Okay so just 2 – 3 months ago, I wrote an article on UOB Bank.

And my conclusion there was that I would not buy UOB, because their business is significantly underperforming DBS and OCBC Bank.

And then literally just 1 – 2 weeks later, I completely changed my mind and I bought a position in UOB Bank.

And I added to UOB bank again recently.

A lot of you have asked for my views on UOB, and whether it is a good “value” buy relative to DBS and OCBC bank which are both at all time highs.

So I figured this was a good time to discuss my latest views on UOB.

Why I decided not to buy UOB Bank a few months back?

From my article on UOB Bank in early Nov 2025:

After doing the research, I have mixed thoughts.

Looking at the numbers above, I really struggle to say that UOB bank is “cheap” even after the sell-off.

Yes share price is down 13% from highs when OCBC and DBS are at all time highs.

But frankly the business performance is just not as good as OCBC and DBS, and this looks to be a structural issue as it has been the case for years (UOB underperforming OCBC and DBS).

And the recent $0.6 billion allowance could be nothing, but it could also be a warning that UOB knows something we don’t.

If you look at the chart, the share price is trending down and below key moving averages, and it doesn’t look pretty.

The only saving grace is that you could argue there is support at $33, which could be a point to add for long term investors.

And then I bought UOB Bank stock a week after…

And of course as fate would have it.

After writing the article, somehow something clicked for me.

And a week after that I changed my mind on UOB.

And I decided to buy a position.

3 big reasons for me:

- Technicals started to improve for UOB Bank

- I changed my mind on UOB’s asset quality… for the time being

- UOB is much cheaper than OCBC and DBS – to some extent this may be “priced in”

Technicals started to improve for UOB Bank

In the original article I said that $33 was a key support level for UOB Bank, and if that support held I could change my mind on UOB.

Well after the article, I noticed that price started to stabilise around low $33, and volume started to pick up.

This was a big bullish sign for me – that made me take a second look.

And since then price action has continued to be bullish, with UOB bank making higher highs and breaking key moving averages.

Further confirming my view.

I changed my mind on UOB’s asset quality… for the time being

But I don’t make investing decisions purely on technical analysis.

I find that the best investment decisions (which to be clear I am not saying UOB is one as you can only judge with hindsight).

But I find the best stocks are when the technical analysis is bullish, AND the fundamental analysis checks out.

In my original article, I shared that a big reason why UOB stock has been underperforming in 2025 is because of their large exposure to Hong Kong real estate.

Hong Kong real estate prices have been terrible the past few years, and UOB bank is likely underwater on some of these loans.

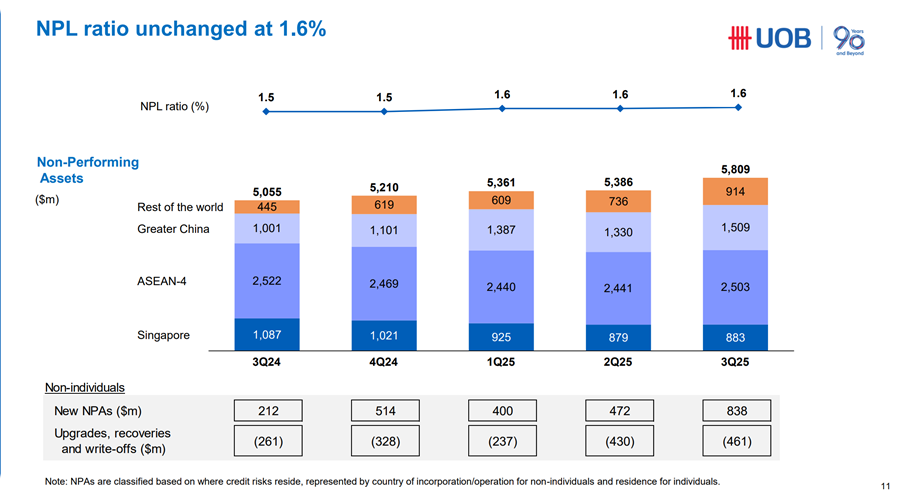

Which eventually led to them booking a $600 million pre-emptive loan loss provision in the last quarter which spooked investors.

Now what changed for me?

I got Gemini to crunch some numbers for me.

This was the analysis:

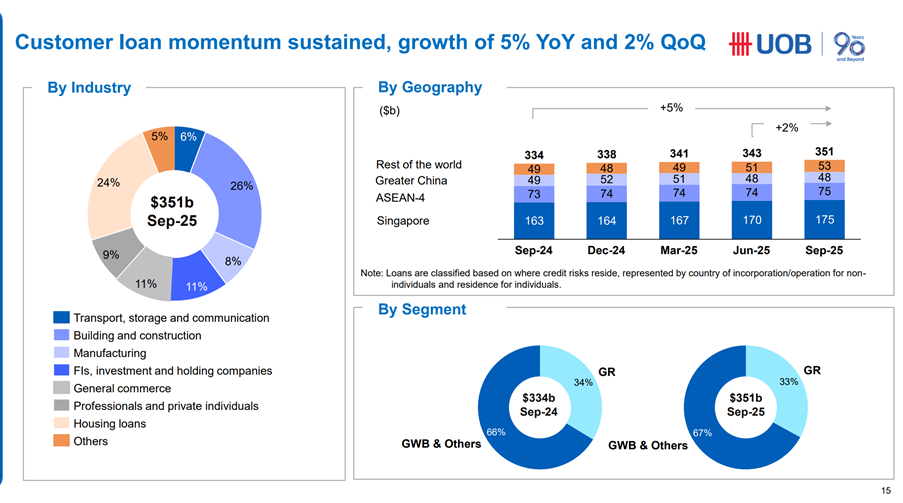

UOB has the highest relative exposure to the Greater China real estate sector among the three local banks.

While the SGD 0.6 billion allowance is technically sufficient to cover current non-performing assets (bringing coverage to >100%), the market remains skeptical.

The “sufficiency” is precarious because it relies heavily on the value of collateral (mostly Hong Kong property), which is currently seeing price declines of ~50% in some segments (like offices).

The 0.6 billion allowance is likely a “floor” rather than a complete shield.

It effectively buffers the bank against the current level of stress, ensuring dividends and capital ratios remain intact for now. However, if Hong Kong commercial property values drop another 10-15% in 2026, UOB will likely be forced to top up these provisions, further dragging on earnings growth compared to DBS and OCBC.

You can see from the chart above that UOB has $48 billion exposure to Greater China.

So if things go bad, there’s a lot of room for things to head south, and a $600 million loan loss provision is probably nothing just like Gemini said.

BUT – assuming no major deterioration in the HK real estate market.

Then actually a $600 million loan loss *could* tide UOB bank through for most of 2026.

In which case if the bad news dies down, then because UOB is so much cheaper than DBS and OCBC bank.

There could be value in a turnaround play.

Where the bad news is already priced in, and as long as things are not as bad as what is priced in, there is upside.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

UOB is much cheaper than OCBC and DBS – to some extent this may be “priced in”

Which brings me to my next point.

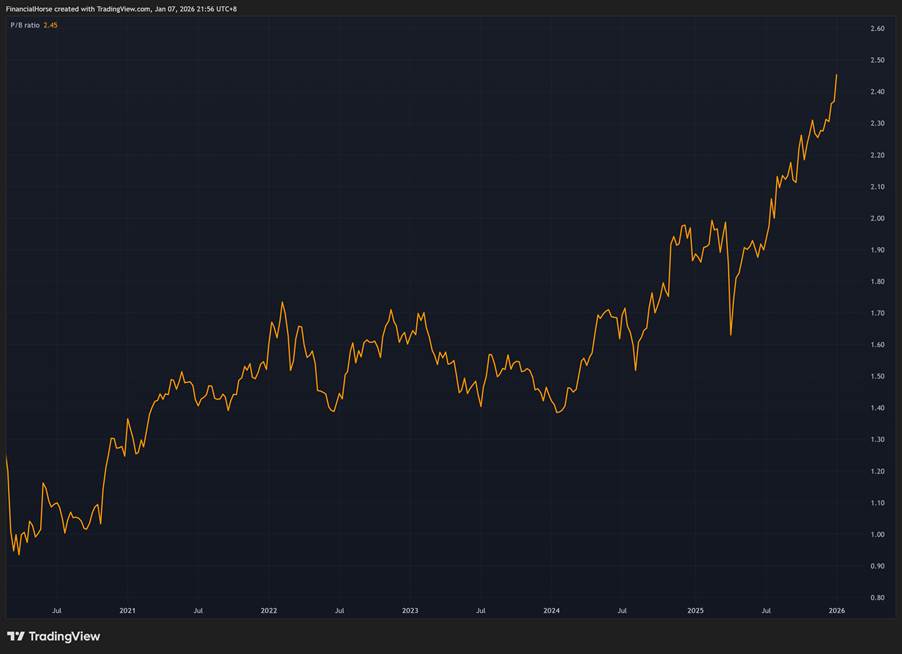

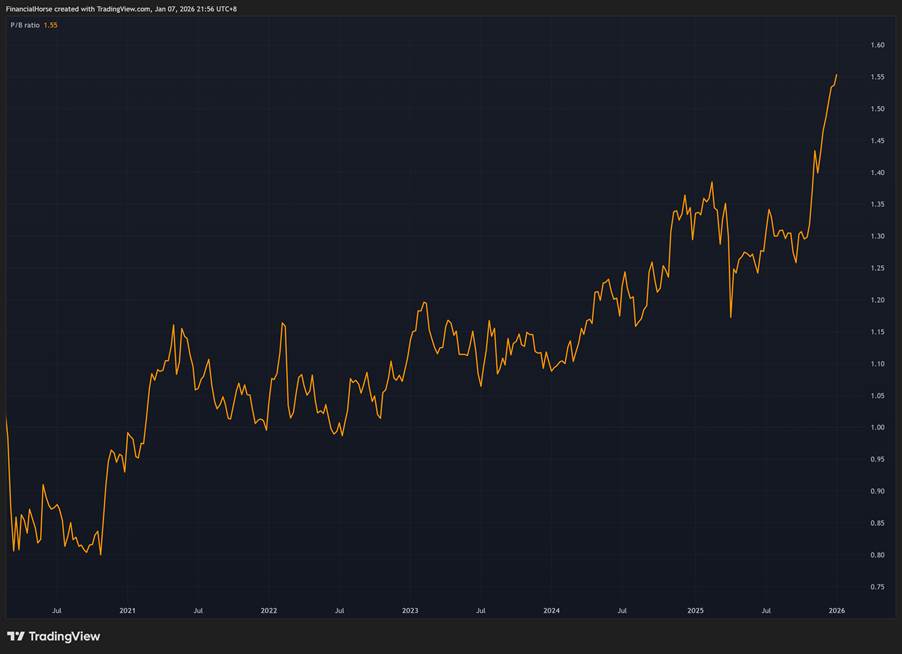

From a pure price to book perspective, UOB is the cheapest of the 3 banks.

You can see this visualized below.

Here is UOB Bank’s Price to Book:

Here’s DBS bank:

And OCBC bank:

You can see how both OCBC and DBS are soaring to new highs in terms of Price/Book. Whereas UOB is rangebound.

I’ve compared the valuations of UOB Bank vs DBS and OCBC bank below.

| Metric | DBS (D05) | OCBC (O39) | UOB (U11) |

| Share Price | ~S$58.40 | ~S$19.00 | ~S$36.00 |

| P/B Ratio | 2.2x | 1.6x | 1.2x |

| Base Dividend | S$2.64 | ~S$0.90 | ~S$1.70 |

| Special/Capital Return | + S$0.60 (Committed Quarterly) | + ~S$0.18 (Committed 10% of Profit) | + ~S$0.50 (At Risk due to Provisions) |

| Total Est. Dividend | S$3.24 | ~S$1.08 | ~S$1.70 – S$2.20 |

| Net Dividend Yield (estimated) | 5.55% | 5.4% | 4.7% – 6.1% (depending on special dividend) |

From a dividend perspective, there is significant uncertainty because you don’t know whether management will continue to pay the special dividend, or skip it to conserve cash.

If the special dividend continues you’re looking at almost 6.1% yield.

If not it drops to 4.7% yield which is below that of DBS and OCBC – in which case the stock probably goes even lower.

So there is a fair bit of uncertainty here.

Yes UOB is cheap, but it is cheap for a reason.

The question is whether there is attractive risk reward.

Macro views on Singapore bank stocks in 2026?

This was what I wrote for FH Premium subscribers this week (on what asset classes I may overweight in 2026):

Would I overweight banks in 2026?

You know what – unlike the other asset classes above, I think you could make a good argument to overweight banks in 2026.

Especially if you don’t want to stock pick or actively manage your portfolio too much.

But that said at these prices I don’t find the risk-reward for bank stocks asymmetric anymore.

You’re probably risking $1.5 to make $1 at these prices.

Base case bank stocks probably still do decently well in 2026 without too much headache, but nobody can rule out a tail risk event where banks stocks drop 20-30%. That’s the risk you have to take.

So banks are for me at best equal weight, but I can get why certain investors would overweight banks.

Why I bought more UOB Bank stock at 6% dividend yield?

So… putting all of the above together.

Why did I buy UOB Bank stock?

Well, I also own a lot of OCBC Bank stock, and with OCBC Bank soaring to all time highs and at a 1.56x book, I really didn’t want to buy more OCBC bank at these prices.

With UOB Bank.

I think the biggest point for me was the technicals showing increasing volume at low 33.

That to me was the sign that suggested investors are looking through the $600 million loan loss provision, and accumulating positions at low 33.

So I bought a speculative position at low $33.

And then when it broke above the 200 day moving average I added again.

I shared my fundamental and macro analysis above – on how if things don’t continue to deteriorate I think the share price will do well.

Do I know if the Hong Kong real estate situation will continue to deteriorate?

Frankly no idea.

But the way I see it, the amount I lose if things deteriorate, is probably less than the amount I make if things don’t.

And with technical analysis confirming – I decided to buy UOB Bank.

And you can see my full portfolio and stock watch on FH Premium.

I would love to hear what you think though!

Would you buy UOB Bank today? Or stick to OCBC and DBS Bank instead?

If you enjoy articles like this, do support Financial Horse on FH Premium and get access to premium articles like this, including my stock watch and investment portfolio.

Hi, not sure if you are aware of the management style and more importantly culture at UOB, and how it compares to DBS and OCBC. Technical analysis and even analysing financials and business decisions are one thing, but nothing will change if the former is not fixed. My take is that UOB is closer to some other neighbouring countries’ local banks (all due respect) than it is to DBS, OCBC and global banks. The gap with the other 2 will continue to widen. Expect more issues like consumer complaints, taking on bad loans without assessing risk, lagging behind in tech, etc. But honestly, don’t know how to price this in as an appropriate haircut to the stock price/growth, apart from not touching it entirely.

That’s a very good point. Appreciate the share.

In 2022, the main talking point for UOB share price was the $5 billion acquisition of Citigroup’s Southeast Asia consumer business. I had predicted that the acquisition might push UOB share price to another league, namely above $30, which it did. However, despite the tailwinds from the Citigroup acquisition and the interest rate hikes, UOB share price did not sustain the bullish momentum and dipped to $27 to $28 bandwidth for the large part of 2023.

Hi there,

I have written an article on UOB in 2025.

https://sgwealthbuilder.com/2025/05/15/uob-share-price-on-the-brink/

The key in UOB’s growth lies in unlocking Citigroup acquisition.

Yeah I agree with the take on Citi. Do you think UOB can do it? M&A synergies are notoriously hard to realise.