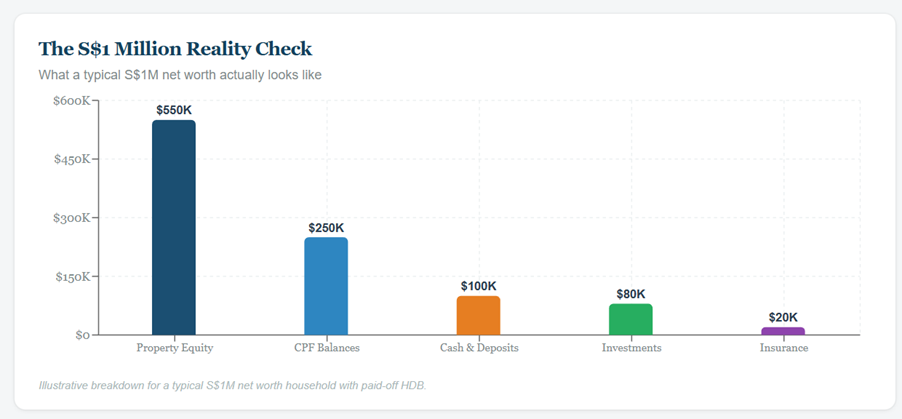

Is S$1 million still “enough” in Singapore?

This is the million dollar question (pun intended).

A decade ago, having S$1 million in net worth would have put you firmly in comfortable territory.

Today? I’m not so sure.

Here’s the problem.

If S$1 million is your total net worth, and S$500,000 – S$600,000 of that is locked up in property and CPF, you might only have S$400,000 – S$500,000 in liquid investable assets.

And that’s being generous — for many Singaporeans, the illiquid portion is even higher.

At a 4% withdrawal rate, S$200,000 in liquid assets gives you about S$8,000 a year in passive income from investments.

Throw in CPF LIFE payouts (estimated S$1,780/month at the FRS for those turning 55 in 2026), and you’re looking at total retirement income of about S$3,100 – S$3,500/month.

That’s… okay for basic expenses in Singapore, especially if your home is paid off.

But it doesn’t leave a lot of room for healthcare costs, travel, or unexpected expenses.

The elephant in the room — property distorts everything

If you’ve been reading carefully, you’ll notice that property is 41% of total household wealth in Singapore.

This creates a really interesting dynamic.

An HDB owner in a mature estate might have a flat worth S$600,000 – S$800,000, which alone puts their household close to the median net worth.

A private property owner in the CCR could be sitting on S$2 – S$3 million in property equity.

On paper, these are wealthy households.

But in reality — can you monetise that wealth?

If it’s your only home, not really. You still need somewhere to live.

This is why I think net worth benchmarks in Singapore need to be taken with a grain of salt.

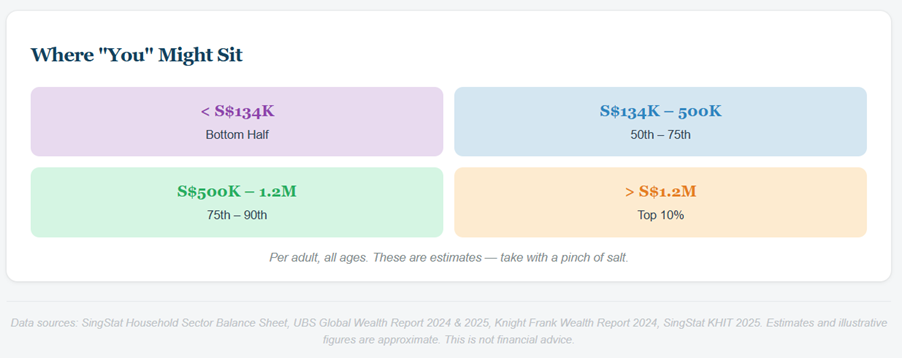

Liquid net worth (cash, investments, CPF — excluding your primary residence) is arguably a much better indicator of your actual financial position.

If your liquid net worth (excluding primary residence) is:

- Below S$100,000: You probably need to focus on building up savings and investments.

- S$100,000 – S$300,000: You’re building a foundation, but not yet financially secure.

- S$300,000 – S$800,000: You’re in a good position, especially with CPF as a backstop.

- S$800,000 – S$2 million: You’re doing very well — this gives you real optionality.

- Above S$2 million: You’re in genuine high-net-worth territory with significant financial freedom.

Closing Thoughts — What is a “good” net worth in Singapore?

So… what is a good net worth in Singapore?

Based on all the data above, here’s my attempt at a simple framework.

By total net worth (including CPF and property):

| Age | “Good” (above median) | “Very Good” (top 20-25%) | “Excellent” (top 5-10%) |

| 30 | S$200,000+ | S$500,000+ | S$1,000,000+ |

| 40 | S$500,000+ | S$1,200,000+ | S$2,500,000+ |

| 50 | S$1,000,000+ | S$2,000,000+ | S$4,000,000+ |

| 60 | S$1,200,000+ | S$2,500,000+ | S$5,000,000+ |

Important caveats:

- These are very rough estimates. There is no official data on net worth percentiles by age in Singapore.

- These include CPF and property equity, which are largely illiquid. Your liquid net worth matters more for actual financial freedom.

- These are per-person numbers. A dual income household would typically have higher combined net worth.

At the end of the day, “good” is relative.

Relative to your age, your income, your goals, and your lifestyle.

If you’re on a path where your net worth is growing year on year, and you’re building towards financial security, you’re doing well.

Don’t let the headlines about average household net worth being S$2 million make you feel inadequate. That number is massively skewed by the ultra-wealthy, and half of it is in illiquid property anyway.

Focus on what you can control — earn more, spend wisely, invest consistently, and let time do the rest.

As always, love to hear what you think!

Where do you stand on the net worth benchmarks, and do you think these numbers are realistic?

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi

Your data sources are not sufficient. You should refer to MOF’s recent paper – Occasional Paper on Income Growth, Inequality, and Social Mobility Trends in Singapore -> Table B1. Source: https://www.mof.gov.sg/news-resources/newsroom/occasional-paper-on-income-growth–inequality–and-social-mobility-trends-in-singapore/

Table B1 shows ‘Average household wealth among resident households, 2023’. On average, resident households have $1.755m in net wealth. Middle 20% households have ~$1m net wealth, while top 20% have ~$5.26m.

Thank you – appreciate this!