It’s been ages since my last article on T-Bills.

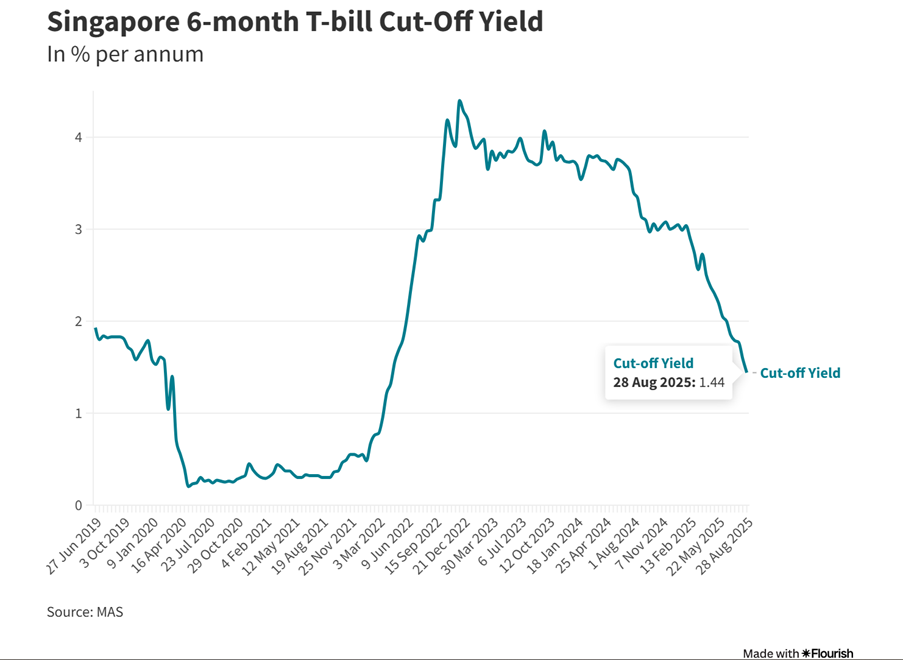

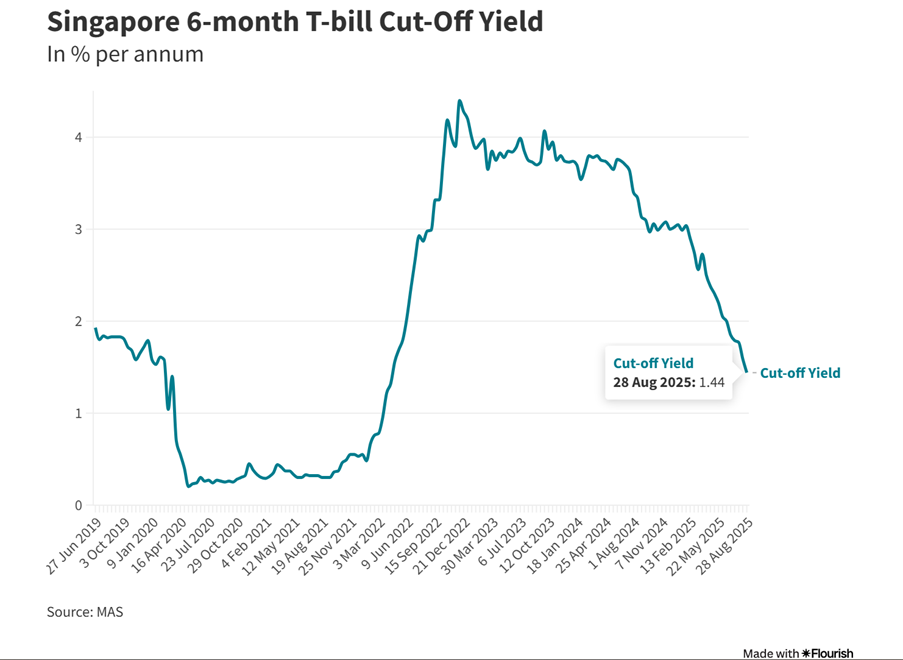

During which time, T-Bills yields have plunged to 1.44%, when it was close to 3.0% just earlier this year.

So I figured it was well overdue for an article discussing T-Bills and this sharp drop in yields.

3 questions I wanted to discuss:

- Will T-Bills yields keep dropping or go back up to 3.0%?

- What are the alternatives to T-Bills in this market? Fixed Deposit, Money Market Funds, Bonds?

- Will I buy more T-Bills today? Where to park cash for the highest yield today?

Estimated yield on the next 6-month T-Bills auction? (11 Sep 2025 Auction)

The next 6-month T-Bills auction is on 11 Sep 2025 (Thurs).

This means that the deadline to apply is:

- 9pm on 10 Sep (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 9 Sep (Tues) for UOB CPF-OA applications

6-month T-Bills yields dropped to 1.44% at the most recent auction

In the most recent 6-month T-Bills auction, cut-off yields fell to 1.44%.

You can see how yields were close to 3.0% earlier this year, so this has been a very sharp drop.

Most definitely not a good sign for investors looking for yield.

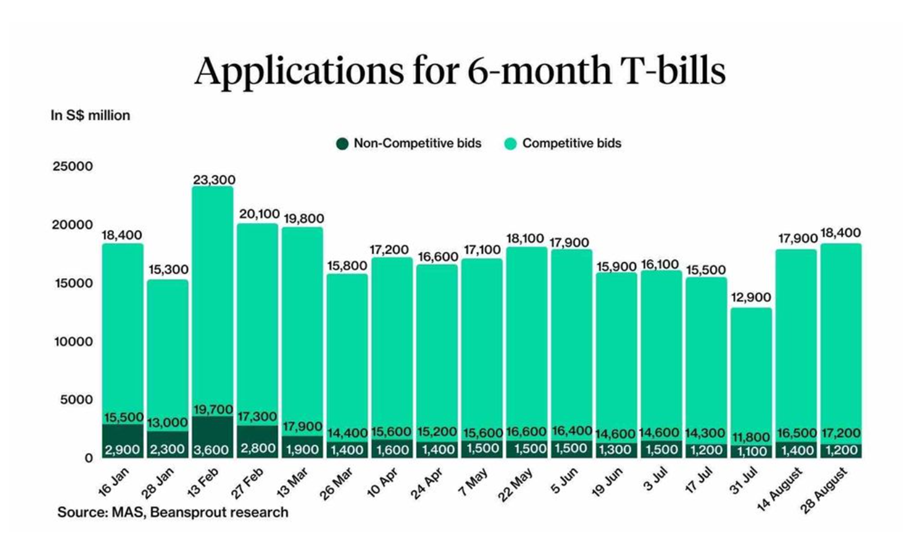

Demand for T-Bills remains very high at $18.4 billion

Whatever the case.

Demand for T-Bills continues to be very high despite the drop in yields.

We see $18.4 billion in demand for T-Bills, despite the drop in interest rates.

Will demand for T-Bills stay high, or will it drop?

A big wildcard is where demand will come in at the next T-Bills auction.

With the sharp drop in interest rates to 1.44% – will we still see strong demand, or will we see investors start to shift cash elsewhere?

Note that at 1.44% it no longer makes sense to park CPF-OA in T-Bills, as after accounting for lost interest you’ll lose money buying T-Bills with CPF-OA.

1.44% is also not that competitive compared to fixed deposits or money market funds, so it is possible that we may see demand for T-Bills drop going forward.

So far at least – that hasn’t really played out though.

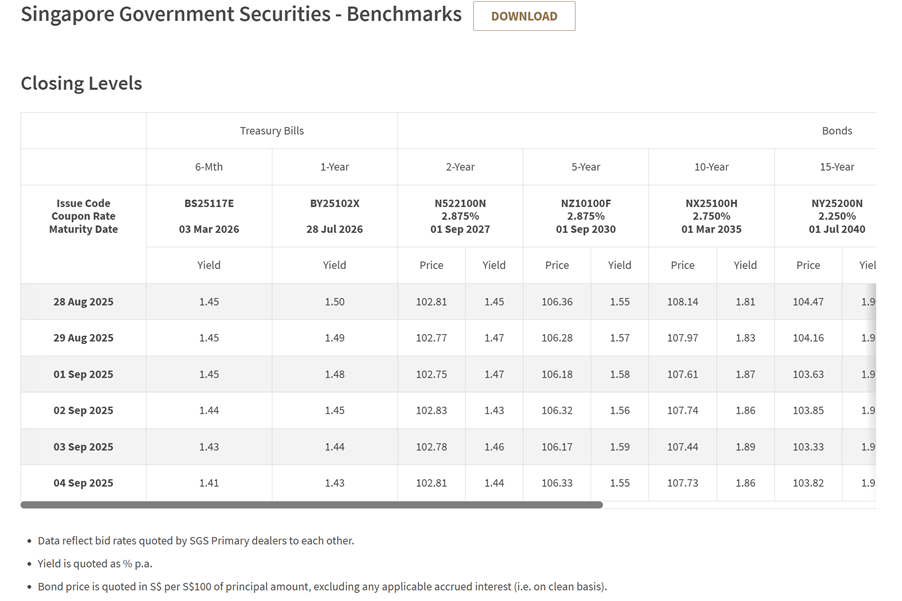

6-month T-Bills yields stable on the open market – trading at 1.41%

On the open market – 6-month T-Bills trade at 1.41%, slightly lower than the latest T-Bills auction yield.

Not a good sign, as this suggests potential downward pressure on yields.

That being said – trading liquidity on the T-Bills is so thin that actually the market pricing is not that useful.

So I would caution against placing too much reliance on market pricing on T-Bills.

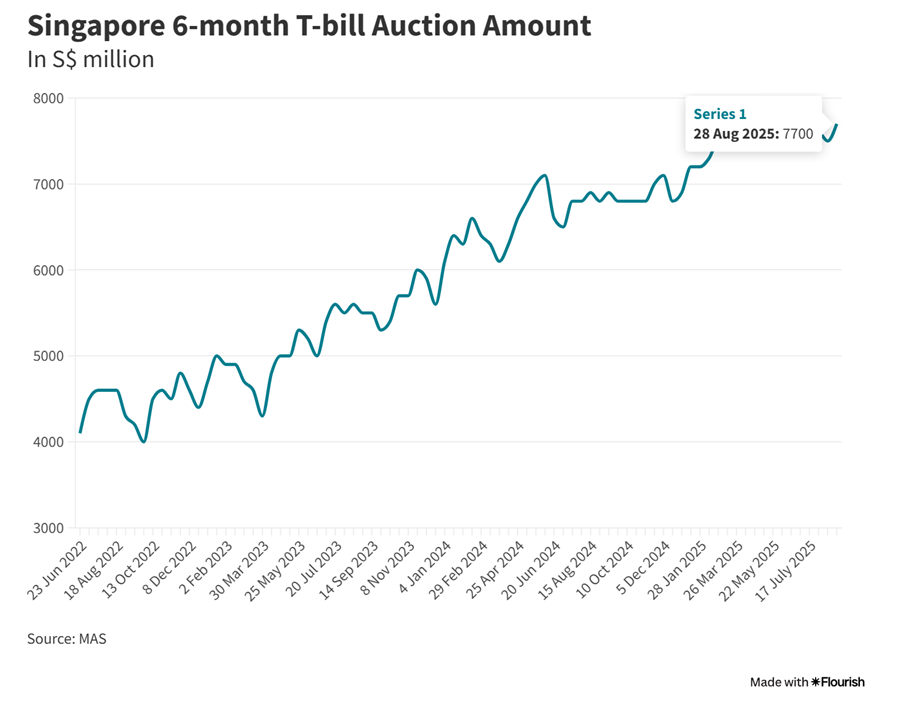

T-Bills Supply is up slightly to $7.8 billion (from $7.7 billion)

T-Bills supply is up slightly from the past few auctions.

That said the increase is miniscule – $7.8 billion vs $7.7 billion at the last auction.

Estimated yield of 1.40% – 1.50% on the 6-month T-Bills auction?

All things considered – I think T-Bills yields probably stabilise around the previous auction price, and market price.

I’m probably going with an estimated yield of 1.40% – 1.50% for the next 6-month T-Bills auction.

Probability analysis of the various outcomes below:

| Scenario | Cut-off Yield | Probability | Key drivers |

| Low | 1.30%–1.40% | 20% | Heavier non-comp flows; soft SGS 6-m benchmark (~1.40% or lower). |

| Base | 1.40%–1.50% | 60% | Benchmark ~1.40–1.45%; demand stays strong. |

| High | 1.50%–1.60% | 20% | Weaker demand; slight rebound in SGS short-end yields. |

What are the alternatives to T-Bills in this market? Fixed Deposit, Money Market Funds, Bonds?

I’ve tabulated the interest rates for the 3 cash options below, as well as with money market funds.

You can see how with the recent drop in T-Bills and institutional fixed deposit yields – actually retail fixed deposits are a pretty attractive option.

| 3 months | 6 months | 12 months | Risk Free | |

| T-Bills yields | NA | 1.44% | 1.54% | Yes |

| Fixed Deposit (direct to bank) | 1.65% | 1.60% | 1.60% | Yes (if below $100,000 SDIC limit) |

| Syfe Cash+ Guaranteed (Institutional Fixed Deposit Rates) | 1.45% | 1.40% | 1.30% | No |

| Money Market Funds | ~2.0% | No | ||

What are the alternatives to T-Bills and Fixed Deposit?

Let me outline the key alternatives to T-Bills and Fixed Deposits below.

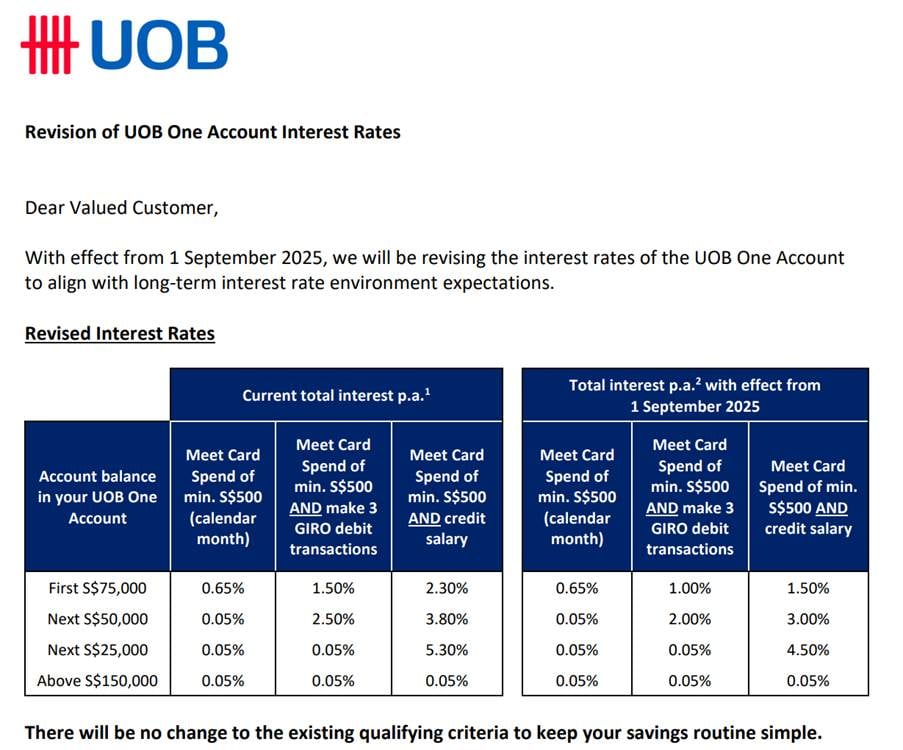

High Yield Savings Accounts – UOB One, DBS Multiplier, OCBC 360 etc

Interest rates for high yield savings accounts have been revised down of late.

UOB One has dropped interest rates (2.5% effective interest rate on $150,000)

UOB one has dropped their interest rates.

And these are the effective interest rates – 2.50% on $150,000, if you hit the criteria of $500 credit card spend and salary credit.

| Balance tier | New: spend $500 + salary | Effective Interest Rate (New) | Effective Interest Rate (Old) |

| First $75k | 1.50% | 1.50% | 2.30% |

| Next $50k | 3.00% | 2.10% | 2.86% |

| Next $25k | 4.50% | 2.50% | 3.21% |

| > $150k | 0.05% |

If you can fulfil the criteria without too much trouble.

I still think it’s worth it, as the 2.5% is still higher than other options like fixed deposits or T-Bills – as you can see above.

That said, if you find it too much of a hassle, or don’t want to put the full $150,000 in, then it probably doesn’t make sense.

And you’re better off with the other options on this list.

Money market fund instruments (like MariInvest)

Alternatively there is MariInvest which is a money market fund that pays about 2.2% over the past 30 days for me.

But given T-Bills are yielding 1.44%, I think money market funds are a pretty decent option right now, especially as you can get the money back any time with T+1 liquidity.

There is some investor discretion required here though, as unlike T-Bills, money market funds are not risk free.

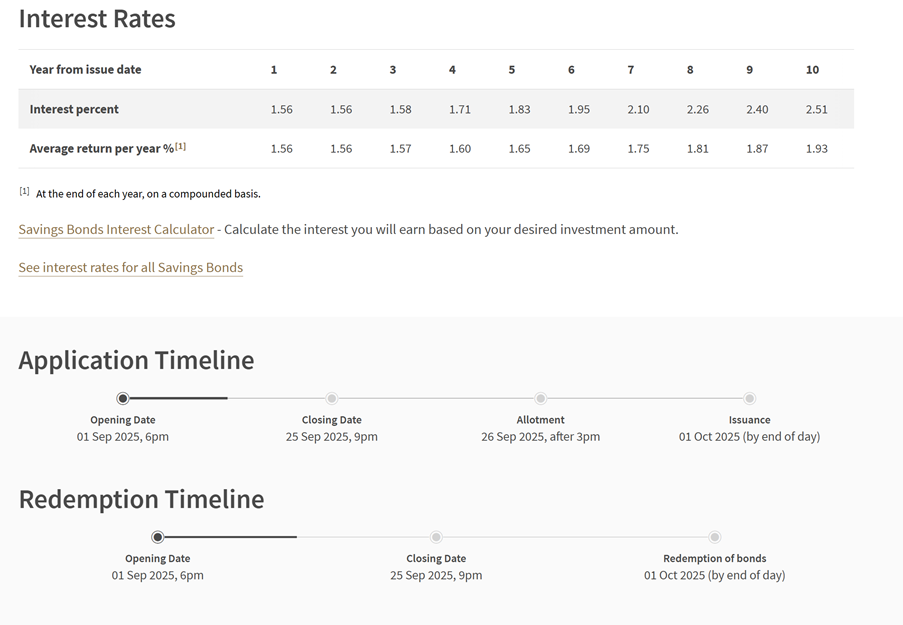

Singapore Savings Bonds are an acceptable alternative too

Interest rates on last month’s Singapore Savings Bonds below.

You’re looking at 1.56% for the first 3 years, stepping up to 1.93% over 10 years.

Funnily enough this is actually higher than T-Bills, and definitely worth checking out.

What about REITS or Bonds?

I wrote an article for FH Premium subscribers recently.

Long story short – I think REITs are a pretty decent buy today, especially with the sharp drop in interest rates.

A blue-chip REITs like CICT today pays about 5.5% dividend yield.

This was a lot less sexy when you could get 3% on a T-Bill (2.5% yield spread).

But when a T-Bill is sub 1.5%, you’re getting a whopping 4% spread vs a T-Bill.

I added to my REITs positions recently, and I think they’re worth considering if you’re happy to take on some risk.

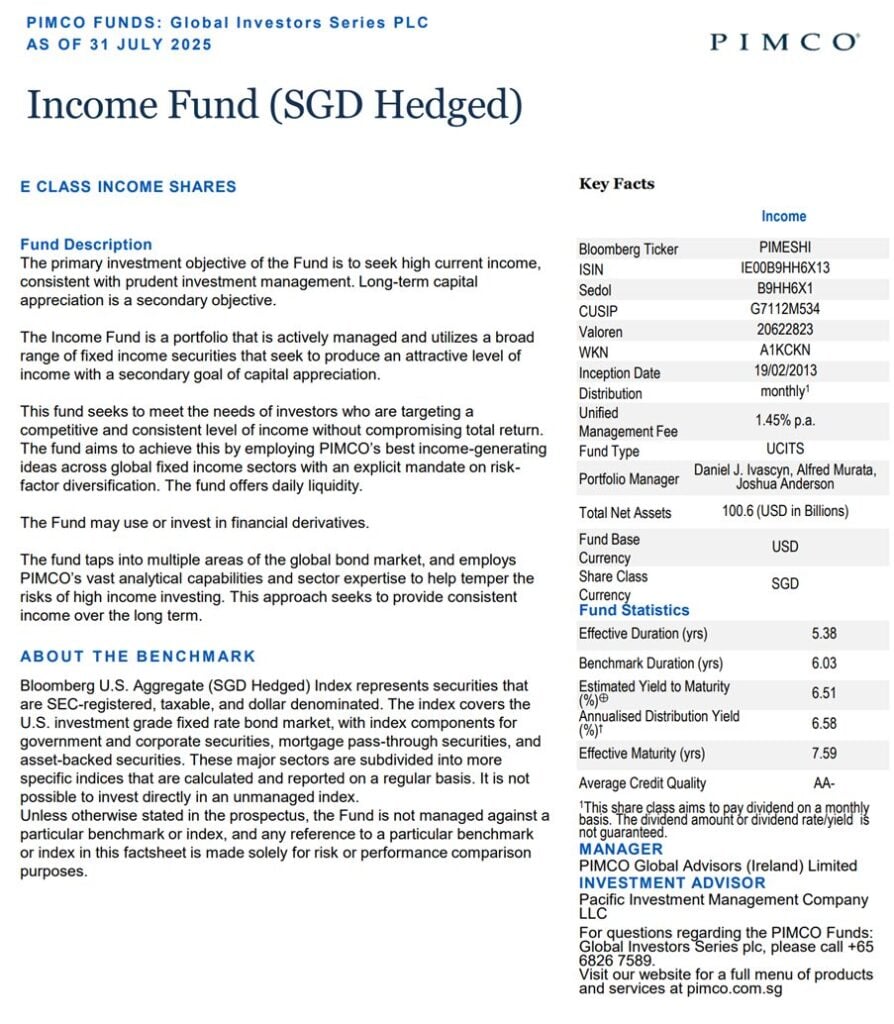

PIMCO GIS Income Fund via Maribank

For more duration, you can consider buying a bond fund.

One example is the PIMCO GIS Income Fund, that you can access via Maribank.

I wrote a detailed review so do check it out if you are keen.

Bottom line is that these bond funds are quite a complex instrument, and not for everyone.

Because if interest rates go up, you can suffer mark to market capital losses.

And there is no way to hold to maturity as the bond fund will automatically reinvest proceeds.

So effectively there is some timing element involved here, in that you want to buy the fund when yields are high, and sell when yields are low, and if you do it the other way around you could see mark to market capital losses.

Best used only if you have a mid to longer term investment horizon.

But that being said.

The thought process here is similar to REITs.

If you are comfortable with some risk of capital loss.

Then you can get a 5%ish yield on something like the PIMCO GIS Income Fund today. That’s worth considering.

Where would I put my cash today?

Personally I haven’t really touched fixed deposits or T-Bills in a while, and after today’s article I don’t really see much that would lead me to change my mind.

Most of the cash that I want in low risk instruments – I’m parking in money market funds, or UOB One (or Singapore Savings Bonds purchased previously at 3%+ yields).

Recently, I’ve actually been adding some REITs as well.

Yes I know that it’s not risk free so not a pure replacement for cash, but the way I see it, as long as I have enough liquid cash set aside, I don’t mind taking on a bit more risk and duration with the rest of the funds, for a higher yield.

But that’s just me – and I would love to hear what you guys think!

Where are you parking your cash for yield today?

Estimated yield on the next 6-month T-Bills auction? (11 Sep 2025 Auction)

The next 6-month T-Bills auction is on 11 Sep 2025 (Thurs).

This means that the deadline to apply is:

- 9pm on 10 Sep (Wed) for cash applications (and CPF-OA applications via DBS or OCBC internet banking)

- 9pm on 9 Sep (Tues) for UOB CPF-OA applications