So I was at the REITs Symposium about a week or two back.

And you know what?

You wouldn’t be able to tell from the REITs share price.

But the REITs Symposium was actually pretty packed, with a lot of investors seemingly keen to understand more about REITs.

Now that really got me thinking.

You can buy a decent, blue-chip REIT with Singapore assets at about 5.5 – 7% dividend yield today.

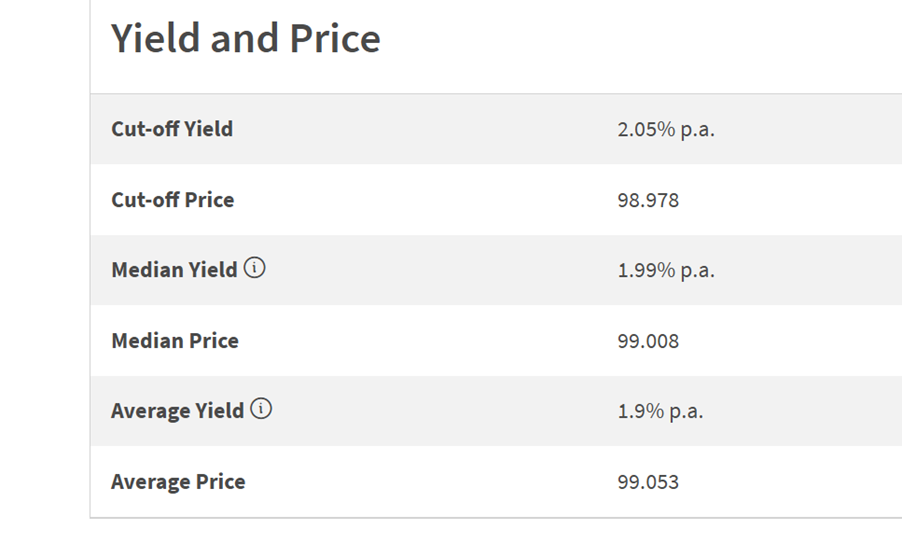

With the latest T-Bills interest rate falling to 2.05%.

Does that make REITs a good buy?

The exact split – that goes back to risk appetite.

But hey that’s just me, and you can see my full portfolio breakdown on FH Premium.

Love to hear what you think! Would you buy DBS Bank at 6.7% dividend yield?

This is an FH Premium post.

I am making this available to all readers to keep you updated on my latest thinking given the current market volatility.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Risks with REITs

Let’s start with the risk with REITs.

2 big ones in my view:

- Higher Interest Rates will hit REIT prices

- Weak Real Estate performance (especially if overseas / China)

Higher Interest Rates will hit REIT prices

Realistically whatever way you spin it.

The Trump administration doesn’t look like they are going to make a meaningful dent in the US budget deficit in the medium term.

This means that medium term, the risk here is for higher long term interest rates.

REIT prices tend to be inversely correlated with long term interest rates (price drops when interest rates go up), so that is not good news.

BUT – Singapore long term yields have been going down?

That being said, here’s the chart for the Singapore 10-year government bond yield.

See the sharp contrast with US 10-year yields above?

Because of a flight to safety (SGD is perceived as a safe haven / neutral currency).

Singapore long term yields have actually been going down – sitting at 2.3% today.

You can get 5.2% dividend yield on a blue chip REIT like CICT today.

That works out to be about a 3.0% yield spread – frankly not too shabby.

Of course, you could argue that on the flip side if interest rates pick back up, there is downside risk for the REITs.

That is a fair point, so it goes back to valuations, what is priced in, and what is the margin of safety.

Follow Financial Horse to avoid missing any post!

Weak Real Estate performance (especially if overseas / China)

The next risk – is that in this new geopolitical paradigm, you need to be quite careful about what kind of real estate you are buying.

Real estate in Singapore, China, US, Europe, are very different.

And that’s even before going into malls, offices, data centres in each market.

Long story short – real estate is not created equal.

Here’s CapitaLand China Trust’s share price for example – because of the weak performance of China real estate, share price performance has not been pretty.

Here’s IREIT Global, with European real estate exposure:

My view?

I don’t think you want to be too fancy in this climate.

I would stick primarily with Singapore real estate today.

Benefits of REITs

On the flipside, what are the benefits of REITs today?

2 key benefits in my view:

- Attractive dividend yields

- Capital gains potential?

Attractive dividend yields

As shared above, you can get 5.2% dividend yield on a blue-chip REIT like CICT today.

That works out to be about a 3.0% yield spread – decent enough for not a lot of risk.

If you’re okay with more risk you can get about 6% yield on a REIT like Ascendas REIT, or 7% yield on a REIT like Starhill Global REIT.

Capital gains potential?

As long as share price stays flat for the next few years, you’re already making a decent return on the dividend alone.

Of course, you could argue that on the flip side if interest rates pick back up, there is downside risk for the REITs.

Vice versa, if interest rates go down, there is upside capital gains potential for REITs.

That is a fair point, so it goes back to valuations, what is priced in, and what is the margin of safety.

Will I still buy REITs at 6% dividend yield?

Gun to my head.

I actually think the REITs are decently priced today.

No doubt I would stick primarily with blue chip REITs with a strong balance sheet / sponsor, and holding primarily Singapore real estate.

And of course I wouldn’t want my entire portfolio to be comprised of REITs, I would still want to throw in US stocks, Singapore stocks, Bitcoin / Gold and so on (see what I am keen to buy, and my full personal portfolio on the FH stock watch).

But assuming you do, I think there’s decent value in REITs today as a part of a Singapore investor’s portfolio.

The exact split – that goes back to risk appetite.

But hey that’s just me, and you can see my full portfolio breakdown on FH Premium.

Love to hear what you think! Would you buy DBS Bank at 6.7% dividend yield?

This is an FH Premium post.

I am making this available to all readers to keep you updated on my latest thinking given the current market volatility.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

Hi FH,

How would you compare NBNtrust viz a viz Sg focused reits like CICT or Capitaland ascendS reits? Would rise in interest rate drive down price of NBNtrust or it’s less sensitive to that?

In my view Netlink would be more sensitive to interest rates, as its a purer bond proxy (little room for DPU growth). This makes it more like a bond style product than a REIT (which can grow DPU if rents go up), and hence more sensitive to rates.