In last week’s article, I wrote about how I may invest in 2026, and I shared that I may underweight REITs in 2026.

This garnered a lot of questions from readers – on why I would underweight REITs in a climate where interest rates are dropping.

Now the short answer, is that while I think short term interest rates stay low, I think long term interest rates may creep up in 2026.

And while short term interest rates stay low, I think they may have bottomed for now.

We see some of this reflected in the 10 year interest rate, which has gone from 1.7% in Nov to 2.2% today.

And if I am right on this – it means that REIT prices could trade sideways for most of 2026, and the return comes only from the dividend yield.

But that said, the fact that so many of you think REITs are a good buy in 2026 led me to rethink my assumptions.

So I wanted to do a deeper analysis.

How much REITS do I hold in my portfolio today

A bit of context to set the tone.

In 2025, I was overweight REITs, as I believed that lower interest rates would benefit REIT prices.

This turned out to be a good call, because my REIT portfolio returned >20% in 2025 (including dividends).

For what is primarily a yield instrument, I was very pleased with those returns.

But that’s all last year now.

Do I want to continue to overweight REITs in 2026?

Will REITS benefit from lower interest rates?

I asked Gemini how do REITs perform if the scenario I envisage plays out – short term rates stay low, but long term rates go up.

This was the answer:

If the yield curve steepens (short-term rates drop, long-term rates rise), you must Underweight S-REITs. This specific scenario creates a “Value Trap” for most REITs: they suffer the valuation hit from rising long rates but fail to capture the immediate cashflow benefits of falling short rates because most have locked in high fixed-rate debt (75%–85% hedged).

That said, I didn’t think this was a very good answer as there is a lot of nuance that wasn’t captured.

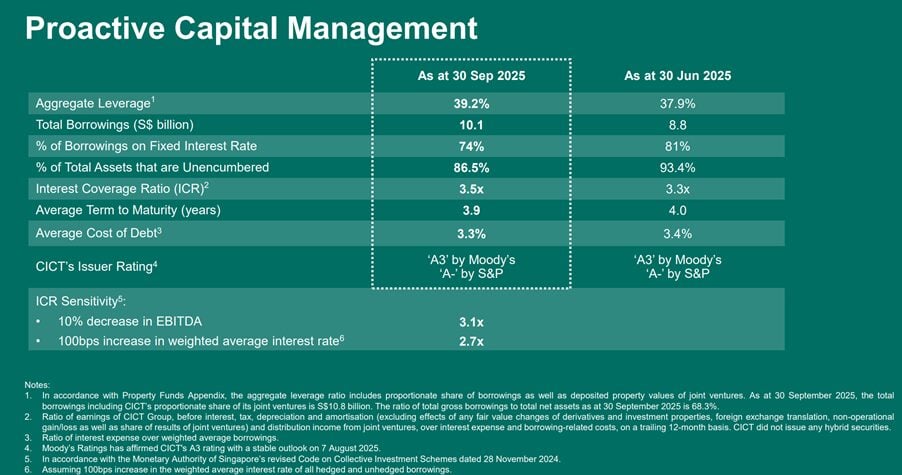

Let’s use CICT as an example.

CICT borrows with an average 3.9 years term to maturity, of which 74% of that is fixed debt.

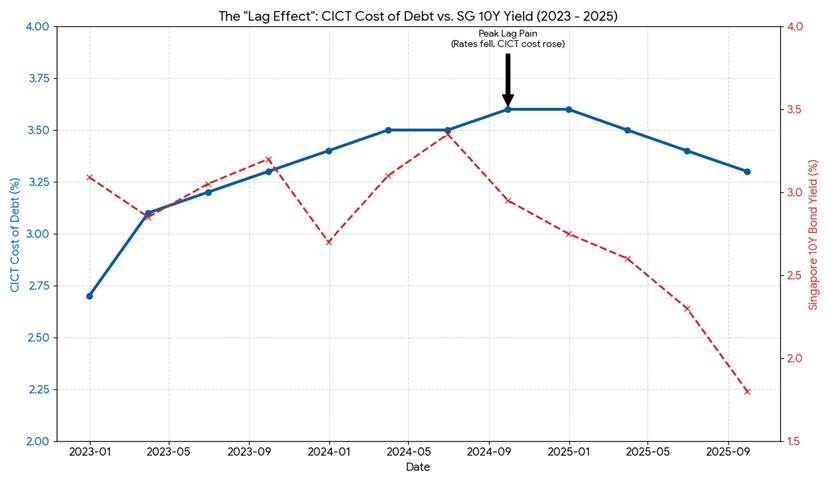

This means that when interest rates drop, there is a lagged effect.

Visualised below – you can see how even though long term interest rates (red) fell sharply from mid 2024, CICT’s weighted cost of debt continued to rise.

And only started to fall in 2025, and even then the drop was not as much as the drop in the 10 year interest rate.

How much will average cost of debt for REITs drop?

Based on the current trajectory, the estimated “Theoretical Floor” for CICT’s average cost of debt is 2.8% – 2.9%.

It is highly unlikely to return to the historic lows of 2.4% (seen in 2021) because the “Zero Interest Rate” era is over.

Even with SORA falling to ~1.3%, credit spreads and term premiums keep the all-in cost of new 5-year debt closer to 3.0%.

To hit this floor, CICT needs to replace its expensive 2023-2024 debt (issued at ~4.0%) with new debt.

Here is the approximate for new debt in early 2026:

| Component | Rate (Est. Jan 2026) | Notes |

| Base Rate (SORA/Swap) | ~1.8% | 5-Year Swap Rate (Assuming SORA is ~1.3%). |

| Credit Spread | +1.0% | The “Risk Premium” for A-rated REITs remains sticky. |

| Amortization/Fees | +0.1% | Upfront fees amortized over the loan life. |

| Cost of New Debt | ~2.9% | This is the marginal cost. |

How long will it take for REITs reach 2.9% cost of debt?

And because CICT holds a lot of fixed debt that is termed out, this leads to the lag effect that we described above.

In plain English – REITs need time to refinance the debt to benefit from lower interest rates

Running some simple numbers, assuming interest rates stay low, we’ll probably only see REITs’ average cost of debt drop to 2.9% in 2027:

| Year | Est. Cost of Debt | Trend |

| 2025 (Actual) | 3.3% | Peaked and turned. |

| 2026 (Forecast) | 3.1% | Improving as 4% hedges burn off. |

| 2027 (Forecast) | 2.9% | The Floor. Hitting the structural limit. |

BUT – and this is my key point.

CICT’s share price has already gone from 1.9 to 2.39.

A whopping 25% increase in share price last year.

Which leads to the question – has the market already fully priced in lower interest rates for REITs?

BUT has the market already priced this in for REITs?

I got Gemini to crunch the numbers for me:

The market has already priced in about 80–90% of this good news. CICT is currently trading at a “Victory Valuation” that assumes the cost of debt will smoothly fall.

At a price of ~$2.38 (Jan 1, 2026 levels) and a forward yield of ~4.7%, investors have already bid up the price in anticipation of the lower interest rates.

1. The “Priced In” Evidence (The 4.7% Trap)

The market is no longer pricing CICT as a “distressed” REIT; it is pricing it as a “blue-chip bond proxy” again.

| Metric | Current Level (Jan 2026) | Historical/Fair Value | Verdict |

| Dividend Yield | 4.7% – 4.8% | 5.2% (10-Year Avg) | Rich. Investors are accepting a lower yield today because they expect DPU growth tomorrow. |

| Price-to-Book (P/B) | ~1.1x | 0.95x – 1.0x | Premium. You are paying a 10% premium over the value of its properties. |

| Cost of Debt Expectation | 3.1% – 3.3% | 2.9% (Your Bull Case) | Partially Priced. The market expects ~3.2%. A drop to 2.9% is a mild “upside surprise,” not a game changer. |

Okay, you can dispute some of the exact numbers and assumptions used.

But big picture wise, I agree with Gemini.

I would say REITs at today price, they already price in a good chunk of the interest rate drop.

For further capital gains upside from here, you need to see interest rates drop more than expected.

Which frankly I am not sure we will see.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Do I Buy REITS for income or for capital gains?

This actually brings me to my next point.

Do you buy REITs for income, or do you buy REITs for capital gains?

If it’s yield – then I say actually REITs will likely continue to deliver.

The lower interest rates is a tailwind for refinancing, and as long as you buy REITs with strong properties the rental should hold up.

So you should see improving DPU going forward.

Which means for yield investors, I think REITs continue to fulfil that role.

If it’s capital gains though – then I think it gets more tricky.

Valuation is an art and not a science.

But gun to my head, I think at this price, the capital gains upside is limited.

Sure maybe you can eke out another 5% capital gains and 10% in a bull scenario.

But I think it’s highly unlikely we repeat the 2025 performance for REITs, unless interest rates go back to zero.

So it depends on what your goal is.

If you have a huge portfolio and a 5% yield is more than enough to meet all your spending needs and more – then REITs still work.

If you’re in the phase of wealth building, then I would say having some REITs is okay, but there may be other assets worth considering.

Investment grade bonds as an alternative to REITs for yield?

At the same time.

Even if you are a yield investor today.

I think there is very strong competition from corporate bonds today.

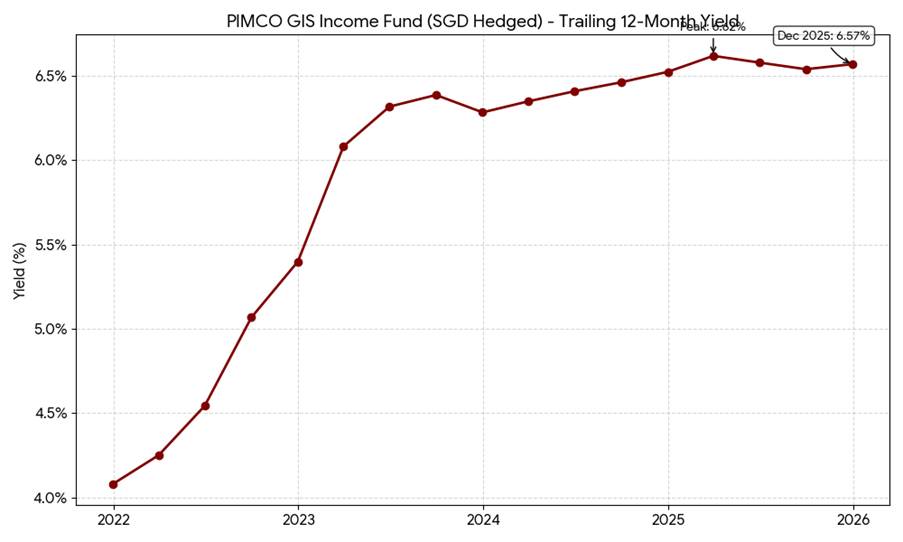

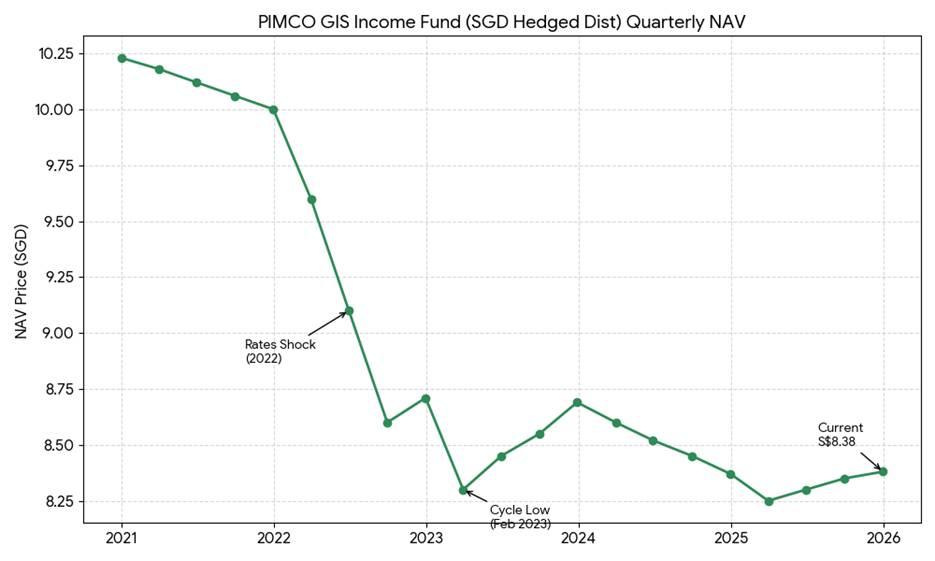

Let’s take PIMCO GIS Income fund as an example.

PIMCO GIS pays about 5.5% yield (after approx 1% fees), SGD hedged.

Compared to CICT which pays a 4.7% dividend yield today, actually PIMCO GIS Income fund is very competitive.

Just to be absolutely clear though – I am NOT saying that bonds are a “safer” investment than REITs.

PIMCO GIS Income Fund price plotted below, you can see how the share price fell almost 20% in 2021 to 2023 with rising interest rates.

So bonds are not risk free.

There is risk of capital loss, and there is also default risk.

But in this climate – I think they are a useful diversifier for a yield investor, and you no longer need to put all your eggs into REITs (which was the case in the 2010s decade).

In other words – REITs today have more competition, especially from bonds.

Why I may buy less REITs in 2026?

Coming back to the original question.

I am overweight REITs in my portfolio today, and I expect to continue owning REITs in 2026.

The question is more of position sizing – how much REITs do I own?

If I am right, then base case I think REIT prices go sideways for a while.

And the returns come largely from the yield.

That’s about 5% from a blue chip REIT like CICT or Ascendas REIT.

If you’re comfortable with that 5% yield, that’s absolutely fine to overweight.

But for me, I think I want to be a bit more aggressive with my portfolio.

And given that with REITs the easy money has already been made.

I may keep REITs positioning to equal or underweight in 2026.

And deploy some of that cash to assets with more potential for growth – stocks, bitcoin etc.

You can see my full stock watchlist on what I am keen to buy on FH Premium.

Love to hear what you think though!

Will you overweight or underweight REITs in 2026?

If you enjoy articles like this, do support Financial Horse on FH premium and get access to premium articles like this, including my stock watch and investment portfolio.

Hi FH,

Thank you for the kind sharing.

I am not an expert on bonds, but with my limited knowledge, I noticed there are several red flags with respect to Pimco.

All the long-term treasury yields are up

The 10-year German yield is up

The 10-year japan yield is up

10-year US yield been flat but staying above 4.00%

10-year SG yield been going up

If these continue to move up in 2026, PIMCO GIS Income fund will likely suffer more capital loss.

On top on that, the yield is fake because one third or more of the dividend yield comes from their cash holding or new investor money. You can see the all these from their excel sheet which they need to declare.

Referring to their excel sheet

in June 2017, they started paying out of capital every month.

At that time, the dividend payout was $0.03403/mth

They increased the dividend payout amount twice to the current payout of $0.4547/mth

Yeah I agree. Which is why I said PIMCO is not risk free. It’s like REITs in that if long rates go up you will see capital losses. And if there are default you will also see losses.

Precious metals stole the limelight in 2025 as gold staged an incredible rally not seen before. The breath-taking form of gold certainly caught many investors by surprise, with many of them lamenting that they have missed the boat. For perspective, gold price surged from US$2,624 per troy ounce in January 2025 to US$4,315 per troy ounce by end of 2025, an increase of 64%. Despite the crazy gold prices, investors are still flocking to buy bullion. Based on BullionStar’s website, there is an “unprecedented demand for bullion in Singapore”.

According to BullionStar, October 2025 was a historic month for them as buy transactions surpassed 12,000 and total sales reached over S$250 million. The buy-to-sell ratio remained strongly in buyers’ favour at 2:1, while the average order value climbed 8%, from S$18,754 in September to S$20,287.89 in October. Given the galloping surge in gold prices in November and December 2025, I am not surprise that the buying momentum for bullion continued towards the end of the year.

Hi Gerald curious to hear your thoughts – do you think think Gold will continue to do well in 2026?